Introduction

Most Indians use "pension" and "annuity" interchangeably — they shouldn't. These two instruments sit at opposite ends of the retirement journey: one builds your corpus over decades, the other converts it into income at retirement. Conflating them leads to poor decisions: either locking capital unnecessarily in low-yield products or arriving at retirement without a plan to generate steady income.

The stakes are real. According to India's SRS Abridged Life Tables 2018-2022, a 60-year-old Indian can expect to live another 18.1 years on average — and many will outlive that. Meanwhile, traditional defined-benefit pensions have largely disappeared for private-sector employees, placing the entire burden of retirement income planning on individuals.

Whether you're a corporate executive with NPS contributions, a founder building wealth outside your business, or an NRI planning a return to India — the decisions you make about these two instruments will shape your retirement income for decades. This article breaks down how annuities and pension plans differ in structure, tax treatment, and purpose, and how to use them together as part of a coherent retirement strategy.

Key Takeaways

- A pension plan (NPS, EPF) accumulates your corpus during working years; an annuity converts that corpus into guaranteed income at retirement.

- NPS offers tax deductions under Sections 80C, 80CCD(1B), and 80CCD(2); annuity payouts are fully taxable as income.

- NPS mandates that at least 40% of the corpus be used to purchase an annuity at exit — the two instruments are complementary, not competing.

- Self-employed professionals and founders should prioritise building a corpus early and plan annuity purchase deliberately at retirement.

- The strongest retirement strategies in India combine NPS for tax-advantaged accumulation, annuities for guaranteed income, and a diversified growth portfolio.

What Is an Annuity?

An annuity is a contract with a life insurance company. You pay a lump sum; the insurer pays you back as periodic income — monthly, quarterly, or annually — either for life or a fixed term. Unlike most investment products, the income continues regardless of how long you live, which is the core value proposition.

Types of Annuities Available in India

Indian insurers offer several variants, each suited to different needs:

- Immediate annuity — payments begin within one year of purchase (e.g., LIC Jeevan Akshay VII, a non-linked, non-participating immediate annuity plan)

- Deferred annuity — accumulation phase first, then payouts begin at a future date (e.g., HDFC Life Pension Guaranteed Plan)

- Annuity with return of purchase price — the original corpus is returned to your nominee upon death

- Joint life annuity — income continues to your spouse after your death

- Single life annuity without return of purchase price — the highest payout rate, but no residual value for heirs

The right variant depends on your family situation, whether you have other assets for heirs, and how much you need to maximise monthly income.

Tax Treatment of Annuity Income

This is where most people get surprised. Annuity payouts in India are treated as "income from other sources" and taxed at your applicable slab rate — there is no exemption, even if the annuity was purchased with post-tax funds.

Someone in the 30% bracket receiving ₹1 lakh per month from an annuity takes home roughly ₹70,000 after tax. That gap makes product selection and income structuring just as important as the headline payout rate.

Who Should Consider Annuities?

Annuities are most relevant for:

- Retirees with an existing corpus looking to convert it into predictable, guaranteed income

- Self-employed professionals and business owners without employer pension contributions who need to build their own income floor

- Investors prioritising capital safety over growth, wanting to eliminate market risk from part of their retirement income

- NPS subscribers, who are already required to deploy at least 40% of their corpus into an annuity at exit — the choice isn't whether to buy one, but which variant to select

What Is a Pension Plan?

In India, "pension plan" covers three distinct categories — insurers often market ULIPs as "pension plans," which creates genuine confusion.

The Three Categories

1. Government-mandated schemes

- EPF (Employees' Provident Fund) — statutory accumulation for organised-sector employees; the Central Board of Trustees recommended 8.25% interest for FY 2025-26, per PIB

- EPS (Employees' Pension Scheme) — formula-based monthly pension under EPFO; pensionable salary is capped at ₹15,000, limiting the EPS benefit for most middle and senior-income earners

2. National Pension System (NPS) Regulated by PFRDA, NPS is the most relevant accumulation vehicle for both salaried and self-employed individuals. As of June 2026, NPS had 2.23 crore subscribers and ₹16,77,514 crore in AUM — figures that place it among the largest regulated retirement vehicles in the country.

3. Employer superannuation funds Defined-contribution schemes offered by some large corporates; treated separately from NPS under the Income Tax Act.

How NPS Works

Contributions go into Tier I accounts (tax-advantaged, locked until age 60) and are invested across three asset classes: equity (Scheme E), corporate bonds (Scheme C), and government securities (Scheme G). You choose the allocation — either actively or through auto-choice lifecycle funds.

At normal exit (age 60 or superannuation):

- Up to 60% of the corpus can be withdrawn as a tax-free lump sum under Section 10(12A)

- At least 40% must be used to purchase an annuity, provided the corpus exceeds ₹8 lakh

- The annuity income from that 40% is taxable under Section 80CCD(3)

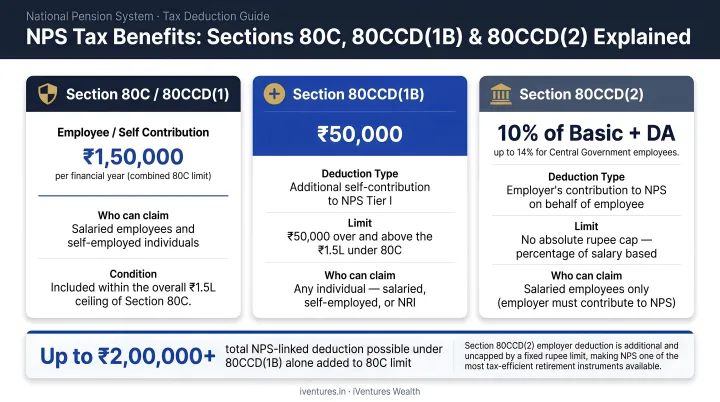

Tax Benefits — The Real Competitive Advantage

NPS's edge over most other instruments lies in its stacked tax benefits:

| Section | Benefit | Limit |

|---|---|---|

| 80C / 80CCE | Self-contribution deduction | Up to ₹1.5 lakh combined |

| 80CCD(1B) | Additional NPS-specific deduction | Additional ₹50,000 |

| 80CCD(2) | Employer contribution | Up to 10% of salary (old regime), 14% (new regime) |

The Section 80CCD(2) benefit is especially valuable for CXO-level executives. Unlike other deductions, the employer contribution under this section has no ₹1.5 lakh ceiling — iVentures Wealth includes NPS contribution structuring in salary optimisation advisory for corporate clients precisely because of this uncapped deduction.

Who Should Consider Pension Plans?

- Salaried professionals in their 30s and 40s who can compound NPS contributions over decades while claiming annual tax deductions

- Corporate executives whose employers offer matching NPS contributions under Section 80CCD(2) — this is essentially free additional retirement savings

- Self-employed professionals who want a disciplined, tax-advantaged accumulation vehicle (NPS Tier I is available to self-employed individuals)

- NRIs and OCIs — OCI cardholders can subscribe to NPS on par with NRIs, with exit proceeds repatriated via NRO/NRE accounts under FEMA rules

Annuities vs. Pension Plans: Quick Comparison

| Dimension | Pension Plan (NPS/EPF) | Annuity |

|---|---|---|

| Purpose | Accumulate corpus during working years | Convert corpus into periodic income |

| When used | Throughout career | At or after retirement |

| Tax benefits | Deductions during accumulation (80C, 80CCD) | None — payouts fully taxable |

| Payout | Lump sum + mandatory annuity at exit | Periodic income directly |

| Flexibility | Rigid lock-in (NPS Tier I until 60) | Product-level options (immediate, deferred, joint life, ROP) |

| Risk | Market-linked during NPS accumulation | Fixed/guaranteed payouts |

| Death benefit | Nominee receives corpus | Depends on annuity type selected |

| Regulator | PFRDA (NPS), EPFO (EPF/EPS) | IRDAI |

For NPS subscribers, annuities are not an alternative to a pension plan — they are the final step within it. At exit, the mandatory 40% annuitisation means every NPS subscriber will purchase an annuity. The decision isn't whether to buy an annuity; it's which type to buy and from which insurer.

One more distinction worth flagging: products marketed as "pension plans" by life insurers — often ULIP-type savings vehicles — are structurally different from NPS or EPF. They may offer deferred annuity features, but typically lack the tax efficiency and regulatory oversight of NPS. When evaluating retirement income options, treat insurer pension plans as a separate category rather than a like-for-like substitute.

Which One Fits Your Retirement Strategy?

The right answer depends on where you are in your career and what you need from your retirement income.

Prioritise NPS/Pension Accumulation If You Are:

- In your 30s or 40s with significant taxable income to shelter

- A corporate executive whose employer offers NPS matching under 80CCD(2)

- A self-employed professional who wants disciplined, tax-advantaged compounding

- A government employee whose retirement corpus is still building

The compounding effect over 20-30 years, combined with annual tax savings, is difficult to replicate with any other instrument.

Prioritise Annuity Purchase If You Are:

- Approaching or at retirement with an existing corpus

- Self-employed without employer NPS benefit, needing an income floor immediately

- Someone who cannot afford any market risk on the portion of savings covering essential expenses

- An NPS subscriber selecting among annuity products for the mandatory 40% at exit

The Optimal Combined Strategy

Most retirees don't face a binary choice. The strongest framework:

- Accumulation phase — contribute to NPS throughout your working years, maximising 80CCD(1B) and, if applicable, 80CCD(2)

- At exit (age 60) — deploy the mandatory 40% into the best-fit annuity (comparing joint life options, return of purchase price variants, and payout rates across LIC, HDFC Life, SBI Life, and others)

- Remaining 60% withdrawal — invest in a diversified, growth-oriented portfolio for liquidity, inflation protection, and legacy

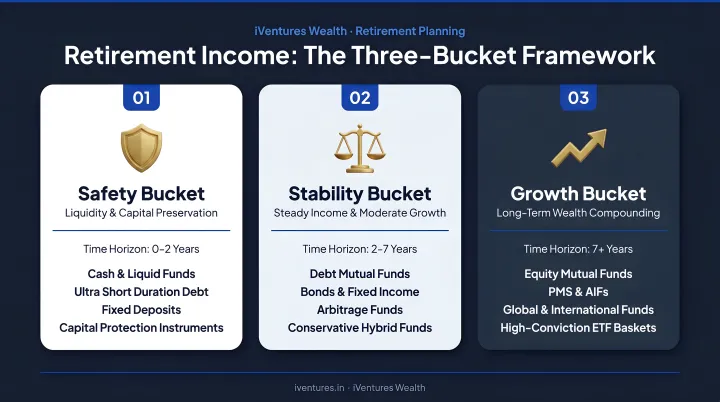

iVentures Wealth's three-bucket framework organises this around three horizons:

- Safety — 5-7 years of expenses in high-quality fixed income

- Stability — a balanced portfolio over an 8-15 year horizon

- Growth — select AIFs, PMS, and private equity

Annuity income covers the Safety bucket; the remaining NPS withdrawal funds Stability and Growth.

For founders, business owners, and self-employed professionals without employer NPS, the approach shifts. iVentures structures multi-asset passive income portfolios combining dividend-paying equities, bond ladders, REITs/InvITs, and private credit AIFs that generate consistent monthly cash flows.

One documented case delivered approximately ₹7.5 lakh per month in passive income while the underlying corpus continued to grow.

Deciding how to split a retirement corpus between an annuity, NPS withdrawal, and a market-linked portfolio requires analysis of your income needs, tax bracket, longevity assumptions, and family obligations. iVentures Wealth's SEBI-registered advisors provide commission-free, fiduciary-grade retirement structuring for UHNIs, founders, and CXOs who need a plan built to last.

Conclusion

Pension plans and annuities aren't competitors. They serve different phases of the same journey — one builds your corpus, the other pays it out. The strongest Indian retirement strategies use both — sequenced around tax efficiency, guaranteed income, and legacy goals specific to your situation.

For affluent professionals managing significant wealth, the real risks are twofold: outliving your savings, and structuring wealth in ways that leave tax benefits unclaimed or lock capital in instruments that don't serve your actual needs.

Your income timeline, tax bracket, family structure, and longevity expectations are yours alone. The retirement plan you build should reflect that — not a template designed for someone else.

Frequently Asked Questions

What is an annuity and what role does it play in retirement planning?

An annuity is an insurance contract that converts a lump sum into guaranteed periodic income for life or a fixed term. In retirement, it eliminates longevity risk — income continues regardless of how long you live, transferring that uncertainty from you to the insurer.

What is the 4% rule in retirement planning?

From William Bengen's 1994 research, the 4% rule suggests retirees can withdraw 4% of their corpus annually without exhausting funds over 30 years. It doesn't apply directly in India — local research points to a safer 3% withdrawal rate, given higher inflation, different tax structures, and instruments like NPS and annuities.

What are the 7 stages of retirement planning?

The typical stages are: goal setting, assessing current savings, calculating retirement corpus, choosing investment vehicles, pre-retirement restructuring, distribution planning, and legacy planning. Annuities and pension plans are most directly relevant in stages four through six.

Can I have both a pension plan (NPS) and an annuity?

For most NPS subscribers, it's mandatory. PFRDA rules require at least 40% of the NPS corpus (where it exceeds ₹8 lakh) to be used to purchase an annuity at exit. The two are part of the same structure — not separate choices.

Is annuity income taxable in India?

Yes. Annuity payouts are fully taxable as "income from other sources" at your applicable slab rate, regardless of whether the annuity was purchased with pre-tax or post-tax funds. Tax planning around annuity income — especially for those in higher brackets — is an important part of retirement structuring.

Which is better for NRIs — an annuity or a pension plan?

NRIs and OCI cardholders can invest in NPS (exit proceeds go to NRO/NRE accounts under FEMA) and purchase annuity products from Indian insurers. The right choice depends on intended retirement location, tax residency status, and applicable DTAA provisions — professional advice is recommended before committing.