What surprises many NRIs is that this burden is not fixed. The Indian tax framework includes several government-sanctioned mechanisms — DTAA claims, ITR-based refunds, and smart account structuring — that can substantially reduce what gets withheld at source.

This guide covers the exact TDS rates you're paying, the three main strategies to reduce them, how to structure your accounts more efficiently, and the compliance documents you need to make it all work.

Key Takeaways

- TDS on NRO interest is mandatory at 30% base rate; surcharge and 4% cess push the effective rate to 31.2%–42.744% depending on income slab

- DTAA-eligible NRIs can claim 10–15% withholding rates by submitting a TRC and Form 10F to their bank before interest is credited

- Filing an ITR-2 in India allows NRIs to claim deductions and recover excess TDS as a refund

- Foreign-sourced income routed through NRE accounts avoids TDS entirely — NRE interest is fully exempt under Section 10(4)(ii)

- Valid PAN and annual document submission are prerequisites for accessing any lower TDS rate

Understanding TDS on NRO Accounts: What You Are Actually Paying

An NRO (Non-Resident Ordinary) account is a rupee-denominated account NRIs use to hold income earned within India — rent, dividends, pension, fixed deposit returns, or any other India-sourced income. Because this income originates in India and is chargeable under Indian tax law, the government taxes it at source before it ever reaches you.

The Governing Law and Why There's No Threshold

TDS on NRO accounts is governed by Section 195(1) of the Income Tax Act, 1961, which mandates deduction on any interest or chargeable sum paid or credited to a non-resident, at the time of credit or payment — whichever comes first. Section 195 contains no minimum monetary threshold.

Unlike resident Indians, who benefit from Section 194A exemptions, NRIs pay TDS on every rupee of NRO interest — regardless of how small the amount.

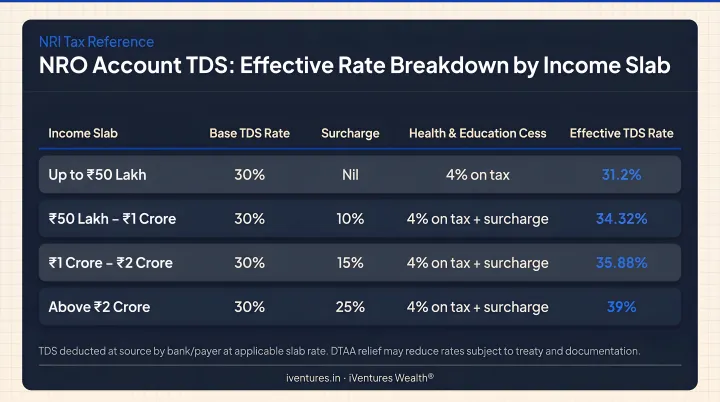

The Actual Rate Stack

The base rate of 30% is just the starting point. Surcharges are added based on total income, and then a flat 4% Health and Education Cess applies on top of tax plus surcharge.

| Total Income Band | Surcharge | Effective Rate on NRO Interest |

|---|---|---|

| Up to ₹50 lakh | 0% | 31.20% |

| ₹50 lakh – ₹1 crore | 10% | 34.32% |

| ₹1 crore – ₹2 crore | 15% | 35.88% |

| ₹2 crore – ₹5 crore | 25% | 39.00% |

| Above ₹5 crore (old regime) | 37% | 42.744% |

| Above ₹5 crore (new regime) | 25% | 39.00% |

Source: Income Tax Department — Non-Resident Individual, AY 2026-27

From FY 2023-24 (AY 2024-25), the new tax regime under Section 115BAC became the default for all taxpayers including NRIs. Under the new regime, the surcharge for income above ₹5 crore is capped at 25%, which is why the maximum effective rate under the new regime is 39% rather than 42.744%.

NRO vs. NRE: The Core Contrast

Interest on NRE savings accounts and NRE fixed deposits is fully exempt from Indian income tax under Section 10(4)(ii). No TDS applies. This makes the choice between account types one of the most consequential tax planning decisions an NRI can make — one many overlook until after a significant amount has already been withheld.

That said, the account type choice is only the first lever. For income that must flow through an NRO account, the effective TDS rate can still be reduced substantially — through DTAA claims, form submissions, and income restructuring strategies covered in the sections below.

Strategies to Reduce TDS on Your NRO Account

Leverage DTAA to Lower Your Withholding Tax Rate

A Double Tax Avoidance Agreement (DTAA) is a bilateral treaty between India and another country designed to prevent the same income from being taxed in both jurisdictions. Under Section 90 of the Income Tax Act, where a DTAA applies, the more beneficial treatment — either the domestic rate or the treaty rate — governs.

For NRO interest, treaty rates are consistently lower than India's 30% domestic rate.

DTAA interest rates for common NRI countries:

| Country | Ordinary NRO Interest Rate | Notes |

|---|---|---|

| UAE | 12.5% | 5% for specified bank/financial institution categories |

| USA | 15% | 10% for bank loan-type interest |

| UK | 15% | Government-related interest may be exempt |

| Canada | 15% | Certain government bond categories exempt |

| Singapore | 15% | 10% for specified banking interest |

| Australia | 15% | Governmental financing categories may be exempt |

The DTAA benefit is not automatic. Section 90(4) makes a Tax Residency Certificate (TRC) a statutory precondition for claiming treaty relief. The NRI must submit the required documentation to their bank before interest is credited. Once approved, the bank deducts TDS at the treaty rate rather than 30% for that financial year.

Miss the submission window, and the bank defaults to the domestic 30% rate — at which point filing an ITR and claiming a refund becomes the primary recourse.

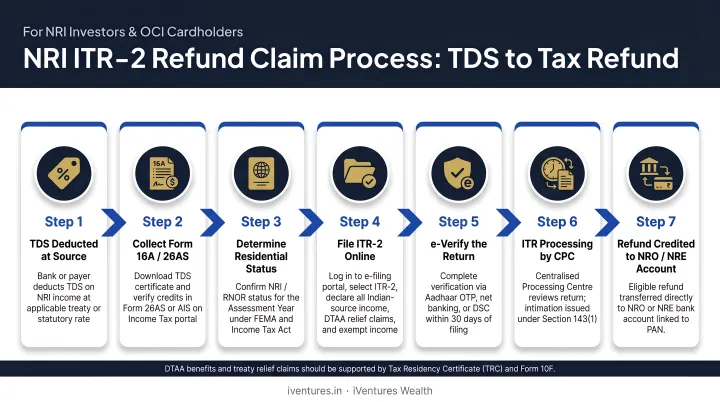

File Your ITR to Claim Deductions and Get a Refund

Even after TDS is deducted at the standard rate, NRIs can file an Income Tax Return in India to reconcile their actual tax liability. The applicable form for non-resident individuals with investment income (excluding business income) is ITR-2, available for online filing on the Income Tax e-filing portal.

When does filing generate a refund?

- If total Indian income for the year falls below the basic exemption limit — ₹2.5 lakh under the old regime, or ₹4 lakh under the new regime (for AY 2026-27) — the NRI can claim a full refund of all TDS deducted

- If actual tax payable (after deductions) is less than TDS already withheld, the excess is refunded to the NRI's pre-validated Indian bank account

Deductions available when filing under the old regime:

- Section 80TTA: Up to ₹10,000 deduction on NRO savings account interest (not applicable to fixed deposits)

- Section 80C: Up to ₹1.5 lakh for eligible India-linked investments such as life insurance premiums or housing loan principal repayment — verify each instrument for NRI eligibility before relying on this

The refund route is particularly useful for NRIs whose total Indian income is modest — for instance, someone earning ₹1.5 lakh in NRO savings interest who had 31.2% withheld can recover the entire amount through ITR filing.

Smart Account Structuring: Rethinking NRO vs NRE

Beyond filing and treaty claims, the most durable tax reduction comes from restructuring where income sits. Keeping less in NRO accounts — and more in tax-exempt structures — cuts TDS exposure at the source.

The case for NRE:

NRE accounts hold rupee funds sourced from foreign income, and the interest earned is completely tax-free. The principal is freely repatriable. NRIs who receive salary, business income, or other foreign-sourced funds should route these directly into NRE accounts rather than NRO accounts — this eliminates TDS exposure on that portion of income entirely.

NRO-to-NRE transfers:

For funds already sitting in NRO accounts, the RBI permits NRIs and PIOs to remit up to USD 1 million per financial year from their NRO account balance — including transfers to NRE accounts — provided the NRI has paid applicable Indian taxes. Once funds move to NRE, future interest earned is tax-free.

Banks typically require Form 15CA (an online declaration) and, for transfers exceeding ₹5 lakh not covered by a withholding order, Form 15CB (a Chartered Accountant certificate). Requirements vary by bank and remittance type — confirm the specifics before initiating the transfer.

FCNR accounts as a third option:

Foreign Currency Non-Resident (FCNR) accounts allow NRIs to hold term deposits in foreign currencies — USD, GBP, EUR, and others — with interest exempt under Section 10(15)(iv)(fa).

For NRIs who want to park foreign currency in India without converting to rupees, FCNR sidesteps both currency risk and Indian income tax on interest. Unlike NRO, FCNR interest does not attract TDS.

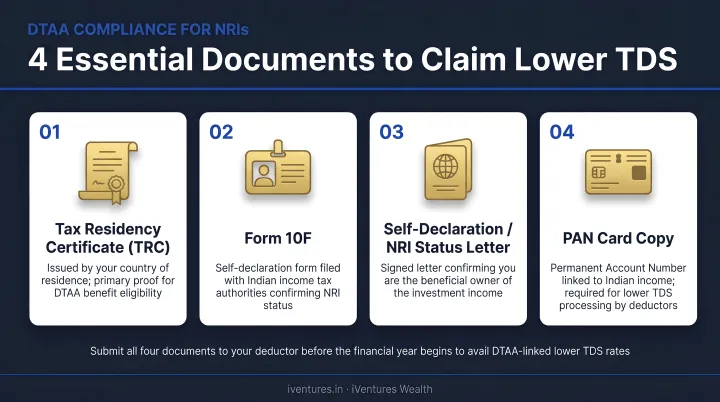

Compliance Essentials: Documents Every NRI Must Have Ready

Claiming DTAA benefits requires proactive documentation submitted to the bank before interest is credited. Missing even one item means the bank reverts to the default 30% rate.

The Four Key Documents

| Document | What It Is | Important Notes |

|---|---|---|

| Tax Residency Certificate (TRC) | Issued by the tax authority of your country of residence | Statutorily required under Section 90(4) — without this, no DTAA claim is valid |

| Form 10F | Bridges any information gaps in the TRC | Must be filed electronically on the IT e-filing portal per DGIT Notification No. 03/2022 (July 2022) |

| Self-attested PAN copy | Confirms your Indian tax identity | Without PAN, Section 206AA mandates TDS at a higher rate |

| No PE Declaration | Confirms you have no permanent establishment in India | Required at the bank level; should state that you have no fixed place of business or agent in India through which income is derived |

These documents must be submitted annually, typically before the start of each financial year. South Indian Bank, for example, specifies Form 10F and PAN copy must be submitted at the beginning of each financial year and no later than 15 April to retain DTAA benefit for that year.

The PAN Situation

Section 206AA imposes higher TDS where PAN is not furnished. However, under Section 206AA(7) read with Rule 37BC, non-residents receiving interest income may avoid the higher rate without a PAN if they provide the following:

- Full name and contact details (email ID and phone number)

- Country of residence address

- Tax Residency Certificate (where available)

- Foreign Tax Identification Number

Documentation is mandatory regardless — the PAN exemption is a conditional relief, not a blanket waiver.

Managing this documentation across multiple NRO accounts and jurisdictions — US, UK, UAE, Singapore, Canada, Australia — adds meaningful administrative complexity. At iVentures Wealth, our NRI/OCI advisory practice handles the full compliance cycle: TRC coordination, Form 15CA/15CB filings, and annual renewal tracking, as part of an integrated cross-border wealth mandate.

Frequently Asked Questions

Is TDS deducted on a NRO account?

Yes. TDS is mandatory on all interest income from NRO accounts — both savings and fixed deposits — under Section 195 of the Income Tax Act. The base rate is 30%, and with surcharge and 4% cess, the effective rate starts at 31.2%. There is no minimum threshold exemption for NRIs.

How to reduce TDS on NRO account?

Three main approaches work:

- Claim DTAA benefits by submitting a TRC and Form 10F before interest is credited, reducing the withholding rate to 10–15%

- File ITR-2 in India to claim deductions and recover excess TDS as a refund

- Restructure into NRE accounts where eligible to eliminate TDS on foreign-sourced funds entirely

What documents are needed to claim DTAA benefits on an NRO account?

You need four documents: a Tax Residency Certificate (from your country of residence), Form 10F filed on the IT e-filing portal, a self-attested PAN copy, and a No PE declaration. Submit all to your bank annually before interest is credited.

Can NRIs get a refund of TDS deducted on NRO accounts?

Yes. NRIs can file ITR-2 in India and claim a refund if total Indian income falls below the basic exemption limit, or if actual tax payable is less than TDS already deducted. The refund is credited to the NRI's pre-validated Indian bank account after processing.

Is TDS applicable on NRE fixed deposits as well?

No. Interest on NRE savings accounts and NRE fixed deposits is completely exempt from Indian income tax under Section 10(4)(ii). No TDS is deducted, making NRE accounts far more tax-efficient for foreign-sourced income compared to NRO accounts.

Does the new tax regime affect TDS on NRO accounts?

Yes. From FY 2023-24, the new tax regime is the default for NRIs, capping the surcharge at 25% for income above ₹5 crore and reducing the maximum effective TDS rate from 42.744% to 39%. NRIs preferring the old regime must explicitly opt for it and notify their bank — otherwise the new regime applies automatically.