The good news: once you understand the core framework, it's manageable. This guide covers the five areas that matter most — capital gains tax (LTCG vs STCG), dividend withholding and DTAA relief, ITR filing obligations, TCS under LRS, and the US estate tax risk that most investors overlook entirely.

Key Takeaways

- Capital gains on US stocks are taxed only in India — the US does not levy capital gains tax on Indian investors (non-resident aliens)

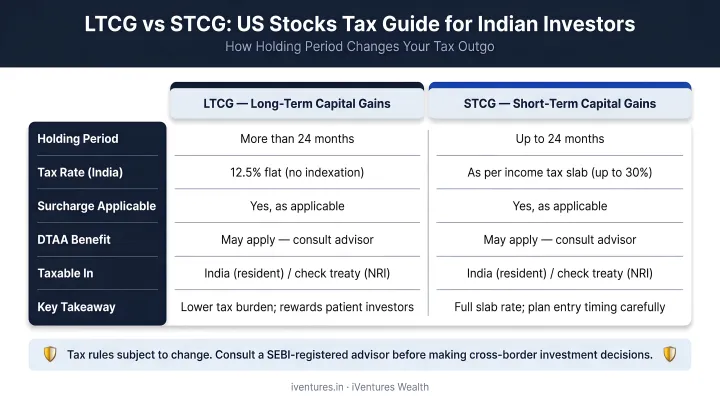

- LTCG rate is 12.5% (effective maximum ~14.95% with surcharge and cess) for US stocks held over 24 months

- STCG is taxed at your income slab rate (up to ~42.74% for high-income investors) for holdings under 24 months

- US dividends face 25% withholding tax at source — claimable as a credit in India via Form 67 under the India-US DTAA

- Schedule FA disclosure is mandatory every year — skipping it risks ₹10 lakh penalties under the Black Money Act, even with zero income

Capital Gains Tax on US Stocks: LTCG vs STCG Explained

The Core Rule: Only India Taxes Your Gains

Indian residents are taxed on global income — so gains from US stocks are fully taxable in India. Here's where most investors assume the worst: they expect double taxation. It doesn't happen on capital gains.

The US generally does not tax capital gains of non-resident aliens on stock sales, provided the investor spends fewer than 183 days in the US during the tax year. Combined with Article 13 of the India-US DTAA, which preserves each country's right to tax under domestic law, the practical outcome is that only Indian tax applies on your US stock gains.

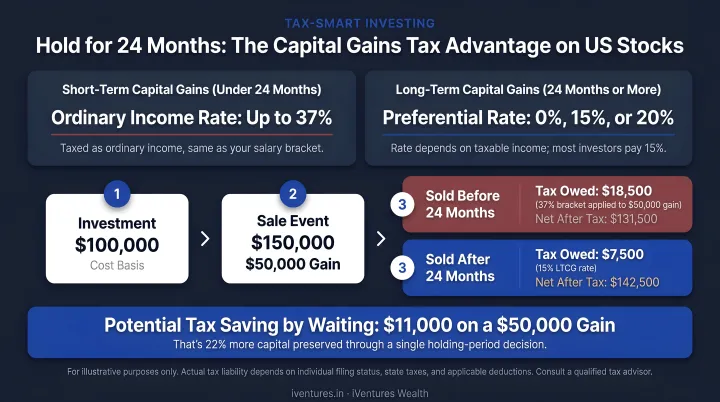

LTCG: 12.5% for Holdings Over 24 Months

US stocks are treated as unlisted/foreign assets under Indian tax law. The holding period threshold for long-term classification is 24 months — not 12 months as applies to Indian-listed equities.

Key LTCG facts:

- Rate: 12.5% (applicable to transfers on or after 23 July 2024 under the Finance (No. 2) Act, 2024)

- Effective maximum rate: ~14.95% after the 15% surcharge cap and 4% cess

- No ₹1.25 lakh annual exemption — that's Section 112A, which is STT-linked and doesn't apply to US stocks

- No indexation — this benefit was permanently removed for foreign equity sold on or after 23 July 2024

- Governing section: Section 112 (not Section 112A)

STCG: Slab Rate for Holdings Under 24 Months

Sell before 24 months and the gains are added to your total income, taxed at your applicable slab rate. The concessional 20% rate under Section 111A doesn't apply here — it's also STT-linked and restricted to Indian-listed equities.

For high-income investors under the old tax regime with income above ₹5 crore, the effective STCG rate on US stocks can reach ~42.74% (30% peak rate × 1.37 surcharge × 1.04 cess).

INR Conversion, FIFO, and Loss Set-Off

INR conversion: Both the purchase price and sale price must be converted to INR using the SBI Telegraphic Transfer (TT) Buying Rate on the last day of the month preceding the transaction month. If you sell in November, use the October 31 rate.

This matters more than most investors realise — if the rupee has depreciated since you bought the stock, your INR gains will look larger than your USD gains. You could show a meaningful taxable gain in rupee terms even if your dollar return was modest.

Two additional rules govern how gains are calculated and offset:

- FIFO (First-In-First-Out): Under Section 45(2A), India applies FIFO to determine which shares are treated as sold when you hold multiple lots

- Short-term capital losses (STCL) can offset both STCG and LTCG

- Long-term capital losses (LTCL) can only offset LTCG

- Loss carry-forward: Losses carry forward for 8 assessment years — but only if the ITR is filed on time

Dividend Tax on US Stocks: The 25% Withholding and DTAA

How the Double-Layer Works

When a US company declares a dividend, the IRS withholds tax before you receive anything. Statutory rate: 30%. With a valid W-8BEN form on file, the India-US DTAA caps this at 25% for Indian retail investors.

So you receive 75 cents for every dollar declared. But Indian tax law requires you to report the gross dividend (100%) as income under "Income from Other Sources" in Schedule OS.

In short, the same dividend gets taxed twice — once by the US at source, and again by India on the full amount. The W-8BEN form and Foreign Tax Credit mechanism exist specifically to manage this double-layer.

The W-8BEN Form

Submit this to your US broker to certify non-US resident status and claim the DTAA-reduced rate. Without it, the full 30% is withheld. W-8BEN stays valid until the last day of the third succeeding calendar year, so set a calendar reminder to renew it before expiry.

Filing the form reduces your US withholding — but it doesn't eliminate your Indian tax obligation. That's where the Foreign Tax Credit comes in.

Claiming the Foreign Tax Credit (FTC)

Under Rule 128, Indian investors can credit the 25% US withholding against their Indian tax liability on the same dividend income. Indian tax law caps the credit at the lower of:

- US tax actually withheld, or

- Indian tax attributable to that dividend income

If your Indian slab rate on that income is lower than 25% — say, 20% — the excess 5% US tax becomes an unrecoverable cost. It cannot be refunded or carried forward. Investors in the 30% slab typically absorb the full credit; those in lower slabs effectively subsidize the US Treasury on the gap.

A Few Practical Points

- Reinvested dividends (DRIP) are taxable in the year received, not when eventually sold. The reinvested amount forms the new cost basis.

- INR conversion for dividends uses the SBI TT Buying Rate on the last day of the month before the dividend receipt month.

- Capital gains on US stocks are NOT taxed in the US — so there's no double-taxation issue on the gains side, only on dividends.

ITR Filing for US Stock Investments: Forms and Schedules

Which ITR Form to Use

You cannot file ITR-1 or ITR-4 if you hold foreign assets — these forms don't include Schedule FA. The correct forms are:

- ITR-2 — for individuals with salary income, capital gains, and foreign assets

- ITR-3 — if you also have business or professional income

The ITR-2 filing deadline for FY 2025-26 (AY 2026-27) is 31 July 2026 for non-audit cases (no extension has been announced as of mid-June 2026).

The Five Key Schedules

| Schedule | What to Report |

|---|---|

| Schedule CG | Capital gains from US stocks — under "unlisted shares / other assets" |

| Schedule OS | Dividend income from US stocks |

| Schedule FSI | All income earned from foreign sources |

| Schedule TR | Summary of foreign taxes paid and credit claimed |

| Schedule FA | All foreign assets held at any point during the calendar year |

The Schedule FA Calendar-Year Trap

Schedule FA runs on the calendar year (January–December), not the Indian financial year. This catches investors out regularly. If you held US stocks at any point during calendar year 2025 — even for one day, even if you've already sold them — you must disclose them in your FY 2025-26 ITR.

Non-disclosure carries penalties of ₹10 lakh per year under Section 42 of the Black Money Act, with potential imprisonment up to 7 years for wilful failure.

Form 67: Filing for Foreign Tax Credit

To claim FTC on US dividend withholding, file Form 67 electronically on the income tax e-filing portal. Attach the US broker's Form 1042-S as supporting documentation. Current official guidance permits Form 67 to be filed on or before the end of the relevant assessment year.

Late filing carries real risk: CPC Bangalore may automatically reject the FTC claim. ITAT Delhi (Kavish Arora, ITA No. 407/Del/2024, January 2025) has treated late filing as procedural in some cases — but don't rely on ITAT relief as a safety net. File Form 67 before submitting your ITR.

Managing these five schedules across a global portfolio — especially with multiple jurisdictions, entities, and asset classes — creates significant coordination overhead between investors and their chartered accountants. For UHNI clients and family offices, iVentures Wealth prepares consolidated income, capital gains, and FTC documentation reports that give CAs a clean, structured starting point, cutting the back-and-forth that typically delays ITR filing for multi-jurisdiction portfolios.

TCS, LRS, and US Estate Tax: Other Key Taxes to Know

Tax Collected at Source (TCS) on Remittances

When you remit money abroad under the Liberalised Remittance Scheme (LRS) to invest in US stocks, TCS applies:

- Rate: 20% on cumulative remittances exceeding ₹10 lakh per PAN per financial year

- LRS annual limit: USD 250,000 per financial year

- TCS is not an additional tax — it appears in Form 26AS and is fully adjustable against your total income tax liability or refundable via ITR

Sale proceeds from US investments must be repatriated to India within 180 days unless reinvested in permitted overseas assets. Balances held beyond this window may attract FEMA compliance issues.

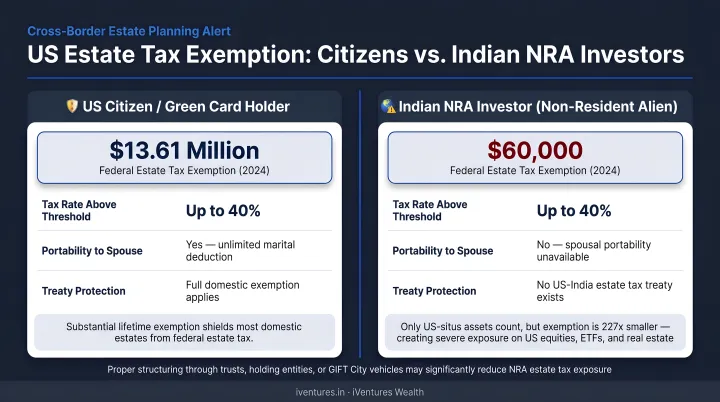

US Estate Tax: A Hidden Risk for Indian Investors

The US imposes estate tax on "US-situs assets" — shares of US-incorporated companies and US-domiciled ETFs (like SPY) — held by non-resident aliens at death. Most Indian investors overlook this exposure entirely.

| US Citizens | Indian Investors (NRAs) | |

|---|---|---|

| Estate tax exemption | ~$13.99 million (2025) | $60,000 only |

| Estate tax rate on excess | 18–40% | 18–40% |

| India-US estate tax treaty | N/A | None exists |

If you hold more than $60,000 in US stocks at death, the excess is subject to US estate tax at rates up to 40%. Unlike many countries, India has no estate tax treaty with the US — meaning your heirs cannot claim a foreign tax credit to reduce this exposure.

How to mitigate it: Ireland-domiciled UCITS ETFs (such as CSPX, VUAG, or SPY5) track the same indices as US-domiciled ETFs but are issued by non-US corporations — so they're not classified as US-situs property. Indian mutual funds with US equity exposure are another route that sidesteps this issue.

Smart Tax Strategies When Investing in US Stocks from India

Tax Loss Harvesting

India has no wash-sale rule equivalent to the US IRC Section 1091. No official CBDT source expressly disallows selling a loss-making position and immediately repurchasing the same stock.

Practical approach:

- Identify US stock positions with unrealised losses before 31 March

- Sell to crystallise the capital loss in that financial year

- Report the loss in your ITR — this is what activates carry-forward rights

- Reinvest if you still want the exposure

Rules on using those losses:

- STCL offsets both STCG and LTCG

- LTCL offsets LTCG only

- Losses carry forward for 8 assessment years — but only if ITR is filed by the due date

The 24-Month Holding Period Arbitrage

For high-income investors, the tax difference between STCG and LTCG on US stocks is enormous. STCG is taxed at slab rates — potentially 42.74% under the old regime for income above ₹5 crore. LTCG is capped at ~14.95%.

If you're sitting at month 22 or 23, waiting the additional weeks to cross the 24-month threshold could save a substantial amount on a large position. On a ₹50 lakh gain, the difference between 42.74% and 14.95% is approximately ₹13.9 lakh in tax — purely from timing.

Getting Professional Advisory Right

For UHNI investors and family offices managing substantial US equity portfolios, the interactions between LTCG timing, FTC optimization, Schedule FA compliance, TCS management, and US estate tax planning are complex — and decisions in one area directly affect outcomes in another.

That interdependence is where specialist advisory earns its value. iVentures Wealth (SEBI RIA: INA000019026), a Gurugram-based wealth advisory firm with 20+ years of experience, works with affluent investors, founders, CXOs, and family offices on exactly these multi-jurisdictional challenges — covering DTAA claim optimization, capital gains computation, FTC documentation, and coordination with chartered accountants on ITR compliance. Minimum investable assets: ₹5 crore for NRI/OCI clients, ₹10 crore for resident professionals and CXOs.

Frequently Asked Questions

How much tax do I pay on US stocks?

LTCG on US stocks held over 24 months is taxed at 12.5% (effective maximum ~14.95% with surcharge and cess). STCG on holdings under 24 months is taxed at your income slab rate — up to ~42.74% for very high-income investors. US dividends face 25% withholding at source, which can be partially or fully credited against Indian tax liability by filing Form 67.

How are US stock options taxed in India?

ESOPs and RSUs from US companies are taxed in two stages. First, at vesting or exercise, the fair market value minus any amount paid by the employee is treated as a perquisite (salary income). Second, when the shares are eventually sold, the gain from FMV on exercise date to sale price is taxed as capital gains — LTCG or STCG based on the 24-month holding period from the exercise/allotment date.

Who pays 42% tax in India?

The ~42.74% effective rate applies to individuals with total income exceeding ₹5 crore under the old tax regime: 30% peak slab rate plus a 37% surcharge and 4% cess. This rate applies to slab-rate income, so STCG on US stocks (held under 24 months) can attract it for high-income investors. LTCG on US stocks is not affected — the surcharge on Section 112 income is capped at 15%.

Do I need to report US stocks in my ITR even if I made no profit?

Yes. All foreign assets held at any point during the calendar year must be disclosed in Schedule FA, regardless of whether any income was earned. This includes stocks you've since sold. Non-disclosure can attract penalties of ₹10 lakh per year under Section 42 of the Black Money Act, with imprisonment possible for wilful failure.

What is Form 67 and when must I file it?

Form 67 is filed electronically on the income tax e-filing portal to claim Foreign Tax Credit for US taxes withheld on dividends. Current guidance permits filing until the end of the relevant assessment year, but submitting before your ITR is recommended to avoid CPC rejection of the FTC claim.

Is there a US estate tax on US stocks held by Indian investors?

Yes. US stocks are US-situs assets, and Indian investors receive only a $60,000 exemption (versus ~$13.99 million for US citizens in 2025). Holdings above this threshold face estate tax rates of 18–40% at death. There is no India-US estate tax treaty. Switching to Ireland-domiciled UCITS ETFs like CSPX or VUAG is a practical way to sidestep this exposure.