This article answers those questions directly: what minimums represent, how they vary across firm types and client tiers in India, why reputable firms set them, and what you actually unlock once you meet one.

Key Takeaways

- Wealth management minimums reflect the economics of delivering personalised, multi-disciplinary advisory—not arbitrary exclusion criteria

- In India, minimums range from ₹25–50 lakh for boutique advisory to ₹5 crore+ for full-service wealth management

- SEBI mandates ₹50 lakh for PMS and ₹1 crore for AIFs; these are regulatory product floors, not advisor minimums

- Meeting a minimum doesn't guarantee fiduciary advice; verify SEBI-registered IA status separately

- Complexity—not just corpus size—determines when wealth management becomes necessary

What Wealth Management Minimums Actually Mean

Investable Assets vs. Total Net Worth

A minimum investment requirement is the threshold of investable assets a firm requires before onboarding a client. This is not total net worth.

The distinction matters. A business owner with a ₹20 crore company, a ₹5 crore home, and ₹3 crore in liquid financial assets has a net worth north of ₹28 crore—but only ₹3 crore that a wealth manager can actually work with. Firms set minimums based on deployable capital because that's what determines service viability and the range of products they can recommend.

Illiquid assets—real estate, business equity, locked ESOPs, provident fund balances—generally don't count toward the investable asset threshold.

Fee Thresholds vs. Asset Minimums

Some firms have no stated asset minimum but charge a minimum annual fee that implicitly creates one. If a firm charges ₹3 lakh per year as a floor, a client with ₹50 lakh in assets is effectively paying 0.6% of AUM before any service has been rendered—a burden that makes the relationship economically impractical at that level.

Ask about fee floors before signing — not after.

How Service Type Affects the Minimum

Within the same firm, minimums often vary by what you're asking for:

- Basic portfolio management — lower threshold, often ₹25–50 lakh

- Goal-based financial planning — typically ₹1–2 crore

- Comprehensive wealth management (tax, estate, alternatives) — ₹5 crore+

- Family office services — ₹10–100 crore and above

Meeting the entry minimum grants access to the base tier only. Services like estate structuring, NRI tax advisory, or AIF access often sit behind higher internal thresholds.

The Regulatory Context

SEBI's IA Regulations define an Investment Adviser as someone who provides investment advice for consideration. SEBI does not set a minimum investable asset amount for becoming a client of an IA — those minimums are commercial decisions made by individual firms.

What SEBI does regulate is the fee structure. Under the 2025 Master Circular, IA fees are capped at 2.5% per annum of Assets under Advice (AUA mode) or ₹1,51,000 per annum per family (fixed fee mode).

AMFI is explicit that mutual fund distributors cannot provide investment advice unless registered with SEBI as Investment Advisers. That IA vs. distributor distinction is a critical one for anyone evaluating an advisor.

The Range: How Minimums Vary by Firm Type and Client Tier

Minimums in India exist on a wide spectrum. The same number can mean entirely different things depending on the type of firm setting it and the service tier being offered.

Entry-Level and Mass Affluent Services

At the lower end, boutique advisors, digital platforms, and smaller SEBI-registered RIAs typically work with clients from ₹25–50 lakh in investable assets. At this level, clients can expect:

- Basic portfolio construction and mutual fund advisory

- Risk profiling and goal-setting conversations

- Standard financial planning frameworks

Trade-offs are real here. Personalisation is limited, dedicated relationship managers are rare, and access to regulated higher-ticket products like PMS or AIFs isn't available because those carry their own SEBI-mandated floors.

HNI Wealth Management

The mid-tier—where meaningful wealth management typically begins—requires ₹1–5 crore in investable assets. Private bank advisory desks and established wealth firms typically classify High Net Worth Individuals using thresholds in this range, with DBS India noting that HNI in India commonly refers to investable surplus above ₹5 crore.

Public bank program thresholds reflect this clustering:

| Programme | Minimum |

|---|---|

| ICICI Wealth Management | ₹50 lakh relationship value |

| Axis Burgundy Private | ₹5 crore Total Relationship Value |

| ICICI Private Banking | ₹5 crore relationship value |

| Kotak Private | ₹7.5 crore relationship value |

These are relationship access thresholds—not SEBI-regulated advisory minimums—but they give a useful market benchmark.

At the ₹1–5 crore HNI tier, clients typically gain access to:

- Dedicated relationship managers and curated product recommendations

- Goal-based planning and periodic portfolio reviews

- PMS (SEBI-mandated minimum: ₹50 lakh) and AIFs (minimum: ₹1 crore per investor)

UHNI and Family Office Services

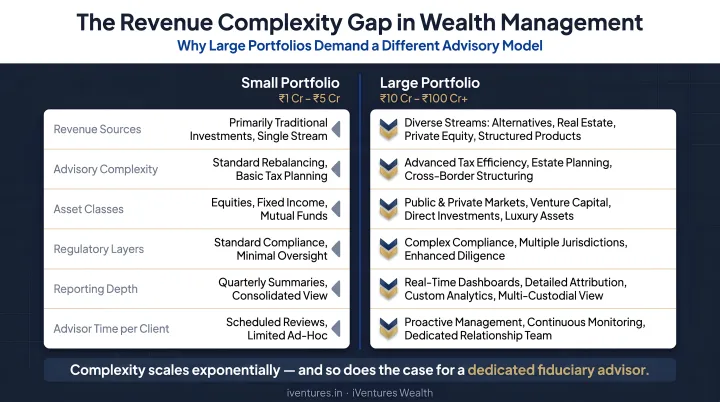

Full-service UHNI wealth management—covering estate planning, tax structuring, alternative investments, multi-generational planning, and family governance—typically begins at ₹5–10 crore in investable assets, with proper family office mandates starting at ₹25–100 crore and above.

According to Knight Frank's Wealth Report 2024, India had 13,263 UHNWIs (defined as USD 30 million+ net worth) in 2023, projected to grow approximately 50% by 2028. That expanding UHNI base is driving demand for the kind of multidisciplinary family office services that justify higher minimums.

EY's Indian Family Office Playbook reports that India's family offices grew from 45 to approximately 300 between 2018 and 2024—each requiring coordinated services spanning investment strategy, succession, governance, and next-generation planning. Each additional service layer—cross-border tax structuring, family governance, next-gen planning—adds to the coordination complexity, and minimums reflect that scope directly.

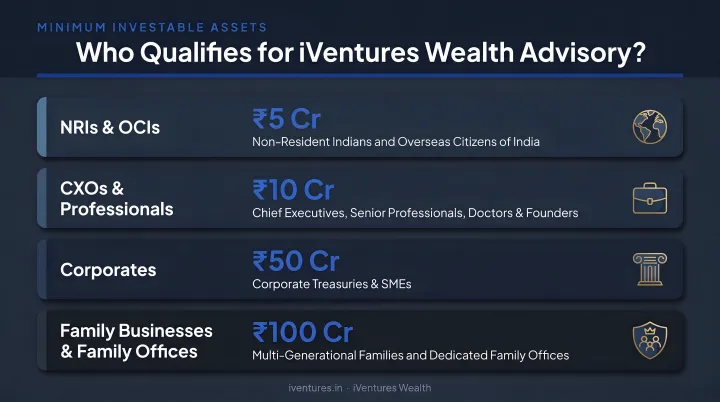

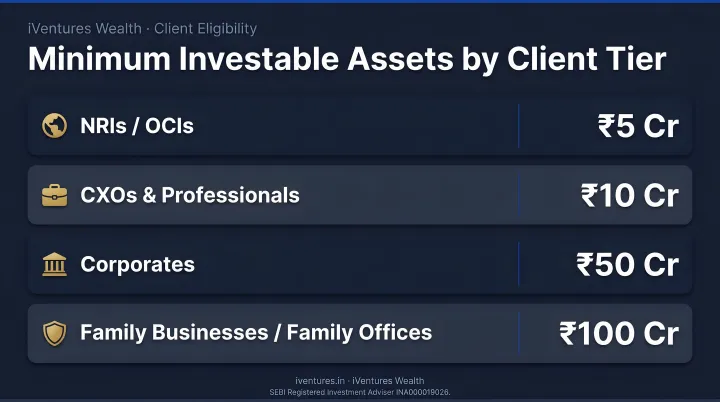

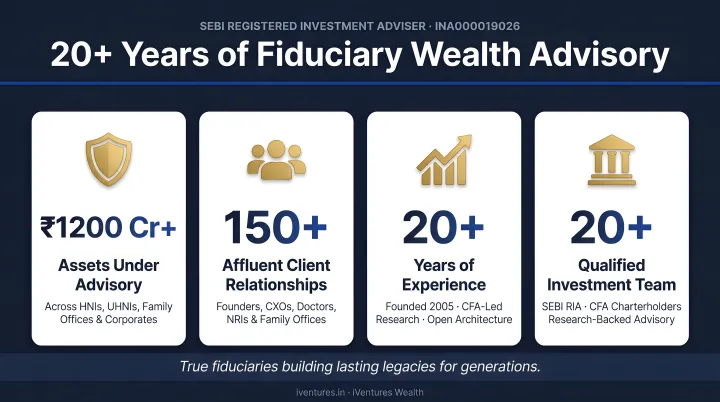

At iVentures Wealth, a SEBI-registered IA (INA000019026) based in Gurugram, minimum thresholds are set by the depth of service each client segment requires—not by assets alone:

| Client Segment | Minimum Investable Assets |

|---|---|

| NRIs & OCIs | ₹5 crore |

| CXOs & Professionals | ₹10 crore |

| Corporates | ₹50 crore |

| Family Businesses & Family Offices | ₹100 crore |

These are investable asset minimums—not net worth requirements—and each tier carries a meaningfully different service scope.

Why Firms Set Minimums: The Economics Behind the Threshold

The Revenue-Service Equation

Holistic wealth management requires a team of credentialed professionals. That team typically includes:

- CFA charterholders for investment research and portfolio construction

- Tax specialists for efficient structuring across jurisdictions

- Legal advisors for estate and succession planning

- Relationship managers who understand each client's complete financial picture

Each of these roles carries a real cost.

Under an AUM-based fee model, the math is straightforward: a client with ₹20 lakh generates a fraction of the revenue needed to sustain high-touch, multi-disciplinary service. SEBI's IA fee cap of 2.5% per annum on AUA sets an upper bound on what firms can charge.

Fee compression complicates this further. As AUM grows, advisory rates typically decline, meaning larger clients generate proportionally less revenue per rupee while their service needs become more complex.

Protecting Service Quality

Firms that accept clients below their viable threshold face a difficult choice:

- Overstretch advisors across too many relationships

- Reduce service depth for smaller clients

- Cross-subsidise smaller relationships using revenue from larger ones

None of these outcomes serve clients well. A well-defined minimum is ultimately a commitment to every existing client: that their advisor's attention, expertise, and service depth won't be diluted by relationships the economics cannot support.

The Tiered Fee Logic

A firm earns more per rupee from a ₹2 crore client than from a ₹20 crore client at the same percentage rate—but the ₹20 crore client's portfolio requires meaningfully more complex planning across tax, estate, and asset allocation. This revenue-complexity gap is precisely why firms concentrate on clients above a threshold: the relationship needs to be economically viable before it can be genuinely valuable.

What You Actually Unlock Once You Meet the Minimum

Meeting a minimum is a starting point, not a finish line. What you actually access — in terms of services, advisory depth, and asset classes — shifts materially at each threshold.

Service Progression by Threshold

₹50 lakh – ₹1 crore:

- Basic portfolio construction across mutual funds and listed equities

- Risk profiling and goal-setting

- PMS access (SEBI-mandated ₹50 lakh floor)

- AIF access at ₹1 crore

₹1–5 crore:

- Dedicated relationship manager

- Goal-based financial planning

- Tax-aware rebalancing

- Introductory estate planning advisory

₹5–10 crore:

- Comprehensive planning including NRI tax structuring, DTAA optimisation, FEMA compliance

- Full PMS and AIF portfolio construction

- Cross-border wealth coordination for NRI clients

- ESOP/RSU management for CXO clients

₹10 crore and above:

- Family office-grade services: estate structuring, private trust establishment, succession planning

- Concentrated stock diversification strategies

- Private equity and structured product allocations

- Consolidated multi-entity reporting across family members and entities

₹50–100 crore+:

- Dedicated advisory teams

- Family governance frameworks and family constitution drafting

- Next-generation training and succession implementation

- Multi-family office (MFO) or single family office (SFO) infrastructure

The Fiduciary Question

Meeting a minimum does not guarantee the advisor is acting in your interest. A distributor registered with AMFI and an IA registered with SEBI may both describe themselves as "wealth advisors"—but only the SEBI-registered IA is prohibited from accepting product commissions.

That distinction matters more than the minimum itself. Before engaging any firm, ask:

- Is the firm SEBI-registered as an Investment Adviser?

- Is it fee-only, with no product trail income?

- What is the SEBI registration number?

iVentures Wealth (SEBI RIA: INA000019026) operates under a CFA-led, fee-only structure — which means advice is never shaped by what earns a commission. No distributor arrangement, regardless of AUM threshold, can replicate that structural safeguard.

Common Myths About Wealth Management Minimums

Myth 1: "The higher the minimum, the better the service."

Not necessarily. A boutique SEBI-registered RIA with a ₹2 crore minimum and a CFA-credentialed team may deliver more personalised, conflict-free advice than a large private bank with a ₹7.5 crore threshold and a commission-laden product shelf. The minimum signals the service tier and the economics behind it—not the quality of judgment or the alignment of interests.

Myth 2: "I need to wait until I have more money before engaging a wealth manager."

Complexity is the real trigger, not corpus size alone. Waiting can be expensive when the situation is already urgent:

- A founder who has just sold equity faces capital gains planning decisions with hard tax deadlines

- An NRI with assets in three countries has DTAA, FEMA, and foreign asset disclosure obligations that don't pause for the portfolio to grow

- A business owner thinking about succession faces needs that become more costly the longer they're deferred

Uncoordinated advice at the wrong moment can create losses that no future portfolio growth will recover.

Myth 3: "Meeting the minimum means I'm getting everything the firm offers."

Entry minimums usually unlock base-tier services only. Estate structuring, NRI tax advisory, AIF access, and family governance typically sit behind higher internal thresholds. Before signing, ask the firm explicitly what the entry minimum covers and what additional minimums or fees unlock each service layer — the answers will tell you more about the firm's structure than any brochure will.

Frequently Asked Questions

What is the minimum investment for wealth management?

Minimums vary widely. Boutique advisors and smaller RIAs in India may begin from ₹25–50 lakh; private bank programmes typically start at ₹50 lakh to ₹2 crore. Full-service HNI and UHNI wealth management generally requires ₹5 crore and above. At iVentures Wealth, minimums start at ₹5 Cr for NRIs/OCIs, ₹10 Cr for CXOs and professionals, and ₹50 Cr for corporates. The right threshold depends on the complexity of your needs, not just the size of your corpus.

Which is better, CFA or CWM?

The CFA (Chartered Financial Analyst) is more rigorous and globally respected, covering investment analysis, portfolio management, and financial markets. The CWM (Chartered Wealth Manager) is more narrowly focused on wealth advisory. For investors, a CFA-credentialed advisor typically signals stronger analytical depth in investment decision-making.

Are wealth management minimums negotiable?

Reputable firms rarely negotiate minimums significantly, because those thresholds reflect genuine service cost economics rather than arbitrary pricing. Some flexibility may exist for high-potential clients—such as a founder pre-liquidity event—but expect any exceptions to be structured carefully, not waived informally.

What is a typical wealth management fee in India?

SEBI caps Investment Adviser fees at 2.5% per annum of AUA or ₹1,51,000 per annum per family (fixed fee mode). In practice, comprehensive wealth management fees typically fall below this ceiling. Fee-only advisors—who charge clients directly with no product commissions—are generally better aligned with client interests than commission-earning distributors.

What happens if my portfolio falls below the firm's minimum after onboarding?

Most firms build in grace periods or communicate formally before taking action on accounts that fall below minimums due to market movements. The specific policy varies by firm. Review the exact terms in your advisory agreement before onboarding—look for the notice period, cure window, and any fee implications.

Do I need wealth management or just a financial advisor?

A financial advisor covers investment and retirement planning for straightforward situations. A wealth manager addresses more complex needs: tax structuring, estate planning, business succession, cross-border assets, and alternatives. If your situation involves multiple entities, illiquid holdings, or cross-border obligations, wealth management is the right category.