Introduction

India now has over 19,000 ultra high net worth households — and that number doubled in the last decade alone. A growing cohort of founders post-exit, promoters with listed equity, and senior executives with substantial ESOPs have crossed a threshold where generic portfolio advice simply stops working. Their needs aren't just bigger — they're structurally different.

Managing ₹5 crore in a well-diversified mutual fund portfolio and managing ₹100 crore across trusts, business entities, NRI accounts, and private equity are not the same discipline. The first is investment management. The second is something else.

Most advisors use the same label. What they deliver — and who they're actually accountable to — is a different matter.

Key Takeaways

- Global UHNW threshold: ₹250 Cr+ in net worth (or US$30M+) — definitions vary by institution and are not interchangeable

- UHNW wealth management spans estate planning, tax structuring, succession, philanthropy, and family office services — far beyond investments alone

- A fiduciary advisor acts in your interest; a distributor earns commissions — know which one you're working with

- India's UHNI population is growing fast, making SEBI-regulated advisory more critical than ever

- Choosing the right partner means verifying SEBI RIA registration, fee transparency, and depth of services

Who Qualifies as Ultra High Net Worth?

The Global Definition

The threshold most institutions use is US$30 million, though the asset basis varies:

| Institution | Threshold | Asset Basis |

|---|---|---|

| Capgemini (World Wealth Report 2024) | US$30M+ | Investable assets |

| Fidelity | US$30M+ | Investable assets |

| Knight Frank (Wealth Report 2024) | US$30M+ | Net worth |

| Altrata / Wealth-X | US$30M+ | Net worth |

The difference between these two measures is consequential. Investable assets exclude the primary residence, illiquid business equity, and personal property — net worth includes everything. A founder with a ₹200 crore stake in an unlisted company and a ₹5 crore liquid portfolio has substantial net worth but limited investable assets, which shapes their advisory needs entirely.

India's UHNI Population

According to the Knight Frank Wealth Report 2024, India had 13,263 UHNWIs in 2023, up 6.1% from 2022, with projections reaching 19,908 by 2028 — a 50.1% increase.

Kotak Private's Top of the Pyramid 2024 uses a broader definition, estimating 283,000 Ultra-HNIs across India with combined net worth of ₹232 trillion, forecast to reach 430,000 by 2028.

These two figures measure different cohorts — but both point in the same direction: India's ultra-wealthy segment is expanding at a pace that demands specialized advisory infrastructure.

Where UHNW Wealth Comes From

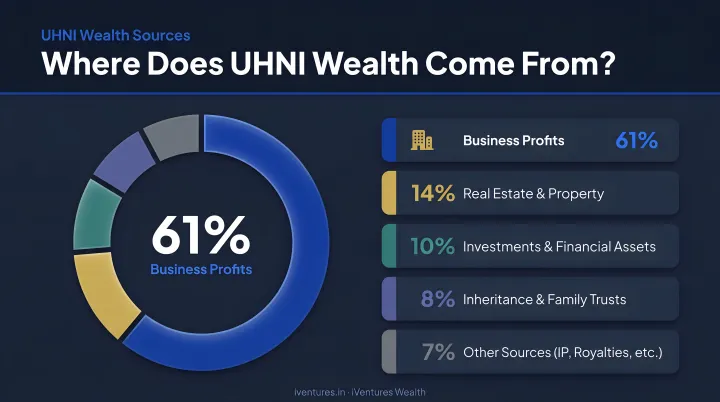

The Kotak Private 2024 survey of 150 Ultra-HNIs found that wealth origins break down as follows:

- 61% — profits from business operations

- 14% — sale of a primary business

- 13% — investments

- 5% — salary income

- 3% — inheritance

- 2% — real estate

The source of wealth directly shapes advisory priorities. A first-generation entrepreneur with concentrated promoter equity faces liquidity risk, succession complexity, and tax exposure at exit — none of which apply to a second-generation inheritor sitting on diversified family assets. Sound advisory starts by recognising this difference, not flattening it.

What Is UHNW Wealth Management?

Beyond Portfolio Management

UHNW wealth management is a comprehensive discipline — encompassing investment management, tax structuring, estate planning, succession, philanthropy, and family governance. What separates it from standard HNI advisory is complexity, not portfolio size.

A typical UHNW client might have:

- Multiple business entities and operating companies

- Assets across several jurisdictions

- Family members with different residency statuses

- Concentrated equity positions in listed or unlisted companies

- Succession decisions that affect both personal and business wealth

No single advisor can manage all of this in isolation. Effective UHNW wealth management requires a coordinated team — investment advisors, tax specialists, estate attorneys, and succession planners — working from a unified strategy.

The Fiduciary Standard

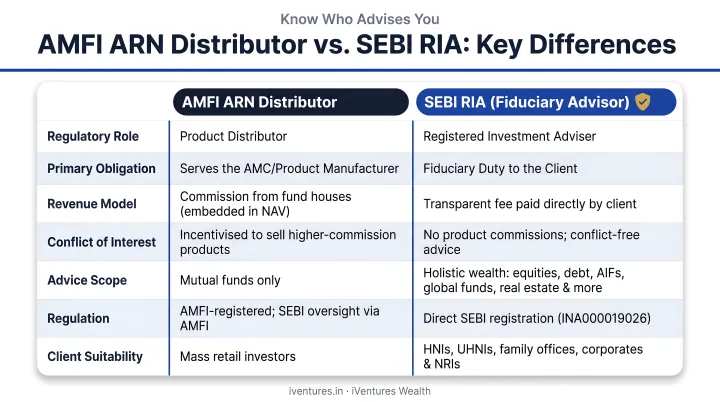

The word "advisor" is used loosely in Indian financial services. It covers mutual fund distributors, bank relationship managers, insurance agents, and SEBI-registered Investment Advisers — groups with very different obligations.

A fiduciary is legally required to act in the client's best interest at all times. As the CFA Institute's position on fiduciary duty makes clear, this is a higher standard than suitability — which only requires that a product not be unsuitable, not that it be the best option available.

Under SEBI's Investment Advisers Regulations 2013, registered Investment Advisers are prohibited from accepting commissions, trail income, or placement fees from product manufacturers. They are paid by the client — which means their recommendations are structurally aligned with client outcomes, not product sales.

At the UHNW level, the stakes of biased advice are concrete. Trail commission on a ₹50 crore allocation — even at 0.5% annually — compounds into crores of value quietly redirected away from the client over a decade. A fiduciary structure removes that conflict by design, not by declaration.

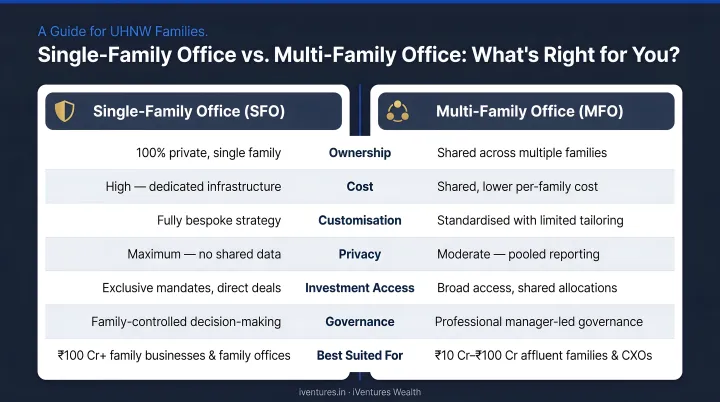

Single-Family Office vs. Multi-Family Office

The most comprehensive structure in UHNW wealth management is the family office — a dedicated setup that handles investments, succession, governance, philanthropy, and often lifestyle management for one family or a group of families.

According to the EY Indian Family Office Playbook 2025, Indian family offices grew from just 45 in 2018 to around 300 by 2024 — a reflection of how quickly UHNW complexity is outpacing standard advisory.

Two models exist:

- Single-Family Office (SFO): Dedicated team and infrastructure for one family. High control, high cost. Suited for families with ₹500 crore+ in investable assets.

- Multi-Family Office (MFO): Shared professional platform serving multiple families. Lower fixed costs, strong expertise. Suited for families in the ₹50–500 crore range.

iVentures Wealth operates as an MFO for UHNI families, providing family-office-level services — investment management, succession, governance, philanthropy, and consolidated reporting — under one coordinated mandate.

Core Services in UHNW Wealth Management

Investment Management

UHNW portfolios require access beyond traditional equity and fixed income. According to the Capgemini World Wealth Report 2024, HNWI alternative allocations rose to 15% globally. Preqin's 2024 data on family office allocations shows planned positions of 22% in private equity, 12% in real estate, and 4% in hedge funds.

For Indian UHNIs, the AIF market has scaled accordingly. SEBI data shows AIF investments crossed ₹4 trillion by March 2024. iVentures Wealth provides access to Category I, II, and III AIFs, private credit (typically 13–16% gross yield through senior secured structures), PMS, pre-IPO allocations, real estate investments, and global funds.

The Wealth Monitor App, iVentures' proprietary platform, gives clients a consolidated, real-time view of their entire portfolio across asset classes, entities, and family members. For a UHNI managing wealth across an HUF, individual accounts, and a trust, this unified visibility is operationally essential.

Estate and Succession Planning

The Kotak Private 2024 report found that approximately 2 in 3 Ultra-HNIs consider a concrete succession plan critical. EY estimates US$1.5 trillion in Indian wealth transfer will occur over the next decade. Nominees are custodians, not legal heirs — a distinction frequently overlooked when setting up nominations. Aligning nominations with the overall estate plan is a foundational step that many families miss.

Effective succession planning draws on several coordinated tools:

- Private trusts to hold key business and property assets

- Wills drafted with documented distribution intent

- Family constitutions that define governance across generations

- Properly structured nomination frameworks aligned with the estate plan

iVentures works with senior legal experts, including Supreme Court-level practitioners, to draft and execute wills. Private trusts are structured to hold key business and property assets with documented succession intent and clear distribution rules for beneficiaries.

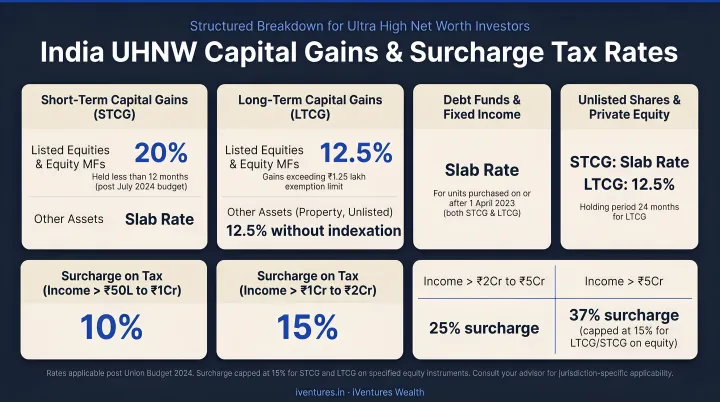

Tax Planning and Optimization

Tax considerations at the UHNW level span multiple income sources and require year-round attention — not just filing compliance. Key current rates include:

- STCG on specified listed securities: 20% (for transfers on or after July 23, 2024)

- LTCG on specified gains: 12.5% without indexation, on gains exceeding ₹1.25 lakh

- Surcharge in the old regime: up to 37% for income above ₹5 crore (capped at 25% under the new regime; note the surcharge does not apply to capital gains under sections 111A, 112, and 112A, where the cap is 15%)

For UHNIs with multiple income streams — business dividends, rental income, investment gains — proactive structuring around these rates can have material impact.

Risk Management and Asset Protection

UHNW risk extends well beyond market volatility. Common exposures include:

- Concentrated promoter or founder stock positions

- Business succession risk tied to a single key person

- Inadequate insurance coverage relative to asset base

- Cybersecurity exposure in digitally managed family wealth

At iVentures, UHNI mandates specifically include concentrated single-stock diversification — executing structured de-risking out of over-concentrated positions over multi-year glide paths, rather than forcing abrupt sales that trigger unnecessary tax events.

Philanthropy and Legacy Planning

An increasing number of UHNIs are moving beyond wealth accumulation toward structured giving. Philanthropy, when planned properly, can be both values-aligned and tax-efficient through charitable trusts, donor-advised structures, or family foundations.

iVentures integrates philanthropy strategy into its family office services, helping clients define giving goals, structure appropriate vehicles, and ensure their generosity achieves measurable, intended outcomes.

The Unique Financial Needs of UHNIs in India

Founders and Promoters: Concentrated Wealth, Complex Needs

India's UHNI population is predominantly first-generation wealth creators. That 61% figure from Kotak — profits from business — reflects a founder class whose wealth is often concentrated in one company, with limited liquid diversification.

The risks this creates are specific and serious:

- Illiquidity: Paper wealth cannot fund lifestyle or succession without planning

- Concentration: A single bad quarter or regulatory event can destroy years of value

- Post-exit complexity: Converting ₹100 crore from a business sale into a structured, multigenerational capital plan requires more than a mutual fund account

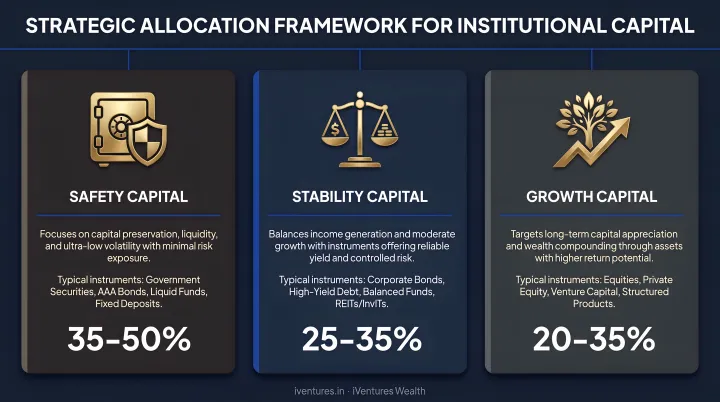

iVentures has worked directly with promoters in this position. One documented example: a first-generation promoter received over ₹100 crore from a business exit across multiple bank tranches, with no deployment framework in place.

iVentures structured the corpus into three buckets — Safety (high-quality fixed income covering 5–7 years of expenses), Stability (an asset-allocated portfolio for an 8–15 year horizon), and Growth (select AIF, PMS, and private equity). A family trust was established to ring-fence the corpus and formalize distribution rules for the spouse and children.

NRIs and Cross-Border Considerations

NRIs with India-linked assets face a distinct layer of complexity that resident Indians don't encounter. Key considerations include:

- NRE/FCNR accounts: Principal and interest are freely repatriable per RBI FAQs

- NRO repatriation: Generally capped at US$1 million per financial year, subject to conditions per RBI Master Circular

- DTAA benefits: Available under sections 90/90A where a treaty exists, applying whichever provision is more beneficial

iVentures advises NRI and OCI clients across US, UK, UAE, Singapore, Canada, and Australia residency situations. This includes DTAA structuring, TDS planning on NRO income, Form 15CA/15CB compliance, and GIFT City structures for USD-denominated wealth management.

The Regulatory Landscape

As of June 2026, the SEBI Investment Adviser register contained 1,039 registered IAs. That is a small number relative to India's wealth management industry, and it's the clearest indicator of how rare genuine fiduciary advisory remains.

The distinction matters:

| Registration | What It Allows | Conflict Risk |

|---|---|---|

| AMFI ARN | Mutual fund distribution; earns trail commissions | Yes — product shelf influences recommendations |

| SEBI RIA | Fee-only investment advice under fiduciary obligation | No — prohibited from earning product commissions |

These are not interchangeable. A bank's wealth management arm typically operates under the distribution model, meaning product recommendations can be shaped by internal shelf arrangements.

iVentures Wealth holds SEBI RIA registration INA000019026, operating as a fee-only advisor prohibited from earning commissions on the products it recommends.

How to Choose the Right UHNW Wealth Management Partner

Evaluate Credentials and Regulatory Standing

Start with basics that are verifiable on public registries:

- Confirm SEBI RIA registration — not just ARN distributor status. Check the SEBI register at sebi.gov.in

- Verify qualifications — CFA, CFP, or equivalent credentials indicate investment expertise grounded in recognized standards

- Review AUM and track record — years in operation and assets under management signal institutional credibility

- Check for regulatory violations — SEBI's public database includes disciplinary history

iVentures Wealth was founded in 2005 and has been SEBI-registered since 2010. The firm is led by a CFA-chartered research team with 20+ years of experience, manages ₹1,200+ crore in assets, and serves 150+ UHNI families, CEOs, and founders.

Assess Depth of Services and Personalization

A UHNW advisor should offer more than portfolio management. Evaluate whether the firm provides:

- Investment management across traditional and alternative asset classes

- Tax planning and optimization (not just compliance)

- Estate, succession, and trust structuring

- Family governance and next-generation planning

- Consolidated multi-entity reporting

- Coordination with legal and tax counsel

Ask specifically: does the advisor take a goals-based approach, or do they optimize for product placement? Do you receive a dedicated relationship manager, or rotate through a call centre?

Understand the Fee Structure and Alignment

Transparency here is non-negotiable. Ask:

- How is the firm compensated? Fee-only (paid by client only) is structurally cleaner than fee-based (advisory fees plus commissions)

- Are there distribution arrangements that influence product recommendations?

- Is the fee schedule disclosed upfront in writing?

A fee-only SEBI RIA earns nothing from the products it recommends. When the advisor's income is entirely independent of product selection, recommendations stay grounded in what actually serves the client — not what generates a commission.

Frequently Asked Questions

What is considered ultra-high net worth in wealth management?

The globally recognized threshold is US$30 million or more, though institutions differ on whether this measures investable assets (Capgemini, Fidelity) or total net worth (Knight Frank, Altrata). In India, definitions vary by institution, but ₹25 crore and above in net investable wealth is commonly referenced as an entry-level UHNI threshold.

What is UHNW wealth management?

UHNW wealth management is a comprehensive, integrated discipline covering investment management, estate planning, tax optimization, succession planning, philanthropy, and family office services. It is structurally different from retail or standard HNI advisory — the focus is on managing, protecting, and transferring significant wealth across generations, not just growing a portfolio.

How is UHNW wealth management different from HNI wealth management?

The difference lies in complexity and scope. UHNW individuals typically have multiple business entities, assets across jurisdictions, succession and legacy concerns spanning several family members, and risk exposures — such as concentrated promoter equity — that require coordinated specialist teams rather than a single advisor managing a portfolio.

What services should a UHNW wealth manager provide?

Core service areas include investment management (with access to private equity, AIFs, and alternatives), tax planning, estate and succession planning, risk management, philanthropic planning, and family office support. The best advisors integrate all of these into a single coordinated strategy rather than treating investments in isolation.

How do I find a trustworthy UHNW wealth management firm in India?

Start with the SEBI public register to confirm RIA registration. Then evaluate the firm on:

- SEBI-registered Investment Adviser status (not just a mutual fund distributor)

- CFA or equivalent qualifications on the investment team

- AUM size and verifiable client track record

- Fee-only or transparent fee-based model with no product distribution conflicts

What is the role of a fiduciary in UHNW wealth management?

A fiduciary is legally and ethically obligated to act in the client's best interest at all times — recommending strategies based on client goals rather than commission incentives. For UHNIs, where a single biased recommendation on a large allocation can cost crores, this distinction is not procedural. It determines whether an advisor is genuinely working for you or for their own book.