A financial planning consultant evaluates your complete financial picture — assets, liabilities, income, tax obligations, and long-term goals — and builds an integrated strategy around it. Unlike specialists focused on a single product or service, they take a panoramic view of your wealth.

This article covers what a financial planning consultant does, how they differ from financial advisors, what credentials and regulations matter in India, and how to identify when you need one.

Key Takeaways

- A financial planning consultant covers investments, tax, retirement, and estate planning — not a single product or domain

- The title is unregulated — always verify SEBI RIA registration and credentials like CFP or CFA before engaging

- Planners design the overall strategy; financial advisors often execute within a specific domain

- A fiduciary consultant — legally obligated to act in your interest — matters most when your financial situation is genuinely complex

- Liquidity events, inheritance, NRI transitions, and retirement all signal it's time for professional planning

What Is a Financial Planning Consultant?

A financial planning consultant is a professional who reviews your full financial situation — assets, liabilities, income, tax exposure, insurance, and goals — and creates an integrated, long-term plan. The role is architectural, not transactional.

This is distinct from a specialist who handles one dimension of your finances. A financial planning consultant coordinates across all of them: investment allocation, retirement corpus, estate structure, tax efficiency, and risk management.

The Title Is Not Regulated — Credentials Are

Anyone can call themselves a "financial consultant" in India. What matters is what sits behind the title:

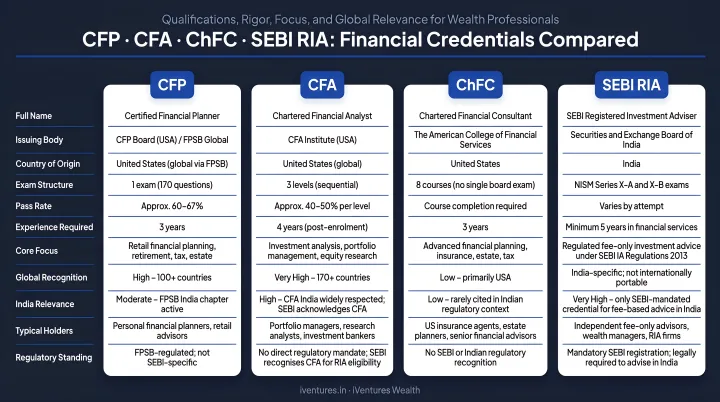

- CFP (Certified Financial Planner): Administered by FPSB India, the CFP covers comprehensive financial planning across all life goals. FPSB India reported 3,215 CFP professionals in India as of December 2024, a 17.7% year-on-year increase

- CFA (Chartered Financial Analyst): Administered by CFA Institute, the CFA focuses on investment analysis, portfolio management, and research — stronger for investment depth than holistic planning

- ChFC (Chartered Financial Consultant): Issued by The American College of Financial Services, covering estate, insurance, tax, retirement, and behavioural finance through an eight-course curriculum

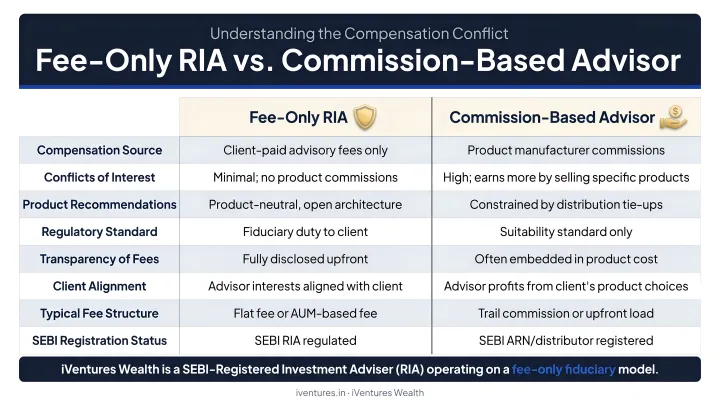

In the Indian context, SEBI registration as an Investment Adviser (RIA) is the most important regulatory credential. Under the SEBI Investment Advisers Regulations 2013, RIAs must act in a fiduciary capacity, disclose conflicts of interest, and cannot receive commissions from product manufacturers. This separates them structurally from mutual fund distributors and commission-based agents.

The Fiduciary Distinction

A fiduciary is legally and ethically required to put your interests first. In India, SEBI-registered RIAs operate under this standard by regulation — their compensation must come from clients, not product providers.

Firms operating under the ARN distributor model earn trail commissions from product manufacturers. That creates a structural misalignment that fee-only RIAs are explicitly prohibited from having.

Who Benefits?

Understanding the fiduciary structure matters most for those with the most to protect. Financial planning consultants are not only for the ultra-wealthy — but the value compounds sharply as financial complexity increases. Their services are particularly relevant for:

- HNIs and UHNIs managing multi-asset portfolios across entities

- Family businesses navigating succession, estate, and liquidity planning

- NRIs and OCIs with cross-border tax and investment considerations

- CXOs, founders, and professionals with concentrated equity or ESOPs

- Anyone at a financial inflection point — liquidity event, inheritance, or retirement transition

Key Roles and Responsibilities of a Financial Planning Consultant

Comprehensive Financial Audit

Before any strategy is designed, a consultant needs a complete view of your financial position. This means reviewing:

- All investment holdings across brokers, mutual funds, demat accounts, and PMS/AIF providers

- Bank accounts, fixed deposits, and NRE/NRO holdings

- Insurance policies and nominee designations

- Real estate holdings and outstanding liabilities

- Tax documents and pending obligations

- For cross-border clients: overseas accounts, ESOP holdings, and foreign assets

The output is a unified financial baseline — what iVentures Wealth describes as a "unified family balance sheet" — that identifies concentration risks, duplicated holdings, and gaps before any allocation decision is made.

Investment Planning and Portfolio Construction

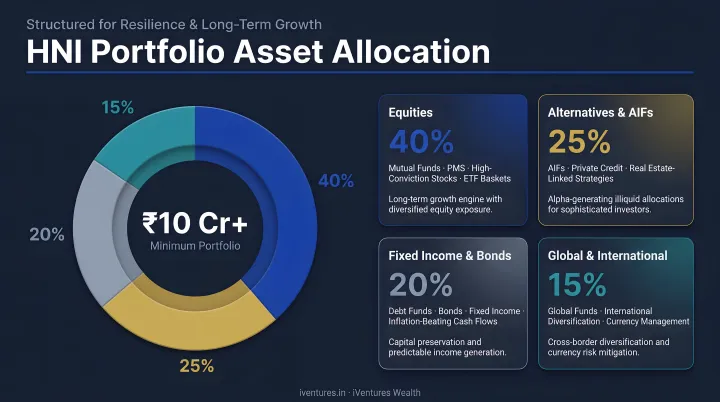

With a clear baseline, the consultant defines risk tolerance, time horizon, and return objectives. Portfolio construction for affluent investors typically spans:

- Equity: Mutual funds, high-conviction stock baskets, ETFs

- Fixed income: Corporate bonds, G-Secs, tax-free bonds, AAA/AA+ rated paper

- Alternatives: Category I/II/III AIFs, private credit, real estate funds

- Global assets: International funds and ETFs for USD-denominated exposure and geographic diversification

Portfolios are reviewed at least quarterly, with tactical rebalancing triggered by market movements, interest rate cycles, or changes in personal circumstances.

Tax Planning and Optimisation

Budget 2024's capital gains changes make tax-aware planning non-negotiable for HNI portfolios. STCG on specified financial assets now sits at 20%, LTCG at 12.5%, with an annual LTCG exemption of ₹1.25 lakh.

A financial planning consultant structures investments to manage this exposure — through asset location, exit timing, tax-loss harvesting, and efficient rebalancing.

For NRIs and those with cross-border holdings, this extends to DTAA optimisation, TDS planning on NRO/NRE income, and FEMA compliance. The consultant handles portfolio-level tax efficiency; a CA handles actual filing.

Retirement Planning

For business owners, CXOs, and professionals without employer pension plans, retirement planning requires building from scratch — without the safety net of employer pensions. A consultant helps with:

- Estimating retirement corpus requirements accounting for inflation, healthcare, and longevity

- Selecting accumulation vehicles — NPS, equity mutual funds, debt funds, AIFs — appropriate to the timeline

- Building a decumulation framework: systematic withdrawal plans, dividend-generating portfolios, and private credit exposure for predictable cash flows

The benchmark is simple: the portfolio must outlast working years, with income structured so lifestyle decisions are driven by choice, not cash flow constraints.

Estate and Succession Planning

A financial planning consultant coordinates with legal advisors to ensure wealth transfers efficiently across generations. This covers:

- Will drafting and executorship support

- Private trust establishment under the Indian Trusts Act, 1882

- Nomination alignment across all financial instruments

- Business succession frameworks and family governance charters

- Cross-border inheritance structuring for NRI families

A common misconception worth addressing: nominees are legal custodians, not automatic heirs. Without proper documentation, assets can be tied up in disputes for years — and the consultant's job is to close those gaps before they become a family problem.

Financial Planning Consultant vs. Financial Advisor: Understanding the Difference

The titles are not interchangeable.

A financial planning consultant functions as a strategist — designing the overall financial roadmap across all dimensions of a client's wealth. A financial advisor often plays a more specialised or transactional role: a stockbroker executing trades, an insurance agent recommending policies, or a mutual fund distributor managing SIPs.

The financial planning consultant oversees the full picture. Each financial advisor operates within a defined domain — executing well within it, but rarely looking beyond it.

The Compensation Difference Matters

How an advisor is paid directly affects the quality of their advice:

| Model | How They're Paid | Conflict Risk |

|---|---|---|

| Fee-only RIA | Client pays advisory fee directly | Low — no product incentives |

| AUM-based fee | Percentage of assets managed | Low to moderate |

| Commission-based distributor | Trail income from product manufacturers | High — incentive to push higher-commission products |

SEBI formally separated the RIA advisory model from the distribution model precisely because of this conflict. Under SEBI's 2020 amendment, RIAs cannot receive consideration from anyone other than the client being advised, in respect of the underlying products or services.

The practical difference: a commission-based distributor's recommendations are shaped by what earns them trail revenue. A fee-only RIA's recommendations are shaped by what's right for you.

When Do You Need a Financial Planning Consultant?

Life Events That Signal the Need

Certain situations make structured professional guidance valuable:

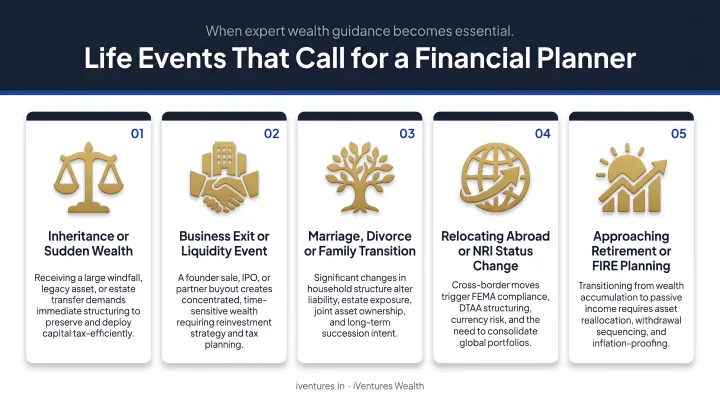

- Business liquidity events: Receiving ₹50–100+ crore from a business exit without a deployment framework creates significant risk — and significant tax exposure

- ESOP windfalls: In 2024, 23 Indian startups executed ESOP buybacks generating over ₹1,448 crore for 3,000+ employees — each a meaningful wealth event requiring structured planning

- NRI transitions: Moving to or from NRI status changes tax residency, FEMA obligations, and banking structures simultaneously

- Inheritance: Receiving significant assets without a clear integration plan often leads to concentration, duplication, and missed tax efficiency

- Approaching retirement: Shifting from accumulation to decumulation requires a deliberate framework, not a continuation of the same equity-heavy portfolio

The Behavioural Case

Research supports the value of professional guidance beyond portfolio construction. Morningstar's Gamma research found that a Gamma-efficient retirement strategy produced 22.6% more certainty-equivalent income versus the base scenario — with much of that gain coming from planning discipline, not market outperformance.

Investors consistently make suboptimal decisions during volatility. The behaviour gap — the difference between what a fund returns and what investors actually earn — is largely a product of panic selling and performance chasing. A financial planning consultant's most valuable function is often keeping clients rational when markets are not.

Who May Not Need One Yet

Someone with simple finances — single income, modest savings, no complex assets or liabilities — can manage well with a robo-advisor or a direct mutual fund platform. The case for a professional consultant typically arrives with complexity: multiple income streams, cross-border assets, an approaching liquidity event, or a portfolio that spans more asset classes than one person can meaningfully track and optimise.

How to Choose the Right Financial Planning Consultant

Verification Checklist

Before engaging any consultant, confirm:

- SEBI RIA registration: Search by name or registration number at the SEBI Intermediaries portal. As of mid-2024, roughly 1,323 registered investment advisers operated in India — a small number relative to the total advisory market

- Credentials: CFP for holistic planning, CFA for investment depth. Confirm designation status directly with FPSB India or CFA Institute

- Regulatory history: Check for any SEBI enforcement actions or disciplinary proceedings

- Fee structure: Ask explicitly how the consultant is compensated. If the answer involves "no charge to you" or "the fund house covers it," that's a commission-based model

The Conflict-of-Interest Conversation

A fee-only, SEBI-registered RIA who earns nothing from product manufacturers represents the most conflict-free advisory model available in India. No commission incentives means no proprietary product bias — the advice follows your goals, not a distribution target.

Firms like iVentures Wealth (SEBI RIA registration INA000019026) operate on this model: fee-only, open-architecture, with access to mutual funds, AIFs, PMS, bonds, and global funds across regulated platforms — selected purely on merit for each client's situation.

Fit Beyond Credentials

Credentials confirm competence. But the durability of an advisory relationship also depends on:

- Communication style and review frequency (at least quarterly is standard)

- Familiarity with situations like yours — NRI taxation, founder liquidity, CXO equity compensation

- Transparency in reporting: consolidated statements, XIRR across all holdings, clear fee disclosure

- Whether the consultant treats your situation as a long-term partnership or a series of transactions

Use the first one or two meetings as a diagnostic: the right consultant asks more questions than they answer, and discloses fees without prompting.

Frequently Asked Questions

What does a financial planning consultant do?

A financial planning consultant reviews your full financial picture — income, assets, liabilities, tax position, and goals — then builds a strategy spanning investments, retirement, tax planning, estate planning, and risk management. The plan evolves as your life circumstances change, not fixed once and left alone.

How does a CFP differ from a CPA or CFA?

A CFP focuses on comprehensive personal financial planning across all life goals. A CPA specialises in accounting, tax preparation, and compliance. A CFA focuses primarily on investment research and portfolio management. Their work can overlap, and some advisors hold more than one designation, but each serves a distinct professional function.

What qualifications should I look for in a financial planning consultant in India?

SEBI registration as an Investment Adviser (RIA) is the key regulatory credential — it imposes a fiduciary obligation and prohibits commission income. Designations like CFP or CFA signal additional depth. Verify SEBI registration on the official SEBI intermediary portal and confirm the consultant operates on a fee-only basis.

When should I hire a financial planning consultant?

Common triggers include significant wealth events (business sale, inheritance, ESOP vest), major life transitions (retirement, NRI status change, a large compensation package), and situations where your financial complexity exceeds what you can manage alone. Engaging early gives your strategy more room to work.

How are financial planning consultants compensated?

The three main models are fee-only (flat fee or hourly), AUM-based (a percentage of assets managed), and commission-based (earnings from products sold). Fee-only and AUM-based models are more aligned with client interests. Commission-based structures carry an inherent conflict that SEBI's RIA framework was designed to address.

Is working with a financial planning consultant worth it?

For individuals with complex financial situations, significant assets, or multi-decade wealth goals, yes. The value shows up in tax savings, risk management, estate efficiency, and the avoidance of costly behavioural errors — not just in portfolio returns.