Both vehicles promise sophisticated, research-driven strategies. Both target HNIs and UHNIs. But they work very differently — in structure, regulation, risk, liquidity, and tax treatment. Confusing one for the other can mean locking up capital you need, paying fees that aren't justified, or taking on risk your portfolio can't absorb.

This article breaks down exactly how PMS and hedge funds differ across every dimension that matters: ownership, regulation, returns, fees, liquidity, taxation, and investor fit. By the end, you'll have a clear framework for deciding which vehicle belongs in your portfolio — and whether you need both.

Key Takeaways

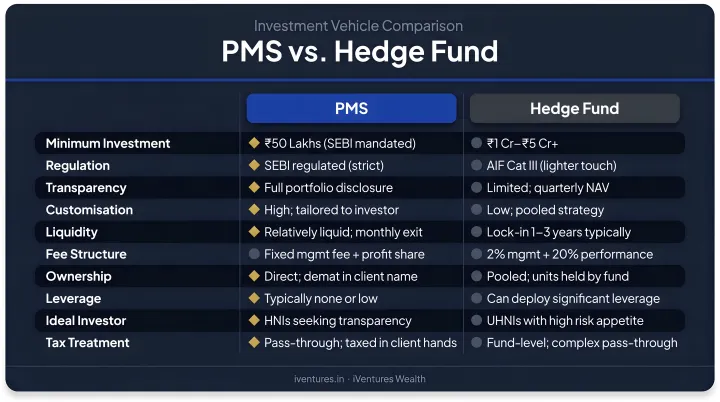

- PMS: SEBI-regulated, individually managed accounts where you directly own the securities — minimum ₹50 lakh

- Hedge funds (Category III AIFs): Pooled, leverage-driven vehicles with a ₹1 crore minimum and significantly higher risk

- PMS suits long-term wealth creation; hedge funds chase absolute returns with greater volatility

- PMS offers better liquidity — hedge funds carry lock-in periods and restricted redemption windows

- Tax treatment differs: PMS gains are taxed in your hands; Category III AIFs are taxed at the fund level, often at higher effective rates

PMS vs Hedge Funds: At a Glance

| Feature | PMS | Hedge Fund (Category III AIF) |

|---|---|---|

| Structure | Individually managed account | Pooled investment vehicle |

| Minimum Investment | ₹50 lakh | ₹1 crore |

| Regulation | SEBI (PM) Regulations, 2020 | SEBI AIF Regulations, 2012 |

| Risk Level | Moderate to high | High to very high |

| Return Expectation | Market-linked, steady | Absolute returns, higher variance |

| Liquidity | Generally high; no mandatory lock-in | Lock-in periods typical; restricted redemptions |

| Fee Model | 1–2% management fee + optional performance fee | 1–2.5% management fee + 15–20% carried interest |

| Transparency | High; individual holding-level reporting | Lower; PPM-based disclosure only |

| Investor Ownership | Direct ownership of securities | Units of the fund; no direct claim on securities |

| Typical Investor | HNIs, CEOs, founders, family offices | Ultra-HNIs, institutional investors, family offices |

What is Portfolio Management Services (PMS)?

PMS is a professionally managed investment service where each client's portfolio is held directly in their own demat account (not pooled with other investors). A portfolio manager constructs and manages a tailored mix of equities, debt, and derivatives based on your specific risk profile and goals. You remain the legal owner of every security in your account.

Two Types of PMS

Discretionary PMS gives the portfolio manager full authority to make investment decisions without seeking client approval for each trade. Most HNIs prefer this because it allows the manager to act quickly and maintain portfolio integrity without administrative delays.

Non-Discretionary PMS positions the manager as an adviser. Every transaction requires your approval before execution. This suits investors who want to stay closely involved in decision-making, though it can slow down execution in fast-moving markets.

Regulatory Framework

PMS in India is governed by the SEBI (Portfolio Managers) Regulations, 2020. Key requirements include:

- Mandatory SEBI registration before operating

- Minimum net worth of ₹5 crore for portfolio managers

- Minimum client investment of ₹50 lakh

- Client reporting at intervals not exceeding 3 months, using Time Weighted Rate of Return (TWRR)

- Mandatory disclosure document covering fees, risks, and related-party transactions

As of April 30, 2026, total PMS AUM in India stood at ₹42,36,467 crore across over 2 lakh discretionary clients. That scale reflects a clear shift: HNIs increasingly want personalised strategies that go beyond what mutual funds can offer.

Use Cases and Taxation

PMS suits investors with ₹50 lakh or more who want a concentrated, research-driven equity portfolio with full visibility into every position — typically CEOs, founders, UHNIs, and family offices building long-term equity wealth.

Tax treatment is straightforward since gains are taxed directly in your hands:

- STCG (equity held under 12 months): 20% under Section 111A

- LTCG (equity held over 12 months): 12.5% on gains above ₹1.25 lakh under Section 112A

These rates apply post-Budget 2024, effective July 23, 2024.

What are Hedge Funds?

In India, hedge fund strategies operate primarily as Category III AIFs under SEBI's Alternative Investment Funds Regulations, 2012. These are privately pooled vehicles that aggregate capital from multiple accredited investors and deploy it using complex, often leveraged strategies unavailable in traditional investment vehicles.

Four Primary Hedge Fund Strategies

| Strategy | How It Works |

|---|---|

| Long/Short Equity | Buys undervalued stocks; shorts overvalued ones to profit from relative performance |

| Global Macro | Takes directional bets on currencies, interest rates, and commodities based on macroeconomic views |

| Market Neutral | Hedges market exposure to profit from relative performance regardless of market direction |

| Arbitrage | Exploits price inefficiencies in mergers, convertibles, or statistical spreads |

Key Features

- Investors hold units of the fund — no direct ownership of individual securities

- Leverage and derivatives are used to amplify returns (and losses)

- Capital is raised through private placement using a Private Placement Memorandum (PPM)

- Minimum ₹1 crore per investor under SEBI AIF Regulations

As of December 31, 2025, Category III AIF commitments in India totalled ₹3,11,944 crore, reflecting growing institutional appetite for hedge-fund-style strategies.

Use Cases and Taxation

Hedge funds suit ultra-HNIs and institutional investors with ₹1 crore or more, a high risk appetite, a longer investment horizon, and a specific need for absolute returns that are uncorrelated with traditional equity markets.

That return potential, however, comes with a tax trade-off. Unlike Category I and II AIFs, Category III AIFs do not have pass-through tax status under Section 115UB of the Income Tax Act — tax is levied at the fund level, which can result in considerably higher effective rates:

- Listed equity STCG: ~23.92% effective rate (20% base + 15% capped surcharge + 4% cess)

- Derivative/business income: Up to ~42.744% at maximum marginal rate (including surcharge and cess)

Actual rates depend on fund structure, income characterisation, and investor status. A qualified tax adviser should review these implications before you commit capital.

PMS vs Hedge Funds: Key Differences Explained

Ownership and Structure

In PMS, every security sits in your personal demat account. You are the legal owner. This has real implications beyond semantics — you can see your holdings in real time, exit specific positions independently, and include securities directly in estate planning.

In a hedge fund, you hold units of a pooled fund. There's no direct claim on any individual security. The fund manager controls all investment decisions, and your rights are governed by the PPM rather than direct ownership.

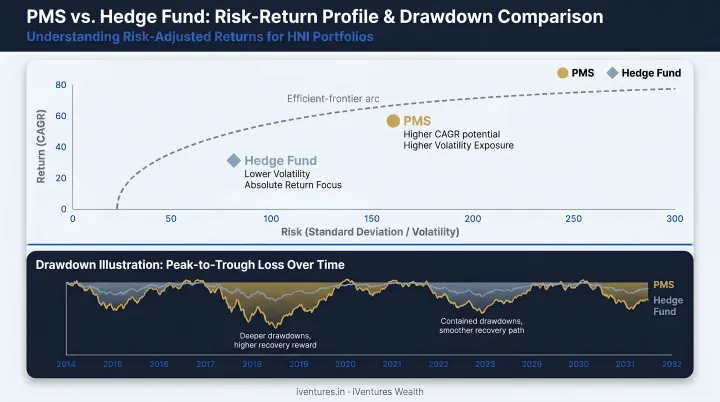

Risk and Return Profile

According to data from PMSBazaar, the average 5-year PMS return across tracked strategies was 18.99% as of March 2024. The CRISIL AIF Index for Category III showed a 5-year return of 18.6% as of September 30, 2025.

The numbers look similar at first glance, but the path to those returns is very different:

- PMS generates returns through concentrated equity positions within a defined risk mandate

- Hedge funds use leverage and complex instruments — amplifying both gains and losses. A market dislocation that causes 15% drawdown in PMS could cause significantly more in a leveraged Category III AIF

Liquidity

PMS investors can generally exit positions as market liquidity allows — no mandatory lock-in, though exit loads may apply in the early years. This matters if you're a founder who may need to access capital for a business opportunity or family event.

Hedge funds impose lock-in periods (close-ended schemes require a minimum tenure) and restrict redemption windows to defined periods under the fund's PPM. Size your Category III AIF allocation accordingly: treat that capital as illiquid for the full duration of the lock-in.

Fee Structures

| PMS | Category III AIF | |

|---|---|---|

| Management Fee | 0.25–2.5% of AUM annually | 1–2.5% of AUM annually |

| Performance Fee | Optional; linked to hurdle rate | 15–20% of profits above hurdle |

| Carried Interest | Less common | Standard feature |

The higher fee structure in hedge funds is only justifiable if returns consistently exceed the hurdle rate after fees. A 20% carry on profits sounds reasonable when the fund delivers 25% — it looks very different when it delivers 12%.

Regulatory Transparency

PMS operates under heavy SEBI oversight: mandatory periodic reporting, individual holding-level disclosures, and direct accountability to each client. Reporting intervals cannot exceed 3 months.

Category III AIFs disclose portfolio information through periodic reports under SEBI's Master Circular, but are not required to make portfolio composition public. That gives fund managers strategic flexibility, though it comes at the cost of your visibility as an investor.

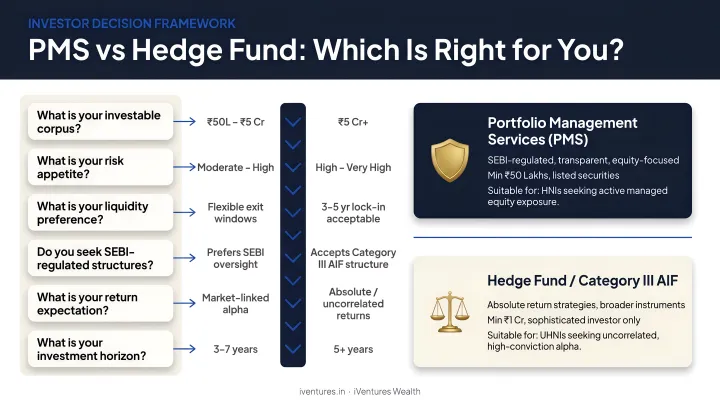

Which is Right For You: PMS or Hedge Fund?

The answer depends on four variables: investable surplus, risk tolerance, investment horizon, and your need for control.

Choose PMS if you:

- Want direct ownership of securities with full transparency

- Prefer SEBI-regulated, individually tailored portfolio management

- Need reasonable liquidity without mandatory lock-ins

- Are building steady, long-term equity wealth with a defined risk profile

- Have ₹50 lakh or more to invest

Choose a hedge fund if you:

- Have ₹1 crore or more and can commit it for the lock-in period

- Have a high risk appetite and want exposure to absolute-return strategies

- Want returns that are less correlated to equity market movements

- Understand the fee structure and higher effective tax rate at the fund level

That said, for many UHNIs and family offices, this isn't an either/or decision. A well-structured portfolio often uses PMS as the core equity allocation — transparent, regulated, and flexible — with a Category III AIF as a satellite position targeting absolute returns. iVentures Wealth's portfolio construction framework positions both vehicles as serving distinct roles within the same wealth plan, not competing for the same allocation.

Navigating these decisions — evaluating fund managers, stress-testing fee structures against realistic return scenarios, and integrating both vehicles into a tax-efficient wealth plan — is where an independent, SEBI-registered adviser adds genuine value.

iVentures Wealth's CFA-led research team has been advising UHNIs, founders, and family offices on these decisions for 20+ years, operating on a fee-only model with no placement commissions from PMS providers or AIF managers.

Frequently Asked Questions

Is PMS like a hedge fund?

Both target HNIs and are professionally managed, but they're structurally different. PMS is an individually managed account where you directly own the securities, governed by SEBI's Portfolio Managers Regulations. Hedge funds pool capital from multiple investors and use complex strategies like leverage and short-selling, with lighter transparency requirements.

What are the 4 types of hedge funds?

The four main strategies are:

- Long/Short Equity — buying undervalued stocks while shorting overvalued ones

- Global Macro — directional bets on currencies, interest rates, and commodities

- Market Neutral — hedging market exposure to profit from relative performance

- Arbitrage — exploiting price inefficiencies in mergers or statistical spreads

What is the minimum investment for PMS and hedge funds in India?

SEBI mandates a minimum of ₹50 lakh for PMS and ₹1 crore for Category III AIFs (hedge funds). The higher threshold for hedge funds reflects the greater complexity, risk, and investor sophistication these vehicles assume.

How are PMS and hedge funds taxed differently in India?

PMS gains are taxed directly in your hands — STCG at 20% and LTCG at 12.5% above ₹1.25 lakh. Category III AIFs are taxed at the fund level (not pass-through), pushing effective rates to ~23.92% on listed equity STCG and up to ~42.744% on derivative income.

Which is better for long-term wealth creation: PMS or hedge funds?

PMS is generally better suited for steady, long-term equity wealth creation with low liquidity risk and full transparency. Hedge funds suit investors seeking absolute, uncorrelated returns over a defined lock-in horizon. Match the vehicle to your risk tolerance, investment horizon, and tax position — not the other way around.

Can NRIs invest in PMS and hedge funds in India?

Yes — NRIs can invest in both PMS and Category III AIFs in India through NRE or NRO accounts, subject to SEBI regulations and FEMA compliance after completing KYC. Repatriation terms and tax treatment vary by account type, so FEMA-compliant structuring matters before committing capital.