The challenges compound quickly: emotionally charged decisions made under legal pressure, risk of inequitable settlements, tax traps that erode settlement value, and the daunting task of rebuilding financial independence from scratch. Many high-net-worth individuals discover, too late, that they failed to plan before filing.

This article covers the practical strategies that matter most — from pre-divorce financial preparation and asset division under Indian law, to tax planning, alimony, estate updates, and rebuilding your portfolio with purpose.

Key Takeaways

- Start financial planning before filing — courts require full disclosure, and early preparation protects your rights

- Indian courts use equitable distribution, not a 50/50 split — documentation and valuation are critical

- Tax on asset transfers and alimony can erode your net settlement — factor this in before agreeing to terms

- Update all beneficiary nominations and estate documents immediately after divorce is finalised

- A structured post-divorce financial plan is essential, not optional — build it before the ink dries

Building Your Financial Foundation Before Filing

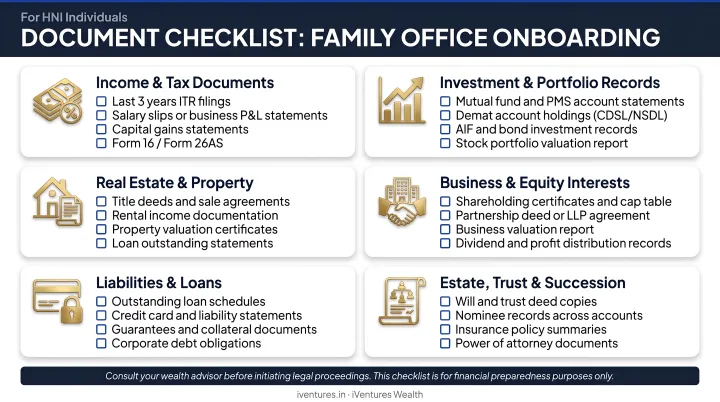

Financial preparation must begin before any legal filing. Courts in India operate on full financial disclosure — the Supreme Court's landmark ruling in Rajnesh v. Neha (2020) mandates that both parties file an Affidavit of Disclosure covering income, assets, liabilities, investments, business interests, and child expenses. Building your file around this affidavit — not a generic net-worth sheet — is the most practical starting point.

Documents to Gather Immediately

- Bank and investment account statements (last 12 months minimum)

- Income tax returns for the past 3 years

- Property titles and loan documents

- EPF, NPS, and PPF statements

- Demat account and mutual fund folio statements

- Insurance policies

- Business ownership documents, partnership agreements, or audited financials

- ESOP vesting schedules (relevant for CXOs and founders)

Share copies with your legal advisor before filing anything.

Separate vs. Marital Property

The distinction between separate property (assets brought into the marriage or inherited) and marital property (acquired during the marriage) significantly affects division outcomes. Document the source of funds for every major asset — purchase receipts, gift records, inheritance documents, and bank trails all matter. For affluent individuals with long marriages and commingled finances, this documentation exercise alone can take weeks.

What to Avoid During This Period

Courts scrutinise financial activity between separation and settlement. Specifically, avoid:

- Making large withdrawals from joint accounts without documented justification

- Significant purchases or new liabilities that alter your apparent financial position

- Transferring assets to relatives or third parties — courts treat this as dissipation of marital property

- Any financial move without first clearing it with your advisory team

Unexplained transfers made after separation can be reversed by the court or treated as evidence of bad faith, which directly weakens your negotiating position.

Assemble the Right Advisory Team

Three professionals are non-negotiable:

- A family law attorney with experience in high-value divorce matters

- A Chartered Accountant to model tax outcomes for each settlement scenario

- A SEBI-registered fiduciary financial advisor to provide a neutral, conflict-free assessment of your overall financial position

The advisor's role is not to advocate for either party — it is to ensure decisions are financially sound, not just legally acceptable.

How Assets Are Divided During Divorce in India

India does not operate under community property law. Unlike some Western jurisdictions where marital assets are split 50/50, Indian courts under the Hindu Marriage Act, 1955 and the Special Marriage Act, 1954 aim for equitable distribution — fair, based on contributions, financial needs, and circumstances — which is not automatically equal.

Real Estate

Property division typically follows one of three paths:

- Sell and split proceeds — cleanest option, but triggers capital gains tax

- One spouse buys out the other — requires a valuation and available liquidity

- Continued co-ownership — rarely advisable post-divorce; creates ongoing financial and legal entanglement

Stridhan — gifts, jewellery, and personal property gifted to the wife before or during marriage — is legally the wife's exclusive property. The Supreme Court reaffirmed this in Rashmi Kumar v. Mahesh Kumar Bhada (1996). Inventory it early with photographs, receipts, and locker details.

Financial Assets

Mutual fund folios, demat accounts, fixed deposits, PMS accounts, and equity portfolios all require valuation and may need to be split or transferred. For HNI and UHNI clients — where portfolios span multiple asset classes, custodians, and product structures — this means coordinating across advisors, brokers, and the court simultaneously.

Key asset types requiring independent valuation:

- Demat holdings and equity portfolios across multiple custodians

- PMS and AIF investments with lock-in or illiquidity considerations

- Fixed deposits and structured products with premature withdrawal penalties

- Foreign-domiciled accounts and global investment holdings

Retirement and Savings Accounts

India has no direct equivalent to the US QDRO mechanism. EPF balances are protected from court attachment under Section 10 of the EPF & MP Act. PPF deposits are similarly protected under the Government Savings Promotion Act.

This means retirement accounts cannot simply be divided like a demat folio. Settlements typically need to incorporate separate payment obligations rather than direct account splits — a distinction courts and advisors must address explicitly before any agreement is finalized.

Business Interests and Founder Equity

Privately held shares, founder stakes, and family business interests are among the most complex assets to value and divide. Courts may order independent business valuations, and operational control is rarely straightforward to protect without strategic settlement structuring. For founders and promoters, the right structuring at this stage can mean the difference between retaining operational control of your business and losing it to a contested court order.

Tax Implications of Divorce You Cannot Ignore

Tax planning is where many divorce settlements lose significant value. In most cases, neither party modelled the after-tax outcome before agreeing to terms — and that oversight can cost crores.

Asset Transfers Between Spouses

Section 47 of the Income Tax Act excludes specified transfers (gifts, wills, irrevocable trusts) from capital gains treatment. However, the provision does not offer a blanket divorce-specific exemption. Every asset transfer in a settlement should be reviewed individually by a CA — the tax character, timing, and structure of the transfer all affect liability.

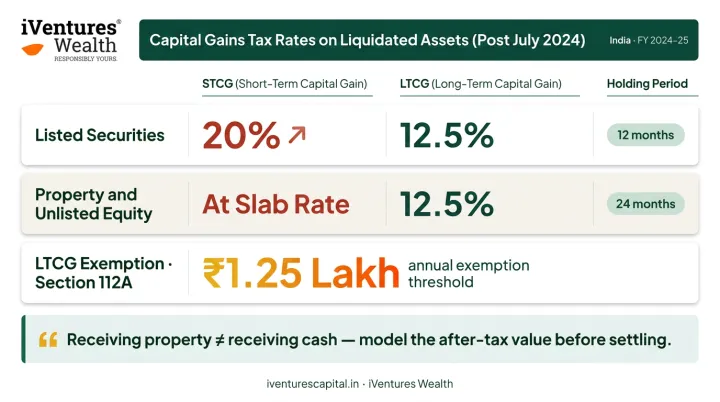

Capital Gains on Liquidated Assets

If jointly held assets are sold as part of settlement — a property, mutual fund units, or equity holdings — capital gains tax applies. CBDT's updated framework from 23 July 2024 applies the following rates:

| Asset Type | Holding Period for LTCG | STCG Rate | LTCG Rate |

|---|---|---|---|

| Listed securities (Section 111A/112A) | 12 months | 20% | 12.5% |

| Other assets (property, unlisted equity) | 24 months | Slab rate | 12.5% |

| LTCG exemption (Section 112A) | — | — | ₹1.25 lakh |

These rates should be factored into settlement negotiations. Receiving a property worth ₹2 crore is not the same as receiving ₹2 crore in liquid assets if the property carries a large embedded capital gain.

Alimony Taxation

- Lump sum alimony: Generally treated as a capital receipt and not taxable as income (ITAT Delhi, ACIT v. Meenakshi Khanna)

- Periodic maintenance: Typically treated as taxable income for the recipient

Work with your CA to compare the net-of-tax value of each structure before agreeing to terms. For a recipient in the 30% slab, the difference between a lump sum and equivalent periodic payments can represent tens of lakhs in additional tax outgo over time.

Individual vs. Joint Filing

India does not permit joint tax filing — spouses are always treated as separate individuals under the Income Tax Act. However, the shift in the year of divorce can still affect tax slab exposure and available deductions. Plan specifically for the financial year in which the divorce is finalised:

- Time large asset liquidations to avoid pushing either party into a higher slab

- Review deduction eligibility (Section 80C, 80D) as household income splits

- Confirm HRA and housing loan benefit positions if shared property is being transferred or sold

Navigating Alimony and Child Support

How Alimony Is Determined in India

Alimony under the Hindu Marriage Act operates on two tracks:

- Section 24: Interim maintenance during proceedings, where a spouse lacks sufficient independent income

- Section 25: Permanent alimony — a gross sum or periodic payment for a term not exceeding the applicant's life

Courts assess marriage duration, income disparity, standard of living, and the dependent spouse's ability to become self-sufficient. There is no fixed formula. The Supreme Court used 25% of the husband's net salary as a benchmark in Kalyan Dey Chowdhury v. Rita Dey Chowdhury (2017). This is a case-specific reference, not a guaranteed outcome. In Parvin Kumar Jain v. Anju Jain (2024), the court awarded ₹5 crore permanent alimony plus ₹1 crore for the son, emphasising that disclosure failures and undisclosed income are heavily penalised.

Child Support

Under HMA Section 26 and HAMA Section 20, courts consider the child's standard of living, education costs, and medical needs alongside both parents' incomes. Support typically runs until adulthood. Document all terms formally in the settlement decree — verbal commitments are not enforceable.

Securing Future Payments

Even with a well-drafted decree, periodic payments carry ongoing risk if the paying party's circumstances change. Where one party depends on alimony for financial stability, consider requiring a life insurance policy on the ex-spouse with the recipient named as beneficiary. Confirm each year that the policy remains active.

Updating Your Estate Plan and Beneficiaries

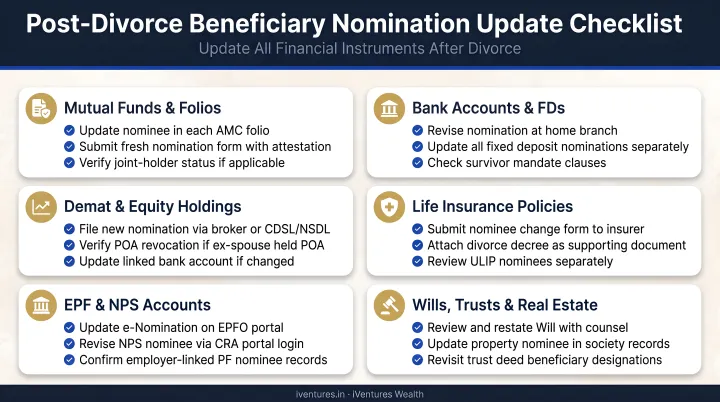

Failing to update estate documents after a divorce can result in your ex-spouse legally inheriting assets you never intended them to receive. Once the divorce is finalised, review every estate document and financial nomination without delay.

Estate Documents to Revise

- Revise your will immediately — under Section 62 of the Indian Succession Act, a will can be revoked or altered at any time

- Update financial and medical powers of attorney to remove your ex-spouse as the named agent

- Review trustee designations and beneficiary schedules in all trust deeds

- Remove your ex-spouse from emergency contacts and fiduciary roles across all institutional records

Beneficiary Nominations to Update

Missing even one nomination can result in assets inadvertently passing to an ex-spouse. Update systematically across:

- Life insurance policies

- EPF (Form 2 / e-nomination through EPFO)

- NPS (e-nomination via CRA/eNPS)

- Mutual fund folios (AMFI rules allow post-purchase nomination updates; SEBI's January 2025 circular revamped nomination facilities)

- Demat accounts (NSDL's online nomination process)

- Bank accounts

Retain written confirmation records for every change — these serve as proof in any future dispute.

Rebuilding Your Wealth After Divorce

Step One: A New Solo Financial Plan

Start with a clear-eyed picture of your current reality — revised income, new expenses, liabilities (rent, EMIs), and updated life goals. Build an emergency fund covering 6–12 months of expenses before making any significant investment decisions. If financial management was previously shared, this liquidity buffer is especially important.

Step Two: Portfolio Review and Rebalancing

Divorce settlements often result in receiving a portion of previously diversified joint assets. The result is frequently an unbalanced portfolio — overweight in certain asset classes, holding illiquid real estate, or concentrated in a single sector or instrument. A comprehensive portfolio review should assess:

- Asset allocation against your revised risk profile and time horizon

- Concentration risk (single stock, single sector, single asset class)

- Liquidity needs over the next 12–24 months

- Tax efficiency of the inherited holdings

Step Three: Long-Term Wealth Creation

Once your portfolio is rebalanced, the focus shifts to rebuilding on your own terms. For women who paused careers or were financially dependent, the stakes are especially high — research shows 41.5% of divorced women in urban India had no income after divorce, making a structured financial plan less optional and more essential.

This is where working with an independent, fiduciary adviser makes a real difference. iVentures Wealth, a SEBI-registered investment advisory firm, helps HNIs and UHNIs restructure post-divorce portfolios, plan passive income streams, and build long-term wealth strategies aligned to their revised goals — with no product commissions driving the advice.

Frequently Asked Questions

How do you deal with divorce financially?

Start financial planning before filing — gather all financial documents, assemble an advisory team (family law attorney, CA, and SEBI-registered financial advisor), avoid reactive financial decisions during proceedings, and create a structured solo financial plan once the divorce is finalised.

What is the 7-year rule for divorce?

There is no universal 7-year alimony rule in India. Under the Hindu Marriage Act, a person not heard of as alive for seven years may be presumed dead for marriage dissolution purposes — but this is unrelated to alimony duration or asset division. Marriage duration is one of several factors courts weigh when determining maintenance. Consult a family law attorney for jurisdiction-specific guidance.

How much alimony should a husband pay after divorce in India?

There is no fixed formula. Courts weigh marriage duration, income disparity, the wife's capacity for self-sufficiency, and the couple's standard of living — with settlements structured as lump sum or periodic payments. The Supreme Court has referenced 25% of net salary in some cases; others have run to several crores. Engage a family law attorney and financial advisor to negotiate an amount grounded in your specific facts.

Who suffers most financially in a divorce?

Research consistently shows women — particularly those who paused careers or were financially dependent — face greater hardship. However, high-income earners face significant exposure through alimony obligations, asset division losses, and tax liabilities. Financial planning is critical for both parties.

Should I keep the house or sell it during a divorce?

Weigh whether you can carry the mortgage and upkeep on a single income, the capital gains tax cost of selling, and whether keeping the house concentrates too much wealth in one illiquid asset. Emotional attachment is real — but so is the financial strain of holding it solo. A financial advisor can model the after-tax outcome of both paths before you decide.