Introduction

India's PMS industry now has 517 registered portfolio managers as of May 2026, managing a total AUM of ₹41.42 lakh crore — yet the number that matters most to private HNI investors is the non-EPFO/PF figure of ₹7.99 lakh crore, growing at 11.7% year-on-year. Client registrations crossed 2.15 lakh in March 2026, reflecting steady demand from affluent investors who want more than what mutual funds offer.

With hundreds of providers competing for attention, even sophisticated investors face a specific problem: SEBI registration gets cited loosely, and it's not always clear what it actually commits a portfolio manager to — or what protections you're entitled to as a client.

This guide covers:

- What SEBI registration actually commits a portfolio manager to

- The three service types defined under PMS regulations

- Key investor protections you can enforce

- A practical framework for verifying and selecting the right provider — including when to work with an independent adviser before committing capital

Key Takeaways

- Only corporate entities with SEBI's INP registration can legally offer PMS in India

- SEBI mandates a ₹50 lakh minimum investment, independent custody, quarterly TWRR reporting, and no upfront fees

- Three service models exist: Discretionary (manager decides), Non-Discretionary (client approves), and Advisory (client executes)

- No lock-in is permitted; exit loads are capped at 3% in Year 1, reducing to nil after Year 3

- Always verify the specific INP registration on sebi.gov.in, as not all "SEBI registered" claims refer to PMS

What Is a SEBI-Registered Portfolio Manager?

Portfolio Management Services involve a licensed entity managing a client's investment portfolio — equities, bonds, and other securities — under a formal agreement. The manager may act independently or based on client direction, depending on the service type selected.

SEBI registration is not a badge of prestige. It is a mandatory legal requirement under the SEBI (Portfolio Managers) Regulations, 2020. Any entity offering PMS without this registration is operating illegally.

Who Can Register

SEBI permits only body corporates — companies or LLPs — to register as portfolio managers. Individuals cannot apply. Key requirements include:

- Minimum net worth of ₹5 crore at all times (Regulation 9)

- A qualified Principal Officer with 5+ years of securities market experience and at least 2 years in portfolio management or investment advisory, plus NISM Series XXI-B certification

- A designated Compliance Officer

- Adequate operational infrastructure

What Registration Commits a Manager To

SEBI registration is not a one-time hurdle — it creates ongoing obligations that protect investors at every stage:

- Full upfront disclosure of fees, strategies, and risk factors in a standardised disclosure document

- Mandatory client agreements before any funds are accepted

- Independent custody of client assets through a SEBI-registered custodian

- Periodic audits subject to SEBI oversight

- Prohibition on guaranteed returns or misleading performance claims

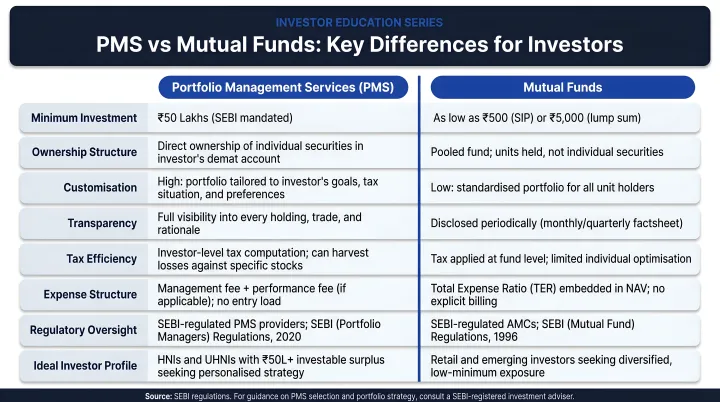

PMS vs. Mutual Funds: A Critical Distinction

| Feature | PMS | Mutual Fund |

|---|---|---|

| Asset ownership | Direct, in client's demat | Units in a pooled fund |

| Customisation | High — portfolio tailored to client | Low — standardised fund mandate |

| Minimum investment | ₹50 lakhs | As low as ₹500 |

| Transparency | Full holdings visibility | NAV-level disclosure |

| Tax-loss harvesting | Possible | Not available to investor |

In PMS, you own individual securities in your own name. This matters practically: you can harvest tax losses on specific holdings, instruct the manager to avoid certain sectors, and see exactly what you hold at any point. A pooled mutual fund structure offers none of that granularity.

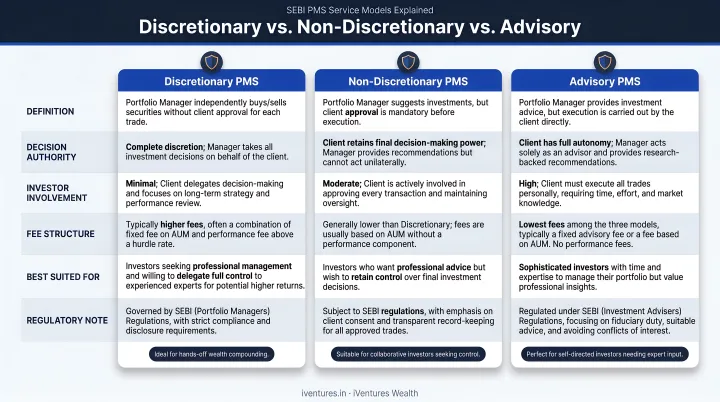

Types of PMS Services in India

The Three Service Models

SEBI defines three service types, each suited to a different investor profile:

Discretionary PMS — The manager has full authority to make buy and sell decisions within the agreed mandate. No client approval is needed per transaction. This is the dominant model, accounting for 84.8% of total AUM and 95.6% of all PMS clients as of March 2026. Suited to investors who want professional management with minimal day-to-day involvement.

Non-Discretionary PMS — The manager recommends trades; the client approves each transaction before execution. Suited to investors who want professional analysis but prefer to retain final decision-making authority.

Advisory PMS — The manager provides advice only. All execution and ownership decisions rest with the client. This is not portfolio management in the active sense — the manager carries no execution responsibility. As of March 2026, only 1,229 clients use this model.

These three models differ in control, not in the underlying assets they can hold. The asset class breakdown adds another layer of choice.

PMS by Asset Class

| Category | Focus | Risk Profile |

|---|---|---|

| Equity PMS | Listed and some unlisted shares | Higher risk, growth-oriented |

| Debt PMS | Bonds, government securities | Lower risk, income-oriented |

| Hybrid PMS | Mix of equity and debt | Moderate risk |

| Multi-Asset PMS | Equities, REITs, InvITs, gold, alternatives | Diversified, varies |

Under Non-Discretionary PMS, Regulation 24(4) permits up to 25% of client AUM in unlisted securities. Large-value investors may have up to 100% in unlisted securities under specific conditions.

Key SEBI Regulations Every PMS Investor Must Know

Minimum Investment and Fee Rules

₹50 lakh minimum: SEBI prohibits portfolio managers from accepting investments below ₹50 lakhs per client (Regulation 23(2)). This threshold doubled from ₹25 lakhs under the 2020 regulations. Partial withdrawals are permitted but cannot reduce the portfolio below this floor. Accredited investors are exempt.

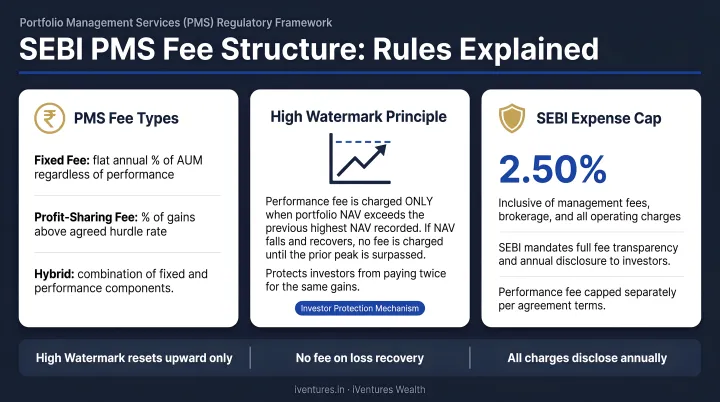

Fee structure rules under Regulation 22:

- Fixed management fee, performance fee, or a combination — all permitted

- No upfront fees — explicitly prohibited under Regulation 22(11)

- Performance fees must follow the high-watermark principle: fees only apply when portfolio value exceeds its previous peak. In practice, if a ₹1 crore portfolio drops to ₹80 lakhs, the manager earns no performance fee until the portfolio recovers past ₹1 crore and generates gains beyond that level

- Operating expenses (excluding brokerage) are capped at 0.50% per annum of average daily AUM

Asset Safety and Reporting

Independent custodian requirement: SEBI mandates that client assets be held by an independent custodian — not by the portfolio manager (Regulation 26). This separation means the manager cannot touch, pledge, or co-mingle client funds. For any manager that cannot clearly identify their custodian arrangement, treat that as a serious warning sign.

Portfolio managers must provide performance reports at least once every three months. Discretionary PMS performance must be disclosed using the Time-Weighted Rate of Return (TWRR) methodology for the preceding three years.

TWRR eliminates the distortion caused by cash flows in or out, making performance figures comparable across managers — critical when evaluating multiple providers side by side.

Investor Protections Against Abuse

SEBI's 2020 PMS Circular explicitly prohibits:

- Guaranteed or indicative returns — any manager promising specific returns is violating SEBI rules

- Lock-in periods — no manager can prevent you from exiting. However, exit loads are permitted:

| Redemption Year | Maximum Exit Load |

|---|---|

| Year 1 | 3% of amount redeemed |

| Year 2 | 2% of amount redeemed |

| Year 3 | 1% of amount redeemed |

| Year 4+ | Nil |

- Excessive associate brokerage — brokerage through self or associates is capped at 20% by value per associate per service annually, and must not exceed rates charged by non-associate brokers

Benefits of Investing Through a SEBI-Registered PMS Provider

Regulatory Protection With Real Teeth

A SEBI-registered portfolio manager is legally bound to act in your interest, disclose conflicts, and maintain compliance records subject to SEBI audits. An unregistered advisor carries none of these obligations — no disclosure requirements, no custodian mandate, no performance reporting standards.

For registered managers, SEBI's SCORES platform (scores.sebi.gov.in) provides a centralised grievance mechanism. Investors can file complaints online, and portfolio managers — as registered intermediaries — are required to respond within defined timelines.

Direct Ownership and Personalisation

Unlike mutual funds, PMS gives you direct ownership of individual securities in your demat account. This has three practical advantages:

- Tax-loss harvesting — losses on specific positions can be realised strategically to offset gains

- Custom mandates — exclusions, sector preferences, ESG criteria can be built into the portfolio

- Transparent holdings — you see exactly what you own, not just a NAV

According to SEBI's PMS data, the PMS client base has grown steadily year-on-year, reflecting the structural shift of affluent investors toward direct ownership models.

Professional Management Standards

SEBI's credential requirements for Principal Officers set a meaningful baseline: 5+ years in securities markets, at least 2 years in portfolio management or investment advisory, and ongoing NISM certification. All three are mandatory conditions for obtaining and retaining registration.

For investors who want additional support evaluating PMS options, working with a SEBI-registered investment adviser adds an independent layer of analysis. iVentures Wealth (SEBI RIA INA000019026), with 20+ years of experience, provides conflict-free PMS evaluation through a CFA-led research team that assesses risk-adjusted metrics — including Sharpe and Sortino ratios — rather than just headline returns.

Because iVentures operates on a fee-only model, it cannot accept commissions from product manufacturers. Recommendations are based purely on suitability and fit with a client's overall financial plan.

How to Verify and Choose the Right SEBI-Registered PMS Provider

Verifying SEBI Registration

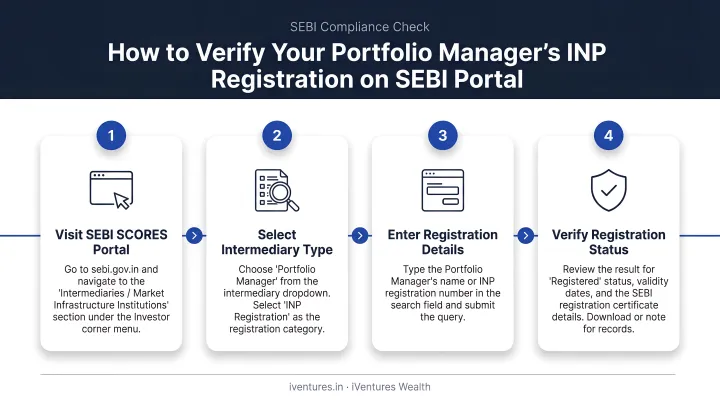

Before committing capital to any PMS provider, verify their registration directly on SEBI's portal. Here's how:

- Go to sebi.gov.in

- Navigate to Intermediaries / Market Infrastructure Institutions → Recognised Intermediaries → Registered Portfolio Managers

- Use the search function to look up by company name or registration number

- Confirm the registration number begins with INP (e.g., INP000008464), shows active status, and matches the entity you're dealing with

Common oversight to avoid: A provider calling themselves "SEBI registered" may hold a different registration type. Investment Advisers carry an INA prefix — a completely different licence category. INP (Portfolio Manager) and INA (Investment Adviser) are governed by separate regulations with distinct mandates. Always verify the specific INP registration, not just the claim.

Once registration is confirmed, the next step is assessing whether the strategy actually fits your goals.

Evaluating the Right PMS for Your Goals

Evaluate on these criteria:

- Investment philosophy fit — does the strategy align with your goals and risk tolerance?

- Track record across cycles — look at 5+ years, including periods of market stress, not just recent bull-run performance

- Fee transparency — understand the split between management fees and performance fees, and check for any hidden transaction charges

- Team stability — has the investment team that built the track record stayed in place?

- Reporting quality — are reports clear, timely, and benchmarked appropriately?

Red flags that should stop any serious investor:

- Promises of guaranteed or unusually high returns

- Vague or missing disclosure document

- No independent custodian arrangement

- Fee structures that are difficult to understand or not disclosed in writing

- Absence from SEBI's official intermediary list

A SEBI-registered investment adviser operating under fiduciary obligations removes conflicts of interest when comparing PMS strategies — their only financial interest is the advisory fee the client pays directly, not placement commissions. iVentures Wealth evaluates PMS strategies through this lens: CFA-led due diligence, integrated into each client's broader financial plan, with no incentive to favour one manager over another.

Frequently Asked Questions

Is PMS regulated by SEBI?

Yes. Portfolio Management Services are regulated under the SEBI (Portfolio Managers) Regulations, 2020. All entities offering PMS must hold a valid SEBI registration and are subject to ongoing compliance requirements, periodic audits, and comprehensive investor protection rules.

How can I check if a portfolio manager is SEBI-registered?

Visit sebi.gov.in, navigate to Intermediaries → Recognised Intermediaries → Registered Portfolio Managers, and search by name or registration number. A valid registration will show an INP-prefix number with active status and matching entity details.

What is the starting amount for PMS?

SEBI mandates a minimum investment of ₹50 lakhs per client, increased from ₹25 lakhs under the 2020 Regulations. Partial withdrawals are permitted, but the portfolio value cannot fall below ₹50 lakhs. Accredited investors are exempt from this threshold.

What is the 5% portfolio rule in PMS?

No such rule exists in SEBI's PMS framework. A 5% concentration limit applies to mutual funds and certain FPI mandates — not portfolio managers. The actual PMS constraints are the 25% unlisted securities cap under Regulation 24(4) and the 20% associate brokerage cap. References to a "5% PMS rule" in marketing materials are typically conflated from mutual fund regulations.

Are there SEBI limits on PMS AUM or portfolio size?

SEBI imposes no ceiling on total AUM a registered portfolio manager can manage. The binding constraints are a ₹50 lakhs minimum per client, a 25% cap on unlisted securities (under non-discretionary/advisory mandates), and a 20% per-associate limit on annual brokerage and transaction charges.