Getting this wrong carries real consequences: a flat 30% TDS deducted before your interest even reaches you, potential FEMA penalties for non-compliance, and double taxation if you don't proactively claim treaty benefits.

This guide covers everything you need: the full NRO tax picture, DTAA relief mechanisms, the NRO vs NRE decision, and how to structure your India-based income efficiently.

Key Takeaways

- NRO accounts are mandatory for NRIs receiving India-sourced income (rent, dividends, interest, salary)

- Banks deduct TDS at 30% plus surcharge and 4% cess automatically—before crediting your income

- DTAA provisions can reduce your effective rate to 10–15% for residents of 90+ countries—but require proactive claiming

- NRO repatriation is capped at USD 1 million per financial year; NRE funds are fully repatriable and tax-exempt

- Filing an ITR in India is still necessary—even after TDS—and can generate a refund if total income falls below the exemption threshold

What Is an NRO Account and Who Needs One?

An NRO (Non-Resident Ordinary) account is a rupee-denominated bank account available in savings, current, or fixed deposit form. Under the RBI's Master Circular on NRO accounts, it exists specifically for persons resident outside India to conduct bona fide rupee transactions—covering income due from Indian sources such as rent, dividends, pension, and interest.

Who Must Open One

Under the Income Tax Act, 1961, Section 6 determines residency through day-count tests. The applicable threshold depends on your situation:

- 182 days in India during the relevant financial year (general rule)

- 60 days in the current year plus 365 days across the preceding four years

- 120 days for Indian citizens or PIOs with Indian-source income exceeding ₹15 lakh—tightened by Finance Act 2020

Once you become an NRI under these tests, any India-sourced income—rent, consulting fees, dividends—must flow through an NRO account. You must also redesignate your existing resident savings account as an NRO account upon acquiring NRI status.

Failing to do so constitutes a FEMA contravention. Under FEMA Section 13, penalties can reach up to 3x the sum involved where quantifiable, or up to ₹2 lakh otherwise, with ₹5,000 per continuing day thereafter.

Key Account Features

- Joint holding: Can include a resident Indian on a "former or survivor" basis

- Power of attorney: A resident Indian can operate the account on your behalf

- Investment access: NRO funds can be deployed into fixed deposits, mutual funds, and Indian equities

- Currency: Held in Indian rupees; inward remittances can be in either INR or foreign currency

The single most important restriction: interest and other income in the NRO account are fully taxable in India, unlike an NRE account.

NRO Account Tax Implications – The Full Picture

The Core TDS Rule

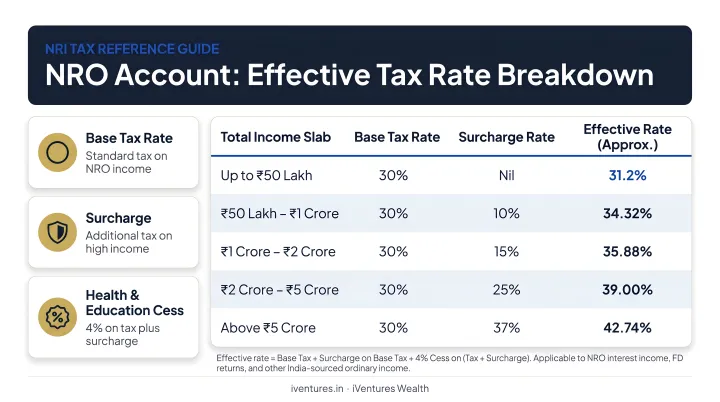

Under Section 195 of the Income Tax Act, banks must deduct tax at source on any interest or sum payable to a non-resident at rates in force. For NRO account interest, the domestic rate is 30%, before surcharge and cess.

A simple illustration:

| Component | Amount |

|---|---|

| Gross NRO FD interest | ₹1,00,000 |

| TDS at 30% | ₹30,000 |

| Net credited to account | ₹70,000 |

And that 30% is the floor, not the ceiling.

Surcharge and Cess: The Real Effective Rate

The 4% health and education cess applies on top of tax plus surcharge. Surcharge slabs for individual NRI taxpayers, per the Income Tax Department's tax rate schedule, are:

| Total Income | Surcharge Rate |

|---|---|

| ₹50 lakh – ₹1 crore | 10% |

| ₹1 crore – ₹2 crore | 15% |

| ₹2 crore – ₹5 crore | 25% |

| Above ₹5 crore | 37% (old regime) / 25% (new regime) |

For a high-income NRI with significant NRO interest, the effective tax rate on interest income can exceed 34–35% after applying the 25% surcharge and 4% cess.

What Income Types Are Taxable in an NRO Account

These rates apply to any income that originates in India. It's the source of income — not your country of residence — that determines taxability:

- Interest on NRO savings accounts and fixed deposits

- Rental income from Indian property

- Capital gains from Indian equities, mutual funds, or real estate

- Consulting fees or salary earned in India

- Dividends from Indian companies

ITR Filing Obligations

TDS being deducted does not eliminate your ITR filing obligation. NRIs with India-sourced income file:

- ITR-2 – for income from house property, capital gains, or other sources

- ITR-3 – if business or professional income is involved

Missing the deadline carries real costs:

- Section 234A interest: 1% per month on unpaid tax

- Section 234F late filing fee: up to ₹5,000 (capped at ₹1,000 if total income is below ₹5 lakh)

The Income Tax Department confirms that excess TDS can only be reclaimed by filing a return within the timeline prescribed under Section 139.

If your total Indian income falls below the basic exemption limit — ₹2.5 lakh under the old regime or ₹3 lakh under the new regime for FY 2024-25 — filing an ITR lets you reclaim the entire TDS deducted.

Section 80TTA Deduction

NRIs can claim a deduction of up to ₹10,000 per year on NRO savings account interest under Section 80TTA. This reduces taxable interest from savings accounts but does not extend to fixed deposit interest.

DTAA: How NRIs Can Reduce Their NRO Tax Burden

How the Mechanism Works

India has signed Double Taxation Avoidance Agreements with over 90 countries. Under these treaties, an NRI can elect to be taxed at the lower of the Indian domestic rate or the applicable DTAA treaty rate on specific income types—particularly interest income from NRO accounts.

For most major countries, the DTAA interest rate is substantially below 30%:

| Country of Residence | DTAA Interest Rate | Source |

|---|---|---|

| USA | 15% (10% for bank loans) | IRS Treaty Text, Article 11 |

| UK | 15% (10% for banks) | GOV.UK Treaty, Article 12 |

| Canada | 15% | Canada Treaty Text, Article 11 |

| Singapore | 15% (10% for banks) | IRAS Treaty Protocol |

For an NRI with ₹10 lakh in NRO FD interest annually, the difference between 30% TDS and a 15% DTAA rate is ₹1.5 lakh—every single year.

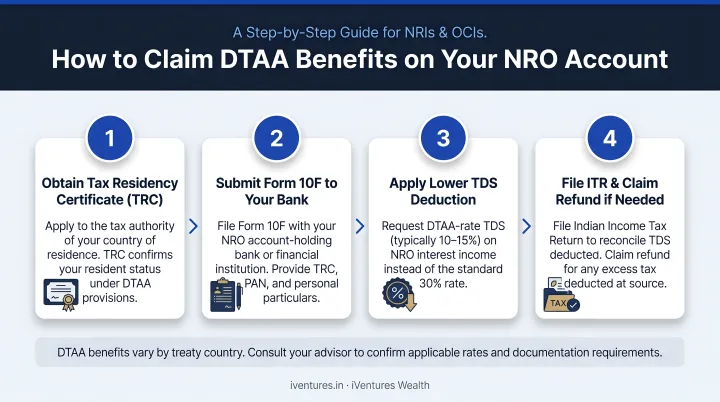

The DTAA Claim Process (Step by Step)

DTAA benefits are not automatic. You must submit documentation to your bank before interest is credited:

- Obtain a Tax Residency Certificate (TRC) from the tax authority in your country of residence — required under Section 90(4) of the Income Tax Act

- Complete Form 10F — required under Section 90(5); since July 2022, filing is electronic via the Income Tax portal, with partial relaxation available for certain non-PAN holders

- Attach a self-attested PAN copy

- Submit all three to your bank before the interest credit date

Once submitted, the bank deducts TDS at the lower DTAA rate. If TDS was already deducted at 30%, you can claim a refund or credit through your ITR.

The Foreign Tax Credit Angle

Successfully claiming the DTAA rate reduces your Indian tax liability, but doesn't always end the story. If India taxes your NRO income first, your country of residence typically allows you to claim a Foreign Tax Credit (FTC) for Indian taxes already paid, preventing double taxation on the same income.

FTC eligibility and mechanics are governed by your resident country's domestic law and the relevant treaty's elimination-of-double-taxation article. For NRIs with significant NRO income, getting this right requires coordinated advice from tax professionals in both countries — the FTC strategy in the US, for instance, works differently from how it applies under the UK or Canada frameworks.

Common DTAA Mistakes to Avoid

- Not submitting TRC before interest is credited (results in automatic 30% deduction)

- Assuming Gulf/UAE residents are automatically exempt (the India-UAE DTAA exists, but specific provisions and documentation requirements apply)

- Not filing an ITR in India at all—and missing the refund opportunity entirely

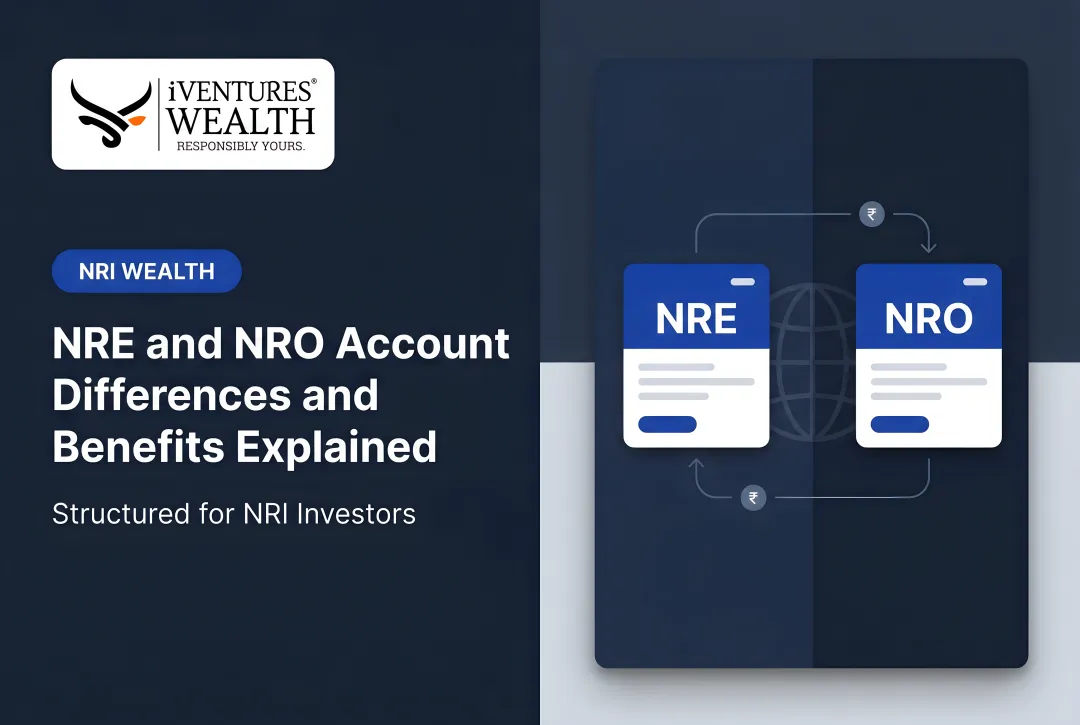

NRO vs NRE: Which Account Works for You?

Side-by-Side Comparison

| Feature | NRO Account | NRE Account | FCNR Account |

|---|---|---|---|

| Currency | Indian Rupees | Indian Rupees | Foreign currency |

| Tax on interest | Taxable at 30% + surcharge + cess | Fully exempt under Section 10(4)(ii) | Exempt under Section 10(15)(iv)(fa) |

| Repatriation | Up to USD 1 million/year (post-tax) | Freely repatriable | Freely repatriable |

| Joint holder | Can include a resident Indian | Must be another NRI | Must be another NRI |

| Best for | India-sourced income | Foreign earnings parked in India | Foreign currency deposits |

The Right Choice Depends on Income Source

- NRO is mandatory for rent, Indian salary, dividends, or capital gains—these cannot legally sit in an NRE account

- NRE is better for foreign earnings you want to hold in India with full tax exemption and repatriation flexibility

- Most NRIs benefit from maintaining both—NRE for foreign-origin income and tax-free interest, NRO for India-sourced income with a structured transfer strategy

Repatriating from NRO: What's Actually Required

Repatriation up to USD 1 million per financial year for legitimate purposes requires:

- Form 15CA filed online by the remitter

- Form 15CB from a Chartered Accountant (exceptions apply under Rule 37BB based on remittance category)

- A declaration confirming applicable taxes have been paid

Transferring NRO funds to an NRE account is permitted within the USD 1 million limit, subject to tax compliance and CA certification. Missing this step is a common oversight that stalls remittances—confirm CA certification requirements with your bank before initiating the transfer.

How iVentures Wealth Helps NRIs Optimise NRO Tax Planning

NRO tax planning doesn't sit in isolation. For NRIs managing significant India-based wealth—rental income, equity portfolios, fixed deposits, or family business interests—it intersects with FEMA compliance, DTAA structuring, Form 15CA/15CB obligations, and cross-border portfolio reporting all at once.

That complexity requires coordinated advisory, not piecemeal advice. iVentures Wealth is a SEBI-registered investment advisory firm (INA000019026) with 20+ years of experience and a dedicated NRI/OCI wealth management practice. The firm's tax optimisation service covers:

- DTAA structuring — TRC management, Form 10F coordination, foreign tax credit documentation across 90+ treaty countries

- TDS planning — proactive reduction of withholding on NRO interest, property sales, and mutual fund redemptions

- Form 15CA/15CB compliance — coordinated with chartered accountants for all eligible repatriation transactions

- Account structure advisory — determining the right split across NRO, NRE, and FCNR for each income stream

- Consolidated portfolio view — a single dashboard spanning NRO/NRE holdings, demat accounts, fixed deposits, and real estate income

The firm operates on a fee-only fiduciary model under SEBI's Investment Advisers Regulations, where every recommendation is shaped by your tax efficiency and financial goals — not product commissions.

iVentures currently advises 150+ affluent families, NRIs, and UHNIs across India. The minimum threshold for NRI/OCI engagements is ₹5 crore in investable assets.

If you're managing India-based income from abroad and want a tailored NRO tax planning consultation, connect with the team at info@iventures.in.

Frequently Asked Questions

What is the tax rate for NRO accounts?

Interest and income in an NRO account are taxed at a flat 30%, plus a surcharge that varies from 10% to 37% depending on total income, and a 4% health and education cess on top. For high earners, the effective rate can exceed 34–35%. DTAA provisions can reduce this to 10–15% for eligible NRIs.

Which is better, NRO or NRE?

It depends on where your money comes from. NRE accounts are ideal for parking foreign earnings in India tax-free with full repatriation flexibility. NRO accounts are mandatory for India-sourced income like rent, salary, and dividends — most NRIs benefit from maintaining both.

Can I deposit ₹10 lakh in my NRO account?

There's no upper limit on deposits from India-sourced income. However, funds repatriated abroad from the NRO account are capped at USD 1 million per financial year after paying applicable taxes and submitting the required CA-certified documentation.

Is NRO account interest taxable even if my total income is below the exemption limit?

Banks will still deduct TDS at 30% regardless of your total income. However, if your total Indian income falls below the basic exemption limit, you can file an ITR and claim a full refund of the TDS deducted.

How do I claim DTAA benefits on my NRO account?

Submit a Tax Residency Certificate from your country of residence, a completed Form 10F, and a self-attested PAN copy to your bank before interest is credited. Once submitted, the bank will apply the lower DTAA rate instead of 30%.

Do NRIs need to file an income tax return if TDS is already deducted?

Yes — ITR filing is advisable or mandatory depending on total income. It lets you claim TDS refunds if over-deducted, report capital gains accurately, and stay compliant — particularly when repatriating funds or selling Indian property.