Disclosure: iVentures Wealth is a SEBI-registered Investment Adviser. SEBI RIA Registration No.: INA000019026.

Investing in India is not just about chasing returns. It is about keeping Indian wealth productive, supporting family goals, preparing for a possible return, managing inherited assets, or ensuring savings in India do not remain scattered across bank accounts, FDs, and old investments.

Your NRE/NRO account structure, tax residency, country of residence, KYC status, repatriation needs, and existing global portfolio can all affect how the investment should be made. SEBI’s investor education material also states that NRIs with NRE/NRO accounts can invest in Indian mutual funds, subject to applicable rules.

Key Takeaways

The short answer: Yes, NRIs can invest in Indian mutual funds through an NRE or NRO account after completing PAN, KYC, and applicable declarations.

The decision that matters more than eligibility: The bigger question is not “Can I invest?” It is “Which route should I use?” NRE and NRO accounts differ in source of funds, taxation, and repatriation treatment.

Who needs extra caution: US/Canada-based NRIs, NRIs with Indian income, frequent India visitors, returning NRIs, and investors with larger India-linked portfolios should review tax, reporting, and repatriation rules carefully.

What this means: For simple cases, investing may be manageable through an AMC, bank, or platform. For affluent NRIs, mutual funds should be reviewed as part of a wider India-linked and global wealth plan.

Can NRIs Invest in Mutual Funds in India?

SEBI’s investor education material states that an NRI with an NRE/NRO bank account can invest in Indian mutual funds after completing the KYC process. But the word “can” is only the starting point. The investment may be made on a repatriable or non-repatriable basis, depending on the account used, source of funds, and applicable rules. That is why two NRIs investing in the same mutual fund scheme may still need different routes.

Eligibility for NRIs, OCIs, and PIOs

NRIs can generally invest in Indian mutual funds, subject to FEMA rules, KYC requirements, and the policies of the fund house. OCI and eligible PIO investors are also commonly allowed to invest under the NRI investment framework, but documentation and country-specific restrictions may apply.

Most NRIs need three things before they can invest:

- a PAN card

- completed KYC

- an NRE or NRO bank account

Some fund houses may also require FATCA/CRS declarations, overseas address proof, passport details, and additional documents based on the investor’s country of residence.

Repatriable vs Non-Repatriable Investment

Mutual fund investing is not just about choosing a scheme. It is also about deciding whether the money should remain freely transferable abroad or stay linked to India.

In simple terms:

| Investment route | Usually linked to | What it means |

|---|---|---|

| Repatriable basis | NRE account | The investment is generally made from foreign income remitted to India, and redemption proceeds may be sent abroad subject to applicable rules. |

| Non-repatriable basis | NRO account | The investment is generally made from India-sourced income, and repatriation may be subject to limits, documentation, and tax compliance. |

RBI’s NRI account guidance notes that NRO balances are generally repatriable up to USD 1 million per financial year, subject to conditions. This makes the account choice important from the beginning, especially for NRIs who may later want to move funds outside India.

Not sure if your NRE/NRO route is set up correctly?

Before adding new mutual fund investments, review whether your account type, KYC status, repatriation need, and tax position are aligned. Review your NRI investment structure

Why the Answer Is Not as Simple as “Yes”

Mutual fund investing becomes complicated because the same product can behave differently depending on the investor’s location, account type, tax residency, and future money movement.

A Dubai-based NRI investing foreign income through an NRE account may mainly care about repatriation and India allocation. A US-based NRI may need to think about FATCA, AMC restrictions, and overseas tax reporting before investing. An NRI with rental income in India may need to use an NRO account, where repatriation and documentation work differently.

So before choosing funds, NRIs should answer five questions:

| Question | Why it matters |

|---|---|

| Where is the money coming from? | Decides whether NRE or NRO may be more suitable. |

| Will the money need to move abroad later? | Affects repatriation planning. |

| Where are you a tax resident? | Determines whether gains may also need reporting outside India. |

| Are you based in the US or Canada? | May affect fund house access and documentation. |

| Does this fit your global portfolio? | Prevents overexposure to one country, currency, or asset class. |

Advisor note: Many NRI investment issues do not start with poor fund selection. They start with weak structuring: the wrong account, outdated residential status, unclear repatriation plan, or tax assumptions that were never checked.

That is why the better question is not just whether NRIs can invest in mutual funds. It is whether the investment route is clean, compliant, tax-aware, and aligned with the investor’s wider India-linked wealth plan.

Who Qualifies as an NRI for Mutual Fund Investments?

For mutual fund investing, NRI status matters in two ways: FEMA decides the investment route, while the Income Tax Act decides tax treatment.

Under FEMA, NRI status affects how money is routed, which bank account can be used, whether the investment is repatriable, and what documents the AMC or platform may ask for.

Tax residency is checked separately under the Income Tax Act. It depends on the investor’s stay in India during the relevant financial year and can affect taxation, reporting, and treatment of Indian income or capital gains.

For NRIs who visit India often, earn rental income, manage family assets, or plan to return permanently, tax residency should be reviewed before making large investments or redemptions.

How NRIs Can Start Investing in Indian Mutual Funds

Once eligibility is clear, the process is mainly about getting the route and documents right.

- Use an NRE or NRO account. NRIs generally need an NRE or NRO bank account to invest in Indian mutual funds. SEBI’s investor education material states that NRIs with an NRE/NRO bank account can invest after completing KYC.

- Complete PAN and KYC. Common requirements include PAN, passport copy, overseas address proof, NRE/NRO bank proof, photograph, FATCA/CRS declaration, and OCI/PIO document if applicable. Requirements can vary by AMC, KRA, platform, and country of residence.

- Choose direct investment or PoA. NRIs can invest directly through an AMC, platform, or intermediary. Some also appoint a Power of Attorney holder in India, but the PoA, signatures, KYC, and bank details must match AMC requirements.

- Update old investments after moving abroad. If you started SIPs or mutual fund investments as a resident Indian, update your residential status, bank details, and FATCA/CRS declarations before continuing or redeeming.

NRE vs NRO Account: Which One Should NRIs Use for Mutual Funds?

The NRE vs NRO choice should come before fund selection because it decides how money enters India, how easily it can move back abroad, and how the investment is reported.

| Factor | NRE Account | NRO Account |

|---|---|---|

| Main use | Foreign income remitted to India | Income earned in India |

| Common examples | Salary abroad, overseas savings | Rent, dividends, pension, interest |

| Repatriation | Generally freely repatriable | Generally allowed up to USD 1 million per financial year, subject to conditions |

| Interest taxation in India | Generally tax-free | Taxable in India |

| Mutual fund route | Usually used for repatriable investments | Usually used for non-repatriable or India-income-linked investments |

A simple way to think about it is this: NRE is usually for bringing foreign income into India. NRO is usually for managing income already earned in India.

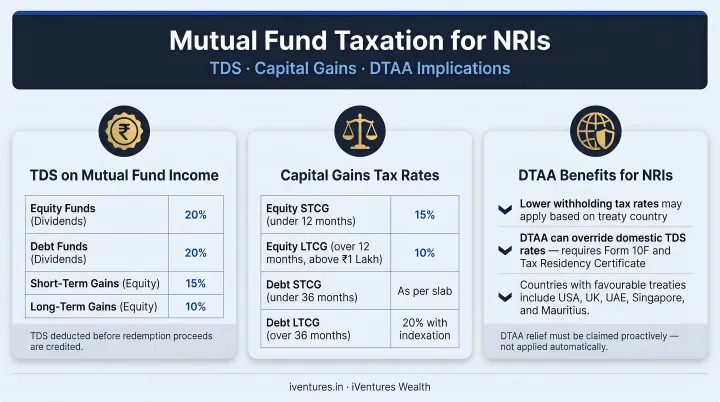

How Are Mutual Funds Taxed for NRIs?

The main tax surprise is not always the rate. It is the timing. In many cases, tax is deducted before the redemption money reaches your account.

TDS on Redemptions

When an NRI redeems mutual fund units, the AMC usually deducts tax at source before crediting the proceeds. So if you redeem ₹10 lakh, the amount that reaches your account may already be reduced by TDS.

That does not always mean your final tax liability is exactly equal to the TDS deducted. Depending on your total income, fund type, holding period, treaty eligibility, and country of residence, you may still need to file returns, claim credit, or adjust the final tax position.

What this means: If you are redeeming money for repatriation, a property purchase, family support, or reinvestment, plan using the amount you may receive after TDS, not the gross redemption value.

Capital Gains Depend on the Fund Type

Mutual fund taxation depends on what kind of fund you hold and how long you hold it. For equity-oriented mutual funds, AMFI notes that short-term capital gains on transfers made on or after July 23, 2024 are taxed at 20%, while long-term gains above ₹1.25 lakh are taxed at 12.5%, subject to applicable conditions under the mutual fund tax regime.

Debt funds, hybrid funds, and other non-equity schemes may be treated differently. The tax outcome can change based on the fund’s asset mix, purchase date, and holding period.

DTAA Can Help, But It Needs Documentation

India has tax treaties with many countries to reduce double taxation. But treaty relief is not automatic just because you are an NRI. You may need documents such as a Tax Residency Certificate, and the final treatment will depend on the treaty between India and your country of residence.

For example, an NRI living in the UAE, Singapore, the UK, or the US may face different reporting and credit rules after the same Indian mutual fund redemption.

What this means: Do not evaluate mutual funds only by headline returns. The more useful number is what remains after Indian tax, TDS, foreign tax treatment, and currency movement.

Planning a large redemption or new allocation?

For NRIs, tax, TDS, repatriation, and resident-country reporting can change the real outcome. Speak to iVentures Wealth before you make the next move.

What US and Canada-Based NRIs Should Know Before Investing

US and Canada-based NRIs can face more restrictions than NRIs in many other countries. This does not always mean they cannot invest, but the process is usually less straightforward.

FATCA and Additional Documentation

For US tax residents, FATCA adds an extra reporting layer. The IRS says certain US taxpayers holding specified foreign financial assets must report them through Form 8938, depending on applicable thresholds.

In practice, this is why AMCs and platforms may ask US/Canada-based NRIs for extra declarations before accepting mutual fund transactions. MF Utility also notes that USA/Canada residents may need to upload the required USA/Canada declaration within the specified timeline, and that mutual funds may accept or reject the transaction based on the evidence provided.

AMC Access Can Change

Not every AMC treats US and Canada-based NRIs the same way. Some may allow transactions online, some may require offline documentation, and some may restrict fresh investments.

Avoid relying on old online lists of “AMCs that accept US/Canada NRIs.” These lists can go out of date quickly. Always verify directly with the fund house, platform, or advisor before investing.

PFIC Risk for US Tax Residents

For US tax residents, Indian mutual funds may also create PFIC-related reporting complexity. The IRS requires shareholders of a Passive Foreign Investment Company to generally file Form 8621 in relevant cases.

This is not a small paperwork issue. It can affect annual reporting, tax treatment, and whether Indian mutual funds are efficient for the investor after US tax rules are considered.

How Indian Mutual Funds Fit Into an NRI’s Global Portfolio

Once the account, KYC, and tax basics are clear, the bigger question is this: how much India exposure should your overall portfolio have?

For many affluent NRIs, Indian mutual funds are only one part of a larger picture. You may already have overseas equities, retirement accounts, Indian property, FDs, ESOPs, business interests, or family assets in India. Looking at mutual funds separately can make the portfolio look more diversified than it really is.

India Allocation Should Not Be Viewed in Isolation

A mutual fund portfolio may look balanced on its own. But if you already own Indian real estate, have family business exposure, or expect to inherit assets in India, your actual India exposure may be much higher than your fund statement shows.

The reverse can also be true. If most of your wealth is outside India, Indian mutual funds may help create a planned India allocation for future goals such as retirement in India, children’s expenses, parental support, or long-term rupee needs.

Currency and Repatriation Matter

Returns should be viewed in the currency in which you will eventually use the money. A good return in rupees may look different after currency movement if the money has to be used in dollars, dirhams, pounds, or Singapore dollars.

Repatriation also matters. If the money may need to move abroad later, the account route and documentation should be clean from the beginning. If the money is meant for India-based goals, the portfolio can be built differently.

Reporting and Succession Should Not Be an Afterthought

As wealth grows, the challenge is not only investment selection. It is visibility. Many NRI families have mutual funds, FDs, property, insurance, and bank accounts spread across family members and institutions.

That creates two risks: the investor may not have a clear view of total exposure, and the family may struggle later if nominee details, records, or succession plans are incomplete.

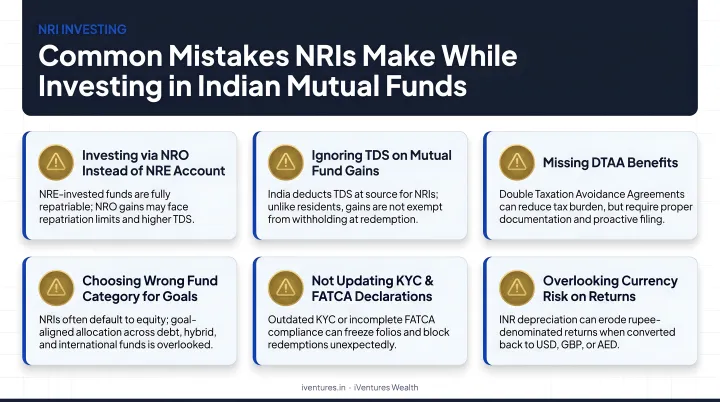

Common Mistakes NRIs Make While Investing in Mutual Funds

Most NRI mutual fund mistakes are not dramatic. They are small setup errors that become painful later, usually at the time of redemption, repatriation, tax filing, or family transfer.

| Mistake | Why it creates a problem |

|---|---|

| Using the wrong account | The source of funds and repatriation route may not match. |

| Not updating residential status | Existing SIPs or folios may continue with outdated investor details. |

| Assuming DTAA applies automatically | Treaty relief usually needs documentation and may depend on the country of residence. |

| Ignoring US tax rules | US residents may face FATCA and PFIC-related reporting issues. |

| Looking only at fund returns | Post-tax, post-currency returns matter more for NRIs. |

| Investing without a repatriation plan | Moving money abroad later may need documentation and limits may apply. |

| Not reviewing nominees and records | Family members may struggle to trace or claim investments later. |

How iVentures Wealth Helps NRIs Structure Mutual Fund Investments

iVentures Wealth can add value as a SEBI-registered investment adviser. The role is not just to help NRIs invest in mutual funds, but to review whether those funds are being used in the right structure.

For an NRI investor, that may include:

- reviewing existing Indian mutual fund exposure across AMCs and family members

- checking whether investments are linked to the right NRE or NRO route

- evaluating India allocation against the investor’s global portfolio

- assessing liquidity and repatriation needs before fund selection

- coordinating investment decisions with tax and reporting considerations

- helping avoid overdependence on scattered FDs, old SIPs, property income, or unreviewed folios

- creating a clearer view of family-level India-linked wealth

For example, an NRI with Indian property, old SIPs, NRO income, and overseas investments may not need “more funds” immediately. They may first need a consolidated review of what they already own, what is taxable, what is repatriable, and what role each investment plays.

That is the difference between buying mutual funds and building a structured NRI portfolio. The first is execution. The second is wealth management.

Move from scattered folios to a structured NRI portfolio view. Book an NRI portfolio review.

Frequently Asked Questions

Can NRIs invest in mutual funds in India?

Yes. NRIs can invest in Indian mutual funds after completing KYC and using an NRE or NRO bank account. SEBI’s investor education material confirms that NRIs with NRE/NRO accounts can invest in mutual funds, subject to applicable rules and documentation.

Can NRIs invest in SIPs?

Yes. NRIs can usually start SIPs or continue existing SIPs after updating their residential status, bank details, KYC records, and FATCA/CRS declarations where required. If the SIP was started while the investor was resident in India, the AMC or platform should be informed after the investor becomes an NRI.

Should NRIs use an NRE or NRO account for mutual funds?

It depends on the source of funds and repatriation need. An NRE account is generally used for foreign income remitted to India, while an NRO account is generally used for income earned in India, such as rent, dividends, pension, or interest. The account choice should be made before investing because it can affect repatriation and tax paperwork later.

Are mutual fund gains taxable for NRIs?

Yes. Mutual fund gains are taxable for NRIs based on the type of fund, holding period, and applicable tax rules. TDS is usually deducted at redemption. For equity-oriented funds, AMFI notes that short-term gains on transfers made on or after July 23, 2024 are taxed at 20%, while long-term gains above ₹1.25 lakh are taxed at 12.5%, subject to applicable conditions under the mutual fund tax regime.

Can US-based NRIs invest in Indian mutual funds?

Some US-based NRIs may be able to invest, but they should be more cautious. Fund house access, FATCA documentation, and US tax reporting can make the process more complex. US tax residents should also review whether Indian mutual funds create PFIC-related reporting obligations under Form 8621.

Disclaimer

This article is for educational purposes only and should not be treated as personalized investment, tax, legal, or financial advice. Investment decisions should be made after considering your risk profile, goals, liquidity needs, tax position, country of residence, and applicable regulations. Please consult a qualified investment adviser, tax professional, or legal expert before acting.