This guide covers why India is a compelling investment destination right now, which asset classes are accessible to NRIs, how to set up accounts compliantly, and how to manage the tax implications across jurisdictions. Whether you are based in the US, UAE, UK, or Singapore, the regulatory and tax landscape is navigable — with the right framework.

One important note before diving in: NRI investments span FEMA regulations, banking compliance, and multi-country tax law. This guide provides a structured overview, but specific situations benefit from professional advice.

Key Takeaways

- NRIs can invest in Indian equities, mutual funds, real estate, fixed deposits, bonds, and NPS — all accessible through NRE or NRO accounts

- India's 6.5% GDP growth (IMF, 2026) and the INR's long-term depreciation create a dual return advantage for NRI investors

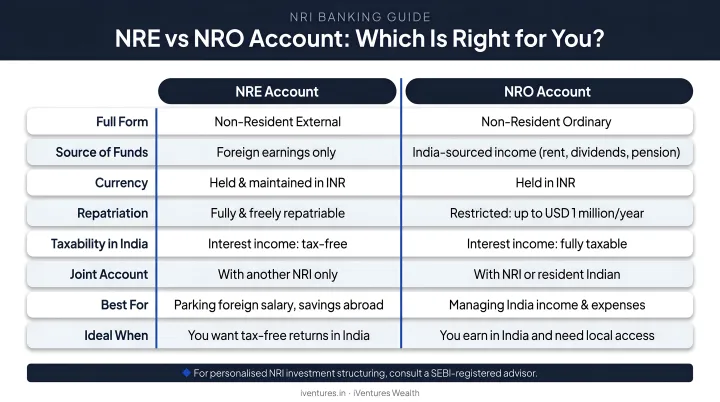

- NRE and NRO accounts serve different purposes — using a regular resident savings account after becoming an NRI is illegal under FEMA

- DTAA agreements protect NRIs from double taxation; submitting a Tax Residency Certificate reduces TDS at source

- A SEBI-registered advisor with cross-border expertise can prevent costly compliance errors and build more tax-efficient, well-structured portfolios

Why India? The Case for NRI Investment Today

According to the World Bank, India grew at 6.5% in FY2024-25 and is projected to grow at 6.3% in FY2025-26 — maintaining its position as the fastest-growing major economy globally. The IMF independently projects 6.5% real GDP growth for 2026.

For NRI investors, sustained growth at this rate creates compounding opportunities across equities, real estate, and debt instruments.

Growth figures, though, are only part of the picture. Three structural factors make India worth examining more closely right now.

The Currency Advantage

The INR has depreciated steadily against the USD over the past two decades. Federal Reserve data shows the exchange rate moved from ₹43.62 per USD in January 2005 to ₹86.27 in January 2025 — a 97.79% rise in rupees required to buy one dollar. By May 2026, the rate stood at ₹95.53.

For NRI investors, this creates a compounding entry advantage: foreign earnings converted to rupees buy more Indian assets over time. When profits are eventually repatriated, gains are amplified in foreign currency terms. This isn't a guaranteed return mechanism, but it is a consistent pattern that has persisted for over 20 years and should be modelled into any repatriation plan.

Higher Yields Than Developed Markets

Indian fixed deposits offer significantly higher yields than most developed-market equivalents. Current benchmarks make the gap clear:

| Market | Current Rate |

|---|---|

| SBI NRE FD (1–2 years) | 6.25%–6.45% (effective Mar 2026) |

| US Federal Funds Rate | 3.5%–3.75% (Apr 2026) |

| UK Bank Rate | 3.75% |

| UAE Base Rate | 3.65% |

| Japan Overnight Rate | ~0.75% |

NRE Fixed Deposit interest is tax-free in India and fully repatriable — making it one of the most straightforward high-yield instruments available to NRIs seeking safety alongside returns.

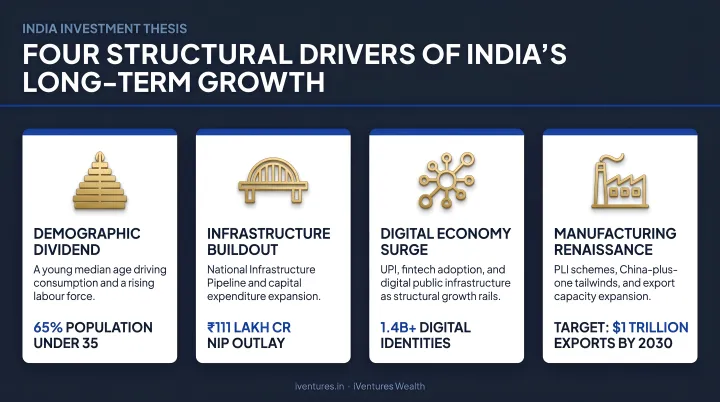

The Demographic and Growth Dividend

India's long-term investment case extends beyond current growth rates. Several structural drivers create 10–20 year tailwinds:

- Government capital expenditure of ₹11.21 lakh crore (3.1% of GDP) in FY2025-26, rising to ₹12.2 lakh crore proposed for FY2026-27

- Production Linked Incentive (PLI) schemes spanning 14 sectors with ₹1.97 lakh crore outlay, already generating over ₹20.41 lakh crore in production and sales

- Digital economy projected to reach nearly 20% of GVA by 2029-30, up from 11.74% in 2022-23

- UPI processed 23,201 million transactions worth ₹29.9 lakh crore in May 2026 alone — a proxy for the scale of India's domestic consumption engine

Each of these drivers is already measurable — not projected. NRIs entering now are buying into infrastructure, digital, and manufacturing expansion that is already underway.

Maintaining Financial Ties and Planning for the Future

Beyond returns, NRIs invest in India for practical and personal reasons: supporting family financially, building a retirement corpus for an eventual return, maintaining property, and diversifying away from single-country economic risk. These motivations are consistent across NRI segments — professionals in the US and UAE, returning expatriates, and NRI family business owners alike.

Top Investment Options for NRIs in India

NRIs have access to a broad range of regulated investment options. The right mix depends on time horizon, risk appetite, tax residency, and repatriation goals. Here is a structured overview.

Equity and Mutual Funds

NRIs can invest in Indian equities through the Portfolio Investment Scheme (PIS) via an NRE PINS account. Key rules:

- Only delivery-based trades are permitted — intraday trading and short selling are not allowed for NRIs

- Equity mutual funds can be purchased through NRE or NRO accounts via SIP or lump sum

- Equity mutual funds offer professional management and broader diversification compared to direct stock picking

US and Canada-based NRIs face additional restrictions due to FATCA compliance requirements. Several AMCs restrict investments from these jurisdictions. Always verify directly with the fund house or broker before investing.

Fixed Deposits and Debt Instruments

Two account types create meaningfully different outcomes for NRI fixed deposits:

- NRE Fixed Deposits: Interest is tax-free in India under Section 10(4)(ii), fully repatriable, no upper limit on repatriation — the most popular choice for NRIs seeking safe, higher-yield returns

- NRO Fixed Deposits: Interest is taxable, repatriation capped at USD 1 million per financial year subject to tax compliance

Beyond FDs, NRIs can also invest in government bonds and Non-Convertible Debentures (NCDs) as debt options for portfolio diversification.

Real Estate

NRIs can purchase residential and commercial property in India without RBI permission. Restrictions apply:

- Not permitted: Agricultural land, plantation property, or farmhouses

- All transactions must be in Indian Rupees routed through NRE or NRO accounts

For NRIs seeking real estate exposure without the complexity of direct ownership, REITs (Real Estate Investment Trusts) listed on Indian exchanges offer a regulated, liquid alternative. Six REITs are registered on Indian exchanges — including Embassy Office Parks, Brookfield India Real Estate Trust, and Mindspace Business Parks REIT. iVentures Wealth advises NRI clients on both direct property and REIT structures, drawing on established partnerships across developments in Gurugram, Mumbai, and Dubai.

NPS, PMS, and Long-Term Instruments

- National Pension System (NPS): Open to NRIs; contributions qualify for tax benefits under Section 80CCD(1)

- PPF: Not available to NRIs — a common and costly misconception. Existing accounts may continue until maturity on a non-repatriation basis only.

- Portfolio Management Services (PMS): Suitable for NRIs with larger investable surpluses. SEBI mandates a minimum investment of ₹50 lakh. PMS offers actively managed, customised equity portfolios — iVentures Wealth structures multi-asset PMS mandates for NRIs with cross-border complexity.

ETFs and Alternatives

NRIs can invest in index ETFs (Nifty 50, Sensex) and gold ETFs through demat accounts. Restrictions apply to currency and commodity ETFs — NRIs may not participate in the currency derivatives segment under FEMA. US and Canada-based NRIs should confirm AMC-level acceptance before investing through ETF routes, as FATCA restrictions apply here as well.

How to Get Started: Accounts, KYC & Documentation

Every NRI must complete a compliance setup before investing. Using a regular resident savings account after becoming an NRI is illegal under FEMA; the RBI requires redesignation to an NRO account as soon as your residential status changes.

Step 1: Open the Right Bank Account

| Account Type | Purpose | Tax on Interest | Repatriation |

|---|---|---|---|

| NRE | Foreign income converted to INR | Tax-free in India | Fully repatriable |

| NRO | Indian-sourced income (rent, dividends) | Taxable | Up to USD 1M/year |

Maintain both accounts — they serve different purposes. For equity investing, an NRE PINS account is also required.

Step 2: Obtain a PAN Card

A Permanent Account Number (PAN) is mandatory for all investment and financial transactions in India. NRIs apply via Form 49A — this can be completed online or through Indian consulates. PAN is required for KYC, mutual fund purchases, property transactions, and tax filing.

Step 3: Complete KYC

Key documents typically required:

- Valid passport copy

- Overseas address proof (utility bill or bank statement)

- PAN card copy

- Recent photograph

- Cancelled cheque from your NRE/NRO account

- Foreign Inward Remittance Certificate (FIRC) to verify source of funds

Many institutions now offer video or digital KYC for NRIs. KYC is a one-time process but must be updated when residential status changes.

Step 4: Open a Demat and Trading Account

With KYC complete, the next step is opening a demat account linked to your NRE or NRO bank account through a SEBI-registered broker — this is required for equities, ETFs, and IPOs. An existing resident demat account must be converted to an NRI demat account upon change of status.

Coordinating banking, brokerage, and compliance across multiple institutions is where most NRIs lose time. iVentures Wealth handles end-to-end onboarding — completing the full setup in 7–10 business days — covering KYC, account structuring, PIS setup, LRS declarations, and first investment execution.

NRI Tax Guide: DTAA, TDS & Repatriation

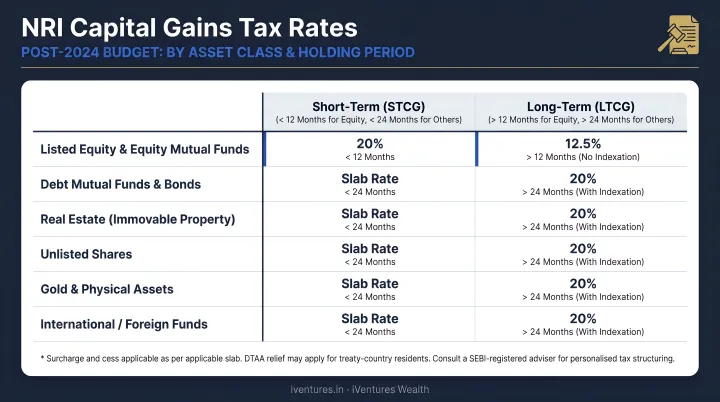

NRIs are taxed in India on income earned or accrued in India. The primary mechanism is Tax Deducted at Source (TDS), applied at the point of redemption or dividend payment. Capital gains tax rates changed materially after July 23, 2024, as summarized below:

| Asset Class | Holding Period | Tax Rate |

|---|---|---|

| Equity mutual funds (STCG) | ≤12 months | 20% |

| Equity mutual funds (LTCG above ₹1.25L) | >12 months | 12.5% (no indexation) |

| Specified debt funds (acquired post Apr 1, 2023) | Any | Deemed short-term under Section 50AA |

| Other hybrid/non-equity (listed units, LTCG) | >12 months | 12.5% |

Understanding DTAA Benefits

India has DTAA agreements with numerous countries, including the US, UK, UAE, Singapore, Australia, and Canada. To avoid double taxation:

- Obtain a Tax Residency Certificate (TRC) from your country of residence

- File Form 10F electronically with Indian tax authorities

- Submit TRC to claim reduced TDS rates or tax credits

Rates differ by treaty. The India-US treaty caps interest TDS at 15% (10% for bank loans), the UK treaty at 15%, and the UAE treaty at 5–12.5%. Always consult a tax advisor in both jurisdictions, as provisions vary considerably by treaty.

Repatriation Rules

- NRE account: Fully and freely repatriable, no upper limit

- NRO account: Capped at USD 1 million per financial year, subject to tax compliance and documentation

The choice of account from day one has lasting implications for how easily funds can be moved abroad later. Many NRIs underestimate this routing decision until repatriation becomes urgent. iVentures Wealth's cross-border advisory specifically addresses NRE/NRO structuring as part of a broader tax-efficient investment plan for NRI clients.

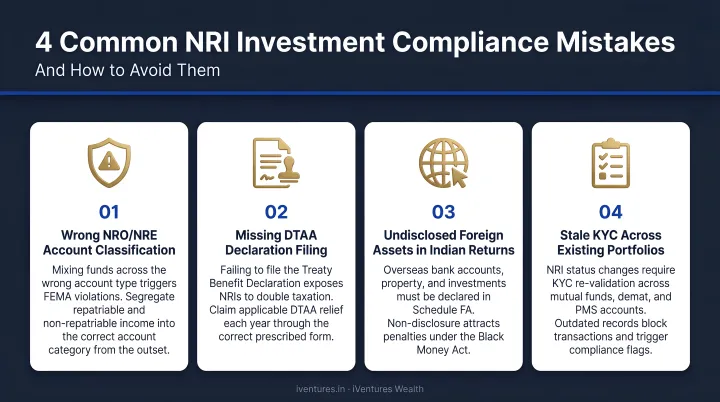

Common Mistakes NRIs Make When Investing in India

Getting the compliance foundation wrong is expensive. The most frequent mistakes:

- Continuing to hold a resident savings account after becoming an NRI — this is a FEMA violation. Under FEMA Section 13, penalties can reach three times the sum involved

- Routing investments through the wrong account type — NRE vs NRO errors create unintended tax or repatriation complications that are difficult to unwind

- Failing to submit DTAA documentation — results in excess TDS deducted at standard rates, requiring refund claims that take time to resolve

- Ignoring compliance changes when returning to India — residential status shifts trigger account redesignation requirements that many NRIs miss

Beyond individual account errors, a larger strategic mistake is treating India investments in isolation from a global financial plan. NRI investors typically hold assets across multiple jurisdictions. Without consolidated visibility across those holdings, they risk:

- Over-concentration in a single market

- Paying unnecessary taxes in two countries simultaneously

- Missing rebalancing opportunities as allocations drift

What this means practically: NRIs need an advisor who can view their full picture — not just the India slice. That includes consolidated reporting across jurisdictions, DTAA structuring coordinated with local tax professionals in the country of residence, and portfolio construction that accounts for currency exposure through structures like GIFT City. iVentures Wealth's NRI advisory practice is structured around exactly this cross-border visibility, rather than treating Indian assets in isolation.

Frequently Asked Questions

Which investment is best for NRIs in India?

There is no single answer — the right choice depends on goals, risk appetite, and time horizon. NRE fixed deposits and equity mutual funds are common starting points. Real estate and PMS suit NRIs with larger surpluses seeking deeper diversification.

Is it a good idea for NRIs to buy property in India?

NRIs can legally purchase residential and commercial property (not agricultural land). It suits those planning to return or seeking rental income, but liquidity, property management complexity, and tax on rental income should be assessed carefully before committing capital.

Why do NRIs invest in India?

Several factors drive the decision: higher returns relative to developed markets, a long-term currency advantage (INR depreciation amplifies gains in foreign currency terms), family obligations, retirement planning, and participation in India's economic growth over a 10–20 year horizon.

What is the 4-year rule for NRIs?

Under Section 6 of the Income Tax Act, an individual is non-resident if present in India for fewer than 182 days in a financial year, or fewer than 60 days in that year and fewer than 365 days across the preceding four years. This look-back period determines residential status for tax purposes. Note: for Indian citizens with income exceeding ₹15 lakh, the Finance Act 2020 reduced the 182-day threshold to 120 days.

What bank account do NRIs need to invest in India?

NRIs need an NRE account for foreign income (fully repatriable, interest tax-free) and/or an NRO account for Indian-sourced income (partially repatriable). Regular resident savings accounts cannot be held after acquiring NRI status; RBI rules require conversion.

Do NRIs pay double tax on Indian investment gains?

Not if they use DTAA protections. By submitting a Tax Residency Certificate to Indian authorities, NRIs can claim reduced TDS rates or tax credits in their country of residence — ensuring the same income is not taxed twice. The specifics depend on which treaty applies to your jurisdiction.