Here is the problem: the PGIM India Retirement Readiness Survey 2025 found that Indians typically start retirement planning at age 37, and only 37% have a retirement plan at all. By the time most people get serious, they have already surrendered years of compounding growth they can never recover.

This article covers exactly what you need to act on now: the compounding math that makes your 30s irreplaceable, India-specific instruments built for this stage, savings benchmarks, tax strategies, and the financial habits that protect everything you build.

Key Takeaways

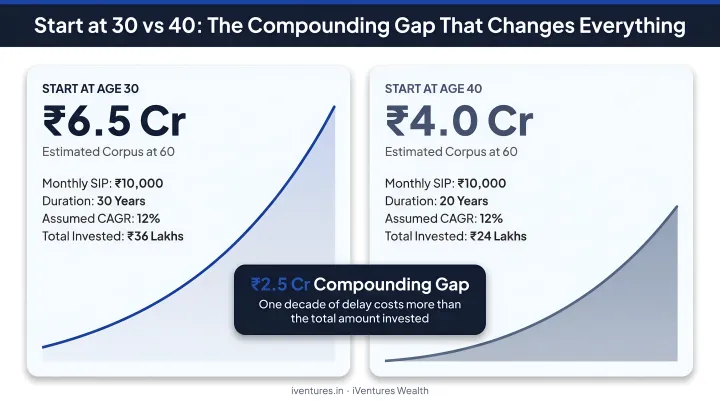

- Starting at 30 vs. 40 with the same ₹10,000 monthly SIP can produce a ₹2.5 crore difference in retirement corpus at 60 (at an assumed 12% annual return).

- NPS, PPF, ELSS, and EPF each serve a distinct role; combining them strategically multiplies your retirement corpus.

- A practical benchmark: aim for 1x your annual income saved by age 30, and 2–3x by age 35.

- Clearing high-interest debt and building an emergency fund are prerequisites, not afterthoughts.

- A SEBI-registered fiduciary adviser delivers a personalised, conflict-free plan built around your long-term goals.

Why Your 30s Are the Most Critical Decade for Retirement Planning

The Compounding Gap Is Larger Than You Think

Consider this illustration, using a standard SIP future-value formula at an assumed 12% annual return:

| Start Age | Monthly SIP | Duration | Total Invested | Approx. Corpus at 60 |

|---|---|---|---|---|

| 30 | ₹10,000 | 30 years | ₹36 lakh | ₹3.53 crore |

| 40 | ₹10,000 | 20 years | ₹24 lakh | ₹1.00 crore |

These figures are illustrative and assume a consistent 12% p.a. return. Actual market returns vary and are not guaranteed.

The person who starts at 40 invests only ₹12 lakh less — but ends up with ₹2.53 crore less. The difference isn't the amount invested — it's the years lost.

At 30, you have 25–30 years for compounding to work. At 40, you have 20. At 50, you're racing against arithmetic. Starting early isn't a lifestyle choice; it's the single most powerful lever available to you.

The Lifestyle Creep Trap

Rising income in your 30s carries a hidden risk. For every 10% income rise, discretionary spending among urban Indians tends to rise by nearly 12%, according to expert commentary reported by the Economic Times. Bigger apartments, car upgrades, premium subscriptions, frequent dining out — each feels justified in isolation, but together they quietly erode your savings rate.

The fix is straightforward: pay yourself first. Before discretionary spending happens, automate your retirement contributions. Treat them like an EMI you cannot miss. Automation removes the temptation to spend what you intended to save — and forces your lifestyle to adjust to what remains, not the other way around.

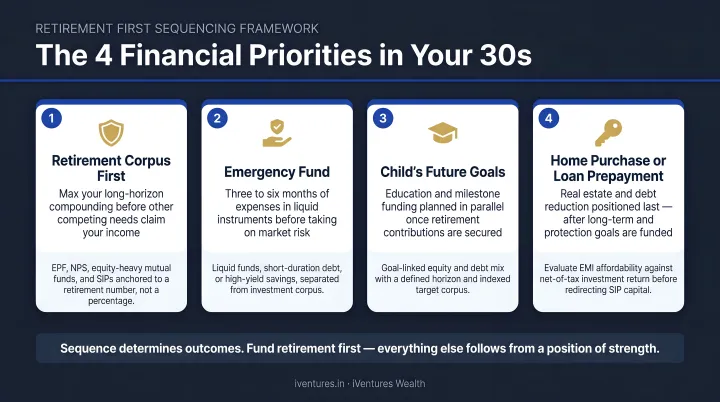

Competing Financial Goals: How to Prioritise

Once lifestyle spending is contained, the harder challenge emerges: your 30s rarely demand just one financial priority. They demand several at once:

- Home purchase EMI — often the largest monthly outflow

- Children's education fund — urgent for parents of young children

- Aging parent support — frequently unplanned but non-negotiable

- Retirement savings — often the first thing people defer, because the deadline feels distant

One principle clarifies the order: you can borrow for education, but not for retirement. There are student loans, scholarships, and education funds. There is no loan product for a 70-year-old who did not save enough.

This does not mean ignoring other goals. It means establishing a non-negotiable retirement contribution first, then structuring the remaining surplus across other priorities. Map every rupee to a specific goal and timeline — and set the retirement line before any other allocation begins. That sequence is what keeps one urgent priority from quietly consuming another.

Know Your Numbers: How Much Should You Be Saving?

Savings Benchmarks by Age

No official Indian regulatory body publishes an age-based salary multiplier the way Fidelity does for US investors, but the following framework is widely used as a directional guide:

| Age | Savings Benchmark |

|---|---|

| 30 | ~1x annual income |

| 35 | 2–3x annual income |

| 40 | 3–4x annual income |

These are not rigid rules. Your target corpus depends on your expected retirement age, desired lifestyle, and planned expenses. Use these as reference points to gauge direction, not as definitive verdicts on your financial health.

The Savings Rate Target

SEBI's investor education material recommends saving 20% of income as a rule of thumb, while Business Standard notes 10–15% as a realistic starting point for young professionals.

A practical approach:

- Start at 10% if 15–20% feels unmanageable right now

- Increase contributions by 1–2% with every salary increment

- Over 5–7 years, you reach the 15–20% target without experiencing a sharp lifestyle disruption

The key is to make increases automatic — link contribution step-ups to appraisal cycles so the money is directed before lifestyle adjusts to the higher income.

Why Inflation Cannot Be Ignored

India's consumer price inflation was 5.0% in 2024 according to World Bank data, with the RBI's official target set at 4% with a 2–6% tolerance band. At 5% inflation sustained over 25 years, a corpus that looks adequate today loses more than two-thirds of its real purchasing power by the time you retire.

Your investment strategy must beat inflation over the long term, not merely keep pace with it. For a 30-year-old, equity-linked instruments aren't a bold choice — they're a necessary one. Avoiding equities to "play it safe" is itself a risk: the risk of your corpus falling short when it matters most.

The Best Retirement Investment Instruments for Indian Investors in Their 30s

NPS: Long-Term Equity Growth With Extra Tax Benefits

The National Pension System now manages ₹14,44,753 crore AUM across 8.40 crore subscribers (NPS Trust Annual Report 2025). For a 30-year-old, it offers a compelling combination:

- Tier I is the locked retirement account; Tier II functions as a flexible savings account

- Active Choice lets you allocate up to 75% in equities — appropriate for a 30-year-old with a 25–30 year horizon

- Auto Choice shifts allocation toward debt as you age, reducing the need for manual rebalancing

- At maturity, 60% of the corpus is tax-exempt as a lump sum; 40% must purchase an annuity

For someone in their 30s comfortable with moderate-to-high risk, a high equity allocation within NPS allows compounding to do significant work over decades.

PPF: The Tax-Free Stability Anchor

PPF earns 7.1% interest (rate effective 01.04.2020 to 30.06.2026 per NSI), fully government-backed. Its EEE (Exempt-Exempt-Exempt) tax status means contributions, interest, and maturity proceeds are all tax-free.

Key features:

- 15-year maturity (extendable in 5-year blocks)

- Partial withdrawals permitted from the 7th financial year

- Annual contribution limit: ₹1.5 lakh

- Qualifies under Section 80C

PPF's role in a retirement portfolio is not to generate the highest return — it is to provide a reliable, government-backed, tax-free debt component that balances the volatility of equity-linked instruments.

ELSS: The Equity-Linked 80C Workhorse

ELSS funds maintain at least 80% in equities with a mandatory 3-year lock-in — the shortest among all Section 80C instruments. ELSS AUM stood at ₹2,17,310 crore as of March 2026 (AMFI Monthly Note, March 2026).

Why ELSS works well for 30-year-olds:

SIPs in ELSS through your 30s allow compounding to build momentum over 25+ years

The 3-year lock-in instils discipline without permanently tying up capital

Equity-linked returns have historically outpaced inflation over long horizons

Gains up to ₹1.25 lakh annually are currently tax-exempt under LTCG provisions

Equity-linked returns have historically outpaced inflation over long horizons

Gains up to ₹1.25 lakh annually are currently tax-exempt under LTCG provisions

Past performance does not guarantee future results.

EPF: The Silent Compounder Many Ignore

For salaried employees, EPF is already running — but most treat it as background noise. The Central Board of Trustees recommended an 8.25% interest rate for FY2025-26, making it a competitive debt instrument.

The most critical EPF habit: never withdraw on job changes. Transfer your EPF to the new employer using Form 13(R) or the EPFO online transfer facility. Withdrawals before 5 years of total service attract TDS (above ₹50,000) and permanently destroy years of compounding.

Building a Diversified Retirement Portfolio

No single instrument should carry the full weight of your retirement plan. A well-structured portfolio for a 30-year-old typically combines:

- Growth engine: ELSS SIPs + NPS equity allocation (higher volatility, higher long-term potential)

- Stable anchor: PPF + EPF (government-backed, lower volatility, tax-efficient)

Getting the allocation right across these instruments depends on your income structure, tax bracket, and risk tolerance. iVentures Wealth works with investors to build and periodically rebalance portfolios that draw from each of these instruments in proportion to their individual financial goals.

Tax Optimisation Strategies to Grow Your Retirement Corpus

Section 80C: ₹1.5 Lakh Most People Leave Partially Unused

The Section 80C deduction limit is ₹1,50,000 per financial year. Qualifying retirement instruments include:

- ELSS mutual funds

- PPF contributions

- EPF employee contributions

- Life insurance premiums

Most 30-somethings contribute to EPF automatically through payroll, but do not actively fill the remaining 80C headroom with ELSS or PPF. Mapping out your EPF contribution and consciously topping up to ₹1.5 lakh through ELSS or PPF is a high-impact step.

Section 80CCD(1B): The NPS-Exclusive Extra Deduction

NPS offers an additional ₹50,000 deduction under Section 80CCD(1B), entirely separate from and beyond the ₹1.5 lakh 80C ceiling. The tax impact at different slabs:

| Income Tax Slab | Tax Saved on ₹50,000 NPS Contribution |

|---|---|

| 20% slab | ~₹10,000 |

| 30% slab | ~₹15,000 |

(Before cess and surcharge)

For a professional in the 30% bracket, the NPS deduction alone saves roughly ₹15,000 in taxes annually — money that stays invested and compounds.

Plan Withdrawal Tax Efficiency Now, Not at 60

These deductions reduce your tax bill today — but the instruments you choose also shape how much tax you pay at 60. The two broad categories behave very differently at withdrawal:

- EEE instruments (PPF, ELSS after 3 years): Contributions, growth, and withdrawals are all tax-free

- Partially taxable instruments (NPS): 40% of the corpus must purchase an annuity, and annuity income is taxed as regular income

Building exposure across both categories in your 30s gives you the flexibility to draw from tax-free sources first and manage your effective tax rate in retirement.

Financial Habits That Protect and Accelerate Your Retirement Savings

Build an Emergency Fund Before You Invest

Three to six months of living expenses held in a liquid instrument — a savings account or liquid mutual fund — is a prerequisite, not a nice-to-have. Without it, the first unexpected expense (job loss, medical emergency, home repair) forces you to liquidate retirement investments, destroying years of compounding at the worst possible time.

Tackle High-Interest Debt Aggressively

Credit card interest can reach 3.75% per month — 45% per annum (SBI Card MITC). No equity investment offers a risk-free 45% return. Eliminating high-cost debt is the closest thing to a guaranteed high return you will ever get.

A sensible priority order:

- Capture your employer's full EPF match

- Eliminate credit card and personal loan debt (18–45% p.a.)

- Build your emergency fund

- Maximise retirement contributions (NPS, ELSS, PPF)

- Channel surplus toward other goals

Protect What You Are Building With Adequate Insurance

Term life cover and health insurance are foundational to any retirement plan. Skipping or under-buying either creates a single point of failure that can undo years of disciplined saving.

Key coverage principles to follow:

- Health insurance: A serious hospitalisation without cover can wipe out 2–3 years of savings in weeks; a ₹10–20 lakh family floater is a reasonable starting floor

- Term life cover: A cover of 10–15× your annual income protects dependents if you are not around to fund the plan yourself

- Annual review: As income rises and liabilities shift, your cover needs to keep pace — what was adequate at 32 may be insufficient at 38

Why Working With a SEBI-Registered Fiduciary Adviser Matters in Your 30s

Generic rules of thumb — "save 15–20%," "invest in NPS" — get you started. They do not account for your specific tax situation, your equity-to-debt ratio, your EPF balance, your competing goals, or your risk tolerance.

As income grows and life events multiply (marriage, children, property, career transitions), DIY planning increasingly leaves money on the table or exposes you to unnecessary risk.

iVentures Wealth is a SEBI-registered investment adviser (RIA No. INA000019026) with 20+ years of experience and ₹1,200+ crore in assets under advisory. As a fee-only firm, iVentures earns no commissions or trail income from product manufacturers — every recommendation is driven purely by your financial interests.

Their CFA-led research team builds personalised retirement strategies for professionals, founders, CXOs, and affluent families across India — mapping every investment to a specific goal, timeline, and required corpus. Coverage includes:

- NPS allocation and ELSS fund selection

- PPF strategy and tax optimisation under 80C and 80CCD(1B)

- Long-term portfolio construction designed to beat inflation

- Goal-linked asset allocation across equity, debt, and alternatives

Frequently Asked Questions

What is the best retirement plan for someone in their 30s?

No single instrument works for everyone. Most people build a strong foundation with a combination of NPS (equity growth + exclusive ₹50,000 tax deduction), PPF (safe, tax-free returns), and ELSS (80C-linked equity growth). The right mix depends on your risk tolerance, income, and goals.

How much should someone in their 30s be saving for retirement?

Aim for 15–20% of gross income directed toward retirement. Start with whatever is manageable — even 10% — and step up contributions by 1–2% with each salary increment. The goal is to reach meaningful benchmarks: roughly 1x annual salary saved by 30, and 2–3x by 35.

How do I start retirement planning in my 30s?

Three immediate steps: calculate your retirement corpus goal using an online SIP calculator, open an NPS Tier I account and start an ELSS SIP to maximise 80C benefits, and log into your EPFO passbook to confirm your balance is being transferred (not withdrawn) on job changes.

Is it too late to start retirement planning at 35?

Not at all. With roughly 25 years to a typical retirement age of 60, compounding still has significant runway. Increasing your savings rate and maintaining higher equity allocation in instruments like ELSS and NPS can compensate for the delayed start.

What is NPS and how does it help in retirement planning?

NPS is a government-backed pension scheme that invests across equity, corporate bonds, and government securities. It also offers a dedicated tax deduction of ₹50,000 under Section 80CCD(1B), which sits entirely outside the standard ₹1.5 lakh Section 80C limit.

How does compounding work in retirement savings?

Compounding means your returns earn returns of their own — and that cycle repeats for decades. Over 25–30 years, someone who starts at 30 with ₹10,000/month can accumulate more than 3x the corpus of someone who starts the same SIP a decade later.