Introduction

Most Indian households do the responsible thing: they save. Money goes into a savings account, an FD gets renewed every year, and the balance grows — on paper, at least.

Here's what that savings account statement doesn't show: with India's CPI inflation running at 4.38% year-on-year as of June 2026, and major banks offering just 2.50% per annum on savings deposits, every rupee sitting idle is actually losing purchasing power. You're not saving — you're slowly falling behind.

Closing that gap requires more than discipline — it requires putting money into assets that can outpace inflation over time. That's what investing is for.

This guide covers the core concepts every first-time investor needs: the difference between saving and investing, five foundational principles, India's main asset classes, and a practical framework to get started. By the end, you'll have a clear picture of where to begin and why it matters.

Key Takeaways

- Investing is goal-driven, not speculative — it puts money into assets that grow over time

- Starting a decade earlier can more than triple your final corpus, thanks to compounding

- India's regulated investment landscape spans mutual funds, PPF, NPS, SGBs, and more — each suited to different goals and time horizons

- Tax savings work best as a byproduct of a sound plan, not as the starting point

- A SEBI-registered investment adviser is legally obligated to act in your interest; a distributor is not

Saving vs. Investing: Why the Difference Matters

Saving and investing are both necessary — but they're not interchangeable, and treating them as the same is one of the most expensive mistakes a beginner can make.

Saving means keeping money in liquid, low-risk instruments — savings accounts, fixed deposits, or cash. The goal is capital preservation and quick access, not growth. Use it for money you might need in the next few months.

Investing means putting money into financial assets — equity, mutual funds, bonds, real estate — so their value grows over time and outpaces inflation. It involves accepting some short-term volatility in exchange for higher long-term returns.

Why Inflation Changes the Equation

The real cost of keeping everything in a savings account becomes clear when you look at the numbers. With savings accounts at 2.50% and inflation at 4.38%, the gap compounds against you every year.

Consider ₹1 lakh parked in a savings account versus invested in an equity index tracking the Nifty 50's historical 14.2% CAGR:

| After 10 Years (Nominal) | After 10 Years (Real Purchasing Power) | After 20 Years (Nominal) | After 20 Years (Real Purchasing Power) | |

|---|---|---|---|---|

| Savings Account at 2.50% | ~₹1.28 lakh | ~₹83,400 | ~₹1.64 lakh | ~₹69,600 |

| Nifty 50 TRI at 14.2% CAGR | ~₹3.77 lakh | ~₹2.46 lakh | ~₹14.23 lakh | ~₹6.04 lakh |

Note: Nifty 50 TRI CAGR is historical (June 1999–December 2021), not a forecast. Figures are illustrative.

The savings account doesn't just underperform — after adjusting for inflation, ₹1 lakh today is worth only ₹69,600 in real terms after 20 years of "safe" saving.

Saving vs. Investing at a Glance

| Saving | Investing | |

|---|---|---|

| Risk Level | Very low | Low to high, depending on asset |

| Expected Return | 2.5–7% p.a. | 8–15%+ p.a. over long horizons |

| Time Horizon | Short-term (0–3 years) | Medium to long-term (3+ years) |

| Liquidity | High | Varies (liquid funds to locked-in instruments) |

| Ideal Use | Emergency fund, near-term goals | Retirement, education, wealth creation |

The practical rule: keep 3–6 months of expenses in liquid savings as your emergency cushion. Every rupee beyond that should be invested — earning returns, beating inflation, and building wealth over time.

The Building Blocks of Wealth: 5 Principles Every Beginner Must Know

Principle 1 – The Power of Compounding

Compounding means your returns earn returns. Over long periods, this mathematical reality creates results that far outpace what you'd expect.

A concrete illustration, using a 12% illustrative rate (not a guarantee):

| Monthly SIP | Duration | Amount Contributed | Illustrative Future Value |

|---|---|---|---|

| ₹5,000 | 25 years | ₹15 lakh | ~₹94.88 lakh |

| ₹5,000 | 15 years | ₹9 lakh | ~₹25.22 lakh |

Source: SEBI SIP Calculator. Illustrative only — markets have no fixed return.

Starting 10 years earlier — with the same monthly amount — produces nearly 3.76 times the outcome. The money invested is only ₹6 lakh more, but the corpus difference is roughly ₹70 lakh. That gap is time, not effort.

Principle 2 – Risk and Return Are Linked

Higher potential returns come with higher short-term volatility. A portfolio that returned 40% in one year can fall 30% the next. Neither extreme defines long-term performance.

Your risk tolerance — how much drawdown you can absorb emotionally and financially — shapes which assets belong in your portfolio. Three factors determine this:

- Time horizon: More time means more room to recover from corrections

- Income stability: Predictable income lets you hold through downturns

- Financial obligations: Dependents, EMIs, and near-term commitments reduce your capacity to take risk

Principle 3 – Diversification Reduces Concentration Risk

No single asset class performs well in all market conditions. Equity outperforms during growth cycles; gold holds up during uncertainty; debt provides stability when equity corrects.

A well-diversified portfolio spreads across:

- Asset classes: Equity + debt + gold + real estate

- Within equity: Large-cap + mid-cap + sector funds

- Geographies: Domestic + international funds

When one asset underperforms, others often compensate. Diversification doesn't guarantee gains, but it limits the damage from any single bad bet.

Principle 4 – Time Horizon Determines Strategy

Match your instruments to your goal's timeline:

- Short-term (under 3 years): Capital protection is the priority. Use liquid funds, short-duration debt, or FDs.

- Medium-term (3–7 years): Hybrid funds or balanced allocation that blends growth with stability.

- Long-term (7+ years): Equity-heavy portfolios can absorb volatility and earn meaningful real returns over time.

Putting your home purchase down payment into equity funds because you expect higher returns — then needing that money in a market correction — is a mistake that time horizon discipline prevents.

Principle 5 – Rupee Cost Averaging via SIP

A Systematic Investment Plan (SIP) invests a fixed sum every month, regardless of market levels. When markets fall, the same ₹5,000 buys more units. When markets rise, existing units appreciate.

Accumulating more units during low NAV (unit price) periods and fewer during high NAV periods reduces your average cost over time — and removes the need to time the market. For salaried investors and beginners, SIPs are simply the most practical way to start.

Where to Invest: Key Options for Indian Beginners

Mutual Funds and SIPs

Mutual funds pool money from many investors and deploy it across securities managed by professional fund managers. For beginners, this is typically the most sensible starting point.

Main categories to know:

- Equity funds: For long-term wealth creation (7+ year horizon)

- Debt funds: For stability and medium-term goals

- Hybrid funds: Balanced exposure for moderate risk profiles

SIPs can start with as little as ₹500 per month. As of June 2026, Indians collectively invest ₹31,781 crore monthly through SIPs — a figure that reflects how mainstream this entry point has become.

Direct Equity (Stocks)

Buying individual company shares offers direct ownership and higher return potential — but requires more knowledge than mutual funds. Beginners who want equity exposure without doing the research themselves are better served by funds first.

If you do pursue direct equity:

- Stick to large-cap, blue-chip companies initially

- Build foundational knowledge of financial statements and market cycles before expanding to mid or small caps

- Treat it as one part of a broader portfolio, not a standalone strategy

Once you're comfortable with market-linked products, it's worth balancing them against instruments that carry no market risk at all.

Government-Backed Instruments (PPF, NPS, SGBs)

Three options worth knowing for risk-averse or tax-conscious investors:

- PPF: 15-year lock-in, 7.1% p.a. interest, EEE tax status (exempt at investment, accumulation, and withdrawal), government-backed

- NPS: Retirement-focused pension scheme; contributions qualify for an additional deduction of up to ₹50,000 under Section 80CCD(1B) beyond the standard 80C limit

- Sovereign Gold Bonds: Government-backed gold exposure paying 2.50% annual interest on the nominal value, with an 8-year tenure; capital gains on redemption are tax-exempt for individuals

Tax-Efficient Investing (ELSS and Section 80C)

ELSS (Equity Linked Savings Scheme) mutual funds invest predominantly in equity and qualify for Section 80C deductions up to ₹1.5 lakh per year under the old tax regime. They carry the shortest lock-in period among all 80C instruments — just 3 years.

Tax-saving should be a by-product of a well-structured plan, not the plan itself. For context, other 80C instruments carry longer lock-ins and less flexibility: PPF locks in for 15 years, NPS runs to retirement, and ULIPs bundle insurance with investment in ways that often reduce overall returns.

Real Estate and Alternative Investments

Traditional real estate requires significant capital, carries illiquidity, and involves transaction costs that erode returns. REITs (Real Estate Investment Trusts) offer an accessible alternative — SEBI has reduced the minimum REIT application amount to ₹10,000–₹15,000, with trading in single units. Five REITs are currently exchange-listed: Embassy, Mindspace, Brookfield India, Nexus Select, and Knowledge Realty.

For those who eventually outgrow standard retail products, AIFs and PMS offer more actively managed or bespoke strategies — typically suited to larger capital bases as wealth grows.

How to Begin Your Investment Journey: A Step-by-Step Approach

Set Your Financial Foundation First

Before putting a single rupee into the market, three things need to be in place:

- A budget and short-term financial plan — you need to know how much you can genuinely invest without dipping into it

- An emergency fund — 3–6 months of expenses in a liquid account, untouched

- High-interest debt cleared — credit cards and personal loans charging 18–36% annually will erase any investment return; eliminate these first

Skipping these steps doesn't just leave you financially vulnerable. It forces premature redemptions when markets fall, locking in losses at exactly the wrong time.

Define Your Goals, Risk Profile, and Time Horizon

Map your goals to timelines before selecting instruments:

- Retirement: 20–30 years — equity-heavy, growth-oriented

- Children's education: 10–15 years — diversified equity with some debt as the date approaches

- Home purchase: 5–7 years — balanced to conservative allocation

- Short-term targets: 1–3 years — liquid and short-duration debt instruments

Once goals are mapped, the appropriate asset allocation follows logically from the timeline and your risk tolerance. This is where working with a SEBI-registered investment adviser — such as iVentures Wealth (SEBI RIA registration INA000019026) — makes a measurable difference. A fiduciary adviser calibrates your allocation to your actual income, liabilities, tax situation, and life stage — not a generic template that fits no one precisely.

Start Small, Stay Consistent, and Review Annually

With goals defined, the next step is simply to begin. The first investment doesn't need to be large — starting early matters far more than starting big, because time is the variable that compounds everything else.

Practical starting framework:

- Long-term goals: SIP in a diversified equity mutual fund

- Near-term goals: Liquid fund or short-duration debt fund

- Tax-saving (if using old regime): ELSS with 3-year lock-in

Review your portfolio at least once a year. Check whether your allocation still matches your goals, rebalance if equity has grown to dominate, and adjust for life changes — a new job, a child, an approaching goal date.

Mistakes Beginners Make and How to Avoid Them

Chasing Past Performance

One of the most reliable patterns in investing: last year's top performer rarely repeats. JM Basic Fund illustrates this clearly — it was the best performer in its peer group in 2007, returning 111.44% against a category average of 59.56%. The following year, it fell -75.71% when the category dropped 55.51% on average. Investors who piled in after the 2007 result bore the full weight of that reversal.

Past returns inform history. They don't predict future performance, and SEBI explicitly states this in its regulatory materials.

Letting Emotions Drive Decisions

Two behavioural traps catch most beginners:

- Panic-selling: Redeeming investments during a market correction locks in losses and misses the recovery

- FOMO-driven buying: Chasing rallies at market peaks concentrates risk at exactly the wrong time

The SEBI Investor Survey 2025 found that among dormant investors, 87% cited poor performance and 75% cited external influences as reasons for stopping — patterns consistent with emotional decision-making rather than strategic exits.

Both traps share a fix: a written investment plan with defined goals, timelines, and asset allocation. Automatic SIPs enforce discipline precisely when emotions argue otherwise.

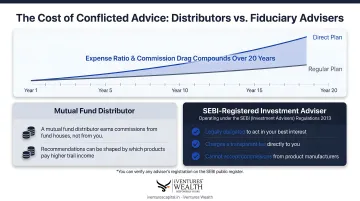

Ignoring Costs and the Advisor Conflict-of-Interest Problem

Expense ratios and distributor commissions compound against you just as returns compound for you. The difference between a direct plan and a regular plan's expense ratio may seem small annually — but over 20 years, it can meaningfully reduce your final corpus.

More consequentially: a mutual fund distributor earns commissions from fund houses, not from you. Their recommendations can be shaped by which products pay higher trail income.

A SEBI-registered investment adviser, operating under the SEBI (Investment Advisers) Regulations 2013, is held to a different standard:

- Legally obligated to act in your best interest

- Charges a transparent fee directly to you

- Cannot accept commissions from product manufacturers

You can verify any adviser's registration on the SEBI public register.

Frequently Asked Questions

How should beginners start investing?

Build an emergency fund first and clear high-interest debt. Then define one goal with a timeline and start a SIP in a diversified equity mutual fund if the horizon is 7+ years. Starting small and early consistently outperforms waiting to invest a larger amount later.

What is the 3-5-7 rule in investing?

It's a thumb rule for minimum holding periods: hold debt or balanced funds for at least 3 years, diversified equity funds for at least 5 years, and mid/small-cap strategies for at least 7 years. These timeframes give each asset class enough time to work through market cycles.

How much money do I need to start investing in India?

SIPs can begin with as little as ₹500 per month, making equity investing accessible at virtually any income level. Consistency over time matters far more than the size of your first contribution.

What is the difference between a mutual fund distributor and a SEBI-registered investment adviser?

A distributor earns commissions from fund houses, which can create conflicts in what they recommend. A SEBI-registered investment adviser (RIA) charges a transparent fee, accepts no product commissions, and is legally bound to act in your best interest.

Is it better to invest in SIPs or lump sum as a beginner?

SIPs are generally better for beginners — they remove the need to time the market, build investing discipline, and use rupee cost averaging to smooth entry points. Lump sum investments can make sense when markets have corrected significantly and the investor has a long time horizon.

How do I assess my risk tolerance before investing?

Consider how long the money can stay invested, how you would respond to a 20–30% portfolio drop, and your current income stability. A risk profiling tool or a conversation with a registered adviser can help clarify where you stand.