Choosing the wrong vehicle doesn't just cost returns. It can mean locking up capital you need, paying taxes you could have deferred, or missing out on asset classes your portfolio genuinely requires.

This article breaks down the structural differences, tax implications, and situational fit of PMS versus AIF — so you can make this decision with clarity.

Key Takeaways

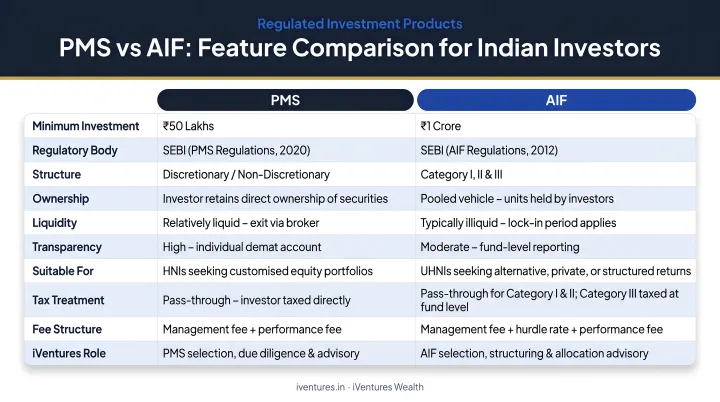

- PMS offers direct ownership of listed securities in your own demat account; SEBI minimum is ₹50 lakh

- AIF is a pooled vehicle giving access to private equity, structured credit, and hedge strategies; minimum is ₹1 crore

- PMS suits HNIs who want equity alpha, transparency, and flexibility to exit

- AIF suits UHNIs willing to lock capital for 5–10 years in exchange for returns uncorrelated with public markets

- Both are SEBI-regulated — the right choice depends on your corpus size, lock-in tolerance, and tax objectives

PMS vs AIF: Quick Comparison

| Feature | PMS | AIF |

|---|---|---|

| Structure | Individually managed; separate demat per investor | Pooled trust structure; investor holds fund units |

| Minimum Investment | ₹50 lakh (SEBI mandated) | ₹1 crore (₹25 lakh for Angel Funds) |

| Ownership | Direct ownership of underlying securities | Indirect ownership via fund units |

| Liquidity | Relatively high; exit within days (exit loads up to 3% in year one) | Low; Category I & II: 3–10 year lock-ins; Category III: quarterly windows |

| Taxation | Taxed directly in investor's hands | Category I & II: pass-through; Category III: fund-level |

| Best For | HNIs seeking personalised equity portfolios with full visibility | UHNIs and family offices seeking institutional alternative strategies |

What Is PMS?

Portfolio Management Services is a professionally managed portfolio of listed equities, fixed income, or structured products — held in your own demat account, with the manager operating through a Power of Attorney. Unlike mutual funds or AIFs, you retain direct ownership of every security. If the manager buys Infosys, it sits in your demat account — not in a pooled structure.

Discretionary vs Non-Discretionary PMS

SEBI recognises two models:

- Discretionary PMS: The portfolio manager makes all investment decisions independently. This is the most widely adopted model for high-conviction, long-term equity strategies

- Non-Discretionary PMS: The manager advises, but you approve each trade — less practical for active strategies

Most HNIs opt for discretionary PMS, where the manager's expertise drives execution without requiring constant investor involvement. That hands-off structure is also what makes PMS well-suited for long-term wealth building.

Why PMS Works for Long-Term Wealth Creation

The structural advantages speak for themselves:

- Concentrated, high-conviction portfolios designed to generate alpha over benchmark indices

- Real-time visibility — every holding, dividend, and corporate action accessible in your demat account

- Customisation to your sector preferences, risk appetite, and financial timeline

- Tax efficiency — since securities are held directly, you control when gains are realised

Fee structure: PMS managers typically charge 2–3% as a management fee, plus a performance-linked fee above a hurdle rate. The High Water Mark mechanism ensures managers can only charge performance fees on gains that exceed the portfolio's previous peak value — you pay for real new wealth created, not a recovery of previous losses.

Who Should Use PMS

PMS works best for founders, CXOs, and professionals with a corpus in the ₹50 lakh to ₹5 crore range who want a personalised equity strategy aligned with long-term goals — retirement, business exit proceeds, or generational wealth.

PMS industry AUM reached ₹42.2 lakh crore in April 2026, up from ₹40.3 lakh crore in September 2025 — roughly 9% year-on-year growth, with 520 SEBI-registered portfolio managers as of June 2026. That trajectory signals a maturing market, not a niche product.

What Is AIF?

Alternative Investment Funds are pooled vehicles regulated under the SEBI (Alternative Investment Funds) Regulations, 2012. A professional fund manager pools capital from multiple investors and deploys it across asset classes that have no equivalent in PMS or mutual funds. You receive units in the fund rather than direct ownership of the underlying assets.

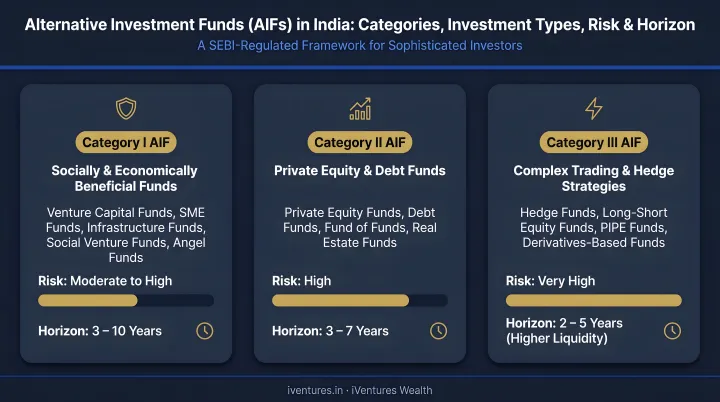

The Three AIF Categories

Each category serves a distinct investment purpose:

- Category I: Venture capital, angel funds, SME funds, infrastructure, and social impact funds. High risk, long horizon, early-stage exposure

- Category II: Private equity, real estate, debt, and distressed-asset funds. Moderate risk with a blend of yield and capital appreciation

- Category III: Hedge funds, long-short equity, PIPE funds, and quantitative strategies. Aims for absolute returns across market cycles; taxed at the fund level

Why AIF Works for Long-Term Wealth Creation

The core value proposition is access — to strategies and asset classes that don't exist in listed markets:

- Private equity and pre-IPO exposure before public market pricing

- Structured credit and private credit AIFs delivering targeted IRRs of 12–16%

- Hedge and long-short strategies that can generate returns uncorrelated to Nifty's direction

For HNI and UHNI clients, private credit AIFs have emerged as a direct response to compressing fixed deposit rates. Senior secured private credit funds — with first-lien collateral backing — typically target IRRs of 12–16%, delivering predictable, inflation-beating cash flows that traditional debt instruments no longer can.

That yield advantage, however, comes with a trade-off: these allocations must be treated as long-duration, illiquid capital.

Liquidity and Lock-In: What You Need to Know

This is non-negotiable: only allocate capital to AIFs that you will not need in the medium term.

- Category I and II AIFs are close-ended with a minimum 3-year tenure; real-world fund lives often run 5–10 years

- Category III AIFs may be open-ended but frequently carry quarterly redemption windows or lock-in clauses

- There is no secondary market liquidity comparable to listed equities

The scale of the AIF market validates its institutional credibility. Total AIF commitments raised reached ₹15.74 lakh crore as of December 2025, with 1,939 registered AIFs as of June 2026 — compared to ₹4.51 lakh crore in commitments just five years earlier.

Who Should Use AIF

AIFs are suited for UHNIs, family offices, and institutional investors with ₹1 crore or more available for long-duration, illiquid allocations. NRIs can also access AIFs through NRE/NRO accounts subject to SEBI and RBI regulations. GIFT City-domiciled AIFs offer an additional advantage: USD-denominated structures that allow NRIs to benchmark returns globally without complex currency management.

PMS vs AIF: Which Is Better for Long-Term Wealth Creation?

Neither vehicle is universally superior. The right answer depends on four factors:

- Investable corpus — ₹50 lakh threshold for PMS; ₹1 crore for AIF

- Liquidity horizon — can you commit capital for 5–10 years without needing it?

- Return objective — listed equity alpha vs. private market or alternative strategies

- Tax efficiency — pass-through status in Category I/II vs. fund-level taxation in Category III

When to Choose PMS

Choose PMS if you want direct equity ownership with full transparency, portfolio customisation, and the flexibility to exit or rebalance across market cycles. It's the natural vehicle for building a concentrated equity portfolio aligned with India's long-term growth story, particularly for investors in the ₹50 lakh to ₹5 crore range.

When to Choose AIF

Choose AIF if you need access to private equity, venture capital, structured credit, or hedge strategies unavailable through listed markets — and can commit that capital for 5–10 years. The lock-in isn't a design flaw; it's what enables fund managers to capture illiquidity premiums that listed market investors simply cannot access.

The Tax Efficiency Dimension

Net-of-tax returns are what actually compound your wealth over time — gross figures can mislead.

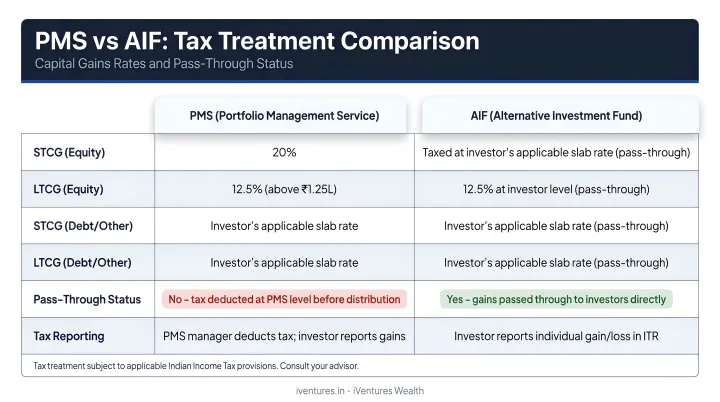

- PMS: Long-term capital gains on equity (held more than 12 months) are taxed at 12.5% on gains above ₹1.25 lakh; short-term gains are taxed at 20% — both assessed directly in the investor's hands

- Category I & II AIF: Pass-through taxation under Section 115UB of the Income Tax Act means income retains its character and is taxed in the investor's hands at applicable rates

- Category III AIF: No specific dedicated tax regime; depending on structure, fund-level taxation at the maximum marginal rate may apply — readers should confirm current applicability with a qualified tax adviser for their specific situation

The pass-through status of Category I and II AIFs is a meaningful structural advantage. The tax treatment of Category III AIFs warrants careful modelling before committing capital.

The Complementary Portfolio Approach

The strongest long-term wealth strategies use both PMS and AIF deliberately, each serving a distinct role.

- PMS anchors the portfolio: liquid, transparent, and built around concentrated equity alpha

- AIF broadens it: private market access, alternative strategies, and return streams that don't move in lockstep with listed equities

Structuring this dual allocation requires more than product knowledge. It requires mapping your tax position, liquidity constraints, and how these vehicles interact across your full financial plan. At iVentures Wealth, a SEBI-registered fee-only RIA with 20+ years advising UHNIs, family offices, and founders, every PMS and AIF recommendation follows rigorous due diligence — with no placement commissions accepted from either side. That structure keeps the analysis grounded in client suitability and investment merit alone.

Frequently Asked Questions

Is AIF better than PMS?

Neither is universally better. AIF offers access to alternative assets and non-correlated strategies suited for UHNIs willing to lock in capital, while PMS offers direct equity ownership, flexibility, and transparency for HNIs focused on listed equity wealth creation. The right choice depends on corpus size, liquidity needs, and investment objectives.

Which type of mutual fund is best suited for long-term wealth creation?

Equity-oriented mutual funds — large-cap, flexi-cap, or index funds — work well for most investors building wealth through diversification and tax efficiency. Investors with larger corpuses seeking higher alpha or customization typically move to PMS (₹50 lakh+) or AIF (₹1 crore+).

What is the minimum investment for PMS and AIF in India?

SEBI mandates a minimum of ₹50 lakh for PMS and ₹1 crore for AIF. Angel Funds under Category I have a lower minimum of ₹25 lakh, limited to eligible angel investors.

Can NRIs invest in PMS and AIF in India?

Yes. NRIs can invest in both PMS and AIF subject to SEBI and RBI regulations. GIFT City AIFs are increasingly attractive for NRIs given the ability to invest in USD-denominated structures and access favourable tax treatment under the IFSC framework — making them a practical option for those managing cross-border wealth.

How are PMS and AIF taxed differently?

PMS gains are taxed directly in the investor's hands as capital gains — 12.5% for long-term equity gains above ₹1.25 lakh, 20% for short-term. Category I and II AIFs have pass-through status, with income taxed in the investor's hands. Category III AIFs may be subject to fund-level taxation depending on structure. Consult a tax adviser for your specific situation.

Can an investor hold both PMS and AIF in their portfolio?

Yes, and many sophisticated investors do. PMS typically serves as the core listed equity allocation for transparency and flexibility, while AIF serves as the satellite allocation for private market exposure or non-correlated returns. Together, they can improve risk-adjusted returns and reduce concentration risk across a portfolio.