Introduction

Millions of NRIs send money home every year — India received over USD 111 billion in remittances in 2022, making it the world's top remittance recipient. Yet a surprising number of those same NRIs have no structured retirement corpus in India.

That gap becomes costly. UAE residents have no state pension. Gulf employment contracts end. And research from IIPS shows that 60% of return emigrants came from Gulf countries, with the 60+ age group having the highest odds of return — meaning retirement in India is not a distant scenario for most NRIs, it's a statistical probability.

Unlike resident Indians, NRIs face a layered set of constraints — cross-border tax rules, FEMA compliance, repatriation limits, and exchange rate risk — that directly affect which retirement instruments are available and how they perform. Choosing the wrong combination costs more than most people expect, which is why understanding the full picture before committing capital matters.

This guide covers the five best retirement plans for NRIs in India in 2026, the tax and repatriation rules that govern them, and a practical framework for choosing the right combination.

Key Takeaways

- NRIs can build India-based retirement portfolios using NPS, annuity plans, mutual fund SIPs, ULIPs, and NRE Fixed Deposits

- NPS offers the highest tax deduction for retirement savings — up to ₹2 lakh per year — and is PFRDA-regulated

- NRE FD interest is fully tax-free in India; NPS lump sum (60%) at maturity is also tax-free

- NRO account repatriation is capped at USD 1 million per financial year by RBI

- Combining NPS, mutual funds, and annuity plans in a single portfolio consistently outperforms relying on any one instrument alone

Why NRIs Need a Dedicated Retirement Plan in India

Many NRIs assume their host-country retirement savings will be enough. They rarely are — at least for a retirement in India.

A UAE End of Service Gratuity (EOSG) is a lump sum, not a pension. A US 401(k) is dollar-denominated and subject to foreign withdrawal taxation. UK pension income converted to rupees is vulnerable to exchange rate swings at exactly the wrong moment — when you stop earning.

Three specific financial risks make India-based retirement planning non-negotiable:

- Exchange rate erosion — Converting foreign savings to INR during a weak rupee cycle can shrink a corpus by 10–20% before it's even deployed

- India-specific inflation — India's CPI averaged between 4.95% and 6.70% annually from 2020 to 2024 (World Bank data), meaning any fixed foreign-currency holding steadily loses real purchasing power in the Indian context

- Absent safety nets — Gulf countries provide no social security for expats after departure; Singapore's CPF is only for citizens and PRs; the US Social Security system requires 40 qualifying quarters that many NRIs haven't accumulated

These risks don't arrive gradually — they converge at the moment of return. The IIPS found that 21% of male and 29% of female return migrants were aged 60+, with a mean return age of 45. Most returns happen when overseas income stops, which is precisely when a structured India-based corpus matters most.

Starting early changes outcomes dramatically. A ₹10,000/month SIP at 10% CAGR grows to approximately ₹1.33 crore over 25 years (starting at age 35) versus just ₹41.5 lakh over 15 years (starting at age 45) — a gap of nearly ₹92 lakh from a ten-year delay. The NPS Trust retirement calculator lets NRIs model these scenarios directly.

Best Retirement Plans for NRIs in India 2026

Choosing the right retirement instrument as an NRI means navigating Indian regulations, FEMA rules, and your home country's tax treatment — all at once. The five instruments below are evaluated on NRI regulatory eligibility, tax efficiency, return potential, repatriation options, and fit across different risk profiles.

National Pension System (NPS)

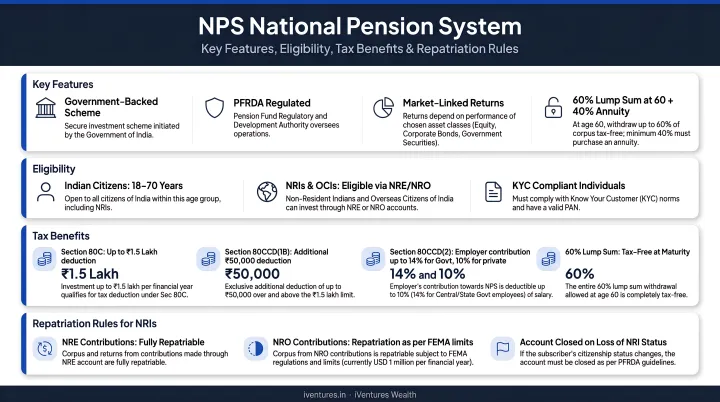

NPS is India's government-sponsored, PFRDA-regulated pension scheme — and the most tax-efficient retirement instrument available to NRIs. Indian citizens with NRI status aged 18–70 can open a Tier I NPS account online through the eNPS portal using Aadhaar or PAN verification.

Note: The PFRDA currently lists eligibility up to 85 years on their All Citizens Model page, though standard guidance for NRI accounts remains 18–70. Confirm current limits with your advisor before applying.

You can fund contributions from NRE or NRO accounts. At exit (age 60), up to 60% of the corpus can be withdrawn as a tax-free lump sum under Section 10(12A), with a mandatory 40% used to purchase an annuity.

| Feature | Details |

|---|---|

| Eligibility | Indian citizens with NRI status; OCI cardholders also eligible; PIOs without OCI are not |

| Returns | Market-linked across equity (E), corporate bonds (C), and government securities (G) |

| Tax Benefit | Up to ₹1.5 lakh under Section 80CCD(1) + ₹50,000 under Section 80CCD(1B) in the old tax regime |

| Liquidity | Partial withdrawal (up to 25%) after 3 years for specific goals; 40% mandatory annuity at 60 |

| Repatriation | Corpus is repatriable if contributed via NRE account |

One practical note: NPS deductions under Section 80CCD(1) and 80CCD(1B) are available under the old tax regime. Under the new default regime (Section 115BAC), confirm deduction availability with your tax advisor before filing.

Annuity / Pension Plans from Insurance Companies

For NRIs who want guaranteed income regardless of market conditions, IRDAI-regulated annuity plans from Indian life insurers convert a lump sum into steady monthly or annual payouts for life.

Current rate benchmarks for age 60 (single life):

- HDFC Life New Immediate Annuity Plan — 5.7% to 6.4% p.a. (with return of purchase price); 7.6% to 8.1% p.a. (without)

- ICICI Pru Guaranteed Pension Plan — ~7.64% to 7.72% p.a. (single life, without return of purchase price)

- LIC Jeevan Akshay VII — ~6.8% (life annuity) or ~5.8% (with return of purchase price) based on published examples

| Feature | Details |

|---|---|

| Eligibility | NRIs can purchase via NRE/NRO accounts; subject to insurer KYC and FEMA norms |

| Returns | Guaranteed fixed rate; locked at purchase |

| Tax Treatment | Annuity income is taxable as "income from other sources"; TDS applies; check applicable DTAA |

| Liquidity | Illiquid once annuity commences; some products offer return-of-purchase-price for nominees |

| Repatriation | Subject to NRE/NRO account rules and insurer terms |

The key trade-off: once an immediate annuity starts, the principal is inaccessible. Deferred annuity options — where the payout begins at a future date — suit NRIs still working abroad who want to lock in a rate now.

Mutual Fund SIPs (Equity and Hybrid)

Mutual fund SIPs offer NRIs the highest long-term growth potential among India's regulated retirement instruments, with full liquidity and no lock-in (except ELSS funds, which have a 3-year lock-in).

NRIs invest via NRE or NRO accounts. SEBI confirms that NRIs with NRE/NRO accounts can invest in Indian mutual funds without requiring a Portfolio Investment Scheme (PIS) permission for mutual fund transactions.

Important restriction for US and Canada-based NRIs: Due to FATCA compliance requirements, many AMCs do not accept investments from US/Canada residents online. SBI Mutual Fund accepts US/Canada NRI investments but only through offline applications. UTI MF explicitly restricts online access for US investors. Check directly with individual AMCs before investing.

| Feature | Details |

|---|---|

| Eligibility | Most NRIs via NRE/NRO; US/Canada NRIs must verify AMC-specific FATCA compliance |

| Returns | Market-linked; equity funds historically 10–14% CAGR over long horizons (verify with current AMFI data) |

| Tax Treatment | LTCG above ₹1.25 lakh taxed at 12.5%; STCG at 20%; no 80C benefit |

| Liquidity | High; redeem anytime; no lock-in except ELSS (3 years) |

| Repatriation | Fully repatriable from NRE account |

NRE Fixed Deposits

NRE Fixed Deposits are the simplest, lowest-risk tool in an NRI retirement portfolio — and the interest earned is tax-free in India. Both principal and interest are fully repatriable per RBI's account regulations.

Current NRE FD rates from leading banks (as of mid-2026):

- SBI: 6.25% (1 year), 6.40% (2 years), 6.05% (5 years) — effective 15 March 2026

- Axis Bank: 6.25% (1 year), 6.45–6.60% (18 months to 2 years)

- ICICI Bank: ~6.45% (2–3 years), ~6.50% (5–10 years)

| Feature | Details |

|---|---|

| Eligibility | Any NRI with a valid NRE account |

| Returns | Fixed; currently ~6.05–6.60% p.a. across 1–5 year tenures |

| Tax Treatment | Interest tax-free in India; check tax treatment in country of residence under DTAA |

| Liquidity | Premature withdrawal possible with penalty; highly liquid relative to other instruments |

| Repatriation | Fully repatriable |

NRE FDs are not a growth vehicle. For NRIs in their 50s shifting toward capital preservation, they work best alongside equity SIPs or NPS — providing a stable, tax-free income floor while market-linked instruments handle long-term growth.

Tax Benefits and Repatriation Rules for NRI Retirement Investments

For NRIs building a retirement corpus in India, tax efficiency and repatriation flexibility are just as important as the returns themselves. Here's what you need to know before committing capital.

Key Deductions

- Section 80CCD(1): NPS contribution deduction up to 10% of gross total income, within the overall Section 80CCE cap of ₹1.5 lakh

- Section 80CCD(1B): Additional ₹50,000 deduction exclusively for NPS, bringing total NPS deductions to ₹2 lakh per year

- These deductions apply under the old tax regime. The new default regime (Section 115BAC) has different deduction rules — verify with your tax advisor for FY 2025–26

DTAA — Why It Matters

NRIs may face tax on Indian investment income both in India and in their country of residence. DTAA treaties reduce or eliminate this double taxation.

Key country positions:

- UAE: No personal income tax in UAE; gains and income taxed only in India under the DTAA

- US: India-US DTAA applies; capital gains treatment depends on asset type and holding period; US persons with Indian mutual funds may face PFIC complications

- UK, Canada, Singapore, Australia: DTAAs exist with India; specific treatment of pension/annuity income and capital gains varies by treaty article

To claim DTAA benefits, NRIs must obtain a Tax Residency Certificate (TRC) from their country of residence and file it with their Indian bank or fund house.

TDS for NRIs

TDS rates for NRIs are higher than for residents. Capital gains from mutual fund redemptions are subject to TDS: 12.5% for LTCG and 20% for STCG on equity funds per the Income Tax Department's non-resident taxation guide.

Note: Forms 15G and 15H are designed for resident individuals and are generally not applicable to NRIs for reducing TDS. NRIs can claim DTAA relief directly through TRC and Form 10F filing.

Repatriation Caps

- NRE accounts: Fully and freely repatriable (principal + interest)

- NRO accounts: Subject to an annual cap of USD 1 million per financial year, with applicable taxes and conditions per RBI master circulars

- NPS corpus: Repatriable if originally contributed via NRE account

- ULIPs and annuity income funded via NRO accounts may face repatriation restrictions

How to Choose the Right Retirement Plan as an NRI

Three questions determine the right instrument mix:

- Where do you plan to retire? If in India, repatriability matters less. If abroad, every instrument must have a clear repatriation path.

- How many years until retirement? Longer horizons allow more equity exposure via NPS and mutual funds. Under 5 years, capital preservation takes priority.

- What monthly income do you need? Working backward from a target income determines the corpus required. At a 5.8% annuity rate, generating ₹50,000/month requires approximately ₹1.04 crore. At 7%, the same income requires around ₹85.7 lakh.

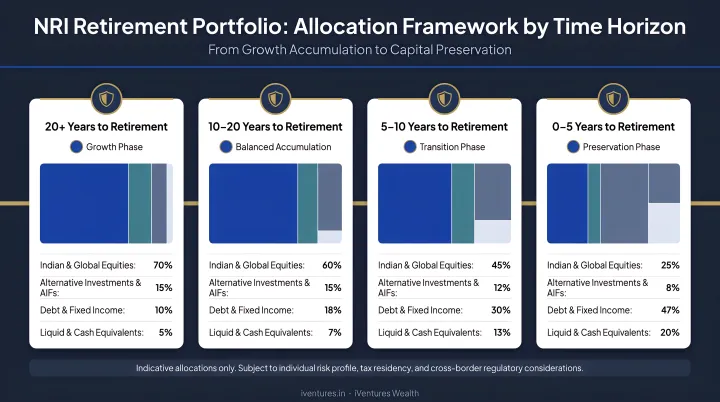

Allocation Framework by Retirement Timeline

| Timeline | Suggested Focus |

|---|---|

| 10+ years to retirement | NPS (for tax efficiency) + Equity Mutual Fund SIPs (for growth); NRE FDs for emergency liquidity |

| 5–10 years | Shift toward hybrid mutual funds; maintain NPS; begin building annuity or NRE FD allocation |

| Under 5 years | Emphasize annuity plans and NRE FDs for income certainty; reduce equity exposure progressively |

Four Mistakes NRIs Commonly Make

- Relying entirely on the host country's retirement plan with no India-based savings

- Investing in NPS without understanding the mandatory 40% annuity purchase at exit

- Ignoring TDS and DTAA planning — and paying taxes that could legally be reduced or eliminated

- Funding instruments through NRO accounts when the intention is to retire abroad, creating repatriation complications later

Cross-border tax planning, FEMA compliance, and multi-jurisdiction portfolio structuring are genuinely complex — working with a SEBI-registered investment adviser who specialises in NRI portfolios can significantly reduce tax drag and repatriation errors.

iVentures Wealth (SEBI RIA INA000019026), with 20+ years of experience and a dedicated NRI/OCI advisory practice, helps NRIs build personalised, tax-optimised retirement strategies covering both Indian and overseas financial goals, including DTAA structuring for UAE, US, UK, Canada, Singapore, and Australia residents.

Conclusion

There is no single best retirement plan for all NRIs. The right strategy depends on where you plan to retire, your tax residency, your investment horizon, and whether you need repatriable funds. For most NRIs, the most balanced approach combines three instruments:

- NPS — for tax efficiency and structured retirement corpus

- Equity mutual funds — for long-term growth and inflation protection

- Annuity plans or NRE FDs — for predictable, repatriable income

The compounding math makes the case for starting early better than any argument can. A ₹10,000/month investment at 10% CAGR from age 35 builds roughly ₹1.33 crore by 60. Starting at 45 produces just ₹41.5 lakh — less than a third of the corpus, for only ten fewer years of investing.

If you're an NRI or OCI looking to structure a retirement plan that is compliant, tax-efficient, and aligned with your goals across geographies, iVentures Wealth (SEBI Registered, INA000019026) offers fiduciary, conflict-free retirement planning advisory. Reach out via info@iventures.in or WhatsApp at +91 99999 85119 for a personalised consultation.

Frequently Asked Questions

Which is the best pension plan for NRI in India?

There is no single best plan — NPS is optimal for tax efficiency and government-backed structure, annuity plans work best for guaranteed lifetime income, and mutual fund SIPs offer the highest long-term growth potential. Combining all three based on your timeline and risk profile typically delivers the best outcome.

Can NRIs get a pension in India?

Yes. NRIs can receive pension income through three main routes: NPS (which mandates 40% of the corpus for annuity purchase at age 60), private annuity plans from IRDAI-registered insurers, and employer pension schemes accumulated before attaining NRI status.

How do I get ₹50,000 pension per month?

At a 5.8% annuity rate, you would need a corpus of approximately ₹1.04 crore. At 7%, the required corpus drops to about ₹85.7 lakh. Use an annuity calculator from any IRDAI-registered insurer to model current rates based on your age and payout preference.

Can NRIs invest in NPS in India?

Yes. Indian citizens with NRI status aged 18–70 can invest through the eNPS portal using NRE or NRO accounts. OCI cardholders are also eligible. PIOs without OCI status are not eligible based on current PFRDA guidelines.

What happens to NPS when an NRI returns to India permanently?

The NPS account continues seamlessly under the All Citizens Model. Upon return, the NRI simply needs to update their KYC and bank details to a resident Indian account. All accumulated corpus and tax benefits remain fully intact.

Is income from NRI retirement plans taxable in India?

It depends on the instrument. NRE FD interest and NPS lump sum (60% at maturity under Section 10(12A)) are tax-free in India. Annuity income is taxable as other income; equity mutual fund gains attract LTCG (12.5%) and STCG (20%). Always verify applicable DTAA provisions with your country of residence to avoid double taxation.