For UHNIs, founders, and active investors managing equity portfolios, real estate, and business assets, the tax drag from poorly timed capital gains decisions can rival — and sometimes exceed — the cost of a bad investment call. This article examines how capital gains liability builds, what drives it, and the strategies that can legally and materially reduce it.

Key Takeaways

- Holding period matters: STCG on listed equity is taxed at 20%, while LTCG above ₹1.25 lakh attracts only 12.5% — a gap wide enough to drive significant tax savings

- Mutual fund scheme switches, buyback proceeds, and unlisted share exits all trigger capital gains, often without obvious warning

- Tax-loss harvesting, gain timing across financial years, and Section 54/54F exemptions rank among the highest-impact planning tools available

- Treat capital gains planning as a year-round discipline embedded in portfolio management, not a reactive end-of-March scramble

How Capital Gains Tax Liability Builds Up for Indian Investors

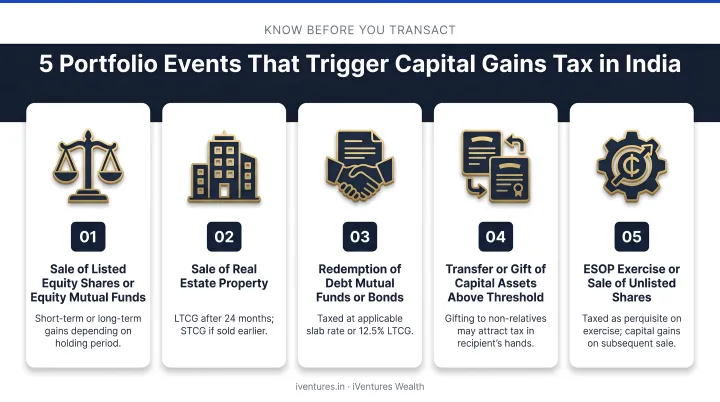

Most investors mentally link capital gains tax to dramatic events — a property sale, an IPO exit, or liquidating a large equity position. The reality is more incremental, and more expensive.

Routine portfolio activity generates taxable events constantly:

- SIP redemptions and fund switches — AMFI classifies switch-outs as redemption applications and switch-ins as fresh purchases, meaning every scheme change is a taxable event

- Mutual fund rebalancing — moving from one fund category to another (say, from a large-cap fund to a flexi-cap) triggers capital gains, even if no cash leaves your account

- Buyback proceeds — post October 2024, buyback proceeds are taxable in the shareholder's hands as deemed dividends; the acquisition cost becomes a separate capital loss entry

- Unlisted share exits and ESOP sales — these are frequently overlooked until they surface at tax filing

For HNIs and UHNIs experiencing multiple such events in a single financial year — equity sales, mutual fund exits, and real estate transactions simultaneously — the cumulative taxable gain can push total income into surcharge territory, materially increasing the effective rate.

That higher effective rate compounds another problem: every rupee paid in tax today is a rupee that stops compounding. A ₹50 lakh STCG tax bill paid today represents not just ₹50 lakh lost — it represents the future value that capital would have generated over the next decade.

Key Factors That Determine Your Capital Gains Tax Burden

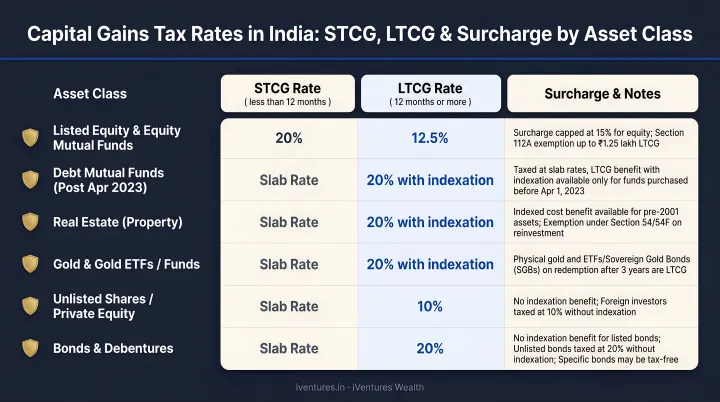

Holding Period: The Single Largest Variable

Selling even a month before the qualifying holding period can double the effective tax rate on some assets. The threshold differs by asset class — and the table below shows exactly how much is at stake.

| Asset Class | LTCG Holding Period | STCG Rate | LTCG Rate |

|---|---|---|---|

| Listed equity shares & equity mutual funds | > 12 months | 20% (Section 111A) | 12.5% above ₹1.25 lakh (Section 112A) |

| REITs / InvITs (listed units) | > 12 months | 20% | 12.5% |

| Debt mutual funds (acquired on/after 1 April 2023) | No LTCG benefit | Slab rates (Section 50AA) | Slab rates |

| Immovable property | > 24 months | Slab rates | 12.5% (without indexation) |

| Physical gold | > 24 months | Slab rates | 12.5% |

| Unlisted shares | > 24 months | Slab rates | 12.5% |

Source: CBDT FAQs on the capital gains tax regime, PIB, post-Budget 2024 (applicable for transfers on or after 23 July 2024)

Surcharges Compound the Stated Rates

The headline rates above are only part of the picture. For investors with total income above ₹50 lakh:

- 10% surcharge applies above ₹50 lakh; 15% surcharge above ₹1 crore

- A 20% STCG rate becomes effectively 23.92% with 15% surcharge and 4% cess

- A 12.5% LTCG rate becomes 14.95% — though surcharge on Sections 111A/112A gains is capped at 15%

For UHNIs realising large gains in high-income years, this surcharge effect directly changes the planning calculus — and should be modelled before any transaction, not after.

When Gains Are Realised Matters as Much as What You Sell

Realising a large gain in a year when other income is already high can push effective tax rates up significantly. For founders and promoters expecting a major liquidity event, sequencing the realisation across financial years — and timing it against other income — is as consequential as the asset selection itself.

Strategies to Reduce Your Capital Gains Tax Liability

Unchecked capital gains tax is one of the most consistent drags on long-term wealth — not because investors ignore it, but because they address it too late. Reduction works across three distinct levels: the investment decision itself, how the portfolio is managed over time, and the structural context in which assets are held.

Strategies That Start With Investment Decisions

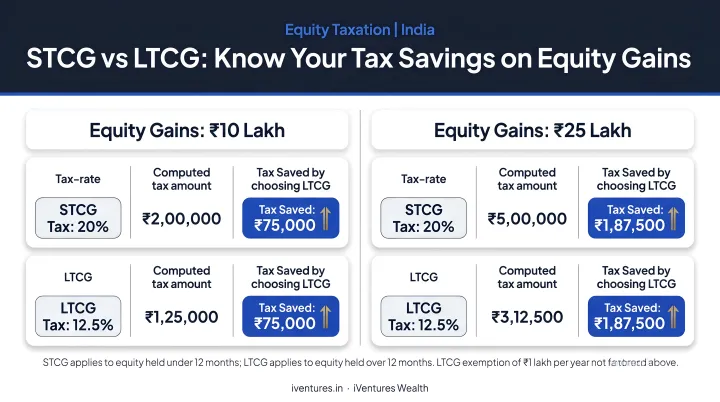

Prioritise long-term holding periods

The rate differential between STCG and LTCG for listed equity is substantial. Consider the numbers before surcharge and cess:

| Realised Gain | Sale at 11 Months (STCG 20%) | Sale at 13 Months (LTCG 12.5%, after ₹1.25 lakh exemption) | Tax Saved |

|---|---|---|---|

| ₹10 lakh | ₹2,00,000 | ₹1,09,375 | ₹90,625 |

| ₹25 lakh | ₹5,00,000 | ₹2,96,875 | ₹2,03,125 |

Waiting two months on a ₹25 lakh position saves over ₹2 lakhs. For larger portfolios with surcharges applied, the savings are proportionally greater.

Apply grandfathering provisions for pre-2018 equity

For equity shares and equity mutual fund units acquired before 31 January 2018, the cost of acquisition under Section 112A is the higher of actual cost and the lower of (a) fair market value on 31 January 2018 and (b) actual sale consideration.

Example: Actual cost ₹100, FMV on 31 January 2018 ₹400, current sale price ₹600. Taxable gain = ₹200 (not ₹500). This grandfathering provision substantially reduces the taxable gain on long-held positions — but only if the FMV on that date is properly documented. This is one reason maintaining lot-level cost records with acquisition dates is not optional for serious investors.

Use Section 54 and 54F exemptions for real estate gains

When selling a long-term residential property (Section 54) or any other long-term capital asset (Section 54F), reinvesting proceeds into a new residential property within specified timelines allows investors to claim full or partial exemption:

- Purchase a new property 1 year before or 2 years after the sale, or construct within 3 years

- From AY 2024-25, the exemption under Section 54F is capped at ₹10 crore — UHNI clients cannot assume full rollover relief on very large exits

- If reinvestment isn't completed before the ITR due date, unutilised proceeds can be deposited in the Capital Gains Account Scheme (CGAS), preserving the exemption while the investment is identified

iVentures Wealth provides advisory support on Section 54, 54EC, and 54F exemptions for real estate transactions, including guidance on CGAS deposits and reinvestment timelines — particularly relevant for clients exiting significant property holdings.

Direct surplus into tax-efficient instruments

ELSS funds (Section 80C deductions), NPS (deferred taxation), and PPF (EEE-exempt status) reduce the portion of a portfolio generating annual taxable events. These instruments earn their place on merit and tax alignment combined — not on tax saving alone.

Strategies That Change How the Portfolio Is Managed

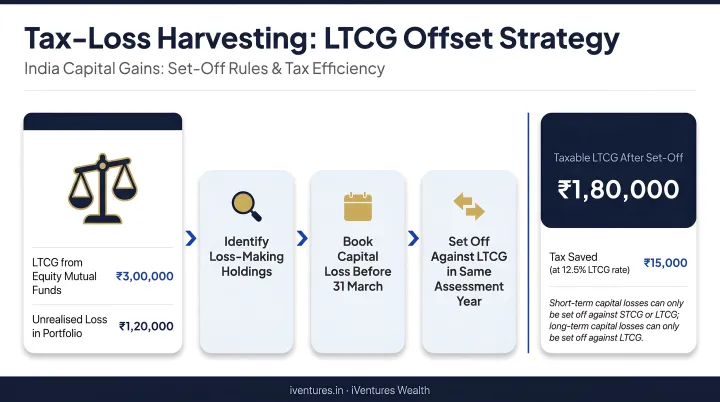

Tax-loss harvesting to offset realised gains

Selling underperforming positions at a loss in the same financial year offsets the taxable gain pool. The set-off rules under Section 74 are specific:

- Short-term capital loss (STCL) can offset both STCG and LTCG

- Long-term capital loss (LTCL) can only offset LTCG

- Unabsorbed losses can be carried forward for up to 8 assessment years, but only if the ITR is filed on time

Quick example: An investor realises ₹15 lakh LTCG on an equity position. By simultaneously booking ₹5 lakh LTCL on an underperforming debt holding, the net taxable LTCG reduces to ₹10 lakh, saving roughly ₹62,500 at the 12.5% rate (before surcharge and cess). Missing the ITR deadline forfeits the carry-forward entirely.

iVentures Wealth integrates tax-loss harvesting into quarterly portfolio reviews, identifying harvesting windows as part of a structured rebalancing process for HNI and UHNI clients — not as a year-end scramble.

Time gain realisation deliberately across financial years

Spreading a large capital gain event across two financial years — particularly when income will be lower in the subsequent year — can reduce both the tax rate and surcharge exposure. For founders and promoters facing secondary sales, buyback exits, or IPO-related liquidity, this sequencing decision alone can save several crore rupees in effective tax.

Tax-aware portfolio rebalancing

Indiscriminate rebalancing — selling winners without regard to holding periods or gain size — generates avoidable taxable events. A tax-aware approach evaluates both the investment rationale and tax cost of every rebalancing decision before execution.

As a SEBI-registered investment adviser, iVentures Wealth builds tax-awareness into its open-architecture portfolio management. Because the firm operates on a fee-only basis with no commission income, it has no structural incentive to recommend switches — decisions are evaluated on the merits of portfolio construction and the tax consequences of execution.

Use HUF structures or family transfers strategically

An HUF is taxed as a separate entity with its own basic exemption limit (₹2.5 lakh under the old regime, ₹3 lakh under the new regime) and separate capital gains slabs. Transferring investments to lower-income adult family members before sale can also reduce the family-level tax burden.

Clubbing provisions must be carefully evaluated. Per the Income Tax Department, income from property transferred to an HUF without adequate consideration is clubbed back with the transferor. Gifting assets to adult children avoids the Section 64(2) issue specifically, but gift, succession, and control implications still warrant a qualified adviser's review before execution.

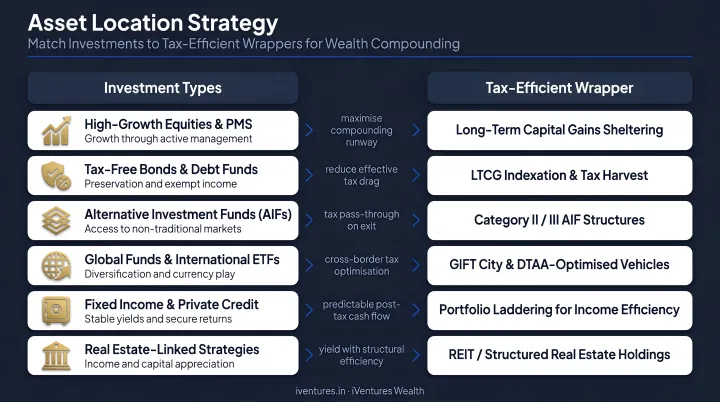

Strategies That Change the Context Around the Investment

Asset location — match assets to tax-efficient wrappers

Where an asset is held is as important as what it is. Gains within a ULIP or NPS are either deferred or exempt at maturity. Holding growth-oriented assets in such tax-deferred wrappers, where eligible, allows compounding to work on the pre-tax amount longer — reducing annual taxable events and deferring the capital gains conversation entirely.

NRI and DTAA-based structuring

NRIs and OCIs investing in India are subject to Indian capital gains tax, but Double Taxation Avoidance Agreements (DTAAs) with certain countries can reduce or eliminate withholding tax on specific gains. Two important caveats:

- The Mauritius and Singapore treaties — historically used for equity gain planning — shifted to source-based taxation for shares acquired on or after 1 April 2017. Pre-2017 grandfathered positions aside, these routes no longer provide broad shelter

- CBDT Circular 01/2025 on the Principal Purpose Test (PPT) under the MLI means structures without genuine commercial substance can have treaty benefits denied

CBDT Circular 01/2025 makes clear that jurisdiction-specific planning — rather than generic treaty structuring — is now the only reliable approach. For NRI and OCI clients, iVentures Wealth provides cross-border tax planning support covering DTAA optimisation across 90+ jurisdictions, TDS planning on Indian asset sales, and Form 15CA/15CB compliance for remittances.

Conclusion

Capital gains tax reduction is not a filing exercise — it's a year-round discipline. The investors who pay the least capital gains tax are typically those who made decisions earlier in the holding period: they waited an extra month before selling, harvested a loss before year-end, or structured a real estate exit with CGAS in mind three months before completion.

For UHNIs, founders, and families managing significant asset portfolios, this kind of planning pays off most when it's woven into portfolio construction, rebalancing, and succession decisions — not retrofitted at filing time. The conversations that protect wealth aren't the ones you have in March. They're the ones you have before the asset moves.

Frequently Asked Questions

What is the best way to reduce capital gains tax in India?

The most effective approach combines extending holding periods past the LTCG threshold, using tax-loss harvesting to offset realised gains within the same financial year, and timing large sale events to fall in years with lower overall income. Proactive planning throughout the year — not just at the point of sale — is what separates effective tax management from last-minute damage control.

What is the "50% rule" for capital gains?

This is a US concept — the IRC Section 1202 exclusion for qualified small business stock held over 5 years. India has no equivalent. The closest analogs are the ₹1.25 lakh annual LTCG exemption (Section 112A), Section 54/54F reinvestment exemptions capped at ₹10 crore, and the loss set-off and carry-forward provisions under Section 74.

What is the difference between short-term and long-term capital gains tax in India?

STCG applies to assets sold before the qualifying holding period — for listed equities, that's under 12 months — and is taxed at 20% (Section 111A). LTCG applies to assets held longer and is taxed at 12.5% above ₹1.25 lakh (Section 112A). For real estate, gold, and unlisted shares, the LTCG threshold is 24 months, with different rate implications.

Can capital losses be carried forward in India?

Yes. Unabsorbed capital losses can be carried forward for up to 8 assessment years under Section 74 — but only if the ITR is filed on time. LTCL can only offset LTCG, while STCL can offset both STCG and LTCG. Missing the filing deadline forfeits the carry-forward right entirely.

Are capital gains from mutual funds taxed differently from equity shares?

Equity-oriented mutual funds follow the same STCG/LTCG treatment as listed equity shares. Debt mutual funds acquired on or after 1 April 2023 fall under Section 50AA and are taxed at slab rates regardless of holding period — eliminating the LTCG benefit that previously made long-held debt funds tax-efficient.

Can NRIs claim capital gains tax exemptions in India?

Yes. NRIs are subject to Indian capital gains tax on Indian assets and can claim Section 54/54F exemptions for property reinvestment if statutory conditions are met. DTAA provisions in their country of residence may also reduce withholding tax on certain gains. Post-2017 changes to Mauritius and Singapore treaty treatment, along with the MLI's Principal Purpose Test, mean jurisdiction-specific structuring requires specialist advice.