Introduction

Picture this: your daughter's engineering college fees are due next month, your father just got discharged from a private hospital after a cardiac procedure, and your SIP reminder sits unanswered in your inbox. This is the daily reality for millions of Indian families in their 40s and 50s — caught between funding their children's futures and supporting aging parents, while their own retirement quietly slips further away.

According to an Axis Max Life and Business Today survey released in January 2026, 57% of India's urban population identifies as the sandwich generation. More worrying: only 38% of this group believes their retirement savings will last beyond 10 years.

India compounds this squeeze in ways most financial frameworks ignore. There is no comprehensive government-funded long-term care system, and private healthcare costs climb every year.

Cultural expectations that adult children will support aging parents — financially and physically — remain deeply embedded. What Western families partially offset through public elder care programs, Indian families absorb entirely out of pocket.

The families who navigate this well share one thing: they stopped treating retirement, elder care, and education as separate problems and started planning them as one.

Key Takeaways

- Retirement savings must be protected first — you cannot borrow to fund retirement the way you can fund education

- Elder care in Indian metros can cost ₹40,000–₹1.5 lakh per month — plan before a health crisis forces the decision

- Section 80D allows up to ₹50,000 in deductions on health insurance premiums for senior citizen parents

- Goal-based investing with separate buckets for retirement, education, and elder care prevents dangerous cross-contamination

- A SEBI-registered fee-only adviser integrates all three goals into one coordinated plan

The Financial Pressures Sandwich Generation Members Face in India

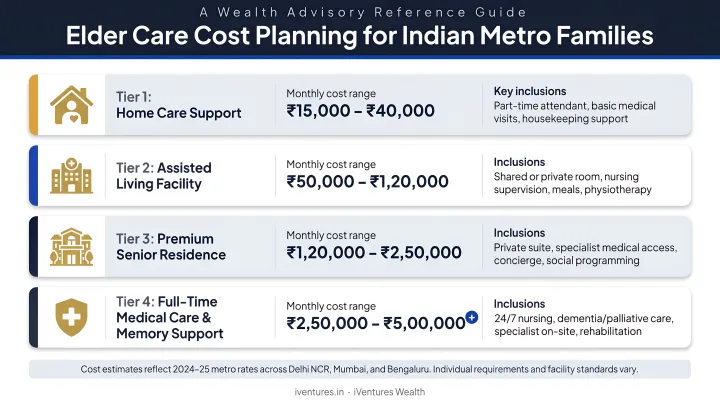

The Elder Care Cost Reality

India has no organised formal long-term care system. Families absorb these costs entirely, and they are not small.

Current approximate ranges from providers in Indian metros:

| Care Type | Monthly Cost Range |

|---|---|

| Part-time home attendant | ₹150–300 per hour |

| Full-time live-in attendant | ₹12,000–25,000 |

| 24/7 non-medical home care | ₹35,000–50,000 |

| Assisted living / care home | ₹40,000–1.5 lakh+ |

These are provider-published ranges, not official national averages. Actual costs vary by city, care intensity, and facility quality. A single hospitalisation in a private ICU can add significantly more — academic research puts the provider cost of a private ICU bed-day at roughly ₹10,600.

With UNFPA projecting that older persons will make up approximately 20% of India's population by 2050, the duration of elder care obligations is only getting longer.

The Education and Retirement Squeeze

Education costs have risen sharply. Quality private school fees in Indian metros run approximately ₹1–4 lakh per year, with international schools charging ₹7–30 lakh annually. Add JEE or NEET coaching — Kota residential programmes currently cost around ₹1.10–1.35 lakh per year excluding GST — and the pressure compounds. Overseas undergraduate degrees in the UK or Australia now routinely cost ₹50–80 lakh or more when tuition and living costs are combined.

When these immediate expenses compete with retirement savings, retirement savings are what give way.

The data from EPFO tells the story indirectly. In FY 2024-25, EPFO processed over 5.08 crore claims worth ₹2,05,932 crore, with more than 60% being advance withdrawals rather than retirement settlements. Indian workers are treating their provident fund as a liquid emergency account. That pattern quietly destroys the compounding that retirement security depends on.

The Invisible Cost: Women Leaving the Workforce

One financial consequence rarely appears in family financial plans: the career impact on women caregivers. The ILO estimates that 708 million women globally are outside the labour force due to unpaid care responsibilities, with Asia-Pacific data identifying this as a primary labour force barrier.

When a spouse reduces hours or exits employment to manage a parent's care, the household loses more than income. EPF contributions stop. Career trajectory flattens. The cumulative retirement shortfall from even a 3–5 year career interruption in one's 40s can be substantial — and it is almost never quantified in advance.

Why Your Retirement Savings Must Come First

The Oxygen Mask Principle

Children can take education loans. Parents may have assets, pensions, or fixed deposits. You cannot borrow to fund your own retirement.

Prioritising your own retirement savings is the most responsible choice available. A parent who depletes their corpus to fund a child's college education or a parent's medical bills often becomes financially dependent on the next generation within 15 years. The burden shifts forward — it does not disappear.

What a Short Pause Actually Costs

Compounding punishes interruptions more than most people realise. Take someone in their mid-40s contributing ₹50,000 monthly toward retirement who pauses for four years to manage a caregiving crisis.

- Those 48 months of missed contributions represent ₹24 lakh in unpaid principal

- More critically, that capital loses 20+ years of compounding before retirement

- The final corpus shortfall is typically 3–5 times the missed contributions, not equal to them

The loss is not ₹24 lakh. It is the retirement security those contributions would have generated across two decades.

What to Protect — Non-Negotiable Items

Even during financially tight periods, these should not be paused or raided:

- EPF contributions — the employer match is free money with permanent tax advantages; once lost, it cannot be reclaimed.

- NPS contributions — Section 80CCD(1B) provides an additional ₹50,000 deduction beyond the ₹1.5 lakh 80CCE ceiling; a missed year means a missed deduction, not a deferred one.

- Equity SIPs dedicated to retirement — pausing during a market downturn locks in losses and forfeits the recovery that follows.

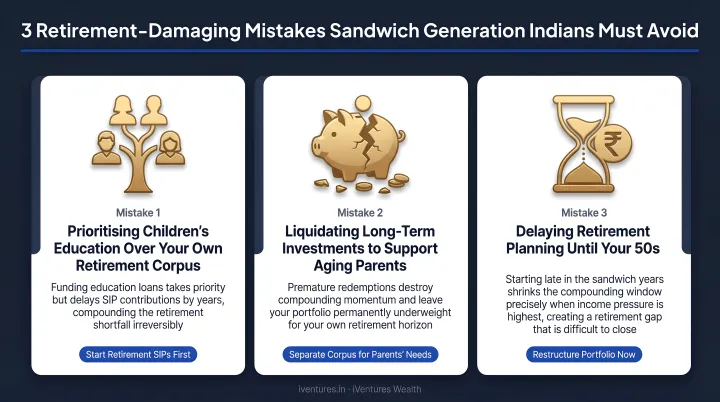

Three Moves That Cause Disproportionate Damage

Borrowing against PPF or EPF — these accounts compound tax-free, and a loan or withdrawal does not merely reduce the balance. It interrupts the compounding cycle precisely when it is working hardest.

Stopping SIPs to fund caregiving — restarting a SIP 2–3 years later cannot recapture units bought during the downturn. The rupee-cost averaging benefit is permanently lost, not deferred.

Liquidating equity during a correction — selling to meet an immediate family expense turns a temporary paper loss into a permanent one. The portfolio also forfeits the recovery gains it would have generated.

Reframing the Cultural Narrative

In the Indian context, prioritising your own retirement is an act of care for your children. A parent who retires financially self-sufficient never asks their children to cover medical bills, living expenses, or housing. Arriving at retirement without financial dependence is itself a form of inheritance — one that costs the next generation nothing.

How to Manage Elder Care Costs Without Derailing Your Finances

Start With a Conversation Before a Crisis

The worst time to discover your parents have no health insurance is the day they need hospitalisation. Have the financial conversation before it becomes urgent:

- What assets do they hold — property, FDs, pension, EPF corpus?

- Do they have health insurance, and what does it cover?

- Are there outstanding loans or liabilities?

- What are their preferences for care — home nursing, assisted living, family care?

Yes, it's an uncomfortable conversation. It's also far less painful than making reactive, expensive decisions mid-crisis.

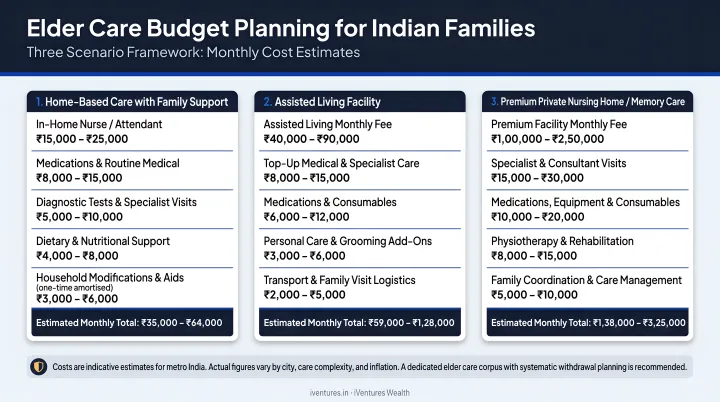

Build a Three-Scenario Elder Care Budget

Rather than guessing a single monthly number, plan across three scenarios:

| Scenario | Situation | Approximate Monthly Budget |

|---|---|---|

| Scenario A | Parents mostly independent, occasional medical visits | ₹10,000–20,000 |

| Scenario B | Part-time home help, regular specialist consultations | ₹25,000–50,000 |

| Scenario C | Full-time nursing care or assisted living facility | ₹60,000–1.5 lakh+ |

Earmark a dedicated elder care fund separate from your emergency fund and retirement corpus. Allowing care costs to bleed into general savings is how retirement plans silently deteriorate.

Legal and Administrative Groundwork

Do this proactively — the cost of doing it reactively is far higher:

- Healthcare Power of Attorney: Designate who makes medical decisions if parents cannot

- Updated will: Ensure it reflects current assets and intentions

- Beneficiary nominations: Verify nominations on all bank accounts, FDs, insurance, and investment accounts

- Jointly held assets: Understand the implications of joint property ownership and transmission

Distribute the Care Burden

Elder care costs — both financial and time-based — should be a shared family responsibility, not silently absorbed by one sibling. A structured family conversation about contributions (financial and caregiving) is uncomfortable but prevents resentment and financial distortion for the person carrying the load.

iVentures Wealth works with multi-generational families to facilitate exactly these conversations — mapping out who contributes what, financially and in caregiving time, across siblings with different income levels and asset bases. It's a practical starting point when family dynamics make the conversation harder than the math.

Funding Your Children's Education the Smart Way

Start Early, Keep It Separate

A dedicated education corpus, built through a separate equity SIP started when a child is young, has a distinctly different risk profile than a retirement fund. With a 12–15 year horizon, it can absorb equity volatility and benefit from compounding. The critical rule: **keep it completely separate from the retirement corpus**.

When families face financial pressure, the temptation is to treat all savings as interchangeable. It is not. Drawing from a retirement SIP to fund education fees sets back a 20-year goal to solve a 1-year problem.

Set Honest Expectations Early

Before a college aspiration becomes fixed, have a frank family conversation about what the budget realistically supports. This means:

- Discussing the education corpus target before a child reaches Class 10

- Exploring scholarship opportunities proactively, not as a fallback

- Considering whether an education loan for a portion of costs is appropriate — it gives the child ownership of their future

- Evaluating domestic alternatives alongside overseas programmes honestly

The Hierarchy Is Clear

If funding a particular education goal requires any of the following, the education plan needs recalibration — not the retirement plan:

- Pausing retirement SIPs

- Liquidating long-term equity investments

- Taking a personal loan to cover fees

Children have options: education loans, scholarships, public universities, deferred postgraduate studies. Retirees do not have equivalent alternatives when corpus is depleted.

Tax Benefits and Insurance Strategies to Know

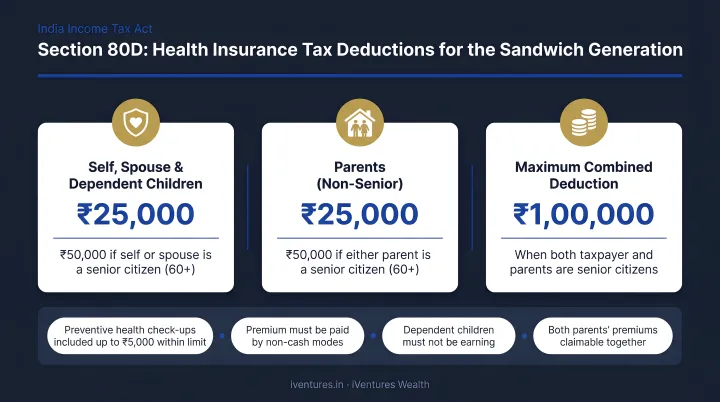

Section 80D: Use It Fully

For AY 2026-27 under the old tax regime, sandwich generation members can claim:

| Coverage | Deduction Limit |

|---|---|

| Self, spouse, and dependent children (below 60) | ₹25,000 |

| Parents aged 60 and above (senior citizens) | ₹50,000 |

| Preventive health check-up (within overall limit) | ₹5,000 |

A family paying health insurance premiums for themselves and senior citizen parents can claim up to ₹75,000 in total 80D deductions. Many families leave this partially unclaimed simply because they have not structured the premiums correctly.

NPS contributions under Section 80CCD(1B) provide an additional ₹50,000 deduction beyond the standard ₹1.5 lakh 80CCE ceiling — making NPS one of the few instruments that genuinely expands the tax deduction envelope.

Insurance Gaps That Need Addressing

Most sandwich generation members in India are underinsured in specific ways:

- Term life cover: Sized to replace income for dependents — both children and parents — not just to cover a home loan

- Senior citizen health insurance for parents: Standalone policies rather than assuming group cover continues post-retirement

- Personal critical illness or disability cover: If the primary earner cannot work, the caregiving burden on the family intensifies at exactly the moment income stops

The Long-Term Care Gap

India does not yet have a mature standalone long-term care insurance category. Most health insurance policies cover hospitalisation and domiciliary medical treatment, but explicitly exclude custodial care — routine assistance with daily activities like bathing, feeding, and mobility.

Some insurers describe long-term care concepts, but as of 2026 this remains an emerging and limited product category in India. Families should not assume their parents' health insurance policies cover sustained home-based nursing care. This gap is why setting aside a separate, dedicated financial reserve for elder care — outside standard health insurance — is a non-negotiable part of the plan.

Building a Multi-Generational Financial Plan: Where to Begin

Establish Annual Family Financial Meetings

Once a year, bring together the key stakeholders — spouse, adult children if applicable, and parents where appropriate — to review:

- Progress toward each goal (retirement, education, elder care)

- Changes in caregiving responsibilities or costs

- Insurance adequacy

- Estate and nomination status for all family members

Treating family finances as a shared agenda rather than one person's burden reduces both financial and emotional strain on the primary earner.

Engage a Fee-Only Adviser Before a Crisis

The optimal time to build a multi-goal plan is in your late 30s or early 40s — before a parent's hospitalisation, before a child's college decision is imminent, and before retirement feels urgent.

A SEBI-registered, fee-only financial adviser can create a consolidated plan that maps retirement, education, elder care, and insurance needs simultaneously. They stress-test it against different care scenarios and prioritise goals based on your family's actual timeline — not in response to a crisis.

iVentures Wealth works specifically with affluent Indian families navigating these multi-generational demands. Their Family Office model covers retirement, child education, estate planning, and passive income structuring within a single advisory relationship.

As a SEBI-registered, fee-only adviser (INA000019026), the firm structures advice around your family's goals — not product commissions.

Frequently Asked Questions

What is the sandwich generation and how common is it in India?

The sandwich generation refers to middle-aged adults financially supporting both aging parents and their own children simultaneously. An Axis Max Life survey from January 2026 found that 57% of India's urban population identifies this way — driven by rising life expectancy and extended financial dependence among young adults.

Should I prioritise my retirement savings or my children's education?

Retirement savings should come first. You can fund education through loans, scholarships, or part-time student work — viable options your children have. You cannot borrow to fund retirement. Protecting your own financial future ultimately protects your children from supporting you later.

How do I start the conversation with my parents about their finances?

Begin with something low-stakes, like reviewing their health insurance coverage together. From there, gradually discuss assets, existing savings, will status, and care preferences. Starting before any health crisis makes these conversations far easier and less emotionally charged.

What tax benefits are available for sandwich generation members in India?

Section 80D allows up to ₹50,000 in deductions for health insurance premiums paid for senior citizen parents, plus up to ₹25,000 for your own family cover. NPS contributions under 80CCD(1B) add another ₹50,000 above the standard 80C ceiling.

How much should I set aside for elder care expenses?

The right amount depends on your parents' existing assets, health status, and care preferences. Build a three-scenario budget and stress-test against the highest-cost scenario — a dedicated elder care fund, kept separate from your emergency fund and retirement corpus, gives you far more precision than a rough estimate.

When should I consult a financial adviser as a sandwich generation member?

Before a crisis hits — ideally in your late 30s or early 40s. A proactive plan built early is far more effective than scrambling to fill financial gaps as a parent's health deteriorates or a child's college deadline approaches.