Introduction

For most Indian business owners, the business is the wealth. A successful entrepreneur's promoter equity, real estate, and operating assets often account for the overwhelming majority of their net worth — yet the personal estate plan lags years, sometimes decades, behind.

That gap has a measurable cost. According to EY's Indian Family Office Playbook 2025, 22% of surveyed Indian family offices have no written succession plan or only verbal understandings — and this is among India's most affluent families, where formal documentation remains the exception.

Without a plan, both sides suffer. Business continuity collapses the moment a founder dies, becomes incapacitated, or steps away — and personal wealth transfer breaks down with it, triggering family disputes, forced asset sales, and avoidable tax leakage.

This guide addresses both sides in full: clear definitions, the three types of business succession, a five-step planning process, key legal instruments under Indian law, and the most costly mistakes to avoid.

Key Takeaways

- Estate planning governs personal assets; business succession planning governs who takes over ownership and management — both must be designed together to avoid conflicts and value destruction

- The core steps: assemble an advisory team → value the business → align personal and estate plans → select and prepare a successor → execute legal documents

- Key instruments: Wills, private trusts, buy-sell agreements, family settlement deeds, and HUF structures

- Start at least 3–5 years before any anticipated ownership transition

- Delaying until a crisis — death, disability, or a partner dispute — forces a reactive outcome and risks a fire sale of the business

What Is Estate and Business Succession Planning — And Why Must They Work Together?

Defining Estate Planning

Estate planning structures your personal assets — property, investments, financial accounts, and personal holdings — so they transfer according to your wishes upon death or incapacity. The instruments include a Will, private trust, nominations, and powers of attorney.

Defining Business Succession Planning

Business succession planning determines who will take over ownership and management of a business when the founder retires, becomes incapacitated, or passes away. It also establishes how that transition will be funded and executed — before a crisis forces the decision.

Why Integration Is Non-Negotiable

For most Indian affluent families, the business is the estate. When these two plans run on separate tracks, a succession plan transferring business shares to one heir can directly conflict with a Will distributing wealth to others. Three consequences follow reliably:

- Heirs inherit illiquid business stakes while needing cash — creating immediate financial pressure

- Poorly sequenced transfers trigger avoidable tax events that erode the estate's value

- Competing legal claims emerge when a Will and a succession agreement point in different directions

The next generation is often left unable to manage inherited assets because there are no documented governance rules — no clear distribution framework, no decision-making authority, and no continuity plan. Across 150+ affluent family relationships over 20+ years, this structural gap is among the most common issues iVentures Wealth identifies during planning reviews.

Types of Business Succession

Family Succession

Intergenerational transfer — passing ownership and management to the next generation — is the most common intended path for Indian family businesses. The challenge is rarely emotional; it's structural.

Indian families often operate under an expectation of equal inheritance, which conflicts directly with the operational reality that management should go only to capable, willing heirs. When this tension isn't addressed explicitly before documents are drafted, it becomes litigation after the founder is gone.

Globally, academic research suggests only roughly 30% of family firms reach the second generation and around 13% the third. India has no shortage of high-profile examples where succession disputes erased generational value.

Internal Succession: Management Buyout and ESOP

Where family heirs are uninterested or unprepared, a founder can transition out by selling to key management (a management buyout, or MBO) or through an employee ownership model like an ESOP. This route preserves business culture, rewards the team that built the value, and keeps operations running without ownership disruption. Mid-market founders with ₹50–200 crore businesses increasingly use this path when family heirs aren't in the picture.

The trade-off is funding. Three structures typically apply:

- Retained earnings: the cleanest option, but requires strong cash generation over time

- Acquisition financing: banks or NBFCs fund part of the buyout, with business cash flows servicing the debt

- Structured earn-out: the founder receives payment over time, tied to post-transition performance

Financial planning must precede the transition — not run parallel to it.

External Exit: Strategic Sale or Financial Buyer

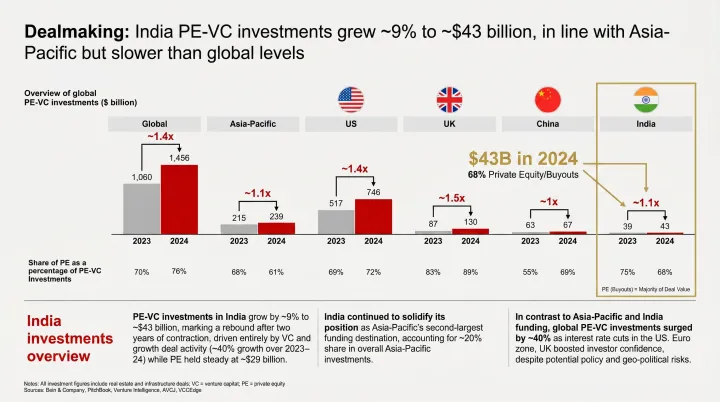

Of the three paths, selling externally — to a strategic buyer, private equity firm, or through a public market transaction — maximises financial return. It also changes the business permanently. For this path, India's PE market provides a meaningful exit pool.

Bain's India Private Equity Report 2025 shows PE-VC investments rebounded ~9% year-on-year to approximately $43 billion in 2024, with buyouts accounting for 51% of total PE deal value. Mid-market family businesses are squarely in this buyer universe.

The catch: proceeds from an external sale must be deployed thoughtfully. A ₹100 crore liquidity event left in scattered bank deposits is not a plan — it is a problem deferred. Without a deployment plan, the exit just transfers the problem from the business to the balance sheet.

Steps in Estate and Business Succession Planning

Step 1: Assemble Your Advisory Team

Succession planning is not a DIY exercise. The work spans disciplines that no single professional can cover alone.

A complete advisory team includes:

- Wealth advisor (SEBI-registered RIA) — coordinates the overall plan across financial, legal, and tax dimensions

- Chartered accountant — handles tax structuring, compliance, and reporting

- Corporate and estate planning lawyer — drafts and executes all legal instruments

- Business valuation expert (IBBI Registered Valuer) — provides credible, defensible valuations

- Insurance advisor — structures funding mechanisms for buy-sell obligations

The coordination function matters as much as the individual credentials. When advisors work in silos, their recommendations conflict — and the client bears the cost.

iVentures Wealth serves as the coordinating advisor in this model, working alongside CAs, legal practitioners, and specialist advisors so that all disciplines stay aligned toward the same succession objective — including wills, trusts, and cross-border structures within the family's overall financial strategy.

Step 2: Get a Professional Business Valuation

You cannot plan a succession without knowing what you are actually transferring or selling.

A credible business valuation determines:

- How much personal wealth the owner can expect post-exit

- What needs to improve before transition to maximise value

- How to structure inheritance fairly among heirs with and without business involvement

ICAI Valuation Standard 301 prescribes three core approaches for private business valuation: income (DCF), market (EBITDA multiples and comparable transactions), and asset-based methods. For any serious succession or exit process, engage an IBBI Registered Valuer and run at least two independent approaches to reconcile shareholder expectations with market reality.

A valuation done 12–18 months before an intended transition also gives the owner time to address what buyers or heirs will question — key-person dependencies, undocumented processes, related-party transactions, and weak corporate governance.

Step 3: Align Personal Financial and Estate Planning

Most business owners discover the same uncomfortable truth when they look closely: the majority of their net worth is illiquid, and their personal investments alone would not fund retirement.

Addressing this gap means building a protected personal corpus separate from operating business risk — with a defined drawdown rule so each profitable year builds personal financial security independent of business cycles.

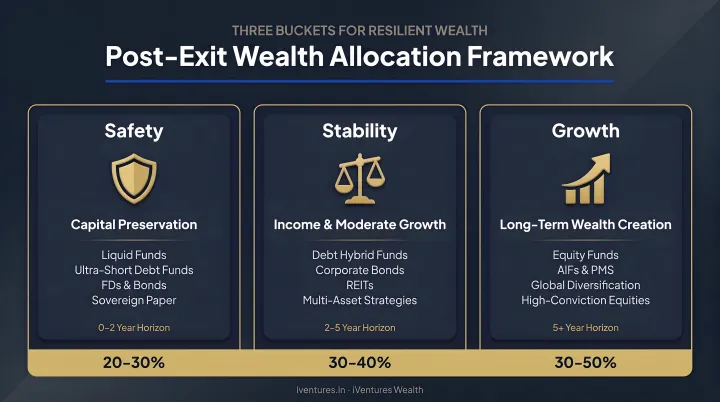

Post-exit, the approach is structured into three buckets:

- Safety — 5–7 years of living expenses in high-quality fixed income

- Stability — a balanced, asset-allocated portfolio with an 8–15 year horizon

- Growth — select AIF, PMS, and private equity opportunities

Simultaneously, the estate plan must be aligned. That means:

- Drafting or updating the Will

- Reviewing and correcting all nominations (which are not succession — see Common Mistakes below)

- Considering a private trust structure for holding promoter shares and personal assets

- Reviewing powers of attorney for incapacity scenarios

Step 4: Select and Prepare Your Successor

Choosing a successor is the most human step in the process — and often the least structured.

The criteria are straightforward: capability, willingness, and readiness. All three must be present. A capable but unwilling heir resents the role. A willing but unprepared heir destroys value.

A formal transition period should include:

- Knowledge transfer and documentation of key processes

- Mentoring with defined milestones

- Gradual handover of responsibilities before full transfer

- Clear timelines agreed in writing

Critically, family dynamics must be addressed openly before legal documents are drafted. Unresolved conflicts over successor selection frequently derail succession plans entirely. Resolving these conversations informally first makes the legal process far smoother.

iVentures Wealth's family office services include next-generation training, family charter drafting, and family governance protocols — recognising that the human side of succession must be structured with the same rigour as the legal side.

Step 5: Draft and Execute All Legal Agreements

Verbal agreements and informal understandings carry no legal weight. Every succession plan must be codified in enforceable documents.

The core instruments for Indian business owners:

| Document | Purpose |

|---|---|

| Shareholder/Partnership Agreement | Defines succession clauses, transfer restrictions, and decision-making rights |

| Buy-Sell Agreement | Pre-defines exit triggers and valuation methodology |

| Will | Governs personal asset distribution on death |

| Trust Deed | Establishes holding structure with distribution and governance rules |

| Family Settlement Deed | Divides assets by mutual consent; prevents future litigation |

Without written agreements, co-owners and family members operate on assumptions — and when pressure arrives, those assumptions become disputes.

Key Legal and Financial Instruments for Indian Business Owners

Will Under the Indian Succession Act

A Will governs how personal assets — including business shares — are distributed after death. For Hindus, intestate succession (without a Will) is governed by the Hindu Succession Act, 1956. Wills for all communities are governed by the Indian Succession Act, 1925.

One important update: the Repealing and Amending Act, 2025 removed the historical requirement that made probate mandatory in Mumbai, Chennai, and Kolkata. Probate is no longer compulsory nationwide, though it remains available and is still requested in high-value or contested situations for title comfort.

Critical misconception to correct: Nominations on bank accounts and demat accounts are not succession. SEBI's 2024 memorandum explicitly clarifies that a nominee receives assets as a trustee for legal heirs — not as a beneficial owner. Nomination facilitates transmission; it does not override a Will or succession law.

Private Trust Under the Indian Trust Act, 1882

A private trust is the instrument of choice for Indian UHNIs who want to:

- Avoid probate friction and delays

- Protect assets from creditor claims and family disputes

- Manage inheritance for minors or multiple beneficiaries across generations

- Ensure business continuity when the founder is no longer active

Under the Income-tax Act, 1961, the tax treatment depends on trust type:

- Revocable trusts — income is clubbed to the settlor

- Irrevocable determinate trusts — taxed at beneficiary-specific rates (the preferred structure)

- Irrevocable discretionary trusts — taxed at the maximum marginal rate

The EY Indian Family Office Playbook 2025 notes that private trusts have become the preferred holding structure among Indian family offices — used to isolate operating company stakes from personal estates and simplify transfers across generations.

Buy-Sell Agreements and Shareholder Agreements

A buy-sell agreement pre-defines what happens when an owner exits due to death, disability, divorce, retirement, or dispute. Without one, the remaining partners face an unknown buyer: a competitor, an estranged family member, or a court-appointed liquidator.

The agreement specifies:

- Triggers — which exit events activate the agreement

- Valuation formula — agreed methodology at the time of execution, not at the time of crisis

- Funding mechanism — typically life insurance for death triggers, and escrow or acquisition finance for others

In India, these provisions are embedded within Companies Act, 2013-compliant shareholder agreements or Indian Partnership Act, 1932 partnership deeds. For businesses with non-resident partners, FEMA and RBI pricing compliance must be built in from the start.

Family Settlement Deed

The Family Settlement Deed is a distinctly Indian instrument — a registered agreement among family members that divides business and personal assets by mutual consent, preventing future litigation before it starts.

The Supreme Court in Kale v. Director of Consolidation recognised that family settlements are binding when fair, voluntary, and intended to resolve family disputes. Where rights in immovable property are created or extinguished, registration is required for enforceability.

This instrument is particularly valuable for multi-generational businesses and joint family structures where assets have accumulated informally over decades. A properly executed deed creates a clean legal separation of interests — often the only way to draw a clear line before disputes crystallise into litigation.

HUF as a Succession and Tax Planning Structure

A Hindu Undivided Family (HUF) is recognised as a separate assessee under the Income-tax Act, 1961, with its own PAN, tax return, and applicable deductions. The Karta manages HUF assets, and income earned in the HUF's name is taxed separately from individual members.

For Hindu families (including Jains, Sikhs, and Buddhists), an HUF can meaningfully reduce individual tax burden when structured correctly.

Limitations to note:

- Applies only to Hindus — not available to Muslim, Christian, or Parsi families

- Partial partitions are not recognised for tax purposes in most contexts

- HUF alone cannot govern the succession of company shares effectively

- Should be used alongside Wills and private trusts, not as a substitute for them

Common Mistakes That Cost Business Owners Their Legacy

The fire sale scenario. When a founder dies or becomes incapacitated without a plan, the business stalls during legal proceedings, ownership becomes unclear, and value deteriorates rapidly. The family faces a choice between a protracted legal dispute and a distressed sale at a fraction of true value. Academic evidence documents average fire-sale discounts of ~8.9%, rising to ~14% under urgent deadlines — with practitioners applying 20–40% distressed-sale discounts in restructuring scenarios. This outcome is entirely avoidable with a 12–24 month runway.

Treating nomination as succession. This is among the most common misconceptions iVentures Wealth encounters during client onboarding. Many business owners update demat account nominations and believe their succession is complete. It is not. A nominee is a custodian, not a legal heir. Without a Will or trust, legal ownership follows succession law — which may not reflect the owner's intentions, and almost certainly produces delays, disputes, and administrative paralysis for heirs.

A plan that was never revisited. Business value, partnerships, tax laws, and family circumstances all shift over time. A succession plan drafted when the business was worth ₹10 crore is not the right plan when it is worth ₹150 crore. Plans must be reviewed at every material milestone:

- Significant business growth or acquisition

- New partners or investor entry

- Marriage, divorce, or birth of children

- Death of a co-founder or key stakeholder

- Material regulatory changes (such as the 2025 probate amendment)

At iVentures Wealth, every succession plan is reviewed at each of these milestones — because a plan that hasn't kept pace with your business is no plan at all.

Frequently Asked Questions

What is estate and business succession planning?

Estate planning structures personal assets (property, investments, accounts) for transfer upon death or incapacity, using instruments like Wills and trusts. Business succession planning determines who takes over ownership and management of a business and how. Together, they form a comprehensive strategy to protect both personal and business wealth across generations.

What are the steps in estate and business succession planning?

The five core steps are: assemble an advisory team, obtain a professional business valuation, align personal financial and estate plans, select and prepare a successor, and draft all necessary legal agreements. The full process typically takes 3–5 years to execute well.

What are the types of business succession?

The three main routes are family succession (intergenerational transfer), internal succession (management buyout or ESOP), and external exit (strategic or financial buyer). Tax treatment, funding structures, and family dynamics differ significantly across all three.

What is the difference between estate planning and succession planning?

The critical risk is misalignment: an estate plan that distributes business shares equally among heirs can directly contradict a succession plan naming a single managing successor. For business owners, the two must be designed together — separately drafted, they frequently create the very disputes they were meant to prevent.

When should I start succession planning for my business?

Most advisors recommend starting at least 3–5 years before the intended transition. For complex businesses, those with multiple partners, or situations requiring significant value-building before transfer, earlier is better. Waiting until a crisis removes all good options.

What happens to my business if I die without a succession plan in India?

Without a plan, the business stalls during probate, co-owners face disputes, and the estate defaults to the Hindu Succession Act or Indian Succession Act — which may not reflect your wishes. The family is typically left choosing between protracted litigation and a distressed sale at a steep discount.