The core challenge: not all financial advisors in India operate under the same rules. Some are SEBI-registered fiduciaries legally required to act in your best interest. Others are commission-driven distributors whose income depends on what they sell you. Choosing the wrong one can cost far more than any advisory fee you'd pay.

This guide walks you through what a professional financial advisor actually is in India, the six criteria that matter most when selecting one, and the red flags that should end any conversation immediately.

Key Takeaways

- SEBI RIA registration is the non-negotiable first filter — verify it before anything else

- Fee-only advisors carry fewer conflicts of interest than commission-based distributors

- CFA and CFP credentials indicate expertise, but they don't substitute for regulatory verification

- Specialisation matters: an advisor serving retail investors may lack expertise for AIF allocations or family office structuring

- Always request written fee and conflict-of-interest disclosures before signing any engagement

What Is a Professional Financial Advisor in India?

In the Indian context, a professional financial advisor is a qualified expert who provides personalised guidance on investments, tax planning, estate structuring, and wealth preservation — and who operates under the appropriate regulatory framework.

The critical distinction lies in how that person is licensed:

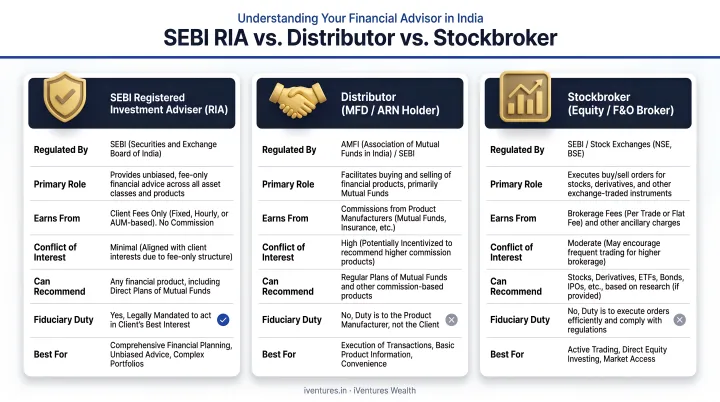

| Category | Regulatory Body | How They're Paid | Fiduciary? |

|---|---|---|---|

| SEBI Registered Investment Adviser (RIA) | SEBI (IA Regulations, 2013) | Client-paid fee | Yes |

| AMFI-Registered Mutual Fund Distributor (ARN) | AMFI | Trail commissions from AMCs | No |

| SEBI-Registered Stockbroker | SEBI / Exchanges | Brokerage | No |

Under SEBI's Investment Advisers Regulations, 2013, only SEBI-registered RIAs are legally bound to act in the client's best interest. Distributors and stockbrokers provide advice that is "incidental" to their primary function — product sales or execution. In practice, this means a distributor recommending a fund may be optimising for their trail commission — not your returns.

Once you understand who is legally obligated to work in your interest, the next question is scope. A SEBI-registered RIA can advise across:

- Portfolio construction and management across asset classes

- Retirement and succession planning

- Tax optimisation and estate structuring

- NRI investment and cross-border advisory

- Family office structuring and multi-entity consolidation

The right advisor's scope should match the complexity of your financial situation, not just your investable assets.

Key Factors to Consider When Choosing a Financial Advisor in India

Choosing an advisor isn't just about credentials. Regulatory standing, fee model, fiduciary obligation, and specialisation fit all matter equally.

SEBI Registration and Regulatory Standing

SEBI RIA registration under the Investment Advisers Regulations, 2013 is the foundational requirement. It means the advisor has met minimum qualification and capital adequacy standards — individual RIAs must maintain a net worth of at least ₹5 lakh; non-individual entities ₹50 lakh.

Registration also carries two critical obligations: the advisor must act in a fiduciary capacity and remains subject to ongoing SEBI oversight.

As of August 2024, SEBI's board memorandum reported only 927 registered Investment Advisers across India — a notably small number relative to India's investor population. That scarcity means you should screen for registration early and not assume that anyone calling themselves a "wealth manager" or "financial advisor" holds this status.

How to verify: Search the SEBI Intermediary Portal or the SEBI public Investment Adviser list using the advisor's name or registration number. Confirm the registration is active before any further evaluation.

Credentials and Professional Qualifications

For SEBI-mandated requirements, look for current NISM Series X-A (Level 1) and X-B (Level 2) certifications — these are the baseline exams for IA registration eligibility.

Beyond regulatory minimums:

- CFA (Chartered Financial Analyst) — signals rigorous investment analysis training; relevant for portfolio construction and macro analysis. Verify through the CFA Society India Member Directory

- CFP (Certified Financial Planner) — covers comprehensive financial planning; relevant for client-facing advisory roles. Verify through FPSB India's CFP Directory, which reported 3,215 CFP professionals in India as of December 2024

Treat credentials as a second screen, not the primary one. Regulatory standing comes first.

Fee Structure and Transparency

Once you've confirmed regulatory standing and credentials, fee structure is the next critical filter — because how an advisor earns money directly shapes what they recommend.

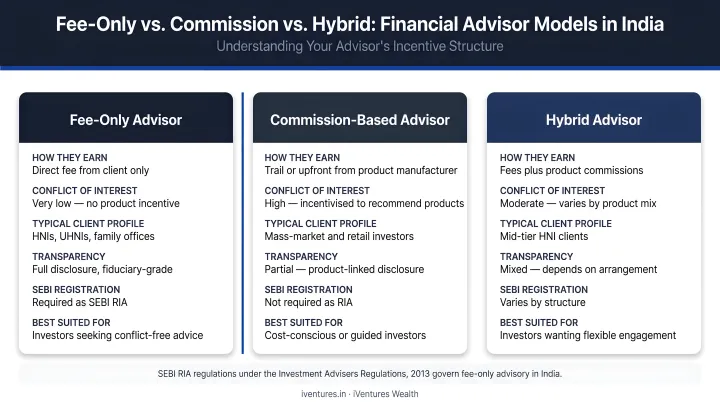

Three fee models exist in India's advisory landscape:

- Fee-only — flat retainer, hourly, or percentage of AUM; typical for SEBI RIAs

- Commission-based — distributors earn trail commissions from product manufacturers

- Hybrid — advisory fee combined with some commission income

The conflict with commission-based advisors is structural, not personal. Their income depends on which products they recommend and how much those products pay. That creates an incentive to favour high-commission products regardless of suitability.

SEBI's 2020 guidelines set fee caps for RIAs at 2.5% of AUA per annum or ₹1,25,000 fixed fee per annum per client family. Check the SEBI Master Circular for Investment Advisers (June 2025) for any updated limits before you engage.

Before signing anything, ask for written disclosure of: fee mode, rupee amount, calculation base, billing frequency, and termination terms.

Fiduciary Obligation vs. Suitability Standard

A SEBI-registered RIA operates under Regulation 15 of the IA Regulations, which requires them to act in a fiduciary capacity — meaning they must prioritise your interests, disclose conflicts as they arise, and recommend only what is genuinely suitable.

A mutual fund distributor operates under AMFI's suitability standard, which only requires that a product not be "unsuitable." That's a lower bar, and it allows for recommendations that serve the distributor's revenue even while technically meeting minimum suitability requirements.

Ask any prospective advisor directly: "Are you a SEBI-registered RIA or a distributor?" The answer determines the standard of care you'll receive.

Specialisation and Range of Services

Not every advisor is equipped for every client profile. An advisor who serves retail investors may not have the expertise to handle:

- AIF allocations (Category I, II, III)

- NRI cross-border structuring and DTAA applications

- Multi-entity portfolio consolidation for family offices

- Corporate treasury management

- Offshore estate and succession planning

Ask about the advisor's typical client profile, average AUM per client, and the specific services offered beyond basic mutual fund allocation. If your situation involves multiple entities, cross-border assets, or succession planning, verify explicitly that the advisor has handled comparable cases.

Track Record, Experience, and Long-Term Relationship Fit

An advisor who guided clients through the 2008 financial crisis, the 2020 COVID crash, and subsequent rate cycles has context that a newer advisor simply doesn't. That experience shapes how they communicate during drawdowns and whether they hold clients to a long-term framework or react to short-term noise.

Beyond track record, relationship fit matters. Communication style, responsiveness, and the advisor's willingness to explain reasoning rather than just deliver conclusions — these determine whether the relationship actually works over time.

Interview at least two or three advisors before deciding. Ask for:

- A written investment policy statement or sample framework

- Specific examples of how they've managed client portfolios through volatility

- Continuity planning details if a key team member departs

Red Flags to Watch Out For When Evaluating a Financial Advisor

SEBI has issued enforcement orders against unregistered advisors multiple times in recent years — including actions against M/s NIFM Equity and Commodity Research (February 2024) and Lifeinspire Knowledge Solutions (2024–25). These cases involved guaranteed returns, trading authority claims, and unverifiable registrations.

Each of these cases shares a pattern. Before you engage any advisor, check your own shortlist against these warning signs:

- Not on the SEBI RIA list — if you can't find them on the SEBI Intermediary Portal, don't proceed

- Guaranteed returns — no SEBI-registered advisor can legally promise fixed investment returns; treat any such claim as an immediate disqualifier

- Vague or undisclosed fees — a trustworthy advisor provides written fee disclosure without hesitation

- Commission-linked product recommendations — ask directly whether they earn any commission on what they recommend

- Operating under a bank or brokerage umbrella — bank wealth managers and brokerage platforms are primarily distribution channels; their advice is incidental to product sales, not fiduciary by design

- High-commission product push — if ULIPs, endowment plans, or regular-plan mutual funds appear without clear justification, ask why direct or lower-cost alternatives weren't considered

Review SEBI's Caution to Investors page for additional enforcement patterns before making any final decision.

How iVentures Wealth Can Help

iVentures Wealth (SEBI RIA: INA000019026) is a Gurugram-based investment advisory firm that has operated on fiduciary principles since 2005. With over ₹1,146 Cr in assets under advice, 150+ affluent families and institutional clients, and a 20+ member qualified advisory team, the firm maps directly to the selection criteria this guide covers.

Against each criterion:

- Regulatory standing — SEBI-registered RIA since 2010; registration publicly verifiable at sebi.gov.in

- Credentials — CFA Charterholder-led research team (Krishna Makhariya, Head of Research and Executive Director); founder Nirmal A. Bansal brings prior experience from DSP Merrill Lynch and holds a degree from UCLA Anderson School of Management

- Fee structure — strictly fee-only model; zero commissions from product manufacturers; all fees disclosed in writing before engagement

- Fiduciary obligation — written conflict-of-interest register provided to clients; advice sourced from the full universe of regulated products without product-shelf restrictions

- Specialisation — serves UHNIs, NRIs/OCIs, family offices, CXOs, corporate treasuries, and founders; minimum thresholds reflect service complexity (₹5 Cr for NRIs/OCIs, ₹10 Cr for CXOs and professionals, ₹50 Cr for corporates, ₹100 Cr for family offices)

Services cover the full wealth lifecycle:

- Personalised portfolio construction and asset allocation

- Family office advisory, including multi-entity consolidation and succession planning

- NRI and OCI cross-border tax and investment advisory

- Corporate treasury management

- Estate and succession planning

- AIF and PMS selection

- Real-time portfolio tracking via the proprietary Wealth Monitor App

Conclusion

Choosing a financial advisor in India follows a clear sequence: verify SEBI RIA registration first, then assess credentials, fee transparency, fiduciary obligation, and specialisation fit. Done rigorously, the process leaves you with a short list of advisors who can actually serve your complexity — not just your assets.

A quick reference before you finalize your decision:

- SEBI RIA registration — non-negotiable starting point; verify at sebi.gov.in

- Credentials — CFA, CFP, or equivalent; check the team, not just the principal

- Fee structure — flat or AUM-based, disclosed upfront, no trail commissions

- Fiduciary clarity — confirms they act in your interest, not a distributor's

- Specialisation fit — NRI, family office, succession, or corporate treasury as relevant

The relationship itself is a long-term one. Goals shift across career stages, liquidity events, and family transitions. A good advisor should be re-evaluated periodically against the same criteria you used to select them — ensuring alignment as your wealth and complexity grow.

Frequently Asked Questions

What is a professional financial advisor?

A professional financial advisor is a qualified expert who provides personalised guidance on investments, tax planning, and wealth management. In India, anyone who charges a fee specifically for investment advice must be registered with SEBI as a Registered Investment Adviser (RIA): that registration is the legal marker of a legitimate professional advisor.

Which is better, PFP or CFP?

In India, the CFP (Certified Financial Planner) designation — administered by FPSB India — is the more recognised and relevant credential for client-facing advisory roles. A general personal financial planning course does not carry the same depth or industry standing.

Is CFP better than MBA?

They serve different purposes. A CFP is a specialised, practice-oriented credential for financial planning with individual clients; an MBA covers broader business management. For advisors serving retail investors in India, CFP combined with SEBI RIA registration is more directly relevant than an MBA alone.

How do I verify if a financial advisor is SEBI registered in India?

Search the SEBI Intermediary Portal using the advisor's name or registration number. Confirm that the registration status is active and current — not expired or cancelled — before engaging.

What is the difference between a SEBI RIA and a mutual fund distributor in India?

A SEBI-registered RIA is a fiduciary who charges the client a fee and is legally required to act in the client's best interest. A mutual fund distributor earns commissions from asset management companies for selling products, meaning their recommendations may reflect which products pay the highest trail commission rather than what suits the client best.

How much does a financial advisor typically charge in India?

SEBI's 2020 guidelines set fee caps at 2.5% of assets under advice per annum or ₹1,25,000 fixed fee per annum per client family. In practice, market rates for fixed-fee engagements range from roughly ₹25,000 to ₹1.5 lakh annually depending on AUM size and service scope. Always confirm current caps against the SEBI Master Circular for Investment Advisers before finalising any fee agreement.