Despite being widely referenced, LRS is frequently misunderstood. Many investors assume it covers businesses, that family limits can be freely pooled, or that TCS is a permanent tax burden. None of these are accurate. For HNIs, UHNIs, and business owners making cross-border financial decisions, these gaps in understanding carry real compliance risk.

This article covers what LRS permits, how it works step by step, how TCS applies under current rules, what the scheme prohibits, and the most common misconceptions worth correcting.

Key Takeaways

- LRS allows all resident individuals — including minors with a guardian countersignature — to remit up to USD 250,000 per financial year

- The scheme is not available to corporates, HUFs, partnership firms, or trusts

- Permitted uses cover personal needs (education, travel, medical) and financial purposes (overseas investments, foreign accounts, property)

- TCS applies above ₹10 lakh — at rates varying by purpose — and is fully creditable when filing ITR

- Prohibited transactions include margin trading, overseas forex trading, and remittances to FATF-blacklisted jurisdictions

What Is the Liberalised Remittance Scheme (LRS)?

LRS is a Reserve Bank of India policy framework under the Foreign Exchange Management Act (FEMA), 1999. It permits resident individuals to remit foreign exchange up to a specified annual limit for any permissible current or capital account transaction — or a combination of both.

A Brief History of the Limit

LRS was introduced on February 4, 2004 with an initial ceiling of USD 25,000. The limit has been revised multiple times in response to macroeconomic conditions:

| Effective Date | LRS Limit |

|---|---|

| February 2004 | USD 25,000 |

| December 2006 | USD 50,000 |

| May 2007 | USD 100,000 |

| September 2007 | USD 200,000 |

| August 2013 | USD 75,000 (reduced) |

| June 2014 | USD 125,000 |

| May/June 2015 | USD 250,000 (current) |

The current limit of USD 250,000 per financial year (April–March) is anchored in RBI Master Direction No. 7/2015-16.

Who LRS Applies To

LRS covers all individuals resident in India as defined under FEMA — including minors, provided a natural guardian countersigns Form A2. It explicitly excludes corporates, partnership firms, HUFs, and trusts.

LRS applies strictly to persons resident in India. NRIs operate under separate RBI guidelines for outward remittances from NRO, NRE, or FCNR accounts — a different regulatory framework covered elsewhere in this guide.

What Can You Remit Under LRS?

The USD 250,000 annual limit is a combined ceiling across all LRS transactions in a financial year. There is no restriction on transaction frequency — only on the total aggregate amount remitted.

Current Account Transactions

These cover personal and lifestyle-related remittances. Authorised dealer (AD) banks can process these without prior RBI approval, provided the transaction is genuine and within limits.

Permitted uses include:

- Private travel abroad (excluding Nepal and Bhutan)

- Gifts and donations

- Emigration expenses

- Maintenance of close relatives abroad

- Business trips and conference expenses

- Overseas employment

- Medical treatment abroad

- Education abroad

Capital Account Transactions

These involve transactions that alter a resident's assets or liabilities outside India. For capital account remittances, the bank account used must have been maintained with the AD bank for a minimum of one year prior to remittance.

Permitted uses include:

- Opening and maintaining a foreign currency account with an overseas bank

- Acquiring immovable property abroad

- Investing in overseas equity shares, debt instruments, mutual funds, and venture capital funds

- Extending rupee loans to NRI or PIO close relatives

- Setting up a Wholly Owned Subsidiary (WOS) or Joint Venture (JV) abroad for a bonafide business purpose — subject to the Overseas Investment Rules and Regulations 2022

For HNIs and UHNIs, LRS is a FEMA-compliant route to access global asset classes — from US-listed ETFs and international bonds to multi-strategy hedge funds. Matching the right instruments to your risk profile and goals is where independent advisory adds real value. iVentures Wealth advises clients on structuring overseas investments under LRS within a regulated, research-backed framework.

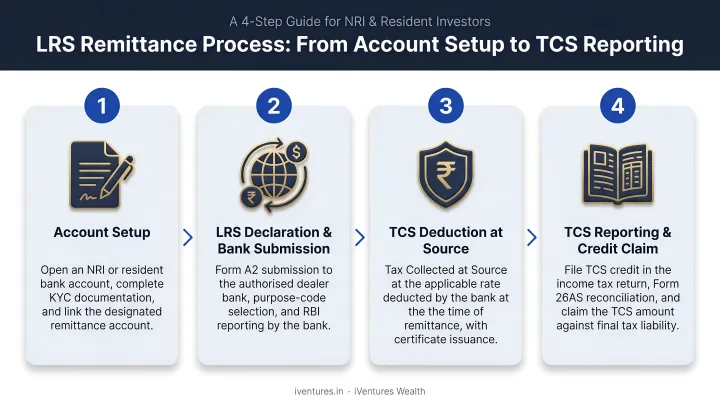

How LRS Works: The Step-by-Step Process

LRS remittances flow from a resident individual's Indian bank account through an RBI-authorised dealer (AD), typically a scheduled commercial bank. The AD verifies eligibility, processes the foreign exchange, deducts TCS, and reports the transaction to RBI.

Before initiating a remittance, keep these documents ready:

- Valid PAN card

- Completed Form A2 (declaration of purpose)

- Bank account maintained for at least one year (for capital account transactions)

- Details of the overseas account or beneficiary

Step 1: Designate an Authorised Dealer and Verify Account Standing

The remitter must designate a specific AD bank branch for capital account remittances. For capital account transactions, the account must have been maintained with that bank for at least one year. For current account transactions (including those processed through FFMCs), this one-year requirement does not apply.

Step 2: Submit Form A2 and Provide PAN

The remitter submits Form A2 declaring the purpose of remittance and confirming the funds are theirs and will not be used for prohibited purposes. PAN is mandatory — without a valid PAN, the remittance cannot be processed. The AD bank relies on this declaration but retains responsibility to verify its genuineness.

Step 3: AD Bank Verifies Cumulative Limit and Processes Remittance

The AD bank checks whether cumulative remittances in the current financial year (across all sources) remain within USD 250,000. Once confirmed, it debits the INR equivalent and initiates the transfer to the designated overseas account or beneficiary. Remittances can be made in any freely convertible foreign currency — not just USD.

Step 4: TCS Deduction and Reporting

The AD bank deducts TCS as applicable at the time of remittance and reports the transaction to RBI. The remitter can track LRS usage through bank statements and reconcile TCS credits via Form 26AS when filing ITR. Understanding where these funds can actually go — and what's off-limits — is the next critical piece of the LRS puzzle.

Tax Implications: TCS on LRS Remittances

TCS under Section 206C(1G) of the Income Tax Act applies to outward remittances under LRS. The current TCS-free threshold is ₹10 lakh per individual per financial year across all LRS modes of payment (the Budget 2025-26 increased this threshold from ₹7 lakh to ₹10 lakh).

Current TCS Rates by Category

| Purpose | Threshold | TCS Rate |

|---|---|---|

| Education via loan from a specified financial institution | ₹10 lakh | Nil |

| Education or medical treatment (self-funded) | Above ₹10 lakh | 5% (FY 2025-26) |

| Overseas tour packages | Up to ₹10 lakh | 5% |

| Overseas tour packages | Above ₹10 lakh | 20% |

| All other LRS purposes | Above ₹10 lakh | 20% |

Note on Budget 2026: The Income Tax Act, 2025 comes into effect from April 1, 2026. Per the PIB Budget 2026 update, TCS for LRS remittances for education or medical purposes (above ₹10 lakh) will be 2% under the new Act.

TCS Is Not a Final Tax

TCS is credited against your total income tax liability when filing an ITR. If TCS paid exceeds total tax owed, the excess is refundable. Credits are reflected in Form 26AS.

One structural nuance matters for business owners remitting under LRS: For sole proprietors, there is no legal distinction between the individual and their proprietary business. Any LRS remittance from a business current account counts toward the individual's USD 250,000 annual limit. Track all remittances at the PAN level.

What LRS Does Not Allow: Prohibited Transactions and Limitations

Prohibited Transactions

The following are not permitted under LRS:

- Purchase of lottery tickets, proscribed magazines, or sweepstakes

- Remittances for margin calls or margin trading on overseas exchanges

- Purchase of FCCBs (Foreign Currency Convertible Bonds) issued by Indian companies in the overseas secondary market

- Trading in foreign exchange abroad (speculative forex trading, not routine currency conversion)

- Capital account remittances — directly or indirectly — to countries identified by FATF as non-cooperative or high-risk

- Remittances to individuals or entities flagged by RBI as terrorism risks

Structural Limitations

- AD banks cannot extend credit facilities (fund or non-fund based) to resident individuals for capital account remittances under LRS

- Banks cannot open foreign currency accounts in India for residents under LRS — the overseas account must actually be abroad

- Offshore Banking Units (OBUs) in India are not treated as overseas banks for LRS foreign currency account purposes

Exceeding the Limit

Once a resident individual has remitted the full USD 250,000 in a financial year, no further LRS remittances are permitted — even if investment proceeds were repatriated during the same year.

Amounts above the limit require prior RBI approval. Exceptions exist for:

- Emigration — with documentation from the overseas authority

- Medical treatment abroad — with documentation from the treating hospital

- Education abroad — with documentation from the institution

In these cases, remittances beyond the annual cap may be permitted with the relevant supporting documents.

Common Misconceptions About LRS

"My company or HUF can use LRS for overseas purposes"

False. LRS is exclusively for resident individuals. Entities excluded from LRS include:

- Corporates and private limited companies

- Hindu Undivided Families (HUFs)

- LLPs and partnership firms

- Trusts and societies

If a company sponsors an employee's overseas expenses for genuine business purposes, those transactions may be handled at the AD bank level as residual current account transactions — without any individual LRS cap — but that falls entirely outside the LRS framework.

"Family members can pool their LRS limits for investments"

Family remittances can be consolidated where each member complies independently — purchasing overseas property as co-owners is a common example. That much is accurate.

For capital account transactions, however — opening a foreign bank account or making portfolio investments — limits cannot be clubbed with family members who are not co-owners or co-partners of that specific overseas investment.

"Income earned on LRS investments doesn't need to come back to India"

Retaining and reinvesting income earned from overseas portfolio investments under LRS is permitted. The misconception lies in what happens when that income is not reinvested.

Foreign exchange that has been received or realised and is not reinvested must be repatriated and surrendered to an authorised person within 180 days of receipt or return to India. Repatriated proceeds do not reset the same-year USD 250,000 LRS capacity.

Conclusion

LRS is a well-defined, FEMA-compliant framework that gives resident Indians structured access to overseas education, healthcare, travel, and global financial markets — up to USD 250,000 per financial year — with clear rules on eligible purposes, documentation, TCS, and what is prohibited.

For UHNIs and investors looking to put this framework to work — whether for international portfolio diversification or cross-border wealth structuring — working with a SEBI-registered advisor like iVentures Wealth helps ensure full compliance, accurate TCS tracking and credit claims, and alignment with long-term financial objectives.

Frequently Asked Questions

What is the maximum amount allowed under the LRS scheme of RBI?

The current LRS limit is USD 250,000 per resident individual per financial year (April–March), applicable as a cumulative ceiling across all outward remittances made during that year. Exceeding this limit requires prior RBI approval; exceptions apply for emigration or medical treatment, provided supporting documentation is submitted.

Who is eligible for the LRS scheme of RBI?

LRS is available to all individuals resident in India as defined under FEMA — including minors, provided a natural guardian countersigns Form A2. It is not available to corporates, HUFs, partnership firms, trusts, or LLPs.

What are the benefits of the LRS scheme of RBI?

LRS provides a legal, RBI-governed route to remit money abroad for education, medical treatment, travel, maintenance of relatives, and overseas investments. It also enables portfolio diversification through foreign stocks, ETFs, mutual funds, and property — all within a compliant FEMA framework.

Can NRIs use the Liberalised Remittance Scheme?

No. LRS applies only to individuals resident in India under FEMA. NRIs have separate remittance provisions — for example, they can remit up to USD 1,000,000 per financial year from their NRO account, subject to applicable conditions and documentation.

What documents are required to make a remittance under LRS?

PAN is mandatory for all LRS transactions, along with Form A2 declaring the purpose. For capital account transactions, the bank account must have been held for at least one year; the AD bank may also request statements or the latest ITR to verify the source of funds.

Is TCS on LRS refundable?

Yes. TCS deducted on LRS remittances is credited against the individual's total income tax liability and can be claimed as a refund when filing the ITR if total TCS paid exceeds tax owed. The TCS credit is reflected in Form 26AS and can be tracked at the PAN level.