Introduction

Affluent Indians no longer accept the old tradeoff between quality and convenience. Professionals in Gurugram, founders in Bengaluru, and NRIs in Dubai or London managing India-domiciled assets all share a common frustration: access to genuinely qualified, fiduciary-grade advisors has historically required geography and rigid scheduling to align. Virtual financial advisory breaks that constraint.

This is not robo-advisory. A virtual financial advisor is a licensed, human professional — SEBI-registered, CFA or CFP-qualified — who delivers the same depth of financial planning as an in-person model through video calls, secure portals, and real-time dashboards. The relationship is fiduciary, the advice is personalised, and the delivery is entirely digital.

According to EY's 2024 India WealthTech report, India's wealthtech market was projected to grow from USD 20 billion in FY20 to over USD 63 billion by FY25. The demand is there. The question is how to engage this model correctly — choosing the right advisor, structuring the first conversation, and building a relationship that compounds in value over time. This guide covers each step.

Key Takeaways

- Virtual financial advisors are qualified human professionals — not algorithms — delivering fiduciary-grade planning through digital channels.

- This model suits NRIs, HNIs, and busy professionals who need expert guidance without geographic or scheduling constraints.

- Come prepared: consolidated asset data, clear financial goals, and KYC documents ready before your first session.

- Honest onboarding, regular monitoring, and proactive communication determine how much value you extract from the relationship.

When Is a Virtual Financial Advisor Right for You?

Virtual advisory works best in specific circumstances. It suits clients with defined, complex needs and the digital fluency to act on structured advice — not everyone, and misapplying it costs both the client and the engagement.

It fits well when you have:

- Complex, defined financial needs — wealth structuring, NRI investment management, tax planning, portfolio consolidation

- Geographic or scheduling barriers to qualified in-person advisors

- Comfort with digital communication and document workflows

- A portfolio sophisticated enough to warrant ongoing fiduciary oversight

It is frequently misused when:

- Clients require urgent, crisis-level intervention where in-person coordination with lawyers and estate planners is essential

- A family office situation demands real-time, multi-entity coordination across physical meetings and legal signings

- The client wants a high-touch relationship that feels tactile rather than digital

The India-Specific Context

Three segments drive virtual advisory adoption in India most visibly.

NRIs managing India-domiciled assets — NRI deposit inflows reached ₹1,15,477 crore in April–December 2024, up 42.8% year-on-year per IBEF citing RBI data. These clients hold NRE, NRO, and FCNR accounts and need DTAA structuring, FEMA compliance, and India investment management — none of which requires physical co-location with an advisor.

Professionals and CXOs in Tier-1 cities — demanding schedules make regular in-person appointments unrealistic. Virtual advisory gives them continuity without the friction.

Founders and entrepreneurs — post-liquidity events compress timelines sharply. When ₹100 crore needs structured deployment across safety, stability, and growth allocations within weeks, the ability to reach an advisor instantly — not schedule a meeting — determines the quality of the outcome.

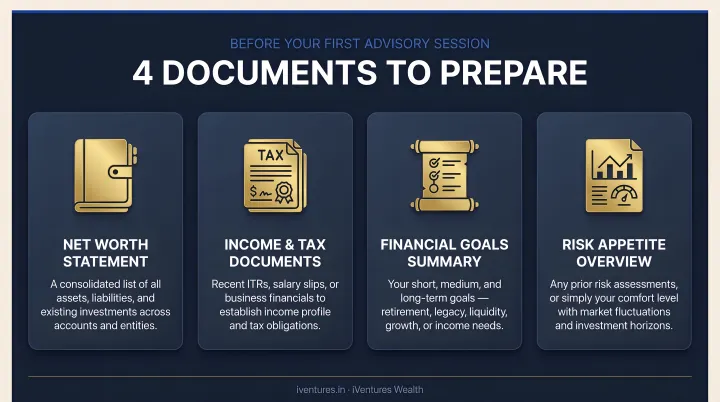

What You Need Before Your First Virtual Advisory Session

Clients who arrive unprepared force advisors to spend early sessions on data collection rather than strategy. That delays meaningful advice and reduces the value of everything that follows.

Have these ready before your first call:

| What You Need | Why It Matters |

|---|---|

| Consolidated asset and liability view | Bank accounts, mutual funds, real estate, PF, business stakes, insurance — advisors can only assess what they can see |

| Clear financial goals | Retirement corpus, liquidity needs, education funding, succession plans — no destination means no strategy |

| KYC documentation | PAN, Aadhaar, passport for NRIs, existing demat/account statements — required for SEBI-compliant onboarding |

| Risk tolerance in concrete terms | Not just "moderate" — scenarios like "I can absorb a 20% drawdown" or "I need ₹2 crore liquid within 90 days" |

SEBI's 2020 Investment Adviser framework mandates risk profiling and suitability assessment before any personalised advice. That process works properly only when clients bring complete, accurate information to the table.

Before your first session, run a quick financial self-audit. This gives your advisor the raw material to build anything useful:

- List every asset class you currently hold

- Note all outstanding liabilities

- Calculate your approximate net worth

- Define three to five specific financial outcomes you want to achieve in the next one to three years

How to Get Started: A Step-by-Step Guide

Virtual advisory follows a defined engagement sequence. Clients who skip the early stages often end up with generic advice that doesn't account for their actual situation.

Initiating the Engagement

Step 1: Schedule a discovery call. Treat this as mutual vetting, not a sales pitch. Ask directly:

- Are you SEBI-registered as an RIA? What is your registration number?

- Do you hold CFA or CFP credentials?

- What is your fee structure — AUM-based, flat fee, or hybrid?

- Do you earn any compensation from fund houses or product manufacturers?

- What technology platform do you use for portfolio reporting and document sharing?

A SEBI-registered RIA is prohibited from accepting commissions from product issuers. If the advisor cannot answer the commission question cleanly, that is your answer.

Step 2: Complete formal onboarding. Submit KYC documentation (PAN, Aadhaar, passport for NRIs, bank and investment statements). Fill out the risk profiling questionnaire honestly — inaccurate answers lead to misaligned portfolios. Read the Investment Advisory Agreement carefully, paying attention to:

- Fee disclosure (all charges, not just advisory fees)

- Conflict-of-interest clauses

- Scope of services and termination terms

iVentures Wealth, for example, handles onboarding entirely online with encrypted infrastructure. Clients receive a written agreement covering fee structure, service scope, and consent processes before any investment is made.

Monitoring and Actively Engaging

During sessions, share your complete financial picture — liabilities, tax situation, business income, upcoming liquidity events. Withholding information creates blind spots. Ask your advisor to explain every recommendation in terms of your specific goals, not just market conditions.

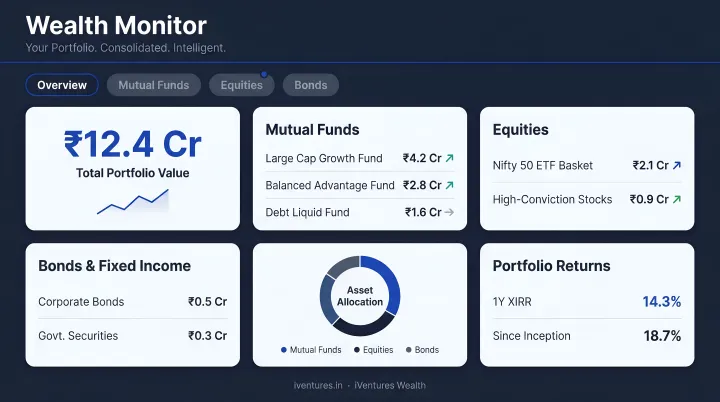

Between sessions, the work continues through your advisor's portfolio monitoring tools. Platforms like iVentures Wealth's Wealth Monitor App consolidate holdings across mutual funds, equities, bonds, FDs, PMS, and AIFs into a single dashboard — with daily performance tracking and goal progress available without waiting for the next scheduled call.

For families with HUF structures or multi-member offices, look for role-based access controls that let different members view relevant portions of the portfolio without compromising overall governance.

Reviewing and Evolving

Set a formal review schedule — quarterly for active portfolios, at minimum bi-annually. Each review should cover:

- Performance against goals, not just against benchmarks

- Asset allocation alignment with current risk profile

- Any life events requiring strategy adjustment (business exit, NRI status change, inheritance, marriage)

- Tax optimisation opportunities for the coming quarter

Know when to escalate or exit. If recommendations start feeling templated, communication becomes reactive rather than proactive, or fee disclosures become unclear — treat those as warning signs. A well-functioning virtual advisory relationship is one where the advisor initiates contact, not just responds to it.

What to Look for When Choosing a Virtual Financial Advisor in India

Regulatory Standing

Verify SEBI RIA registration first. Check the SEBI Investment Adviser public register using the advisor's registration number (it will begin with "INA"). As of August 2024, SEBI's review memo noted only 927 registered IAs operating in India — a small pool relative to the demand. Registration confirms the advisor is legally bound to a fiduciary standard and prohibited from earning product commissions.

Credentials and Research Depth

Look for CFA (Chartered Financial Analyst) or CFP (Certified Financial Planner) qualifications — these signal rigorous training in portfolio construction, equity research, and holistic financial planning. An advisor backed by a research-first team offers analysis-backed recommendations rather than product-driven ones.

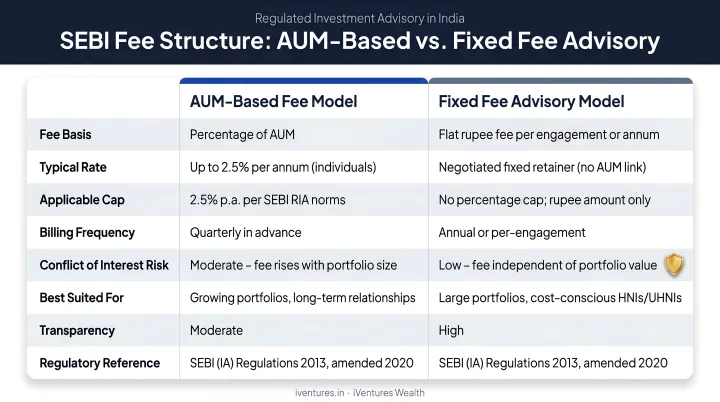

Fee Structure

Ask directly: does the advisor earn any trail income, placement fees, or commissions from fund houses or product manufacturers? Fee-only advisors are structurally more aligned with client outcomes.

SEBI's 2020 guidelines allow fees under two modes: AUA (Assets Under Advice)-based (capped at 2.5% per annum per family) or fixed fee. The key is that all charges — advisory, transaction, fund management — are disclosed in writing before you invest.

Technology Infrastructure

A capable virtual advisory platform should offer:

- Encrypted client portal for document sharing and communication

- Real-time portfolio dashboard with consolidated reporting

- Multi-entity access (personal, HUF, family, corporate)

- Goal tracking and performance analytics

Before signing on, ask the advisor for a demo of their reporting platform — what you see should give you a clear, consolidated picture of your entire portfolio, not a collection of separate fund statements.

Track Record and Client Profile Fit

Specialization matters more than general experience. An advisor who primarily serves salaried professionals is not equipped the same way as one with depth in UHNI succession planning, NRI cross-border structuring, or post-liquidity founder portfolios. Before committing, ask:

- Who is their typical client, and does your profile match?

- What is their total AUM and approximate number of relationships?

- How long have their longest-standing clients been with them?

Best Practices to Get the Most Out of Virtual Financial Advisory

Come prepared to every session. Arrive with specific questions, a note on any changes in your financial situation since the last call, and a clear agenda. A 45-minute structured session consistently delivers more value than an open-ended hour of updates.

Don't wait for scheduled reviews. If you close a business deal, receive a large inheritance, change tax residency, or take on a significant liability — inform your advisor immediately. Strategy adjusted in real time is always more effective than strategy adjusted retrospectively.

Seek guidance, not validation. This is the most common misuse of an advisory relationship. Clients who use sessions primarily to confirm decisions they've already made miss the advisor's most valuable function.

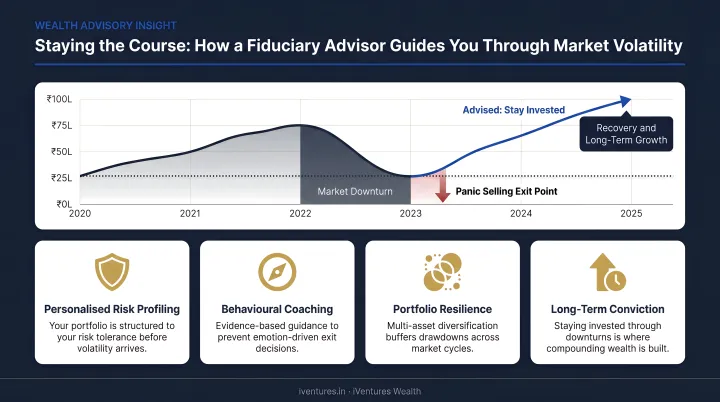

Research by Vanguard estimates advisors can add up to 3% in net returns — much of which comes from behavioural coaching: preventing panic-selling, correcting overconcentration, and surfacing risks clients haven't considered. A fiduciary-registered advisor should push back when the situation warrants it.

Maintain continuity. The value of a virtual advisory relationship compounds over time. Advisors who understand your full financial history — including past mistakes, tax positions, and family dynamics — deliver materially better advice than those who only see your current portfolio.

Frequently Asked Questions

What is a virtual financial advisor?

A virtual financial advisor is a licensed, human professional — typically SEBI-registered as an RIA in India — who delivers fiduciary-grade financial planning and investment advice through digital channels such as video calls and secure portals. This is distinct from a robo-advisor, which uses algorithms rather than human judgement.

Is it worth paying 1% to a financial advisor?

For HNIs and UHNIs, a well-structured fiduciary advisory relationship generates value in tax efficiency, portfolio optimisation, and downside protection that far exceeds the advisory cost. The 1% figure reflects AUM-based pricing — flat-fee structures may suit larger portfolios better and are worth comparing before you commit.

How do I verify that a virtual financial advisor is SEBI-registered in India?

Visit the SEBI Investment Adviser public register on the SEBI website and search by the advisor's registration number (beginning with "INA"). SEBI registration is a legal requirement for anyone providing investment advice for a fee in India and confirms fiduciary obligations are in place.

What is the difference between a virtual financial advisor and a robo-advisor?

Robo-advisors automate portfolio management using preset parameters — low-cost but standardised, with no capacity for nuance. Virtual human advisors deliver customised, judgement-based planning that accounts for your full financial context: goals, tax situation, life stage, and risk profile in ways an algorithm cannot.

What documents do I need to get started with a virtual financial advisor?

The standard requirements for SEBI-compliant onboarding are: PAN card, Aadhaar, passport (for NRIs), existing investment and bank account statements, and entity documentation for family offices or corporates. The entire process can be completed digitally.

How often should I meet with my virtual financial advisor?

Quarterly reviews are the baseline for active portfolios, with additional touchpoints triggered by major financial events, significant market moves, or life changes. A good advisor proactively initiates contact rather than waiting for the client to reach out.