Yet most couples treat financial planning as little more than splitting bills. It's actually something more demanding: aligning two different money histories, two risk tolerances, and two visions of the future into one coherent plan.

This article covers the strategies that matter most — from your first honest financial conversation through to investing, retirement planning, and estate documents that protect what you've built together.

Key Takeaways

- Schedule regular money conversations to align on priorities before gaps in expectations become financial friction

- Set shared goals across three time horizons — short, medium, and long-term — with specific ₹ targets attached to each

- Structure cash flow allocation deliberately: needs, lifestyle spending, and wealth-building contributions each deserve a defined share

- Manage investments as a unified household portfolio to eliminate duplication, plug coverage gaps, and optimize tax efficiency

- Review nominations, insurance coverage, and estate documents after every major life event — marriage, child, property, or inheritance

Why Financial Planning Matters for Couples

Two incomes, shared expenses, and coordinated investments create real mathematical advantages over planning in silos. A 2023 Journal of Consumer Research study found newlywed couples assigned to joint bank accounts sustained higher relationship quality — driven largely by better financial goal alignment and stronger communal norms around money.

That alignment, however, doesn't happen automatically. Small disagreements about spending priorities can harden into entrenched patterns over time. Hidden debts or undisclosed spending — financial infidelity — can erode trust in even stable relationships.

Three outcomes make joint planning worth the effort:

- Accelerated wealth creation — coordinating savings rates, tax planning, and investments across two incomes builds wealth faster than two individuals acting independently

- Reduced financial stress — shared visibility into accounts and goals reduces the anxiety that fuels money arguments

- Protection against surprises — when both partners understand the household's full financial picture, there is little room for costly surprises

Start With an Open Financial Conversation

The first serious money conversation is the hardest. Many couples have been together for years without knowing each other's exact income, outstanding debts, or savings rate. That's not unusual — but it needs to change before any plan can be built. Approach it as a joint audit, not a performance review.

What to Cover in Your First Financial Discussion

Work through these questions together:

- What is each partner's monthly take-home income?

- What are current assets — savings accounts, investments, EPF balance, property?

- What are outstanding liabilities — home loan, personal loans, credit card balances, with interest rates?

- What are fixed monthly expenses for each partner?

- What is each partner's current savings rate?

- What financial fears does each person carry? What goals feel most urgent?

The goal is a complete, honest picture — no judgement, no score-keeping.

Uncovering Your Financial Personalities

Couples with opposite money mindsets — one spender, one saver; one risk-taker, one conservative — don't need to become identical. They need to understand the difference before building a plan, because conflict usually comes not from bad intentions but from mismatched defaults.

In practice, partners often carry different risk tolerances shaped by upbringing, career stability, and prior financial experiences. What matters is that both complete a risk assessment individually, then work toward a blended household investment approach that reflects both comfort levels.

Scheduling Regular Financial Check-ins

Money conversations shouldn't happen only when something goes wrong. Set a recurring schedule:

- Monthly: Review cash flow, track spending against budget, flag any changes in income or fixed expenses

- Quarterly: Measure progress against savings goals, review investment performance, discuss upcoming large financial decisions

Both partners should come prepared with updated account balances and any changes worth discussing. Treating these as normal calendar events — not emergency summits — removes most of the emotional charge.

Build a Shared Financial Plan: Goals, Budget, and Accounts

Conversations without documentation stay aspirational. A usable plan has numbers, deadlines, and named accounts attached to each goal.

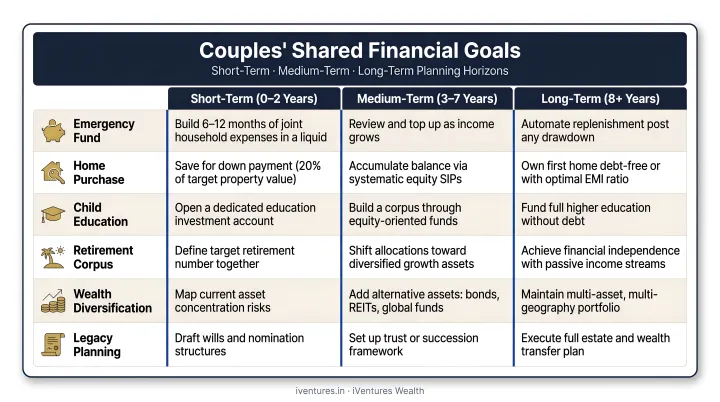

Setting Shared Financial Goals

Categorise goals by time horizon and assign a target amount to each:

| Time Horizon | Examples | Target Timeline |

|---|---|---|

| Short-term | Emergency fund, debt payoff, vacation fund | 1–3 years |

| Medium-term | Home purchase, children's education corpus | 3–7 years |

| Long-term | Retirement corpus, generational wealth | 10+ years |

Vague intentions — "we want to retire comfortably" — don't translate into action. A specific target like "₹8 Cr retirement corpus by age 60" does.

Choosing the Right Account Structure

Three models work for couples, each with genuine tradeoffs:

- Fully joint accounts — maximum transparency, but limited personal financial autonomy

- Fully separate accounts — each partner retains independence, but shared goals can drift without active coordination

- Hybrid structure — joint account for household expenses and shared savings goals; separate accounts for individual discretionary spending

The hybrid approach tends to work well for couples who want both transparency and personal financial space. For Indian couples, a few specifics deserve attention:

- Review joint account ownership rules, nomination requirements, and equal access implications

- Revisit the account structure after marriage or any major life event — default settings rarely reflect actual intentions

Creating a Joint Budget

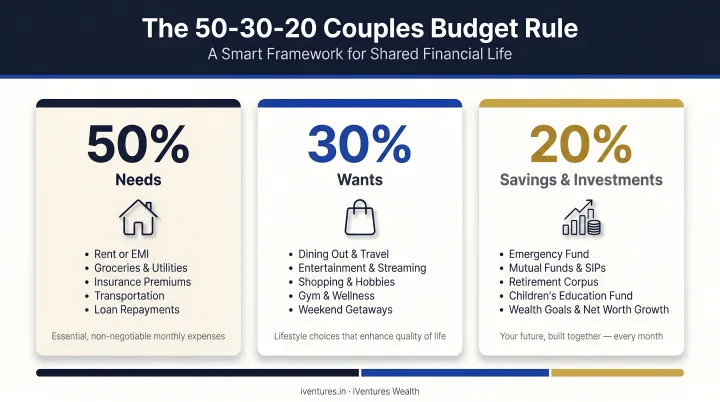

The 50/30/20 rule — commonly attributed to Elizabeth Warren and Amelia Tyagi — gives most couples a workable starting framework:

- 50% of combined take-home income to fixed needs: rent or EMI, utilities, groceries, insurance premiums

- 30% to discretionary wants: dining out, entertainment, travel

- 20% to savings and investments

Couples at different income levels or life stages may need to adjust these ratios. A household aggressively paying down a home loan might shift to 55/15/30. What matters is that the ratios are chosen deliberately, not inherited by default — an arbitrary split tends to underfund savings quietly over time.

Zero-based budgeting is an alternative for couples who prefer assigning every rupee a specific purpose. Several budgeting apps now let both partners track spending as it happens, which tends to surface misalignments early — before they become disputes.

Building an Emergency Fund

A budget without a safety net is fragile — before investing aggressively, build a buffer. Experts recommend 3–6 months of essential household expenses in a liquid, accessible account — a high-yield savings account or liquid mutual fund works well. This is especially important when one partner has variable income, is self-employed, or is mid-career transition.

Business Standard reported that 75% of Indians lacked adequate emergency funds and could default on EMIs after a sudden job loss. An emergency fund isn't optional — it's what keeps a single adverse event from becoming a financial crisis.

Investing and Retirement Planning as a Team

Investment decisions are where couples face the sharpest friction — different risk tolerances, different ideas about when to retire, different views on how much is "enough." Working through these disagreements before building a portfolio prevents them from surfacing at the worst possible moment.

Coordinating Investment Portfolios

View both partners' individual investments as a single household portfolio. This changes how you allocate.

If one partner holds aggressive equity positions — say, a growth-oriented equity SIP portfolio — the other's allocation might reasonably compensate with more stable fixed-income instruments. The goal is an overall household risk profile you're both comfortable with, not two separate portfolios optimised in isolation.

This is where a SEBI-registered advisor — such as iVentures Wealth's CFA-led team — can help, profiling each partner individually and building a single coordinated strategy that reflects both comfort levels.

Planning Retirement Together

Retirement is where misalignment becomes expensive. Fidelity's 2024 research found 53% of couples disagreed on the exact savings amount needed for retirement, and a separate Ameriprise study found 1 in 4 couples hadn't agreed on how much to save.

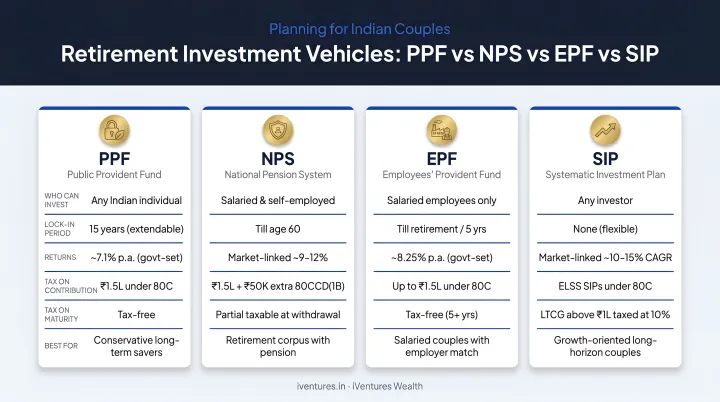

For Indian couples, retirement planning typically spans several vehicles — and coordinating them matters:

- PPF — joint accounts are not permitted under the PPF Scheme 2019, so both partners should maintain individual accounts

- NPS — individual accounts with separate tier structures; nomination alignment is important

- EPF — typically employer-linked; ensure nominee details are current

- Equity SIPs — the primary long-term growth engine for most households; allocation should reflect combined risk tolerance

One often-underestimated factor: healthcare costs. Aon's 2025 report projects India's employee medical plan costs to rise 11.5% in 2026, continuing a sustained upward trend. A retirement corpus that looks sufficient at 60 may fall short at 75 if healthcare costs aren't factored in explicitly.

Managing Debt as a Couple

Existing debt also shapes how much each partner can realistically contribute to retirement vehicles — which makes full transparency non-negotiable before merging financial plans. Both partners should disclose every outstanding liability — home loans, personal loans, credit card balances — with interest rates and minimum payments listed.

From there, two repayment strategies work depending on temperament:

- Debt snowball — pay off smallest balances first; the quick wins build momentum

- Debt avalanche — target highest-interest debt first; minimises total interest paid over time

Choose whichever approach your household will actually follow through on — that consistency matters more than mathematical optimisation.

Protecting Your Future: Insurance and Estate Planning

Protection planning is the most commonly skipped part of couples' financial planning — and the most consequential to skip.

Review these together:

- Health insurance — evaluate whether combining under one employer's plan is cost-effective versus maintaining separate covers

- Term life insurance — critical when both partners have income dependents, shared EMIs, or young children; India's life insurance protection gap stands at 87% according to the National Insurance Academy

- Disability insurance — covers income loss if one partner cannot work; routinely overlooked, yet even a short gap in earnings can derail shared financial plans

Insurance coverage addresses the risk of income loss — but it doesn't protect how your assets are distributed. That requires a separate, deliberate step.

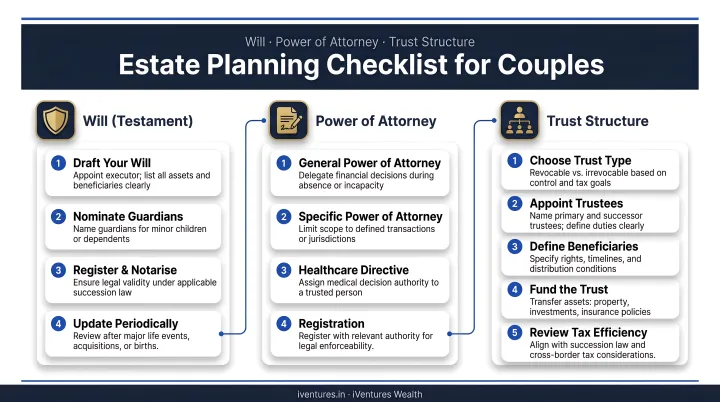

Updating Beneficiaries and Estate Documents

After marriage — or any major life event — both partners need to update beneficiary nominations across every account: life insurance policies, EPF, NPS, bank accounts, and mutual fund folios. This step is account-specific and frequently missed.

One critical clarification: nominations do not replace a Will. The Supreme Court of India confirmed in Shakti Yezdani v. Jayanand Jayant Salgaonkar (2023) that a nominee is effectively a custodian, not a beneficial owner — legal heirs can still assert overriding claims without proper succession documents in place.

At a minimum, couples should:

- Draft or update a Will that clearly reflects current asset distribution intentions

- Establish Power of Attorney for both medical and financial decisions

- For households with more complex assets — business ownership, inherited wealth, multiple properties — explore trust structures for efficient, conflict-free wealth transfer

iVentures Wealth helps couples navigate this process — coordinating with empanelled legal counsel on Will drafting and trust structuring, while ensuring the estate plan stays aligned with nomination decisions and broader succession intentions.

When to Seek Professional Financial Advice

Some situations genuinely benefit from professional guidance. Consider working with a SEBI-registered advisor when:

- There is a significant income disparity between partners, creating asymmetric tax and investment implications

- One or both partners have complex assets — business ownership, inherited wealth, multiple real estate holdings, or ESOPs

- You have NRI or cross-border considerations — foreign income, DTAA obligations, or assets across jurisdictions

- Financial disagreements keep recurring despite good intentions

- You want a comprehensive plan built without blind spots

If any of these apply, a fee-only, SEBI-registered advisor is worth the conversation. iVentures Wealth works with couples — including founders, CXOs, and affluent families — on personalised plans spanning investment strategy, tax optimisation, estate planning, and retirement. As a fiduciary firm with 20+ years of experience and ₹1,200+ Cr in assets under advisory, they charge only for advice, not for products placed. Reach the team directly at info@iventures.in.

Frequently Asked Questions

How do you do financial planning as a couple?

Start with an open conversation covering each partner's income, debts, assets, and money mindset. From there, set shared goals across short, medium, and long-term horizons, build a joint budget, coordinate investments as a single household portfolio, and schedule regular reviews to keep the plan current.

What is the 50/30/20 rule for couples?

The rule divides combined take-home income into 50% for essential needs, 30% for discretionary spending, and 20% for savings and investments. Couples can adjust these ratios based on their income level, life stage, or specific priorities — such as accelerating debt repayment or building a home deposit.

What is the 2-2-2 rule for couples?

The 2-2-2 rule is a relationship maintenance framework: a date every 2 weeks, a weekend getaway every 2 months, and a longer trip every 2 years. Applied to money management, the same cadence works well — regular check-ins, monthly budget reviews, and an annual goal-setting session keep finances aligned without turning them into a recurring source of conflict.

Should couples keep finances separate or combine them?

Fully joint, fully separate, or hybrid structures each work depending on the couple's comfort level, income situation, and shared goals. The hybrid model — joint account for shared expenses and goals, separate accounts for personal spending — tends to balance transparency with individual autonomy most effectively.

When should couples hire a financial advisor?

When dealing with complex assets, major life transitions (marriage, inheritance, retirement planning), significant income differences between partners, or recurring financial disagreements that a structured plan could resolve. A SEBI-registered, fiduciary advisor removes conflicts of interest and provides objective guidance.

How do couples plan for retirement together in India?

Align on a retirement vision and target corpus early, then coordinate tax-advantaged instruments — PPF (individual accounts per partner), NPS, EPF, and equity SIPs — as a unified household strategy. A SEBI-registered advisor helps ensure the combined portfolio reflects both partners' risk profiles, shared lifestyle goals, and rising healthcare costs.