The will vs. trust decision sits at the heart of this problem. These two instruments work differently, activate at different times, and serve different purposes. The choice between them — or a combination of both — shapes how quickly your heirs receive assets, how much of the process becomes public, and how much control you retain over distribution after you are gone.

In India, this decision is governed by the Indian Succession Act 1925, the Hindu Succession Act 1956, and the Indian Trusts Act 1882. Understanding which legal framework applies to your situation is the starting point for any serious estate plan.

Key Takeaways

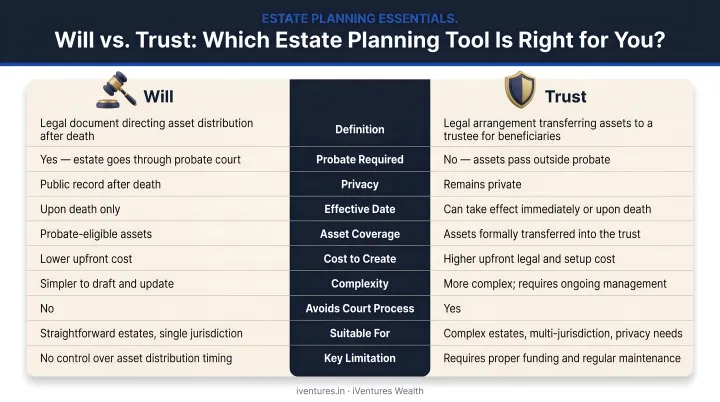

- A will takes effect only after death and may require probate; a trust can operate during your lifetime and continues after death

- Trust assets bypass probate, enabling faster and private wealth transfer

- Wills are simpler and less expensive to create; trusts offer greater control but involve higher setup and administration costs

- Kotak Private's 2024 TOP Report found 89% of Ultra-HNIs have wills, yet only 17% hold private trusts

- That gap becomes increasingly costly as estate complexity grows

- Most affluent families benefit from using both instruments together

Will vs. Trust: Quick Comparison

Both instruments serve estate planning goals — but they work differently, activate at different times, and carry distinct cost and privacy implications. Here's how they compare at a glance:

| Feature | Will | Trust |

|---|---|---|

| When it activates | Only upon death | Upon creation and funding; continues after death |

| Probate | May require probate proceedings (mandatory in certain Indian jurisdictions for immovable property) | Assets in trust bypass probate entirely |

| Privacy | Becomes public record once filed for probate | Remains private; not accessible through public records |

| Setup cost | Lower upfront cost; simpler to draft | Higher drafting and administration costs |

| Distribution control | Single transfer at death; no ongoing conditions | Conditional and staged distributions (age-based, milestone-based) |

| Incapacity planning | No coverage during lifetime | Can manage assets if the grantor becomes incapacitated |

What Is a Will?

A will (formally, a Last Will and Testament) is a legal document specifying how a person's assets and affairs should be handled after death. In India, wills for non-Muslims are governed by the Indian Succession Act 1925. Hindus, Buddhists, Sikhs, and Jains can also dispose of property by will under Section 30 of the Hindu Succession Act 1956.

What a Will Allows You to Do

- Name beneficiaries for property and financial assets

- Appoint an executor to carry out your wishes

- Designate guardians for minor children — a function no other instrument replaces

- Leave specific gifts or charitable bequests

For a valid unprivileged will, the Indian Succession Act requires the testator to be of sound mind and not a minor, with the will signed and attested by two or more witnesses. Registration is optional under Section 18(e) of the Registration Act 1908, though registering a will adds an evidentiary layer of protection.

What a Will Cannot Do

A will has real limitations that catch many families off guard:

- No legal force during your lifetime — it activates only at death

- Does not override nominee designations — life insurance policies, EPF, and PPF accounts follow their own product-specific rules; the Supreme Court has confirmed in Shakti Yezdani v. Jayanand Salgaonkar that nomination for securities does not create a new line of succession

- Does not cover jointly held assets, which pass automatically to co-owners

- Does not govern assets already placed in a trust

One area of active change is probate. The Repealing and Amending Act 2025 removed Section 213 of the Indian Succession Act, which had previously made probate mandatory in certain jurisdictions — so the legal landscape here is shifting.

What hasn't changed: contested wills or complex estates can still result in extended court proceedings. Specific advice from a qualified practitioner remains essential.

When a Will Makes Sense

A will is the right foundation for anyone with a relatively straightforward estate — a primary residence, standard financial accounts, a clear family structure.

It is especially critical for parents of minor children. Without a formally appointed guardian, Indian courts will make that decision for you. Dying intestate (without a will) means your assets are distributed according to succession laws, which may not reflect your intentions at all.

What Is a Trust?

A trust is a legal arrangement where a person (the settlor or grantor) transfers ownership of assets to a trustee, who manages and distributes them for the benefit of named beneficiaries. In India, private trusts are governed by the Indian Trusts Act 1882. The Act defines trust, trustee, beneficiary, and trust property, and sets out the conditions for valid creation under Sections 5 to 8.

Types of Trusts Relevant to Indian Estate Planning

Revocable trusts allow the grantor to retain control and modify or dissolve the trust during their lifetime. Income from a revocable transfer continues to be taxed in the grantor's hands under Section 61 of the Income Tax Act.

Irrevocable trusts involve a permanent transfer of assets. Once settled, the grantor relinquishes direct control — the trade-off being tax efficiency and creditor protection. Section 47(iii) of the Income Tax Act excludes transfers under irrevocable trusts from taxable transfer treatment, subject to statutory conditions.

Private family trusts are the most commonly used structure among HNIs and UHNIs in India for multi-generational wealth transfer. These can hold a range of assets — financial securities, immovable property (via a registered trust deed), and business interests — subject to asset-specific legal requirements.

One important technical point: a trust can only govern assets formally transferred into it. Immovable property requires a registered non-testamentary instrument or a will for the transfer to be valid. Simply drafting a trust deed without actually settling assets into it leaves those assets outside the trust's protection.

Key Advantages Over a Will

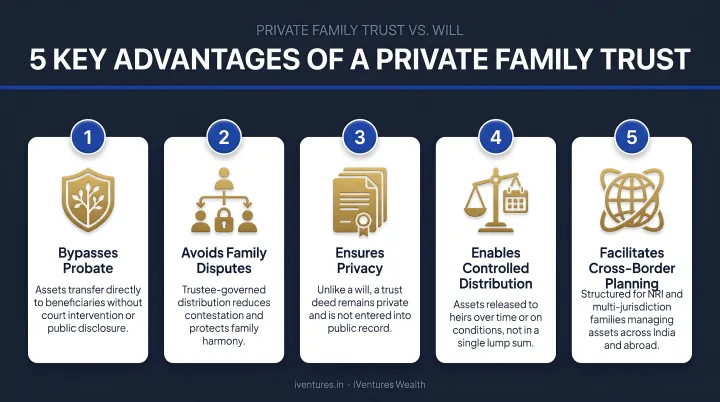

- Probate avoidance — assets already held in trust bypass estate proceedings entirely, because they are not the testator's personal property at the time of death

- Privacy — trust administration does not go through court, so asset details, beneficiary names, and distribution terms stay out of public records

- Conditional distribution — trustees can release funds upon reaching a certain age, completing education, or achieving other milestones

- Incapacity protection — the trust continues to function and manage assets if the settlor becomes incapacitated, something a will cannot do

- Governance for complex situations — families with special-needs dependents, financially inexperienced heirs, or blended family structures can build specific rules into the trust deed

Costs and Administration

Trusts involve more detailed legal drafting, ongoing administrative obligations, and — where a professional or corporate trustee is engaged — recurring management fees. Stamp duty for immovable property transfers into trust varies by state. Setup costs vary by asset type, state law, trustee model, and distribution complexity — no single national benchmark applies.

When a Trust Makes Sense

A trust becomes particularly valuable when the estate is large or structurally complex:

- Multiple properties across states

- Business interests or promoter shareholdings (note that transfers of listed company shares into family trusts require careful analysis under the SEBI Takeover Code)

- Assets held across jurisdictions for NRI/OCI families

- Beneficiaries who are minors, have special needs, or are not yet equipped to manage significant assets

- Family offices seeking formal governance structures for multi-generational wealth

These are exactly the scenarios where trust advisory becomes central to a family's overall wealth plan — not a one-time legal exercise, but an ongoing governance structure.

At iVentures Wealth, trust advisory is a core component of the family office service framework. The firm has structured private trusts for clients including parents of special-needs children, business owners with NRI beneficiaries, and founders who needed a formal structure to protect and govern the corpus after a significant liquidity event. In each case, what began as a wealth transfer question became a documented, tax-efficient plan built to outlast the founder.

Will vs. Trust: Which Is the Right Choice?

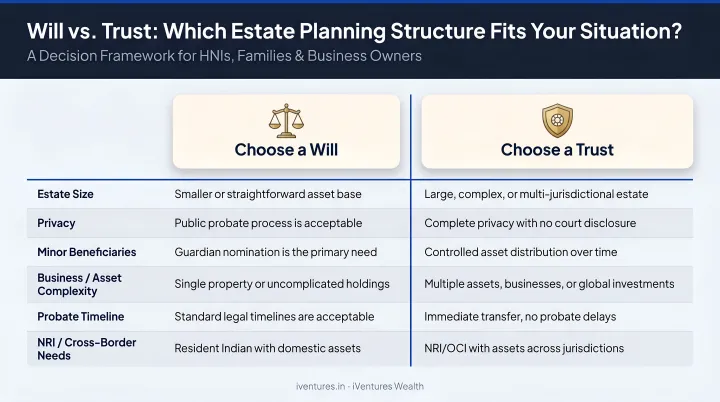

There is no universal answer. The right choice depends on several factors that vary significantly from one family to the next.

Primary Decision Factors

| Factor | Points Toward a Will | Points Toward a Trust |

|---|---|---|

| Estate complexity | Simple, consolidated | Large, multi-asset, multi-state |

| Probate preference | Acceptable | Prefer to avoid |

| Privacy needs | Less critical | High priority |

| Family structure | Clear, nuclear | Blended, special needs, or multiple generations |

| Business ownership | None or minimal | Significant promoter stake |

| NRI/OCI involvement | None | Assets or beneficiaries across jurisdictions |

| Budget | Limited | Higher upfront cost acceptable |

Using Both Together

Many UHNIs and affluent families benefit most from a combined strategy. A private family trust holds core wealth — business interests, significant properties, financial portfolios — while a will acts as a catch-all for assets not formally transferred into the trust and handles personal directives like guardian appointments.

This structure ensures nothing is unaccounted for. Assets that fall outside the trust at the time of death are still governed by the will, rather than defaulting to intestacy laws. According to a 2024 Mint report, 84.8% of Indian households have no will at all — meaning most families are not starting from a will-and-trust strategy, but from nothing.

A Note on Common Mistakes

In iVentures Wealth's advisory experience, the most frequent errors among affluent families include:

- Nominees are custodians, not heirs — actual succession follows the will or applicable law, regardless of nomination

- A trust deed without proper asset settlement offers no probate protection; unfunded trusts are a common and costly oversight

- Estate plans left unchanged after major life events — divorce, business exits, new residency — can create exactly the disputes they were designed to prevent

For individuals managing significant or multi-generational wealth, the will vs. trust decision should be part of a broader estate and legacy planning strategy — not a standalone choice made in isolation.

iVentures Wealth's family office advisory services help UHNIs, founders, and affluent families structure estate plans aligned with their overall wealth goals. This includes coordinating with qualified legal practitioners on will drafting, guiding private trust establishment, supporting cross-border succession coordination, and integrating lifetime gifting strategies into the wider financial plan.

Conclusion

Neither a will nor a trust is universally superior. Wills are a necessary foundation for everyone — simple, legally sound, and essential for personal directives that no other instrument can replicate. Trusts offer control, privacy, and probate avoidance that become increasingly valuable as the size and complexity of an estate grows.

Estate planning is not a one-time event. Family circumstances change, assets grow and shift, and India's succession laws — from the Indian Succession Act to state-level stamp duty norms for trusts — continue to evolve. Treating an estate plan as a fixed document rather than a living strategy is itself a common and costly mistake.

If your estate has reached a scale where the will vs. trust question genuinely matters, the structure you put in place today determines not just what your family inherits, but the tax efficiency, privacy, and continuity with which they receive it. iVentures Wealth works with HNIs, UHNIs, and family offices on succession structuring and estate advisory — coordinating with legal counsel to build plans that hold up as wealth and family dynamics evolve. Reach out to start that conversation.

Frequently Asked Questions

What is better — a will or a trust?

Neither is universally better. Wills are simpler, less expensive, and essential for every adult with assets or dependents. Trusts offer greater control, privacy, and probate avoidance, making them better suited to larger or more complex estates. The most comprehensive approach for affluent families typically uses both.

Does a trust override a will?

A trust and a will operate independently. Assets placed in a trust are governed by the trust deed and fall outside the testator's personal estate, so the will cannot dispose of them. The will governs only assets that remain outside the trust. They complement rather than override each other.

Can I have both a will and a trust?

Yes, and for most affluent families this is the recommended approach. A trust manages core assets and avoids probate, while a will covers remaining assets and personal directives, including guardian appointments for minor children, which only a will can handle.

What assets cannot be covered by a will in India?

Assets with nominee designations (life insurance, EPF, PPF), jointly held property that passes automatically to co-owners, and assets already settled into a trust fall outside the scope of a will. Each is governed by its own legal mechanism regardless of what the will states.

What is the main disadvantage of a trust?

The primary drawback is cost and complexity: initial drafting and ongoing administration are more demanding than a will. For irrevocable trusts specifically, the grantor permanently relinquishes direct control over transferred assets, which requires careful consideration before committing.

Do NRIs in India need a will, a trust, or both for their Indian assets?

NRIs with immovable property in India are subject to Indian succession law under Section 5 of the Indian Succession Act, making an India-specific will important for those assets. A private family trust can also be structured to manage and transfer holdings across jurisdictions, though FEMA compliance and cross-border tax implications require asset-by-asset analysis.