Research from the Centre for Financial Inclusion found that 87% of Indian entrepreneurs did not maintain separate budgets or accounts for business and household finances. That single habit — or lack of it — creates cascading problems: tax filing errors, inaccurate business performance assessments, and personal financial exposure to every business cycle.

This blog covers six practical financial planning tips tailored specifically for Indian entrepreneurs and business owners — from budgeting and tax strategy to retirement and working with the right advisor.

Key Takeaways

- Separate personal and business finances from day one — commingling creates tax, legal, and cash flow problems

- Tax planning works best year-round, not just in March before filing deadlines

- Entrepreneurs have no EPF or employer pension — self-directed retirement planning is non-negotiable

- A SEBI-registered, fee-based fiduciary advisor eliminates the conflicts that commission-based advisors carry

Tip 1: Separate Your Personal and Business Finances

Mixing personal and business money is one of the most common — and most damaging — financial mistakes Indian entrepreneurs make. It happens gradually: a business expense paid from a personal account here, a personal purchase on the business card there. Before long, neither picture is accurate — and that creates problems that compound quickly.

The consequences are real:

- GST returns, TDS, and income tax filings all require clean separation between business income and personal income; mixed accounts make every filing harder

- For sole proprietors especially, commingled finances blur the line between personal and business obligations, increasing legal exposure

- Banks evaluate MSME borrowers through financial statements, bank statements, GST returns, and cash flow records — as confirmed by the MSME Ministry's lender guidance; mixed accounts make that assessment nearly impossible

How to Create Clean Separation

Fixing the problem comes down to three practical steps:

- Open a dedicated business current account — route all business income and expenses through this account, without exception

- Use a separate business credit card — never use personal cards for vendor payments, office expenses, or travel

- Pay yourself a defined salary or owner's draw — transfer a regular, pre-decided amount to your personal account rather than making ad-hoc withdrawals whenever cash is available

Among early-stage entrepreneur clients, a consistent pattern shows up: household expenses directly tied to business cash flows, with no real boundary between company capital and family income. When revenue dips, personal finances absorb the impact immediately. Getting this separation right from the start eliminates that exposure.

Tip 2: Build a Budget and Master Cash Flow Management

Creating a Business and Personal Budget

Entrepreneurs need two distinct budgets — not one combined spreadsheet.

Business budget should track:

- Fixed costs: rent, salaries, software subscriptions, loan EMIs

- Variable costs: marketing spend, raw materials, client entertainment

- Seasonal adjustments for festival-driven revenue cycles or project-based income

Personal budget should account for:

- Household expenses and EMIs

- Insurance premiums

- Savings and investment contributions

Once the business budget is in place, review it monthly against actual figures. Then calculate your runway — how many months can your business sustain itself on current cash reserves if revenue stopped tomorrow? A 2020 NASSCOM survey reported in TechCrunch found 70% of Indian startups had less than three months of runway during the COVID disruption. Knowing this number before a crisis — not during one — is the entire point.

Monitoring and Optimising Cash Flow

Runway awareness is only half the picture. Cash flow and profit are not the same thing — a business can show strong profits on paper and still fail because customers haven't paid yet.

Consider a simple example: you complete a ₹20 lakh project in March, invoice the client, and record it as revenue. But the client pays in 60 days. Meanwhile, your vendors need payment in 30 days. On paper, the business is profitable. In practice, you may not be able to meet payroll.

Actionable cash flow strategies:

- Send invoices immediately on project completion — not at the end of the month

- Offer small early-payment discounts to incentivise faster collections

- Negotiate extended payment terms with suppliers where possible

- Maintain a short-term credit facility (overdraft or working capital loan) as a liquidity buffer

Tools like Tally, Zoho Books, or QuickBooks automate this tracking, giving you a live picture of receivables, payables, and available cash. That visibility turns reactive decisions into proactive ones.

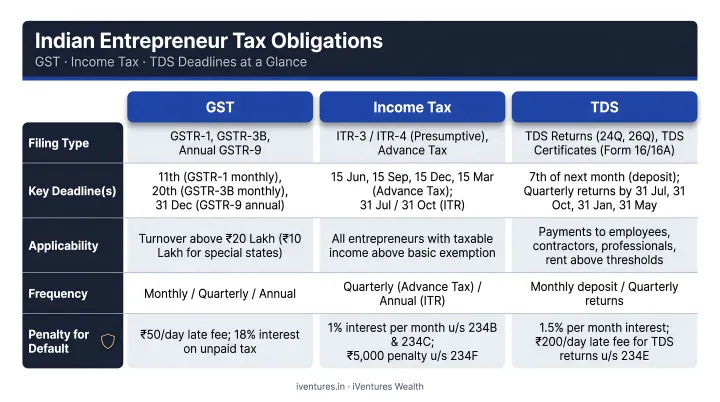

Tip 3: Tax Planning Strategies for Entrepreneurs

Understanding Your Tax Obligations

Indian entrepreneurs face multiple simultaneous tax obligations, and missing any of them triggers penalties that erode profits.

| Tax Obligation | Key Requirement |

|---|---|

| Income Tax | Advance tax paid quarterly; personal filing for proprietors |

| GST – GSTR-1 | Monthly: 11th of following month; Quarterly (≤₹5 Cr turnover): 13th of month after quarter |

| GST – GSTR-3B | Monthly: 20th of following month; Quarterly: 22nd or 24th depending on state |

| TDS | Deduct and deposit as per applicable schedule |

| Professional Tax | Varies by state |

Business structure also affects taxation directly. Sole proprietors file business income under personal income tax returns. Private Limited Companies file separately as corporate entities and are taxed at corporate rates. LLPs occupy a middle ground between the two. Choosing the right structure — and understanding its tax implications before you incorporate — matters more than most founders realise.

Strategies to Reduce Your Tax Burden Legally

Several provisions specifically benefit entrepreneur taxpayers:

Personal income deductions worth knowing:

- Section 80C: Up to ₹1,50,000 via PPF, ELSS, life insurance premiums, and home loan principal

- Section 80CCD(1B): Additional ₹50,000 deduction for NPS contributions — available on top of 80C limits

Business expense deductions:

- Section 37: Office rent, internet, travel, marketing, and other business expenses not covered under Sections 30–36 are deductible

- Section 32: Depreciation on equipment, machinery, and other business assets reduces taxable income

For eligible businesses, presumptive taxation simplifies compliance significantly:

- Section 44AD: Presumptive taxation for eligible businesses with turnover up to ₹3 crore (₹2 crore if cash receipts exceed 5% of gross receipts)

- Section 44ADA: Presumptive taxation for professionals up to ₹75 lakh (₹50 lakh if cash receipts exceed 5%)

Decisions made in April — about business structure, investment instruments, and expense categorisation — affect your March tax liability far more than anything you scramble to do in the final quarter.

Tip 4: Build an Emergency Fund and Protect Your Business

Entrepreneurs need a larger emergency fund than salaried employees — not smaller. Income is irregular, receivables can slow, and business downturns can extend for months without warning.

A practical starting point: 6 to 12 months of both personal living expenses and business operating costs, held in liquid instruments. Some advisors go further — structuring a dedicated safety bucket covering 5–7 years of personal expenses in high-quality fixed income, so personal financial stability stays insulated from whatever happens in the business.

The COVID period demonstrated why this matters. The World Bank documented severe MSME cash flow and liquidity stress across India during 2020, with government intervention required at scale to prevent widespread business failures. Businesses that entered the disruption with liquidity reserves had options; those without had very few.

Insurance: Not Optional, Foundational

Since no employer covers these costs, entrepreneurs must self-fund their risk protection:

- Health insurance for self and family — this is the most immediate gap

- Term life insurance — sized to replace income and cover business liabilities

- Business liability insurance — especially critical for service businesses and consultants

- Key-man insurance — if the business depends heavily on a specific individual, their death or disability can threaten the entire enterprise

India's overall insurance penetration stood at just 3.7% in 2024–25 according to the IRDAI Annual Report, with non-life at only 1.0%. Entrepreneurs are almost certainly underinsured relative to their actual risk exposure.

Insurance coverage addresses individual risk, but partnership risk requires a separate layer of planning. For businesses with multiple partners, a buy-sell agreement — a pre-agreed plan for ownership transfer in the event of death, disability, or dispute — protects both business continuity and each owner's personal estate.

Tip 5: Invest for Long-Term Wealth and Plan for Retirement

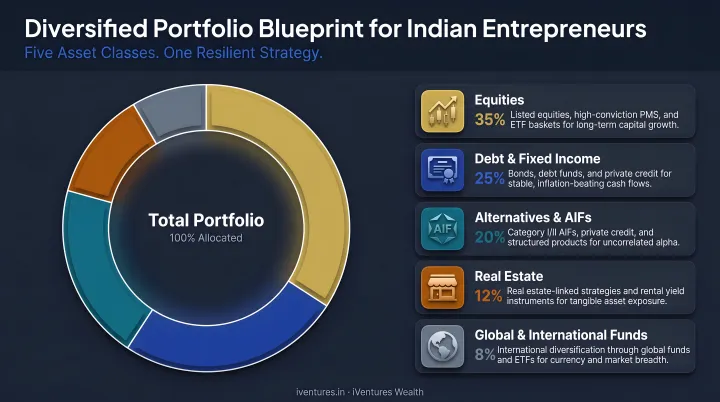

Building a Diversified Investment Portfolio

The most common wealth trap for entrepreneurs: the business is the investment portfolio. Promoter equity plus one or two properties, with minimal financial assets elsewhere. One bad business cycle hits the entire financial life simultaneously.

This concentration risk needs active management. Building personal wealth separately from the business creates financial independence — the kind where a bad quarter does not affect school fees, EMIs, or retirement savings.

A diversified personal portfolio for entrepreneurs typically spans:

- Equity mutual funds and direct stocks — long-term growth

- Debt instruments and bonds — stability and income

- Global funds and ETFs — geographical diversification, dollar-denominated exposure

- REITs — rental income without property management

- Alternative Investment Funds (AIFs) and PMS — for higher-conviction strategies at appropriate thresholds

Building this kind of separation requires deliberate structuring. iVentures Wealth (SEBI RIA: INA000019026), which manages ₹1200+ Cr in AUM for founders, CEOs, and UHNIs, applies a drawdown rule where each profitable business year feeds a ring-fenced personal corpus. One client outcome: a structured income portfolio generating approximately ₹7.5 lakh per month in passive income, entirely independent of business performance.

Retirement Planning Without a Corporate Safety Net

Entrepreneurs have no EPF, no employer-matched provident fund, and no pension. The starting point for retirement planning is accepting that — and building a self-directed plan from the first year of consistent business income.

Key retirement vehicles available in India:

- NPS (National Pension System): Available to all Indian citizens aged 18–70, including the self-employed. Tier I contributions qualify for deductions under 80CCD — with the additional ₹50,000 deduction under 80CCD(1B) being particularly valuable for entrepreneurs in higher tax brackets

- PPF: 15-year lock-in, EEE tax treatment (contributions, interest, and maturity proceeds all exempt), currently earning 7.1% for April–June 2026

- ELSS mutual funds: Shortest lock-in among 80C instruments (3 years), equity exposure, tax-efficient for long-term compounding

Which instruments you choose matters less than when you start. The same monthly contribution begun at age 30 versus age 40 produces a dramatically larger corpus by age 60 — purely because of the additional decade of compounding. Betting on a business exit to fund retirement means depending on valuations, timing, and market conditions that are largely outside your control.

A successful business exit feeds into this picture, not separately from it. Capital gains tax optimisation on equity stakes, Section 54F reinvestment options, and structured post-exit deployment all require advance planning — decisions made during the exit process itself are almost always reactive and costly.

Tip 6: Work With a Financial Advisor Who Understands Entrepreneurship

Most financial advisors are built for salaried clients: predictable income, employer-sponsored benefits, standard tax deductions. Entrepreneurs are a different brief — irregular cash flows, business risk concentration, complex tax structures, succession planning, and liquidity events that don't follow a tidy schedule.

What to look for in a financial advisor as an entrepreneur:

- Understands business concentration risk and how to reduce it systematically

- Operates as a fiduciary — fee-based, conflict-free, not earning commissions on what they recommend

- Holds SEBI registration — the key regulatory credential for investment advisers in India (fewer than 1,100 registered investment advisers exist nationally, per SEBI's current records)

- Can coordinate with your CA and legal counsel on tax-efficient structures, not just recommend investment products in isolation

That fiduciary requirement matters in practice. Under SEBI's Investment Advisers Regulations 2013, registered advisers must disclose conflicts of interest and are barred from receiving commissions or trail income from product manufacturers. A mutual fund distributor or bank relationship manager operates under no such restriction — their recommendations may reflect product incentives, not your best interest.

iVentures Wealth (SEBI RIA: INA000019026) has worked with founders, CEOs, CXOs, and business owners since 2005, with ₹1200 Cr+ in AUM across 150+ affluent relationships. Advisory spans tax-efficient portfolio construction, succession and estate planning, and liquidity event management — areas where most generalist advisors fall short for entrepreneurs.

Frequently Asked Questions

What is financial planning in entrepreneurship?

Financial planning in entrepreneurship is the process of managing both personal and business finances together — setting goals, building structures to achieve them, and ensuring the business can sustain itself through all growth stages. Unlike salaried planning, it must account for irregular income, business concentration risk, and the absence of employer-sponsored benefits.

What are the steps of financial planning?

According to FPSB's official financial planning framework, the process involves six elements: establishing the client relationship, collecting information, analysing and assessing the situation, developing recommendations, implementing strategies, and monitoring and reviewing the plan periodically.

What is the 70-10-10-10 rule for money?

The 70-10-10-10 rule is a budgeting heuristic: allocate 70% to living expenses and business reinvestment, 10% to savings, 10% to investments, and 10% to debt repayment or giving. Entrepreneurs should adapt these ratios to their business stage, income variability, and personal goals.

Why should entrepreneurs separate personal and business finances?

Clean separation enables accurate tax filing, protects personal assets from business liabilities, gives lenders the financial records they need to assess creditworthiness, and allows you to evaluate actual business performance — without personal spending distorting the numbers.

When should an entrepreneur start planning for retirement?

From the first year of consistent business income. With no employer-sponsored pension or EPF, every year of delay costs you compounding gains. NPS, PPF, and ELSS are available immediately — each offering tax benefits alongside long-term accumulation.