Most investors assume their bank relationship manager, mutual fund distributor, or insurance agent is working in their best interest. Legally, they are not required to. Commission-driven intermediaries earn trail income from the products they recommend — a structural conflict that rarely gets disclosed.

This guide lists five top SEBI-registered Investment Advisors in India for 2026, explains what makes each one distinct, and gives affluent investors, UHNIs, NRIs, family offices, and corporates a clear framework for choosing the right one.

Key Takeaways

- SEBI RIAs are legally bound to act as fiduciaries — charging clients directly, not earning product commissions

- Only 1,044 entities hold valid SEBI RIA registration against 12+ crore NSE investors; always verify on SEBI's portal before engaging any advisor

- The best RIA matches your financial profile, not just brand recognition

- UHNIs, family offices, and NRIs require advisors with consolidated oversight, tax structuring, and multi-entity capabilities

- iVentures Wealth (Reg. No. INA000019026) is among North India's leading SEBI RIAs — 20+ years of experience, ₹1,146+ Cr in assets under advice

What Is a SEBI-Registered Investment Advisor and Why Does It Matter?

A SEBI-registered Investment Adviser (RIA) is a professional or firm authorised under the SEBI (Investment Advisers) Regulations, 2013 to provide personalised, fee-based investment advice. Under Regulation 2(1)(m) of those regulations, the definition covers any person who, for consideration, provides investment advice to clients.

This is meaningfully different from a mutual fund distributor or bank RM. Distributors earn trail commissions from AMCs — an arrangement the AMFI Master Circular (January 2026) explicitly governs, including restrictions on distributors using titles like "Wealth Adviser" unless they hold a SEBI RIA registration.

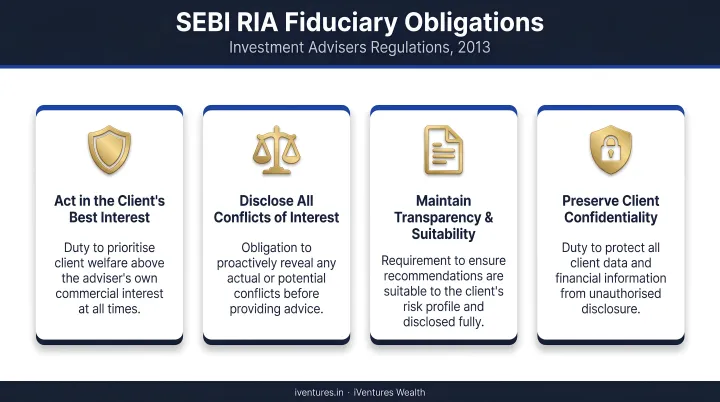

The Fiduciary Distinction

Under Regulation 15(1), a SEBI RIA must act in a fiduciary capacity toward clients and disclose all conflicts of interest. This is a statutory obligation — enforceable under SEBI regulations, not just a marketing claim. The regulations also prohibit RIAs from receiving consideration from any party other than the client on any products they recommend.

What this means in practice:

- Risk profiling is documented (Regulation 16)

- Advice must be suitable for the client (Regulation 17)

- All fees and conflicts must be disclosed in writing (Regulation 18)

- A written client agreement is mandatory before advisory begins

Given that SEBI's own October 2024 board memorandum noted the IA and RA base "was not commensurate with India's investor base" — with just 927 IAs against 12 crore+ unique investors at that time — choosing the right RIA, rather than an unregistered "adviser," carries real financial and legal weight.

Top SEBI-Registered Investment Advisors in India for 2026

These advisors were shortlisted based on SEBI registration validity, depth of services, client segment relevance, and regulatory track record — not AUM size alone. Always verify registration on SEBI's official Investment Adviser list before engaging any firm.

1. iVentures Wealth

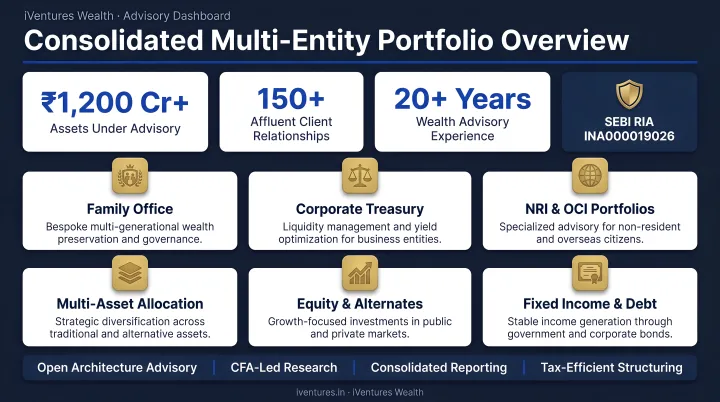

Founded in 2005 and SEBI-registered since 2010, iVentures Wealth (legal entity: I Ventures Capital Private Limited, CIN: U74900DL2009PTC188312) is a Gurugram-based wealth management firm managing ₹1,146+ Cr in assets for 150+ affluent families, UHNIs, NRIs, CEOs/CXOs, and corporates across India.

Leadership includes Nirmal A. Bansal (Founder & Director, former Merrill Lynch professional, UCLA Anderson alumnus) and Krishna Makhariya (Head of Research, CFA charterholder), supported by Executive Directors Rishi Kapur and Nitin Jindal — the latter also serving as Compliance Officer.

What sets iVentures apart:

- Operates as a true fee-only fiduciary — zero commissions, trail income, or kickbacks from product manufacturers

- Consolidated multi-entity portfolio view via the Wealth Monitor App (iOS: 4.7★, Android: 4.2★), covering mutual funds, equities, PMS, AIFs, bonds, FDs, NRE/NRO accounts, and international holdings

- Cross-border NRI/OCI advisory spanning the US, UK, UAE, Singapore, Canada, and Australia — covering DTAA structuring, FEMA compliance, repatriation planning, and LRS-based global investing

- Full-spectrum family office services for families with ₹50 Cr+ investible assets — covering succession planning, estate structuring, governance frameworks, and multi-generational legacy planning

- Product-neutral corporate treasury advisory for corporates, SMEs, trusts, and LLPs with ₹50 Cr+ surplus

- Zero investor complaints on record across FY 2021–22 through FY 2025–26

| Detail | Information |

|---|---|

| SEBI Registration | INA000019026 | Accredited with NSE and CDSL |

| Key Services | Wealth management, family office advisory, equity research, NRI/OCI tax advisory, corporate treasury, Wealth Monitor App |

| Best Suited For | UHNIs, family offices, NRIs/OCIs, CEOs/CXOs, founders, corporates, SMEs, trusts, and women investors in Delhi NCR and beyond |

| Minimum Thresholds | ₹5 Cr (NRIs/OCIs) | ₹10 Cr (CXOs/professionals) | ₹50 Cr (corporates) | ₹100 Cr (family businesses) |

2. Bajaj Capital Investment Advisers

Bajaj Capital has operated in Indian financial services since 1964. Its SEBI-registered investment adviser entity provides regulated, fee-only advisory with documented goal planning, risk profiling, and structured portfolio governance — separate from its broader distribution business.

Key differentiators:

- National footprint with wide client accessibility across India

- Planning-first process with structured periodic reviews

- Clear separation between fee-based advisory and product distribution

| Detail | Information |

|---|---|

| SEBI Registration | Company-disclosed: Bajaj Capital Limited, RIA No. INA100001368. Verify legal entity and current status on SEBI's official IA list before engaging |

| Key Services | Goal-based financial planning, portfolio advisory, asset allocation, periodic reviews and reporting |

| Best Suited For | Salaried families, pre-retirees, and first-time RIA clients seeking hand-holding and a recognised national brand |

3. ET Money Genius

ET Money Genius is a mobile-first investment advisory platform operating under a SEBI-registered Investment Adviser framework. Its operating entity is Banayantree Services Limited. The platform converts personalised advice into immediate action — SIP setup, fund investing, and goal tracking — all within a single app.

Key differentiators:

- Fast, low-friction onboarding that moves from advice to execution in minutes

- Real-time portfolio nudges and structured advisory journey

- Designed for investors who prefer managing wealth on a smartphone

| Detail | Information |

|---|---|

| SEBI Registration | Company-disclosed: Banayantree Services Limited, RIA No. INA100006898, validity Jan. 2017 – Perpetual. Verify on SEBI's official IA list before subscribing |

| Key Services | Personalised financial plans, SIP setup and management, portfolio tracking, advisory via app |

| Best Suited For | Mobile-first salaried professionals, first-time investors, and DIY investors seeking guided goal-based investing |

4. International Money Matters Pvt. Ltd. (IMMPL)

IMMPL is a boutique, planning-first advisory firm with SEBI RIA registration, focused on structured financial plans with a documented investment policy, defined rebalancing triggers, and a structured review schedule.

Key differentiators:

- Policy-driven discipline that reduces ad-hoc portfolio decisions

- Relationship-led advisory with clear accountability on retirement, tax, and income planning

- Appeals to investors who want process and structure over product pitches

| Detail | Information |

|---|---|

| SEBI Registration | Company-disclosed: International Money Matters Pvt. Ltd., RIA No. INA200010676, validity May 2018 – Perpetual. Verify legal entity name and registration on SEBI's official IA list |

| Key Services | Comprehensive financial planning, asset allocation, rebalancing, retirement and tax-aware guidance, portfolio monitoring |

| Best Suited For | Salaried families, pre-retirees, and DIY investors seeking a structured, accountability-driven advisory process |

5. Holistic Investment Planners

Holistic Investment Planners is a relationship-led advisory firm that documents client goals, risk capacity, and asset allocation rules into a written investment policy — then holds portfolios accountable to it through a regular review schedule.

Key differentiators:

- Governance-first approach that keeps portfolios aligned through market cycles

- Measurable progress against documented goals

- Appeals to busy professionals who want discipline over product recommendations

| Detail | Information |

|---|---|

| SEBI Registration | Verify exact legal entity name and registration number directly on SEBI's official IA list before onboarding — no registration number is independently confirmed in this guide |

| Key Services | Financial plan, asset allocation and rebalancing rules, ongoing portfolio monitoring, retirement and tax-aligned guidance |

| Best Suited For | Salaried families, pre-retirees, and hands-on investors seeking process-driven advisory with transparent guardrails |

How to Choose the Right SEBI-Registered Investment Advisor

Step 1: Verify SEBI Registration First

Cross-check the advisor's legal entity name, registration number, validity, and city on SEBI's official Investment Adviser list before committing. If the entity is not listed, do not engage. The registration number should also appear on their website, advisory agreement, and fee document.

Step 2: Assess Fee Model and Conflict of Interest

SEBI RIAs charge clients directly — either a flat/retainer fee or a percentage of assets under advice. Current SEBI guidelines cap the AUA-based fee at 2.5% per annum per client family, with a fixed fee cap of ₹1,51,000 per annum per client family.

Ask explicitly:

- Does the advisor earn any commission, distribution trail, or referral income?

- Is the advisory agreement strictly fee-only?

- Request a written conflict-of-interest declaration before signing

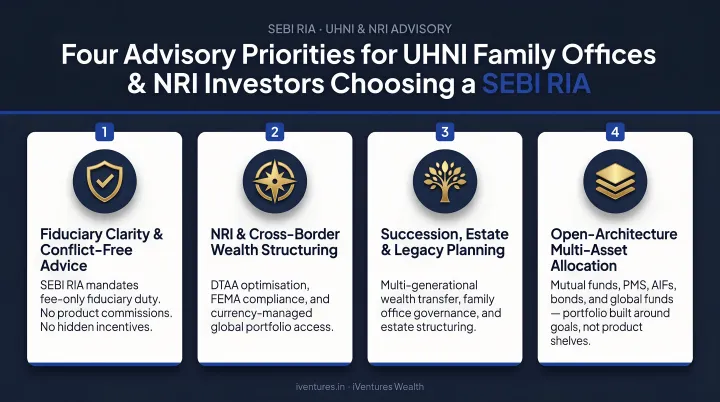

Step 3: Match the Advisor to Your Financial Profile

A firm specialised in UHNI and family office mandates, like iVentures Wealth, has different capabilities than a digital-first platform built for salaried SIP investors. For UHNIs, family offices, NRIs, and corporates, prioritise advisors offering:

- Consolidated multi-entity portfolio oversight

- Tax optimisation and cross-border advisory

- Succession and estate planning

- Personalised portfolio construction — not template-driven plans

Step 4: Demand a Written Investment Policy

Any credible SEBI RIA should document your goals, risk profile, asset allocation rules, and rebalancing thresholds in writing. Ask to see a sample policy, confirm the review frequency, and clarify how the advisor communicates when market conditions or your personal circumstances shift.

Step 5: Conduct a Discovery Call

Before signing, hold a detailed meeting and evaluate the advisor on four fronts:

- Listening: Do they ask detailed questions before offering any recommendations?

- Clarity: Are risk disclosures and fee structures explained plainly, without jargon?

- Transparency: Do they proactively flag conflicts, even when none exist?

- Process: Is there a documented grievance redressal mechanism in place?

If the answer to any of these is unclear after one conversation, keep looking.

How We Selected These Advisors

Each advisor featured here was evaluated against a consistent set of criteria:

- Valid SEBI Investment Adviser registration

- Fee structure clarity and transparency

- Relevance to affluent, HNI, and UHNI investor needs

- Depth of services beyond basic mutual fund allocation

- Regulatory compliance track record

- Client trust indicators — years in operation and assets under advisory

This list is not an exhaustive ranking of all SEBI-registered RIAs in India, nor a guarantee of future performance. It is a curated shortlist to give investors a credible starting point. Conduct your own verification on SEBI's official portal and request advisory agreements before engaging any firm.

SEBI's own board memorandum noted the IA base is not proportionate to India's investor population. With roughly 0.86 RIAs per 100,000 unique NSE investors (calculated from SEBI's 1,044 IA count and NSE's 12.2 crore unique investor figure), verification and careful selection are non-negotiable in 2026.

Conclusion

In a market crowded with commission-driven intermediaries, a SEBI-registered Investment Advisor operating as a true fiduciary — with transparent fees, documented processes, and zero conflict of interest — is the regulatory standard that protects your wealth.

Choosing the right one requires matching their client focus, service depth, and advisory philosophy to your specific financial goals. Brand recognition alone is not a sufficient filter.

Those criteria point toward firms with verified track records, clear fee structures, and a defined client mandate. For UHNIs, affluent families, NRIs, and corporates, that shortlist is short for a reason.

iVentures Wealth (SEBI Reg. No. INA000019026) has operated under that mandate since 2005 — 20+ years of personalised, research-driven advisory across ₹1,146 Cr in assets under advice. Verify their registration on SEBI's portal, then schedule a consultation to see whether their advisory approach fits your financial objectives.

Frequently Asked Questions

What is a SEBI-registered Investment Advisor (RIA)?

A SEBI RIA is a professional or firm registered under the Investment Advisers Regulations, 2013, legally required to act as a fiduciary, charge fees directly from clients, and provide unbiased recommendations. This is structurally different from mutual fund distributors or insurance agents, who earn commissions from product manufacturers.

How can I verify if an investment advisor is SEBI registered?

Visit SEBI's official Investment Adviser list at sebi.gov.in, search by the firm's legal name, and cross-check the registration number, status, city, and validity period. Never rely solely on the advisor's own website — always confirm directly on the portal.

What is the difference between a SEBI RIA and a mutual fund distributor?

A SEBI RIA charges clients a fee and cannot earn commissions from product manufacturers. A mutual fund distributor earns trail commissions from AMCs, creating a structural conflict where product selection may be influenced by commission rates rather than client suitability.

How much does a SEBI-registered Investment Advisor charge?

SEBI caps RIA fees under two models: a percentage of assets under advice (maximum 2.5% per annum per client family) or a fixed/retainer fee (currently capped at ₹1,51,000 per annum per client family). Review the fee disclosure document and advisory agreement before onboarding to understand inclusions and billing cadence.

Can NRIs and OCIs work with a SEBI-registered Investment Advisor in India?

Yes. Under SEBI Regulation 4(i), investment advice provided to Non-Resident Indians or Persons of Indian Origin falls within the IA Regulations. Some RIAs, including iVentures Wealth, specifically serve NRI and OCI clients across cross-border tax planning, DTAA structuring, and repatriation advisory.

What should UHNIs and affluent investors specifically look for in an Investment Advisor?

UHNIs and affluent investors should prioritise advisors who offer consolidated multi-entity portfolio views, family office-level services, personalised asset allocation, and succession and estate advisory. Relationship depth and long-term continuity matter far more than standardised product-driven plans.