Introduction

There's a quiet contradiction at the heart of many Indian doctors' financial lives. Years of extraordinary academic discipline. A high income that arrives—finally—after a decade of training. And yet, a surprising number of physicians reach their mid-40s with minimal investable wealth, under-insured practices, and no retirement plan worth the name.

The problem isn't income. It's everything that surrounds it.

A doctor's financial journey differs from virtually every other high-earning profession. Income starts late—often past 30 after completing MBBS, MD/MS, and sometimes a fellowship. By then, peers in other fields have had years of compounding working in their favour.

It also arrives through multiple channels simultaneously: hospital salary, OPD fees, consulting retainers. And it lands squarely in the highest tax bracket from day one, leaving little margin for error.

Generic financial advice—the kind written for a 25-year-old software engineer starting their first SIP—doesn't address any of this.

This article is built for that specific situation. It covers the five pillars that matter most for Indian medical professionals:

- Building a financial foundation suited to a late and multi-source income

- Tax-efficient investing that works within the highest bracket

- Risk management for both income and practice

- Retirement planning that accounts for a compressed savings window

- Estate planning to protect what's been built

Key Takeaways

- A doctor starting SIPs at 32 instead of 25 needs roughly 2.35x the monthly amount to reach the same retirement corpus—making early, structured investing non-negotiable.

- Tax deductions under 80C, 80D, and 80CCD(1B) can collectively reduce taxable income by up to ₹2.75 lakh annually under the old regime.

- Professional indemnity and own-occupation disability insurance are the two most critically underused covers in the medical profession.

- 84.8% of Indian households have no will—a statistic that becomes more costly as wealth accumulates.

- Practice reinvestment is useful, but relying on it alone leaves doctors financially concentrated and exposed.

Why Medical Professionals Need a Specialized Financial Strategy

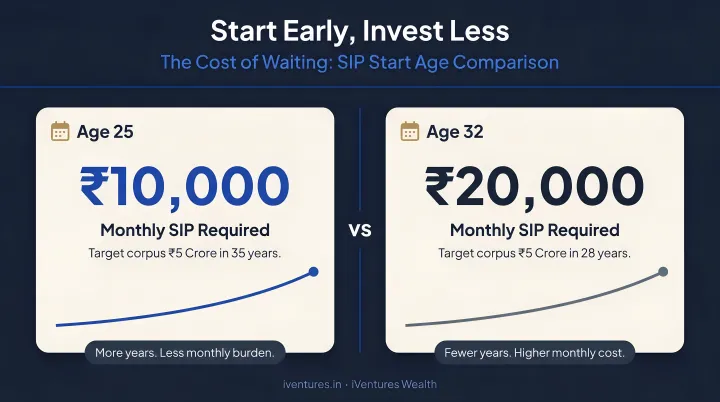

The Delayed Start Problem

Under NMC regulations, MBBS alone takes 4.5 years of academic study plus a compulsory one-year internship. Add a three-year MD/MS postgraduate programme and the arithmetic is stark: a doctor entering MBBS at 18 completes basic postgraduate training at roughly 27–28—before subspecialty fellowships, DM/MCh, or any additional credentials.

Most doctors don't begin earning meaningfully until 30–32.

That gap has a compounding cost that surprises even financially aware physicians. Assuming a 12% annual return and a ₹1 crore target corpus by age 60:

| Start Age | Monthly SIP Required |

|---|---|

| Age 25 | ~₹1,555/month |

| Age 32 | ~₹3,661/month |

A seven-year delay more than doubles the required monthly investment. The later a doctor starts, the harder each rupee has to work — which makes the structure of early income decisions matter more than the amount.

Income Complexity and the Tax Trap

That delayed start also means doctors are playing catch-up precisely when their income structure becomes most complex. Few professions draw from as many simultaneous channels: a fixed hospital salary, private OPD consultation fees, retainers from diagnostic centres, CME honoraria, and medicolegal report fees — each with different tax treatment and documentation requirements.

This complexity creates three common failure modes:

- Underclaimed deductions — income from multiple sources gets consolidated poorly, and legitimate expense claims go undocumented

- GST confusion — while healthcare services are exempt under CBIC Notification No. 12/2017, non-clinical consulting income may attract different treatment; understanding what qualifies is critical

- Cash flow mismatch — monthly expenses run on a hospital salary cycle while private practice income arrives irregularly, making budgeting harder than it appears

The Lifestyle Inflation Trap

Income complexity alone doesn't explain the wealth gap among doctors. The other force at work is behavioural. Years of financial austerity during training create a psychological rebound when income finally arrives, and the social pressure to signal success — through a luxury car, premium housing, or expensive holidays — is real and professionally reinforced in Indian medical culture.

The result: doctors become "income rich but wealth poor" well into their 40s. A 2023 study found that only 34% of Indian healthcare professionals had basic financial literacy and just 12% had invested in products like mutual funds or stocks — a gap that becomes expensive when compounding years are spent on consumption rather than investment.

Tax Planning and Investment Strategies for Doctors

Maximising Deductions Under the Old Tax Regime

The new tax regime is now the default for individuals, but for doctors with significant deductible expenses, the old regime often yields better outcomes. The key is actually using the deductions available:

Section 80C (up to ₹1.5 lakh):

- ELSS mutual funds (recommended over endowment plans or ULIPs)

- Public Provident Fund (PPF)

- Life insurance premiums on pure-term policies

- Education loan principal repayment

Section 80D (up to ₹75,000 in optimal configurations):

- ₹25,000 for self, spouse, and children's health insurance

- ₹25,000 additional for parents' premiums

- Limits increase to ₹50,000 per group if the insured is a senior citizen

Section 80CCD(1B):

- An additional ₹50,000 NPS contribution deduction, completely outside the 80CCE aggregate cap

- Most doctors who haven't opened an NPS account are leaving this benefit entirely unused

Coordinating these three deductions with a CA who understands medical income structures is where the meaningful tax savings actually materialise.

The HUF Advantage

The Hindu Undivided Family (HUF) structure is one of the most underused tax tools available to eligible Indian doctors. Under the Income Tax Act, an HUF is assessed as a separate "person" with its own PAN, its own basic exemption slab, and crucially, its own ₹1.5 lakh Section 80C deduction basket.

For Hindu, Buddhist, Jain, or Sikh doctors, a properly constituted HUF can receive ancestral property income or gifts and be assessed separately—effectively splitting the family's tax burden across two entities.

This strategy requires a CA and a financial adviser working together. The HUF must be constituted correctly, income must genuinely belong to the HUF entity, and the structure must be maintained with proper books. Done right, it's entirely legal and significantly impactful in practice.

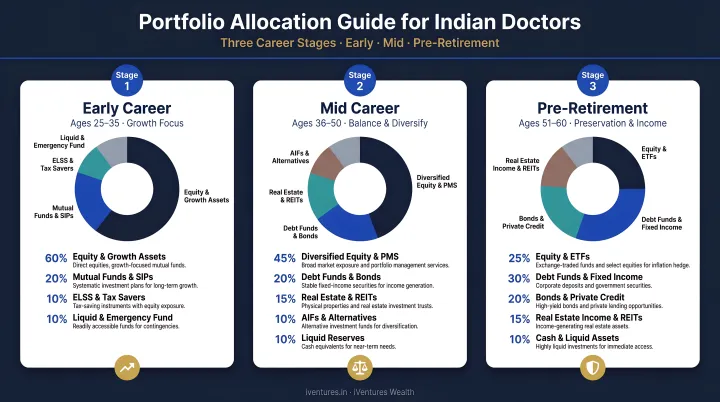

Building a Stage-Appropriate Investment Portfolio

Tax efficiency sets the foundation — but it works best when coordinated with a portfolio built for your life stage. The right allocation for a 32-year-old doctor starting her first SIP looks very different from what suits a 52-year-old specialist winding down clinical hours:

Early career (30–40):

- Equity-heavy SIPs in diversified and flexi-cap mutual funds

- Focus on long-term compounding; volatility is an advantage at this stage

- Avoid ULIPs and endowment plans—their internal costs and opaque returns make them poor wealth-building vehicles

Mid-career (40–50):

- Add debt mutual funds and Sovereign Gold Bonds for balance

- Consider REITs for income diversification

- Begin systematic review of insurance coverage adequacy

Pre-retirement (50+):

- Gradually shift toward capital-preserving and income-generating instruments

- Systematic Withdrawal Plans (SWPs) from accumulated mutual fund corpus

- Annuity planning through NPS Tier-I

One point on asset location that many doctors miss: debt instruments and dividend-paying assets generally produce tax-inefficient income under the old regime. Placing them within tax-sheltered structures and keeping long-term equity investments in growth-oriented funds allows LTCG tax rates (currently 12.5% on gains above ₹1.25 lakh for equity) to do their work rather than being eroded by slab-rate income tax.

This kind of integrated construction — where fund selection, tax treatment, and life-stage allocation are considered together — requires an adviser whose recommendations aren't shaped by product commissions. iVentures Wealth (SEBI RIA registration INA000019026) works on a fee-only basis, with a CFA-led research team that builds personalised strategies for medical professionals across each of these dimensions.

Risk Management: The Insurance Checklist Every Doctor Must Have

Professional Indemnity: The Non-Negotiable

A National Consumer Disputes Redressal Commission review of 253 medical-negligence cases from 2015 to 2019 illustrates the litigation landscape Indian doctors operate in. Cases span every specialty, and even outcomes in a doctor's favour involve years of legal process and significant expense.

Professional indemnity insurance covers legal defence costs and damages arising from alleged negligence in clinical practice. The risk exposure differs significantly by specialty—a general practitioner's liability profile is materially different from a surgeon's or an interventionist's.

Despite this, many Indian doctors either carry no professional indemnity insurance or carry inadequate limits. The IMA's National Professional Protection Scheme offers a baseline option for IMA life members, but specialists performing high-risk procedures should evaluate whether standalone commercial policies provide more appropriate coverage limits.

Term Insurance vs. the ULIP Trap

Insurance agents frequently approach doctors with ULIP or endowment proposals positioned as "investment-cum-protection" solutions. The practical problem: ULIPs carry layered charges—premium allocation, mortality, and fund management fees—that erode returns, while the actual life cover provided is typically insufficient.

A pure-term policy delivers far more coverage per rupee of premium. Coverage benchmarks suggest 10–12 times gross annual income for those under 55, increasing to approximately 15 times for those over 45. For a doctor earning ₹30–50 lakh annually, this means cover in the range of ₹3–7.5 crore—available through term insurance at a fraction of the cost of an equivalent ULIP face value.

The separate-and-invest approach—term insurance for protection, mutual funds for growth—consistently outperforms bundled insurance products across 10- and 20-year horizons.

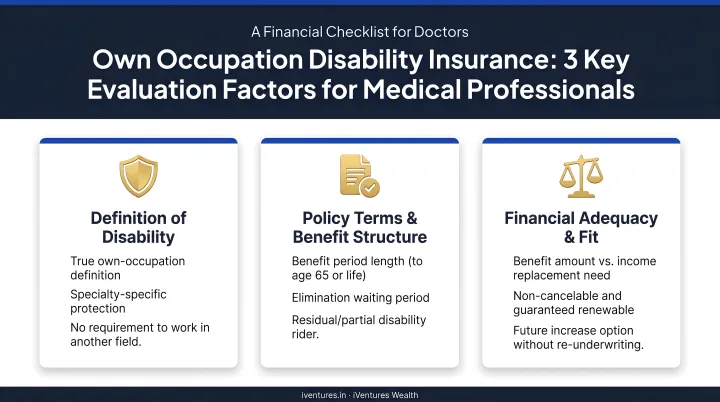

Disability Insurance: The Coverage Most Doctors Don't Have

Most Indian doctors skip disability insurance entirely—yet it covers what may be the single most financially devastating risk they face. An orthopaedic surgeon who develops a hand tremor, or a cardiologist who suffers vision loss, may be unable to practice their specialty even if they can still work in some capacity.

This is where own-occupation coverage matters. It pays benefits when you cannot perform your specific medical role—not just when you cannot work at all. When evaluating policies, examine three factors:

- Whether the elimination period (the waiting period before benefits start) fits your cash reserves

- Whether the benefit duration extends to age 60 or only until partial recovery

- Whether the own-occupation definition explicitly covers inability to perform your specific specialty

Personal Health Insurance: Don't Rely on Group Cover

Medical inflation in India runs at 14%, and the average health insurance claim in FY24 reached ₹70,558—up 11.35% year-on-year. Major cardiac procedures now cost ₹2–3 lakh, kidney transplants ₹10–15 lakh, and the largest single cardiac claim in the past year exceeded ₹1.1 crore.

Employer group cover typically covers only 74% of hospital expenses and lapses when a doctor changes hospitals or starts independent practice. A comprehensive family floater with a sum insured of at least ₹25–50 lakh—indexed upward every few years given medical inflation—is essential, and should be maintained separately from any employer group policy.

Retirement Planning for Physicians: Starting Late, Finishing Strong

Calculating Your Retirement Number

PGIM India's 2025 Retirement Readiness Report found that only 37% of Indians had a retirement plan—down sharply from 67% in 2023. For doctors starting late, the absence of a plan is particularly expensive.

Calculating a retirement number requires three inputs:

- Expected monthly expenses at retirement (current expenses, adjusted for inflation to the retirement date)

- Retirement duration (a 60-year-old doctor today should plan for 25–30 years of income)

- Required corpus (using a safe withdrawal rate, typically 3–4% for India's inflation environment, the corpus = annual expenses ÷ withdrawal rate)

A doctor expecting ₹2 lakh/month in today's money, planning for 30 years post-retirement, needs a corpus that most people significantly underestimate when they try to guess rather than calculate.

NPS: A Dedicated Retirement Vehicle Worth Using

The National Pension System offers two benefits doctors often overlook together:

- 80CCD(1) deduction — contributions within the 80CCE limit alongside 80C

- 80CCD(1B) deduction — an additional ₹50,000 entirely outside the aggregate cap

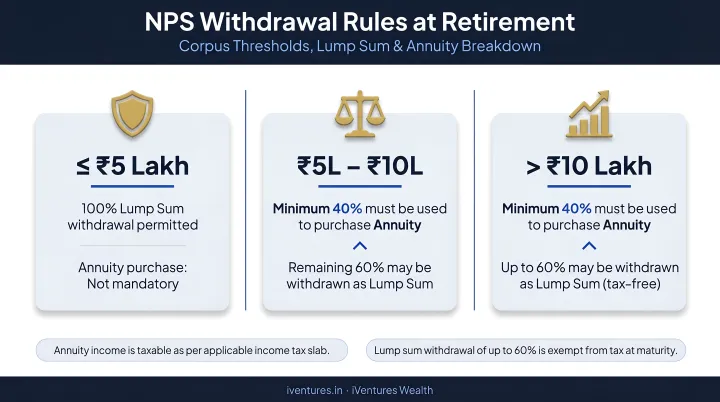

At normal exit (age 60 or after 15 years of subscription), the withdrawal rules are:

- Corpus above ₹12 lakh: up to 80% as lump sum; at least 20% must go into annuity

- Corpus below ₹8 lakh: full amount can be withdrawn as lump sum

- Partial withdrawals: up to 25% of own contributions, permitted up to four times before age 60, with a minimum four-year gap between withdrawals

For a doctor in the 30% tax slab, the ₹50,000 80CCD(1B) deduction saves ₹15,600 annually. Over a 25-year career, that alone compounds into a meaningful retirement buffer—before accounting for the returns on the NPS corpus itself.

Practice Succession: The Asset Without a Plan

NPS addresses the savings side of retirement. But for doctors who own clinics, the practice itself is often the largest single asset—and the one with no succession plan, no formal valuation, and no exit strategy.

A practice can be valued based on revenue multiples, patient list value, or EBITDA—but most doctors have never had this conversation with an adviser. The exit route determines the tax outcome: each option carries different implications:

- Sale to a junior partner — typically structured as a business transfer; capital gains treatment depends on asset classification

- Acquisition by a corporate hospital chain — often involves goodwill valuation and slump sale considerations

- Structured wind-down — requires careful timing of asset disposals to manage tax incidence across years

These scenarios should be modelled well before the transaction, not after a term sheet arrives.

iVentures Wealth works with doctors on exactly this: mapping the practice exit, structuring the resulting capital event, and building a post-liquidity corpus that supports retirement income without a tax-efficiency gap at the point of transfer.

Estate Planning and Building a Multi-Generational Legacy

The Three Non-Negotiable Documents

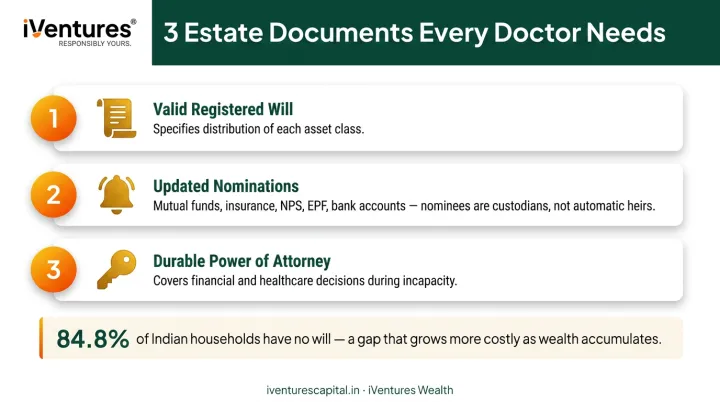

84.8% of Indian households do not have a will. For high-earning doctors with complex assets—practice ownership, insurance policies, mutual fund folios, real estate, EPF, NPS—dying intestate creates the conditions for prolonged family disputes and frozen assets.

Every doctor needs three documents in place:

- A valid, registered will — specifying distribution of each asset class clearly

- Nominations updated in every account — mutual fund folios, insurance policies, NPS, EPF, bank accounts. Nominees are legal custodians, not automatic heirs; without a will, even a named nominee can be challenged

- A durable power of attorney — for financial and healthcare decisions in case of incapacity

These aren't once-done documents. They need to be reviewed whenever a major asset is acquired, a family situation changes, or a nomination goes unupdated after marriage or divorce.

Private Family Trusts and Asset Protection

Under the Indian Trusts Act, 1882, a private family trust is a legally recognised structure for holding and transferring wealth across generations. For doctors with malpractice liability exposure, placing accumulated personal assets within a properly constituted trust structure creates a legal separation between professional liability and family wealth.

Trust structures also allow:

- Assets pass to heirs on terms set by the settlor—not unconditionally, and not subject to a beneficiary's creditors

- Wealth transfers within a documented framework, reducing probate friction and the risk of legal disputes

- The trust outlives the individual, providing continuity across generations that a simple will cannot

For doctors navigating this complexity, working with an advisor who coordinates legal, tax, and wealth planning in one place makes a significant difference. iVentures Wealth supports private trust establishment in coordination with legal counsel—including for families with NRI children or cross-border assets. Their family office advisory also includes inter-generational financial conversations, helping spouses and adult children understand the family's financial architecture before they inherit it.

The firm's documented case of "Two-Generation Consolidation" demonstrates what this looks like practically: consolidating nine separate financial relationships into a unified family balance sheet, establishing a simple family charter, and setting up a basic trust for minor grandchildren—creating clarity and reducing future dispute risk.

Frequently Asked Questions

What are the key pillars of medical wealth management?

The five pillars are: financial foundation (budgeting, debt management, emergency fund), tax-efficient investing, risk management through insurance, retirement planning, and estate planning. Each builds on the previous. Getting the foundation right before optimising taxes or investing aggressively prevents costly mistakes.

Is paying 1% to a financial adviser worth it for a doctor?

For doctors whose professional time is extremely valuable, a SEBI-registered fee-only adviser who earns no product commissions typically saves far more through tax optimisation, insurance structuring, and portfolio efficiency than the advisory fee costs. The relevant question is not the fee percentage but whether the adviser is conflict-free, qualified, and genuinely acting in the client's interest.

When should a doctor in India start financial planning?

The ideal time is during residency or fellowship—even on a modest stipend. The structures set up early (SIPs, term insurance, health cover, emergency fund) compound dramatically over time. Every year of delay at the beginning of a career is disproportionately expensive relative to delays at later stages.

How can doctors legally reduce their income tax in India?

The primary levers under the old regime: maximise Section 80C (ELSS, PPF), Section 80D (health insurance for self and parents), and Section 80CCD(1B) (NPS). A properly constituted HUF creates a separate tax entity with its own deduction basket. All legitimate practice expenses must be documented, claimed, and coordinated with a CA and financial adviser.

What type of insurance is most critical for a medical professional?

Professional indemnity insurance and own-occupation disability insurance are the two most underutilised and critical covers—most doctors carry neither. A pure-term life policy providing 10–15 times annual income is the third essential. ULIPs and endowment plans should not be mistaken for adequate life cover.

Should a doctor invest in expanding their practice or in financial markets?

Both are valid, but practice reinvestment should be treated as one asset class within a diversified portfolio—not the only wealth-building strategy. Doctors who concentrate entirely in practice growth can find themselves financially exposed if clinical income is disrupted. Diversification across financial instruments provides a runway that practice assets alone cannot offer.