Unlike resident Indians, NRIs face TDS deducted at source on every redemption, mandatory account structures under FEMA, and the genuine risk of paying tax twice on the same gains unless treaty paperwork is in place. The July 23, 2024 budget changes also reset several key rates, meaning advice from even two years ago may now be outdated.

This guide covers the exact capital gains rates post-July 2024, how TDS works in practice, when and how to use India's DTAA network, and what happens to existing holdings when residential status changes.

Key Takeaways

- NRIs must invest through an NRE or NRO account—resident savings accounts are not permitted under FEMA

- STCG on equity mutual funds is taxed at 20%; LTCG above ₹1.25 lakh is taxed at 12.5% (effective July 23, 2024)

- Filing an ITR in India lets NRIs reclaim TDS overpayments, since deduction rates often exceed actual tax liability

- Submitting a Tax Residency Certificate (TRC) and Form 10F to the AMC before redemption can lower TDS under DTAA provisions

- US and Canada-based NRIs face additional FATCA compliance requirements that restrict which AMCs they can invest with

Before You Invest: Three Essentials Every NRI Needs

The Right Bank Account

NRIs cannot route mutual fund investments through a resident savings account. FEMA requires redesignation to an NRI account, and SEBI confirms that NRIs can invest in Indian mutual funds through NRE or NRO accounts after completing KYC.

The account type matters beyond just compliance—it determines whether redemption proceeds can be freely repatriated:

| Account Type | Source of Funds | Repatriability | Interest Tax Treatment |

|---|---|---|---|

| NRE (Non-Resident External) | Foreign earnings | Freely repatriable | Tax-free in India |

| NRO (Non-Resident Ordinary) | India-sourced income | Up to USD 1 million per financial year | Taxable as India income |

Mutual fund redemption proceeds are typically credited to the linked NRO account. If full repatriation is a priority, discuss account linkage with your advisor before the investment is made—not at redemption.

PAN Card

Once your bank account is in order, the next prerequisite is a Permanent Account Number. No AMC will process your investment without one. Both Protean eGov and UTIITSL offer online PAN application routes, including pathways for foreign citizens, so this step is fully achievable from abroad.

KYC Update

When residential status changes, KYC must be updated with all AMCs and KYC Registration Authorities (KRAs). The SEBI KYC FAQ specifically lists a passport and overseas address proof as required documents for NRI investors. A cancelled cheque from the NRE/NRO account is also standard.

Digital KYC options are now widely available across most AMCs and KRAs, making it possible to complete the entire onboarding process remotely without a visit to India.

Capital Gains Tax on Mutual Fund Redemptions: The Full Breakdown

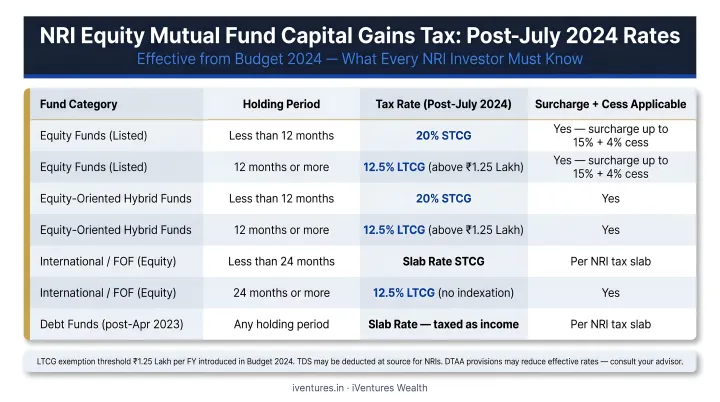

NRI capital gains tax rates mirror those for resident Indians, but with one operationally significant difference: tax is collected via TDS at redemption, not at year-end. The rate depends on fund type and holding period.

Equity-Oriented Funds (65%+ in Domestic Equity)

These are the clearest cases. Per AMFI's current tax regime table and the Finance (No. 2) Act, 2024, the applicable rates effective July 23, 2024 are:

- STCG (held under 12 months): 20% flat, regardless of income slab (up from 15%)

- LTCG (held over 12 months): 12.5% on gains exceeding ₹1.25 lakh per financial year (up from 10% on ₹1 lakh); no indexation benefit

Illustrative example: An NRI redeems equity mutual fund units after 14 months, realising a gain of ₹3,00,000. The taxable LTCG is ₹3,00,000 minus ₹1,25,000 exemption = ₹1,75,000. Tax at 12.5% = ₹21,875 (plus applicable surcharge and cess).

Debt and Specified Mutual Funds

The rules here changed materially in April 2023 and remain in effect:

Specified Mutual Funds (equity allocation below 35%, governed by Section 50AA): All gains are treated as STCG regardless of holding period, taxed at the investor's applicable income tax slab rate. Indexation and LTCG benefits that existed before April 2023 no longer apply.

Other Mutual Funds (equity between 35–65%):

- STCG (held up to 24 months): taxed at slab rate

- LTCG (held over 24 months, for sales on or after July 23, 2024): 12.5% without indexation

- Note: Before July 23, 2024, the LTCG rate was 20% with indexation and the threshold was 36 months

Hybrid Funds

Hybrid funds sit between equity and debt, so tax treatment follows the dominant asset class. If a fund maintains 65% or more in equity on an annual average basis, it qualifies as an equity fund for tax purposes. Otherwise, the debt/other fund rules apply. Confirm the fund's current composition directly with the AMC before assuming a category, since allocations can shift over time.

TDS on NRI Mutual Fund Redemptions

Unlike resident Indians who settle tax at year-end, AMCs deduct TDS directly at the point of redemption for NRI investors — the amount is withheld before the proceeds reach your account.

TDS Rate Structure

| Fund Category | Gain Type | TDS Rate |

|---|---|---|

| Equity funds | STCG | 20% |

| Equity funds | LTCG | 12.5% |

| Debt/specified funds | STCG (slab-based) | 30% |

| Debt/specified funds | LTCG (where applicable) | 12.5% or 30% |

| IDCW (dividend) payouts | All fund types | 20% |

All rates are subject to applicable surcharge and cess.

The Refund Route

TDS rates often exceed actual tax liability—particularly for debt fund investors where 30% is deducted but the NRI's actual slab rate is likely lower. The solution is to file an Income Tax Return in India and claim a refund of the excess, a route confirmed in the Income Tax Department's non-resident taxation guide.

The Proactive Approach: TRC + DTAA

For NRIs who want to reduce TDS upfront rather than recover it later, there is a proactive alternative. Submitting a valid Tax Residency Certificate and Form 10F to the AMC before redemption allows the AMC to apply the applicable DTAA treaty rate at source, under Section 90 of the Income Tax Act. This can meaningfully reduce the amount withheld, depending on the treaty between India and the NRI's country of residence.

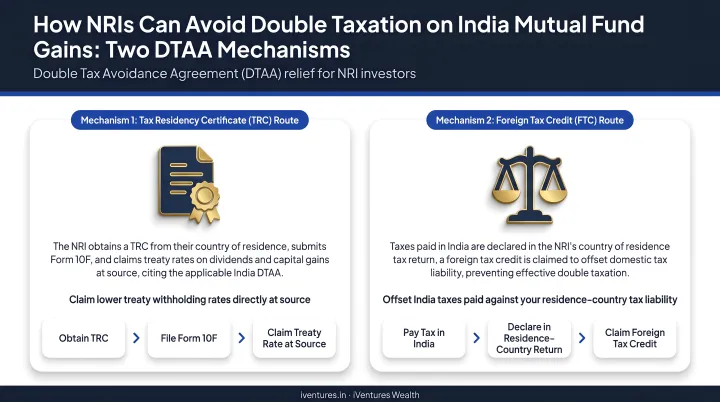

Using DTAA to Avoid Double Taxation

An NRI's mutual fund gains are taxed in India via TDS at redemption. The same gains are typically reportable—and often taxable—in the country of residence. Without a treaty in place, that's double taxation on the same income.

How DTAA Resolves This

India has an extensive CBDT-published DTAA network covering countries including the UK, UAE, Singapore, Australia, and the US. Two mechanisms are available:

- Lower TDS at source: Submit a valid TRC and Form 10F to the AMC before redemption. If the applicable treaty specifies a lower withholding rate, the AMC can apply it directly

- Foreign Tax Credit (FTC): Pay Indian TDS at standard rates, then claim credit for that tax in the country of residence when filing the foreign tax return

Treaty provisions vary significantly by country. Do not assume a specific rate or exemption applies without checking the actual India-country treaty text.

US-Based NRIs: A More Complex Scenario

The IRS taxes US citizens and resident aliens on worldwide income, which includes Indian mutual fund gains—potentially even on unrealised, mark-to-market basis depending on how the funds are classified. The India-US DTAA coordinates taxing rights but does not eliminate US reporting obligations. Form 1116 is the standard mechanism for claiming foreign tax credit on Indian taxes paid.

For US-based NRIs — and those in other multi-reporting jurisdictions — the interaction between Indian TDS, DTAA provisions, and IRS obligations makes cross-border tax advice genuinely necessary, not optional. Working with an advisor who understands both sides of the filing picture can prevent costly misclassifications and missed credit claims.

What Happens to Your Mutual Funds When You Become an NRI?

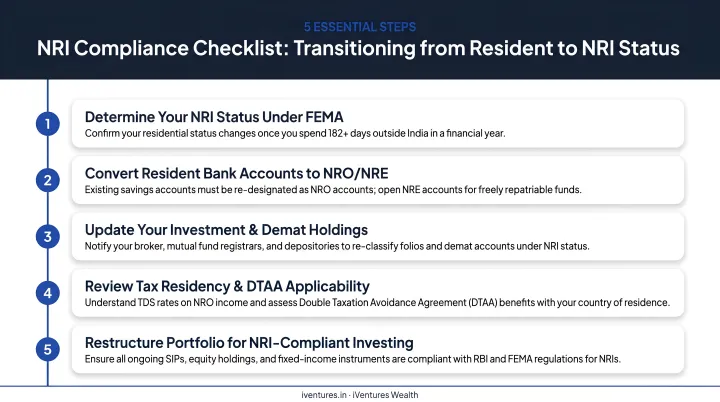

Existing mutual fund holdings are not forfeited. Under Section 6(5) of FEMA, a person who becomes non-resident can continue to hold assets acquired while they were resident in India. But there are mandatory compliance steps that cannot be ignored.

Required Steps Upon Becoming NRI

- Update KYC status with all AMCs and KRAs to reflect NRI status

- Link fund folios to an NRE or NRO account—redemption proceeds will be credited to the linked NRO account

- Transition active SIPs to be debited from the NRE/NRO account; SIP mandates on resident savings accounts must be cancelled and re-registered

- Update FATCA/CRS self-certification across all financial institutions

- Review tax residency documentation to determine applicable DTAA coverage

The most common compliance gap is continuing SIP debits from a resident savings account after NRI status is established. This violates FEMA and can attract penalties.

Upon Return to India

The process reverses. The process reverses when you return for permanent stay. RBI guidelines require the following steps:

- Convert NRE and FCNR(B) accounts into resident or RFC accounts

- Re-update KYC to resident status with all AMCs

- Relink mutual fund folios to a resident savings account

Retaining NRI-designated accounts after regaining resident status violates FEMA. A compliance review at this stage — covering accounts, folios, and tax residency documentation — helps avoid inadvertent penalties.

Special Consideration: US and Canada-Based NRIs

NRIs resident in the US and Canada face restrictions beyond standard NRI compliance.

The FATCA Factor

India and the US signed a Model 1 FATCA Intergovernmental Agreement in 2015. Under this framework, Indian financial institutions report US-reportable account information to Indian authorities, which then exchange it with the IRS. Indian Rule 114F supports both FATCA and CRS reporting obligations.

In practice, not all Indian AMCs have built out the compliance infrastructure needed to onboard US and Canada-based NRI investors. MF Utility publishes specific requirements for US/Canada residents — including mandatory FATCA-CRS declarations and additional documentation — and this remains one of the more reliable reference points for understanding what's required.

Practical Guidance for US/Canada NRIs

- Confirm the AMC's current policy on US/Canada NRI investors before starting onboarding — eligibility varies significantly across fund houses

- Submit FATCA-CRS declarations alongside standard NRI KYC; these are non-negotiable additions, not optional paperwork

- Expect limited digital access; some AMCs require in-person steps for US/Canada residents that other NRIs can complete remotely

- Factor in US tax obligations separately — Indian mutual fund gains may qualify as PFIC income, triggering specific reporting elections or annual mark-to-market treatment under US tax law

The AMC landscape for US/Canada NRIs is narrower than for NRIs elsewhere. Shortlisting only AMCs with established FATCA onboarding — and clarifying the PFIC election strategy with a cross-border tax advisor — before choosing a platform will save significant friction later.

Frequently Asked Questions

What happens to mutual funds when you become NRI in India?

Existing holdings remain valid under FEMA Section 6(5), but you must update your NRI status with all AMCs, link folios to an NRE or NRO bank account, and transition any active SIPs to be funded from those accounts. Continuing to operate through a resident savings account after acquiring NRI status breaches FEMA and can attract penalties.

Are mutual funds allowed for NRI?

NRIs can invest in Indian mutual funds subject to FEMA compliance by routing investments through NRE or NRO accounts and completing NRI KYC. NRIs can invest in Indian mutual funds by routing investments through NRE or NRO accounts and completing NRI KYC, subject to FEMA compliance. US and Canada-based NRIs face additional FATCA requirements and should verify AMC eligibility before investing.

How can I avoid double taxation on my India investments as an NRI?

Submit a valid Tax Residency Certificate and Form 10F to the AMC before redemption to access the applicable treaty withholding rate. For taxes already deducted in India, claim a Foreign Tax Credit in your country of residence. Treaty terms vary by country, so review the specific India-country DTAA provisions — iVentures Wealth provides specialised NRI/OCI cross-jurisdictional advisory, including TRC management and FTC documentation, for clients with ₹5 Crore or more in investable assets.

What TDS rate is deducted on mutual fund redemptions for NRIs?

Equity fund redemptions attract 20% TDS on STCG and 12.5% on LTCG; debt/specified fund redemptions attract 30% TDS regardless of holding period; IDCW payouts attract 20% TDS across fund types. All rates are subject to surcharge and cess. If TDS exceeds actual tax liability, NRIs can file an ITR in India to claim a refund.

Can NRIs invest in mutual funds through SIPs?

NRIs can register SIP mandates on their NRE or NRO accounts. Existing resident SIPs can continue after updating account details, but SIP debits cannot continue from a resident savings account once NRI status is established. The mandate must be re-registered on the NRI account.

Do NRIs investing in Indian mutual funds need to file an income tax return in India?

NRIs whose total Indian income exceeds the basic exemption limit, or those with excess TDS deducted, must file an ITR in India. Filing also generates documentation needed to claim Foreign Tax Credit in the country of residence, so it remains advisable even when TDS appears to cover the full liability.