Add to this the absence of any employer pension for most private practitioners, high early-career expenses, and medical inflation that Milliman estimates at 12–13% annually — and you have a genuinely different retirement planning problem.

This article covers what that problem actually looks like, how to size the right corpus, which investment instruments to use, how to reduce your tax burden, and when to get structured help.

Key Takeaways

- Physicians start earning a decade later, compressing the compounding window by 8–10 years compared to most other professions

- Private practitioners have no pension safety net — the entire retirement burden is self-funded

- India's safe withdrawal rate is closer to 3%, not the commonly cited 4%

- NPS, PPF, ELSS, and equity mutual funds must be allocated deliberately — each instrument solves a different retirement problem

- Tax deductions worth over ₹2.75 lakh per year are available but frequently underused

- Build a liquid buffer covering 12–24 months of expenses before stepping away from practice

Why Indian Physicians Face Unique Retirement Planning Challenges

The Delayed Start Problem

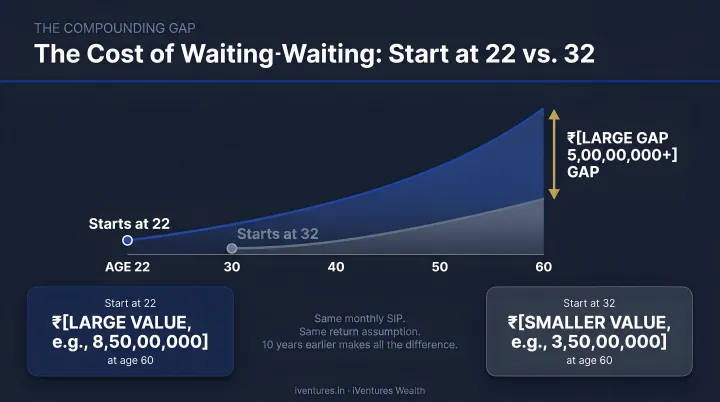

Most professionals begin earning in their early 20s. A physician completing MBBS (4.5 years + 1 year internship), MD/MS (3 years), and an optional DM/MCh (3 years) doesn't reach sustained income until 32–35 at the earliest. That's roughly 10 years of lost compounding.

Consider: ₹10,000 invested monthly from age 22 versus age 32, growing at 12% CAGR, produces a corpus difference of approximately ₹3.5 crore by age 60. That's not a marginal difference — it's a decade of compounding that can't be recovered simply by investing more later.

No Pension for Private Practitioners

Government doctors employed before 2004 benefit from the Old Pension Scheme. Those recruited after fall under mandatory NPS. But private practitioners, clinic owners, and hospital consultants get neither. The entire retirement burden falls on the individual physician — funded solely from practice income.

That absence of any institutional safety net makes the savings behavior in the early career years especially consequential.

First-Decade Cash Flow Compression

The first 10 years of practice are typically the worst for retirement savings — not because income is low, but because:

- Education loan repayments consume significant monthly cash flow

- Housing loans coincide with career establishment

- Children's school fees and social commitments add pressure

- Clinic or practice setup costs often require capital deployment

Most physicians reach their 40s with strong earnings and little to show for it in long-term savings — not due to poor intent, but structural timing.

Medical Inflation Is Not General Inflation

According to Milliman's research on Indian medical trends, India's medical trend reached 12% in 2024 and is projected at 13% for 2025. MoSPI's CPI Health data puts official health inflation at 3.6–3.8% — but actuaries note this figure doesn't capture insurer-facing treatment costs, utilisation intensity, or procedure-cost increases.

For retirement planning purposes, a conservative medical cost escalation assumption of 10–12% is more realistic than the headline CPI figure suggests.

Burnout and the Early Retirement Trap

A 2025 JAPI study found that 46.1% of Indian healthcare practitioners reported moderate to high personal burnout. Many physicians want to exit practice earlier than planned — but financially can't. The desire for early retirement runs directly into the reality of an underfunded corpus, which forces continued practice beyond what physicians consider sustainable.

How Much Retirement Corpus Do Indian Physicians Actually Need?

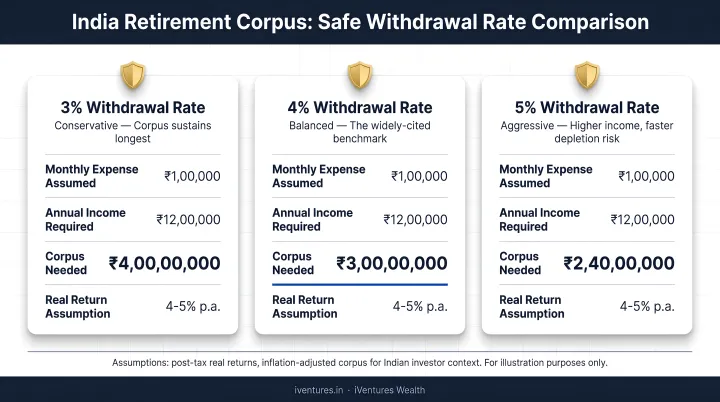

The 25x Rule — Adjusted for India

The popular 25x annual expense rule (derived from a 4% safe withdrawal rate) was developed for US market conditions. Research published on SSRN by Ravi Saraogi specifically examining India's safe withdrawal rate concludes that a 3% withdrawal rate is appropriate for the average Indian investor, with conservative investors capped at 2.6%. This implies a 33x annual expense multiplier, not 25x.

Illustrative example:

A physician targeting ₹15 lakh in annual retirement expenses (today's money) needs:

| SWR Assumption | Corpus Required (today's money) |

|---|---|

| 4% (US-standard) | ₹3.75 crore |

| 3% (India-appropriate) | ₹5 crore |

| 2.6% (conservative) | ₹5.77 crore |

Add inflation-adjusted growth over 20–25 years before retirement, plus a separate healthcare expense buffer, and the real number climbs well beyond ₹5 crore for most urban physicians.

Income Replacement vs. Expense Replacement

A common planning error: physicians try to replace their peak practice income in retirement. The actual target is considerably smaller — post-tax, post-EMI, post-savings living expenses.

Once practice-related costs, loan repayments, and children's education are no longer part of the picture, the annual retirement expense figure may be 40–50% lower than current gross income. This changes the corpus target significantly. But you need to calculate your actual number, not assume it.

What typically drops out of the retirement budget:

- Clinic or practice operating costs

- EMIs and loan repayments

- Children's education and dependent expenses

- Active professional insurance premiums

Longevity Risk Is Real

That corpus target also needs to stretch further than most physicians assume. India's SRS 2018–22 data shows remaining life expectancy at age 60 is 18.1 years for the general population. Urban, educated, health-conscious physicians can expect considerably more. A retirement at 60 could mean a 25–30 year drawdown period. Under-saving isn't a recoverable error at age 70.

Best Investment Instruments for Physician Retirement in India

National Pension System (NPS)

NPS Tier I is one of the most tax-efficient retirement vehicles available to self-employed physicians. The deduction structure is:

- Section 80CCD(1): Up to 20% of gross income for self-employed individuals, within the ₹1.5 lakh Section 80CCE cap

- Section 80CCD(1B): Additional ₹50,000 exclusively for NPS contributions, above the 80C ceiling

The Scheme E (equity) portion of NPS has delivered strong long-term returns — 10-year annualised returns across major pension fund managers have ranged from 13.8% to 14.3% (NPS Trust data, July 2023). A physician in their 40s can allocate up to 75% to equities; this should taper toward 50–60% through the 50s as retirement approaches.

The limitation: NPS mandates 40% annuity purchase at maturity, which reduces flexibility. Plan for this in overall portfolio design.

PPF and ELSS Mutual Funds

PPF suits the conservative, guaranteed-return component of a physician's portfolio:

- Annual contribution limit: ₹1.5 lakh

- EEE tax status — contributions, returns, and maturity are all tax-exempt

- 15-year lock-in, with partial withdrawal allowed after year 7

- Best used as a stable fixed-income counterweight to equity exposure

ELSS mutual funds are the equity alternative within the ₹1.5 lakh Section 80C limit:

- 3-year lock-in (shortest among 80C instruments)

- Market-linked returns with equity growth potential

- Better suited for physicians with a 15+ year horizon who can absorb short-term volatility

Physicians below 45 should lean toward ELSS over PPF within the 80C allocation, unless they specifically need stable debt exposure. Once the 80C bucket is optimised, the next layer of wealth creation typically comes from open-ended equity funds.

Equity Mutual Funds and SIPs

For physicians with a 20–30 year runway, equity mutual funds are the primary wealth-creation engine. The BSE Sensex Total Return Index has delivered:

- 15-year CAGR: 11.16%

- 20-year CAGR: 13.29%

- 25-year CAGR: 14.34%

(Source: BSE Sensex White Paper, January 2026)

Systematic Investment Plans (SIPs) align well with a physician's monthly income pattern. A disciplined ₹1 lakh monthly SIP at 12% CAGR over 25 years produces approximately ₹18.8 crore (before any step-up increases).

Fund category guidance:

- Core allocation: Flexi-cap or large-cap index funds for stability

- Growth kicker: Mid-cap allocation up to 20–25% for physicians under 45

- Simplicity default: A Nifty 50 index fund + Nifty Next 50 combination is a defensible, low-cost foundation

Real Estate

Real estate is a familiar asset class for physicians, though it works best as a supplement rather than the foundation of a retirement portfolio. Key considerations:

- Illiquidity: Unlike mutual funds, real estate can't be partially redeemed during a medical emergency or market opportunity

- Rental yields from Grade A commercial property can reach 8–12%, making it a useful supplementary income stream

- Concentration risk: Many physicians already have practice premises and a residence — adding more real estate compounds single-asset exposure

- REITs and InvITs offer real estate exposure with liquidity, quarterly distributions, and significantly lower entry points than direct property

As a rule of thumb: real estate at 15–20% of net worth adds diversification. Beyond 50%, it concentrates risk in a single illiquid asset class — the opposite of what a retirement portfolio needs.

Tax Optimization Strategies Physicians Shouldn't Ignore

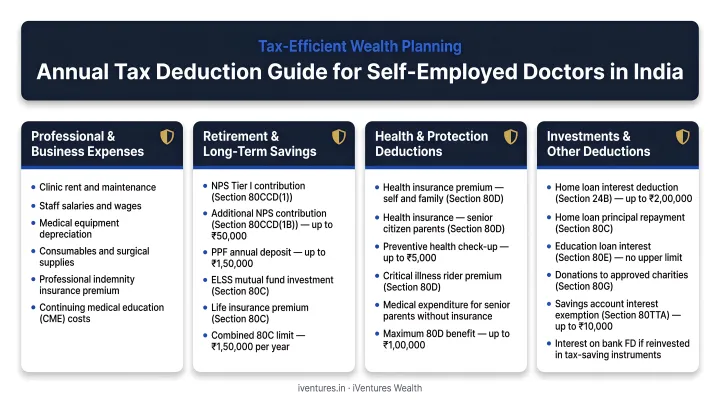

A self-employed physician in the 30% tax bracket can access the following annual deductions:

| Section | Instrument | Maximum Deduction |

|---|---|---|

| 80C | PPF, ELSS, LIC premium | ₹1,50,000 |

| 80CCD(1B) | NPS Tier I | ₹50,000 |

| 80D | Self + spouse + children health insurance | ₹25,000 |

| 80D | Senior citizen parents' health insurance | ₹50,000 |

| Total | ₹2,75,000 |

At the 30% slab, this translates to approximately ₹82,500 in annual tax savings — before any impact on surcharge or cess. Reinvested consistently over 20 years at even a conservative 10% return, that annual saving compounds into a significant corpus — one most physicians never account for in their retirement projections.

LTCG vs. FD: The Tax Efficiency Gap

Where you park those savings matters as much as the savings themselves. Post Budget 2024, long-term capital gains on listed equity above ₹1.25 lakh are taxed at 12.5%. Interest income from fixed deposits is taxed at the physician's full slab rate — 30% for high earners. Choosing equity mutual funds over FDs for long-term accumulation isn't just about returns — the tax differential significantly widens the post-tax gap at higher income levels.

Professional Income Structuring

Self-employed physicians operating as sole proprietors forfeit significant tax efficiencies. Registering as a professional firm or LLP opens up legitimate expense deductions — equipment depreciation, professional subscriptions, staff costs — that reduce taxable professional income directly. iVentures Wealth coordinates with external CAs when advising clients on income structuring, since this intersects tax law and compliance beyond pure investment advisory.

Keeping personal and practice finances structurally separate is the non-negotiable starting point. It's what makes both accurate tax filing and reliable retirement projections possible in the first place.

Planning Your Withdrawal Strategy Before You Retire

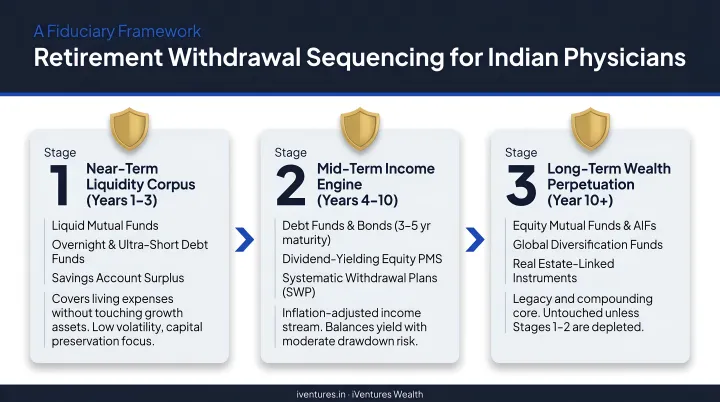

Sequencing Withdrawals for Tax Efficiency

The order in which you draw from retirement accounts directly affects how much you keep. A sensible sequencing approach for most physicians:

- Draw from taxable accounts first — liquid funds, short-duration debt, non-tax-advantaged equity — allowing NPS and PPF to compound longer

- Use NPS lump sum and annuity in the mid-retirement phase; 60% of NPS corpus at maturity is tax-free

- Systematic withdrawals from equity mutual funds in later retirement, benefiting from LTCG treatment at 12.5% above ₹1.25 lakh threshold

The Bridge Income Strategy

Physicians rarely stop overnight. Consulting, teaching, or telemedicine in early retirement (ages 60–65) can generate ₹3–8 lakh annually without full practice commitments. This bridge income reduces pressure on the corpus and allows equity holdings to grow during the critical early-retirement window — the period most vulnerable to sequence-of-returns risk.

That same sequence-of-returns risk makes a cash buffer non-negotiable before you touch your corpus.

Build a Liquid Buffer Before You Retire

Before drawing from your corpus, maintain a separate liquid emergency fund covering 12–24 months of expenses in short-duration debt funds or high-yield savings instruments. If markets fall 30% in your first year of retirement and you have no buffer, you're forced to sell equity at a loss — locking in damage that compounds against you for decades, regardless of how well the rest of your portfolio is structured.

Why Physicians in India Need a Dedicated Wealth Adviser

Physicians are trained to find diagnoses in complex, ambiguous clinical data. That same analytical rigour rarely extends to personal finances — not because of inability, but because time, bandwidth, and domain-specific knowledge are genuinely limited outside medicine.

A SEBI-registered investment adviser who understands the income pattern, tax situation, and compressed retirement timeline specific to medical professionals can build a plan that actually fits. iVentures Wealth has been advising doctors and medical professionals for over two decades, with CFA-led investment research and a fee-only model — meaning advice is never shaped by product commissions.

Dr. Arvind Mehta, an orthopaedic surgeon and healthcare entrepreneur who works with the firm, noted that life-stage planning helped him create separate funds for his daughter's education and retirement, doubling his financial discipline within six months of engagement.

The distinction worth making: SEBI-registered RIAs (Registered Investment Advisers) operate under a fundamentally different incentive structure than most advisers a physician might encounter:

- SEBI RIAs: Legally prohibited from earning distribution commissions — advice is shaped purely by client interest

- Bank relationship managers and mutual fund distributors: Earn commissions on products they recommend — creating an inherent conflict of interest

For a physician whose retirement corpus is their primary financial security, that difference matters considerably.

Frequently Asked Questions

What are the 7 stages of retirement planning?

The broadly recognised stages are: goal setting, financial assessment, investment strategy design, tax planning, corpus accumulation, pre-retirement transition, and drawdown management. For physicians, the accumulation stage begins later and runs shorter — making strategy and tax planning especially critical.

What age do most doctors retire at?

A BMJ Leader 2025 meta-analysis found most physicians retire between ages 60 and 69. In India, many private practitioners continue beyond 65 due to insufficient corpus, while burnout is increasingly pushing physicians to seek earlier exits — often without the financial preparation to support them.

What is the ideal retirement corpus for a doctor in India?

Using India's appropriate 3% safe withdrawal rate, a physician targeting ₹12–15 lakh in annual expenses needs a corpus of ₹4–5 crore in today's money — adjusted upward for medical inflation at 10–12% and a potential 25–30 year drawdown period. Urban physicians with higher lifestyle expenses may need ₹7 crore or more.

Which is better for physicians in India — NPS or equity mutual funds?

Both serve different purposes and work best together. NPS offers superior tax deductions (an extra ₹50,000 under 80CCD(1B)) but locks 40% into annuity at maturity, while equity mutual funds provide full flexibility and higher long-term growth. A combination — NPS for tax efficiency, equity SIPs for wealth creation — is the stronger approach.

Can self-employed doctors in India build their own pension?

Yes. NPS Tier I is open to all Indian citizens regardless of employment type. Combined with PPF for stable accumulation and systematic equity SIPs for growth, self-employed physicians can construct a pension-equivalent income stream without any employer involvement.

How does medical inflation affect retirement planning for Indian physicians?

India's medical inflation runs at 12–13% annually — far above general CPI — meaning healthcare costs in retirement can double every 6–7 years. A dedicated healthcare expense buffer and adequate health insurance coverage are essential, not optional, for any physician's retirement plan.