This guide covers everything NRIs need to know about ULIPs in 2026 — who's eligible, which plans are worth evaluating, the tax position, how to actually invest, and the factors that matter most before committing capital.

Key Takeaways

- NRIs and OCIs can invest in Indian ULIPs under FEMA and IRDAI regulations

- ULIP premiums qualify for a ₹1.5 lakh deduction under Section 80C (old tax regime only)

- Maturity proceeds may be tax-exempt under Section 10(10D), subject to the ₹2.5 lakh annual premium cap (Finance Bill 2021)

- NRE or NRO accounts are both accepted for premium payments; proceeds from NRE-funded policies are freely repatriable

- US and Canada-based NRIs face FATCA/FBAR obligations — consult a cross-border adviser before investing

Can NRIs Invest in ULIP Plans in India?

Who Qualifies as an NRI

Under Section 2(30) of the Income Tax Act, a non-resident is a person who is not resident in India. Residency is determined under Section 6 — anyone who spends fewer than 182 days in India in a financial year is treated as a non-resident.

OCI (Overseas Citizen of India) cardholders, registered under Section 7A of the Citizenship Act 1955, are generally treated at par with NRIs for economic purposes, though they are not Indian citizens. Both NRIs and OCIs are eligible to invest in Indian ULIP plans.

Tax residency, OCI legal status, FEMA account type, and insurer underwriting are each separate questions — meeting the NRI definition doesn't automatically mean any particular insurer will issue a policy.

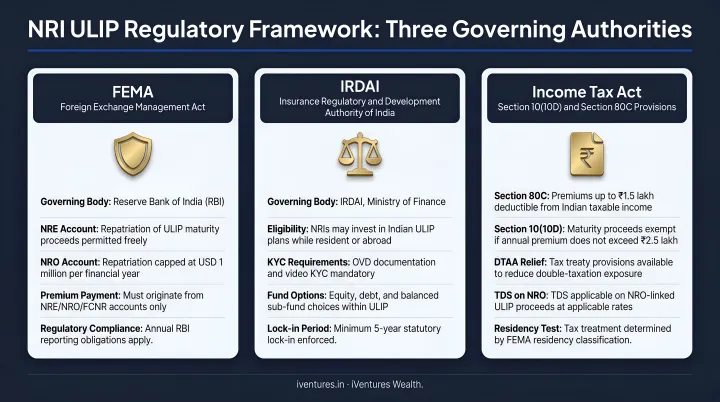

The Regulatory Framework

NRI ULIP investments are jointly regulated by three authorities:

- FEMA and RBI govern how premiums flow in and proceeds flow out

- IRDAI sets product rules, charge caps, and lock-in requirements

- Income Tax Act governs deductions and exemptions on premiums and payouts

Premiums must be paid from an NRE (Non-Resident External), NRO (Non-Resident Ordinary), or FCNR account, or via direct inward remittance from a foreign bank. Insurers will require KYC documentation and AML compliance before issuing a policy. According to RBI guidelines, NRO account remittances abroad are generally capped at USD 1 million per financial year, while NRE and FCNR account balances are treated as freely repatriable.

The US and Canada Caveat

The rules above apply broadly — but for NRIs residing in the US or Canada, there's an additional layer to account for. Under FATCA (Foreign Account Tax Compliance Act), Indian insurers that have signed inter-governmental agreements — HDFC Life, Axis Max Life, ICICI Prudential, and others — collect FTIN and self-certification data and report it through Indian tax authorities to the IRS.

Beyond reporting, US-based NRIs should be aware that FinCEN's FBAR rules require reporting of foreign financial accounts when the aggregate value exceeds $10,000 at any point during the calendar year. IRS Form 8938 may apply to specified foreign financial assets above applicable thresholds. These obligations don't necessarily prohibit ULIP investment, but they do create compliance requirements that should be evaluated before committing.

No major insurer publicly states a blanket refusal to issue policies to US or Canada residents — but product-specific acceptance varies. Confirm directly with the insurer before applying.

Top ULIP Plans for NRIs in India 2026

Comparative Overview

The table below covers leading ULIP plans based on officially verified insurer brochures. Where exact minimum premiums for specific modes were not confirmed from official sources, the most conservative verified figure is shown.

| Plan | Insurer | Min. Annual Premium | Entry Age | Lock-in | Key Feature |

|---|---|---|---|---|---|

| Click 2 Wealth | HDFC Life | ₹12,000 | 30 days – 60 yrs | 5 years | 18 fund options, unlimited free switches, nil allocation/admin charges, return of mortality charges |

| Platinum Wealth Plan | Axis Max Life | ₹1,00,000 | Verify in brochure | 5 years | Premium-segment ULIP, high minimum threshold, wealth booster features |

| ICICI Pru Signature | ICICI Prudential | ₹5,00,000 | 0 – 41 yrs (verify) | 5 years | Premium-segment ULIP with comprehensive fund menu |

| LifeTime Classic | ICICI Prudential | Verify in brochure | Verify in brochure | 5 years | ULIP with top-up facility, ₹2,000 minimum top-up |

| Wealth Infinia | Aditya Birla Sun Life | ₹5,00,000 (single pay) | Verify in brochure | 5 years | 5 investment strategies, 19 fund options, returns policy charges |

| Goal Assure IV | Bajaj Allianz Life | Verify in brochure | Verify in brochure | 5 years | Unit-linked savings plan (policy doc version 032026) |

| eWealth Plus | SBI Life | Verify in brochure | Verify in brochure | 5 years | Individual unit-linked non-participating life savings product |

| Kotak T.U.L.I.P | Kotak Life | ₹1,00,000 | 18 – 60 yrs | 5 years | Term with unit-linked insurance plan structure |

Important note: "Verify in brochure" entries reflect cases where the research retrieved official documents but exact figures weren't fully extracted. Always confirm current data directly from the insurer's latest brochure before applying.

Equity-Oriented Plans (10+ Year Horizon)

For NRIs with higher risk tolerance and long investment horizons, equity-oriented allocations within ULIPs have historically delivered stronger returns — though market risk applies throughout.

- HDFC Life Click 2 Wealth offers Blue Chip, Flexi Cap, Midcap Momentum, and index fund options, with FMC up to 1.35% p.a. The nil charge structure and unlimited free switches keep costs competitive over long tenures.

- ICICI Pru Signature targets premium investors (₹5 lakh minimum) with a broad equity fund menu suited to concentrated equity positions.

- ABSLI Wealth Infinia provides 19 fund options across five investment strategies, with the added benefit of policy charge returns.

HNI and UHNI-Focused Plans

For high-ticket NRI investors, two plans are designed specifically around larger premium bands:

- Axis Max Life Platinum Wealth Plan starts at ₹1 lakh (limited/regular pay) and is built around wealth booster features — making it a natural fit for UHNI clients prioritising structured accumulation

- ICICI Pru Signature, with its ₹5 lakh entry point, delivers a wider fund menu and charge structures that improve materially as premium size increases

At higher premium bands, charge structures often become more favourable. The IRDAI-mandated "Benefit Illustration" document is the clearest way to compare projected net returns across plans — which is precisely why no ULIP can be labelled as delivering the "highest returns."

Returns depend entirely on the fund type selected, investment tenure, market conditions, and charges deducted. Evaluate plans against your personal financial goals and risk profile, not rankings.

Tax Benefits of ULIPs for NRIs

Section 80C Deductions

NRIs are entitled to the same Section 80C deduction as resident Indians — up to ₹1.5 lakh per annum on ULIP premiums, provided the annual premium doesn't exceed 10% of the sum assured (for policies issued on or after 1 April 2012; older policies used a 20% cap). This deduction is available only under the old tax regime and not under the new default regime.

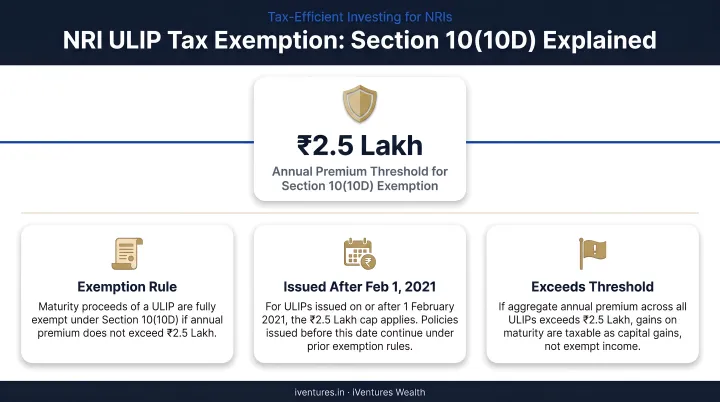

Section 10(10D) Exemption

- Death benefit: Always fully tax-free for the nominee, regardless of premium amount

- Maturity proceeds: Tax-exempt if annual premium doesn't exceed 10% of sum assured

One threshold matters above all others: for ULIPs issued on or after 1 February 2021, if aggregate annual premiums across all ULIPs exceed ₹2.5 lakh, maturity gains become taxable as capital gains. This rule was introduced by Finance Bill 2021 — not Budget 2023 as some sources incorrectly state. No verified Budget 2024 or 2025 change to this threshold was found.

TDS for NRIs

Resident life-insurance payouts fall under Section 194DA (2% TDS). For NRIs, payouts fall under Section 195 at "rates in force" — there is no single flat TDS rate. The rate depends on whether the payout is taxable, the nature of the income, applicable surcharge and cess, and any DTAA relief available.

NRIs can apply for a lower or nil TDS deduction certificate using Form 13 if their income falls within exempt limits.

DTAA Considerations by Country

India has DTAA agreements with over 80 countries. How this applies to ULIP proceeds varies:

| Country | DTAA Status | Practical Impact |

|---|---|---|

| UAE | DTAA exists | UAE has no personal income tax, so DTAA is less practically relevant for most NRIs |

| USA | DTAA with India applies | Treaty relief may be available; FATCA/FBAR reporting obligations add compliance layer |

| UK | Comprehensive DTAA with India | Treaty relief may apply to taxable proceeds; consult a cross-border specialist |

For NRIs in the US and UK, a cross-border tax adviser — not just an Indian CA — is essential to correctly navigate the interaction between Indian TDS and foreign filing obligations. iVentures Wealth supports NRI clients across the US, UK, UAE, and Singapore with DTAA planning, TDS optimization, and coordination with foreign tax filings as part of its NRI wealth management advisory.

Repatriation

How ULIP proceeds can be moved abroad depends on the account from which premiums were paid:

- NRE-funded premiums: Maturity proceeds are freely repatriable, subject to FEMA documentation and tax clearance

- NRO-funded premiums: Subject to the annual RBI cap of USD 1 million per financial year

Tax must be settled before repatriation, and the insurer and your bank will require documentary evidence of the source of funds.

How NRIs Can Invest in a ULIP Plan in India

Documents Required

Most insurers require the following from NRI applicants:

- Valid passport (identity and age proof)

- Recent passport-size photographs

- Overseas address proof

- Indian address proof (if applicable)

- Income proof

- PAN card (or Form 60 if PAN not held)

- OCI/PIO card, if applicable

- FATCA self-certification form

Specific requirements vary by insurer — some may request additional KYC or AML documentation, particularly for high-premium plans.

Modes of Premium Payment

NRIs can pay ULIP premiums through:

- Net banking from NRE or NRO accounts

- Inward remittance from a foreign bank account via SWIFT transfer

- Debit or credit cards issued abroad (subject to individual insurer acceptance)

- Cheques or demand drafts drawn on NRE/NRO accounts

Premiums paid via NRE or FCNR accounts are the most straightforward route as they establish a clear, repatriable source trail for maturity proceeds.

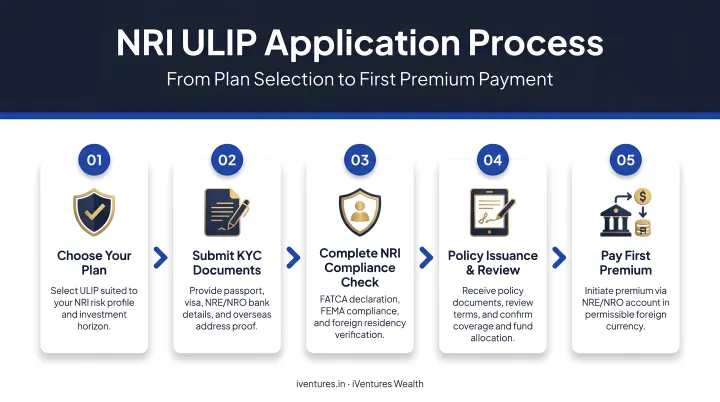

Step-by-Step Application Process

- Choose a plan aligned with your investment horizon, risk appetite, and premium capacity

- Complete the proposal form, which most major insurers now offer online

- Submit KYC documents including FATCA self-certification

- Undergo medical underwriting if required based on age or sum assured level

- Remit the first premium via NRE/NRO account or inward remittance

NRIs looking to structure a ULIP within a broader cross-border financial plan can work with iVentures Wealth, a SEBI-registered investment adviser with NRI/OCI advisory expertise, to evaluate options, navigate DTAA implications, and coordinate with tax advisers across jurisdictions.

Key Factors NRIs Should Consider Before Choosing a ULIP

Fund Options and Switching Flexibility

Evaluate the range of equity, debt, and hybrid funds available. Free (or low-cost) switching matters — life changes, and so does risk appetite. NRIs with a 10+ year horizon may lean heavily toward equity initially, but should have a clear pathway to gradually shift toward debt funds as the policy matures and retirement approaches.

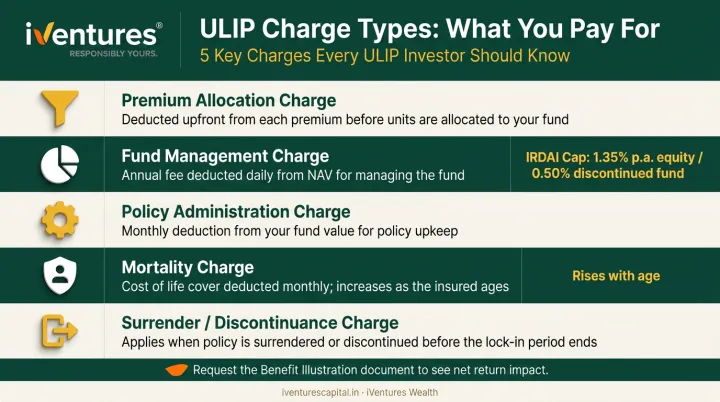

Charge Structure Transparency

ULIP charges directly erode returns. Know what you're paying:

- Premium allocation charge — deducted upfront from each premium

- Fund management charge (FMC) — capped by IRDAI at 1.35% p.a. for equity funds, 0.50% for discontinued policy funds

- Policy administration charge — monthly deduction from fund value

- Mortality charge — cost of life cover, increases with age

- Surrender/discontinuance charge — applies if you exit early

Ask for the Benefit Illustration document — it compares projected returns at standardised assumed growth rates and is the clearest way to see the impact of charges on net returns.

Lock-in Period and Liquidity

All ULIPs carry a mandatory 5-year lock-in under IRDAI rules — no partial withdrawals or full surrender before the end of the fifth year. NRIs should assess whether they can sustain premium payments from abroad for at least five years. After the lock-in, partial withdrawals are permitted subject to insurer-specific minimum unit clauses.

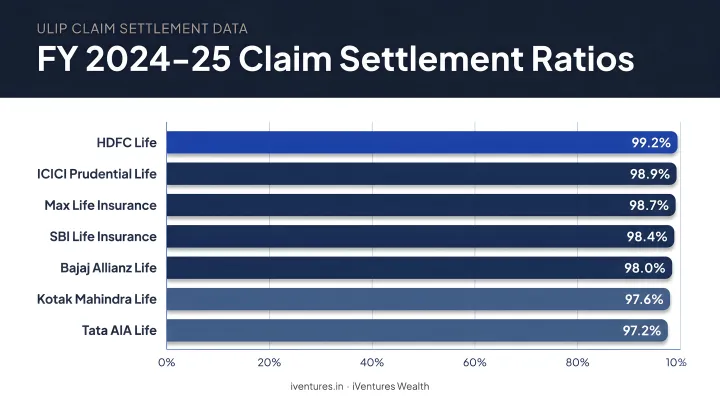

Insurer Claim Settlement Ratios

According to the IRDAI Annual Report 2024-25, all seven major insurers covered in this article settled over 98% of claims by number of policies:

| Insurer | Claim Settlement Ratio (FY 2024-25) |

|---|---|

| Max Life Insurance | 99.51% |

| HDFC Life Insurance | 99.07% |

| Bajaj Allianz Life | 99.04% |

| SBI Life Insurance | 98.90% |

| Kotak Mahindra Life | 98.82% |

| ICICI Prudential Life | 98.75% |

| Aditya Birla Sun Life | 98.20% |

For NRI families where nominees are in India while the insured is abroad, a high claim settlement ratio carries real practical weight.

Fit Within a Broader Cross-Border Plan

A ULIP shouldn't be evaluated in isolation. For NRIs, it must sit within a plan that addresses:

- Currency risk — INR-denominated returns versus the NRI's home currency purchasing power

- Estate planning — nominee designations across Indian and foreign jurisdictions

- Portfolio diversification — avoiding duplication with mutual funds, PMS, or other India-linked equity exposure

This is where a fiduciary adviser adds real value. iVentures Wealth's NRI wealth management service covers estate planning coordination, nominee alignment across jurisdictions, and cross-border tax structuring — so any ULIP fits within the broader portfolio rather than duplicating it.

Frequently Asked Questions

Which ULIP plan gives the highest returns for NRIs?

No ULIP guarantees the highest returns — outcomes depend on the fund type (equity vs. debt), tenure, market conditions, and the plan's charge structure. Compare equity-oriented plans from HDFC Life, ICICI Prudential, and ABSLI by evaluating 5- and 10-year fund performance relative to benchmark indices, not headline plan rankings.

Are ULIP returns tax-free for NRIs?

Maturity proceeds may be exempt under Section 10(10D) if annual premiums don't exceed 10% of the sum assured. For ULIPs issued on or after 1 February 2021, aggregate premiums above ₹2.5 lakh make gains taxable as capital gains. NRIs must also factor in their country of residence's tax rules and applicable DTAA provisions.

Is a ULIP a good investment for NRIs?

ULIPs can work well for NRIs who want life cover and market-linked returns within a single, tax-efficient structure. They're most suitable for those with a 7–10+ year horizon who don't need high liquidity. NRIs from the US or Canada should weigh FATCA-related compliance obligations carefully before proceeding.

Can NRIs from the US or Canada invest in Indian ULIPs?

US and Canada-based NRIs often face practical hurdles, as many Indian insurers are cautious about issuing policies due to FATCA and FBAR compliance obligations. No insurer publicly states a blanket refusal, but product-specific acceptance must be confirmed directly with the insurer. A cross-border tax adviser is essential before applying.

Can NRI ULIP maturity proceeds be repatriated abroad?

Yes, generally. Proceeds from NRE-funded premiums are freely repatriable after tax clearance, while NRO-funded proceeds are subject to the RBI's annual cap of USD 1 million per financial year. Both the insurer and the bank require documentary evidence of the source of funds.

What is the lock-in period for ULIPs for NRIs?

The lock-in is 5 years for all investors, including NRIs — this is an IRDAI mandate, not a resident-only rule. No partial withdrawals or full surrender are permitted before the fifth year ends. After the lock-in, partial withdrawals are allowed under insurer-specific terms, though staying invested longer typically improves returns.