For Indian founders, the stakes are particularly high. Capital gains tax, shareholding structure, estate planning, and SEBI-regulated advisory choices all intersect at the exit. Getting any one of them wrong is costly. Getting all of them right requires coordination that most founders have never had to think about before.

This guide covers the five dimensions that matter most: the mindset shift from entrepreneur to capital steward, pre-exit preparation, tax strategy, post-exit portfolio construction, and estate planning — each examined through the lens of Indian regulatory reality.

Key Takeaways

- Wealth management for founder exits begins before the deal closes, not after

- LTCG on unlisted shares is now 12.5% without indexation (effective rate: 13.00%–14.95%), making tax structuring the largest lever on net proceeds

- Diversifying a concentrated exit position is the most consequential risk decision a founder will face

- A SEBI-registered RIA cannot earn product commissions, making it the only legally conflict-free advisory structure

- Estate and succession planning should be structured simultaneously with the exit, not deferred

When a Business Becomes Capital: The Founder's Financial Transition

For most founders, nearly all of their net worth sits inside a single, illiquid entity for years. The exit changes that overnight. A large, liquid capital pool arrives — and with it, a set of risks that look nothing like the risks of running a business.

Concentration Risk Doesn't Disappear at Exit

The most common mistake post-exit founders make is replicating the same concentrated exposure they just sold. Reinvesting the majority of proceeds into a new venture, a familiar sector, or a single asset class recreates the single-asset risk profile they escaped.

Research from Yale's 2025 post-exit entrepreneur study surveying 52 post-exit entrepreneurs with a net worth of at least USD 10 million found that 70% had not planned for post-exit life and 59% had not found a new purpose — a psychological reality that directly affects financial decision-making in the months after closing.

The liquidity paradox compounds this. For the first time, founders have maximum financial flexibility — yet without a structured framework, that freedom produces reactive choices:

- Angel investments made under social pressure

- Real estate purchased simply to avoid idle capital

- Market timing errors driven by impatience rather than strategy

The Emotional Dimension

For many Indian founders, the business represents identity, daily structure, and long-term purpose — not just a financial asset. The post-exit period can bring genuine disorientation, and that psychological state is not separate from financial decision-making. It shapes it.

A deliberate pause period of 3 to 6 months before deploying capital into new commitments is worth building into the plan. This is not inaction — structured planning, tax review, and advisor engagement should begin immediately. Deployment is deferred until clarity arrives.

That deliberate framework is precisely what structured post-exit advisory addresses. iVentures Wealth's approach for founder clients converts the liquidity event into a three-bucket capital plan — Safety, Stability, and Growth — while simultaneously establishing family trust governance. The goal is replacing the founder's daily financial purpose with an equally intentional structure for managing the capital that purpose created.

Pre-Exit Wealth Planning: Why It Starts Before the Deal Closes

The window between signing an LOI and deal close — or earlier, during due diligence preparation — is the most consequential planning window in a founder's financial life. Decisions made before closing can significantly reduce tax liability and improve estate efficiency. Decisions deferred to after closing are often irreversible.

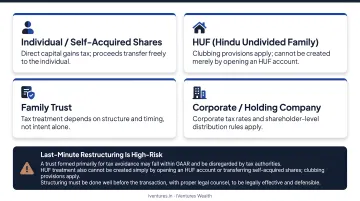

Structuring Ownership Before the Transaction

How shares are held at the time of exit matters enormously. The tax computation and legal transferability of proceeds differ depending on whether shares are held by:

| Holding Structure | Key Tax/Legal Consideration |

|---|---|

| Individual | Direct taxpayer; Section 112 LTCG treatment applies |

| HUF | Separate taxable entity, but Section 64(2) clubs back income from self-acquired property transferred without adequate consideration |

| Determinate Trust | Trustee assessed as representative for beneficiaries under Sections 160–161 |

| Discretionary Trust | Section 164 may apply maximum marginal rate; revocable-trust income can be clubbed with settlor |

| Holding Company | Corporate taxpayer; distribution to founder is a separate, additional taxable step |

One critical warning: last-minute restructuring is high-risk. A trust formed primarily for tax avoidance may fall within GAAR and be disregarded by tax authorities.

HUF treatment also cannot be created simply by opening an HUF account or transferring self-acquired shares — clubbing provisions apply. Structuring must be done well before the transaction, with proper legal counsel, to be legally effective and defensible.

Timing the Exit for Tax Efficiency

The holding period threshold for unlisted shares to qualify as long-term is more than 24 months. A transaction closing in one financial year versus the next — or before versus after crossing the 24-month mark — can produce meaningfully different tax outcomes.

For founders who are NRIs, OCIs, or who plan to shift residency post-exit, three additional dimensions come into play:

- FEMA compliance on repatriation of sale proceeds

- DTAA treaty benefits and applicable withholding rates under the relevant tax treaty

- Residency timing relative to the exit date, which determines which tax regime applies

Each of these variables compounds the others. This is a specialist planning area where errors are expensive.

iVentures' founder advisory mandate includes direct coordination with the founder's tax counsel, legal counsel, and CA. Investment deployment timelines are structured to work within the exit's legal and tax framework, not independently of it.

Tax Strategies to Protect Exit Proceeds in India

Tax planning is the first and most time-sensitive wealth management decision at a founder exit. For a founder exiting a private company, getting the structure right can protect crores that would otherwise be lost to avoidable tax.

Current LTCG Rate on Unlisted Shares

Following the Finance (No. 2) Act 2024, resident LTCG on unlisted shares transferred on or after 23 July 2024 is taxed at 12.5% without indexation. The effective rates, after applying the capped 15% surcharge and 4% cess, are:

- 13.00% — for total income up to ₹50 lakh

- 14.30% — for total income between ₹50 lakh and ₹1 crore

- 14.95% — for total income above ₹1 crore

Short-term capital gains (for shares held 24 months or less) are taxed at the individual's applicable income tax slab rate — which can reach 30% for founders with substantial other income.

Capital Gains Reinvestment Exemptions

Section 54F allows individuals and HUFs transferring a long-term capital asset (other than a residential house) to claim an exemption by investing in one residential house in India. Key conditions:

- Full exemption when the new house cost equals or exceeds the net consideration

- Proportionate exemption otherwise: LTCG × new house cost / net consideration

- Must not own more than one other residential house on the transfer date

- Purchase window: one year before or two years after transfer; construction: three years after

- The ₹10 crore cap on cost and net consideration (introduced by Finance Act 2023, effective AY 2024–25) means proceeds above ₹10 crore do not qualify for additional exemption under this route

Capital Gains Account Scheme (CGAS): If a founder cannot deploy the reinvestment within the same financial year, unused net consideration must be deposited in a CGAS account before filing the return (no later than the Section 139(1) due date) to preserve exemption eligibility. Account A is savings-type; Account B is term deposit. Unused CGAS funds become taxable LTCG in the year the reinvestment period expires.

One practical caution: Section 54F defers tax by concentrating liquidity into a single illiquid asset. That can directly contradict the diversification goal driving the exit in the first place.

The exemption makes sense where it fits the founder's genuine lifestyle and estate objectives — not as a reflexive tax-avoidance move.

Charitable Giving and Section 80G

For founders with philanthropic intent, donations to registered trusts or Section 8 companies can reduce taxable income in the exit year through Section 80G deductions. The four deduction classes are:

- 100%, no qualifying limit — specified government funds (PM Relief Fund, PMNRF, etc.)

- 50%, no qualifying limit — certain approved charitable institutions

- 100%, with limit — donations subject to 10% of adjusted gross total income ceiling

- 50%, with limit — other approved charities, capped at 10% of adjusted gross total income

Two conditions founders routinely miss: cash donations above ₹2,000 are ineligible, and a private family-benefit foundation does not qualify automatically. The recipient must hold valid 80G approval and satisfy all prescribed conditions.

Building a Diversified Post-Exit Investment Portfolio

The portfolio that replaces a founder's business has a different job: generate returns through intelligent asset allocation, with minimal daily involvement. This shift — from operator to owner of capital — requires a deliberate structure, not improvised deployment.

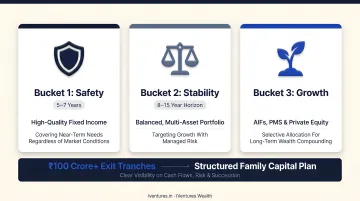

The Three-Bucket Framework

iVentures Wealth's documented approach for large liquidity events structures capital into three distinct buckets based on time horizon and purpose:

- Bucket 1 — Safety: 5–7 years of living expenses in high-quality fixed income, covering near-term needs regardless of market conditions

- Bucket 2 — Stability: A balanced, multi-asset portfolio built for an 8–15 year horizon, targeting growth with managed risk

- Bucket 3 — Growth: Selective allocation to AIFs, PMS, and private equity for long-term wealth compounding

This framework was applied in a documented case study involving a promoter who received over ₹100 crore in exit tranches — converting a one-time liquidity event into a structured family capital plan with clear visibility on cash flows, risk, and succession.

Understanding this framework naturally raises the next question: which specific asset classes fit into each bucket, and what does access actually require?

Asset Classes and Access Thresholds

For founders with large post-exit corpuses, the full asset allocation universe becomes available:

| Asset Class | Instruments | Access Threshold |

|---|---|---|

| Public Equities | Direct stocks, mutual funds, ETFs | Open |

| Fixed Income | Bonds, debt funds, FDs | Open |

| PMS | Institutional-grade equity strategies | ₹50 lakh minimum |

| AIFs | Private equity, private credit, hedge strategies | ₹1 crore minimum |

| Real Estate | REITs, commercial, residential | Varies |

| Global | International funds, ETFs, global diversification | Open (with FEMA compliance) |

Allocation percentages should reflect individual goals, risk tolerance, time horizon, and tax position — not one-size-fits-all benchmarks. AIF commitments grew from ₹3.69 lakh crore in March 2020 to ₹11.34 lakh crore by March 2024, as this asset class becomes increasingly institutionalised in India.

iVentures Wealth's open-architecture model means PMS and AIF recommendations span the full market — not a limited proprietary shelf.

For founders whose wealth spans multiple legal structures post-exit, the Wealth Monitor App provides a consolidated dashboard across mutual funds, PMS, AIFs, equities, bonds, and FDs — with multi-entity toggling between individual, family, and HUF portfolios.

Estate, Succession, and Legacy Planning for Founders

A founder exit creates a clean, well-defined capital base — which is far easier to structure into wills, trusts, and succession plans than a complex active business with ongoing liabilities. That makes the exit a natural inflection point for generational wealth planning.

Yet PwC's 2019 India Family Business Survey found that only 21% of 106 Indian family businesses had a robust, documented, and communicated succession plan — with 34% having no plan at all. For founders, deferring estate planning post-exit replicates this gap at exactly the wrong moment.

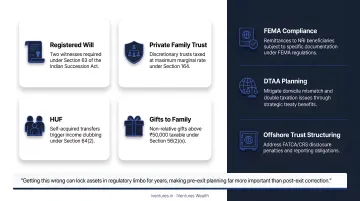

Key Instruments for Indian Founders

- Registered Will: Requires signature and attestation by at least two witnesses under Section 63 of the Indian Succession Act. Registration is optional but strongly recommended for probate ease.

- Private Family Trust: Legal ownership transfers to trustees; beneficial interests follow the trust deed. Discretionary trusts carry a specific tax risk: they attract maximum marginal rate taxation under Section 164, unlike determinate trusts.

- HUF: Separate taxable entity for Hindu, Jain, and Sikh families; arises from family status, not contract. Transferring self-acquired property to an HUF without adequate consideration triggers income clubbing under Section 64(2).

- Gifts to family: Gifts from specified relatives are exempt without a monetary ceiling. Non-relative gifts above ₹50,000 annually become taxable under Section 56(2)(x).

Cross-border family situations add another layer. Founders with NRI children, dual-citizenship members, or overseas assets must navigate:

- FEMA compliance — gift and inheritance remittances to NRI beneficiaries follow separate LRS and FEMA rules

- DTAA planning — misaligned domicile status can result in double taxation on estate transfers

- Offshore trust structuring — beneficial ownership reporting under FATCA/CRS applies; non-disclosure creates penalties, not just tax inefficiency

Getting this wrong can lock assets in regulatory limbo for years, making pre-exit planning far more important than post-exit correction.

How to Choose the Right Wealth Advisor After a Founder Exit

The advisor a founder selects post-exit shapes everything that follows — tax outcomes, estate structure, and long-term capital preservation. For a corpus of ₹10 crore and above, the quality of advice and planning depth matters far more than fee minimisation.

The Fiduciary Distinction That Actually Matters

| Advisor Type | Compensation | Conflict |

|---|---|---|

| SEBI Registered Investment Adviser (RIA) | Client-paid fee only; no product commissions | Structurally conflict-free |

| AMFI-registered distributor | Trail commissions from fund houses | May recommend products that pay more, not products that fit best |

| Private bank relationship manager | Salary + internal product incentives | Institutional selling pressure documented |

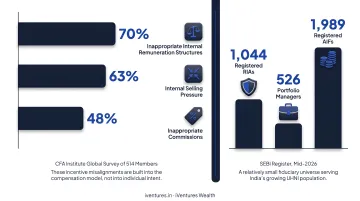

CFA Institute's global survey of 514 members found that 70% cited inappropriate internal remuneration structures, 63% cited internal selling pressure, and 48% cited inappropriate commissions as causes of mis-selling. These incentive misalignments are built into the compensation model — they exist regardless of any individual advisor's intentions.

As of mid-2026, SEBI's register lists 1,044 registered RIAs against 526 portfolio managers and 1,989 registered AIFs — a relatively small fiduciary advisory universe serving India's growing UHNI population.

What to Evaluate When Selecting an Advisor

Given that fiduciary advisors remain scarce relative to India's UHNI population, knowing what to look for narrows the field quickly:

- SEBI RIA registration — verifiable on the SEBI intermediary lookup at sebi.gov.in

- Open-architecture product access — ability to recommend across the full PMS, AIF, equity, debt, and global fund universe

- Experience with large liquidity events — demonstrated familiarity with tax coordination, 54F windows, and estate planning integration

- Team depth — CFA-qualified research and in-house compliance capability

- Fee transparency — written confirmation of no trail commissions, referral fees, or product-linked income of any kind

iVentures Wealth (SEBI RIA INA000019026) meets each of these criteria — CFA-led research, open-architecture access, and 20+ years of post-exit work spanning three-bucket liquidity deployment, family trust establishment, 54F/54EC tax planning, and global portfolio construction, coordinated alongside the founder's CA and legal counsel.

Frequently Asked Questions

What are the exit opportunities for private wealth management?

Post-exit, founders gain access to institutional-grade instruments: PMS (minimum ₹50 lakh), AIFs (minimum ₹1 crore), private credit, global funds, and family office services — entry points most retail investors never reach. A SEBI-registered RIA navigates this universe without product shelf bias, recommending across the full market on a fee-only basis.

How is capital gains tax calculated on a founder's exit from a private company in India?

For unlisted shares held over 24 months, LTCG applies at 12.5% without indexation (effective 13.00%–14.95% after surcharge and cess, for transfers on or after 23 July 2024). Shares held 24 months or less attract STCG at the founder's applicable slab rate. Tax planning initiated before the deal closes can materially reduce the final burden.

How soon before an exit should a founder start wealth management planning?

Ideally 12–24 months before the transaction. This window allows time for shareholding restructuring, estate planning, tax positioning, and advisor selection — founders who engage a SEBI-registered RIA before proceeds are received consistently preserve more net wealth than those who act after.

What is the difference between a SEBI RIA and a wealth distributor for post-exit planning?

A SEBI RIA earns fees only from clients and is legally prohibited from earning product commissions, making them structurally conflict-free. A distributor earns trail commissions from fund houses and may recommend products that pay them more rather than products that fit best. For large post-exit corpuses, this distinction directly affects long-term net returns.

How can Indian founders transfer exit wealth to the next generation tax-efficiently?

Private Family Trusts, registered Wills, and HUF structures are the primary vehicles, each with distinct tax treatment. Discretionary trusts risk maximum marginal rate taxation; HUF transfers of self-acquired property trigger clubbing provisions. Legal and wealth advisors should work in coordination, not in isolation.

What should a founder do with exit proceeds in the first 90 days?

Park proceeds in low-risk liquid instruments (liquid funds or short-duration debt) while completing a structured goal-setting and tax review with a SEBI-registered RIA. Avoid rushing into new ventures, real estate, or equity markets under time pressure. The 90-day window is for planning and positioning, not deployment.