Introduction

Investing in Indian equities from abroad is entirely possible, but the documentation requirements are more demanding than what resident Indians face. NRIs must satisfy both SEBI's KYC requirements and FEMA regulations simultaneously, which means a longer document list, potential notarization, and account-type-specific requirements that many first-time applicants don't anticipate.

The most common outcome? Applications stuck in review for weeks due to a missing declaration, an expired utility bill, or a name mismatch across documents.

This guide covers everything: the complete document checklist that applies across both account routes, what changes depending on whether you choose an NRE-PIS or NRO Non-PIS account, how attestation works, and the mistakes that most reliably delay account activation.

Key Takeaways

- Required documents span identity, NRI status, address, banking, and compliance—exact combination depends on account type

- PAN card and FATCA/FEMA declarations are mandatory for all NRI applicants without exception

- Notarization is required only when KYC status on the ITD portal is not already marked "Non-Resident"

- PIS (repatriable) and Non-PIS (non-repatriable) routes have different documentary requirements—primarily around the RBI permission letter

- Submitting complete, correct documents upfront reduces the overall timeline to roughly 3–4 weeks

What Is an NRI Demat Account and Who Can Open One?

An NRI Demat account is an electronic repository for holding stocks, bonds, and other securities listed in India. It is maintained through a Depository Participant (DP) affiliated with either NSDL or CDSL, India's two central depositories. When opening one, you must specify the account type as "NRI" with a sub-type of either "Repatriable" or "Non-Repatriable" — a distinction that shapes everything from your document list to repatriation rights.

Who is eligible?

- Non-Resident Indians (NRIs)

- Overseas Citizens of India (OCIs)

- Persons of Indian Origin (PIOs) — PIO cardholders were deemed OCI cardholders from January 9, 2015, per SEBI's investor guidelines

All investments are governed by the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 and must comply with SEBI's KYC framework. Which account type you choose determines more than just banking linkage — it affects how freely you can move capital.

Repatriable vs. Non-Repatriable: The Two Account Types

The choice between an NRE and NRO account determines your document list, banking linkage, and investment flexibility.

NRE Demat Account:

- Linked to an NRE bank account

- Funds and returns can be freely repatriated abroad

- Requires Portfolio Investment Scheme (PIS) approval from the RBI through a designated Authorised Dealer bank

- Ideal for investors who plan to move capital back overseas

NRO Demat Account:

- Linked to an NRO bank account

- Repatriation is capped at USD 1 million per financial year

- No PIS letter required

- Recommended for NRIs earning India-sourced income (rent, dividends) who plan to reinvest locally

- F&O (futures and options) trading is only permitted through the NRO route under current SEBI rules

Complete Document Checklist for an NRI Demat Account

The following documents apply across both NRE-PIS and NRO Non-PIS account routes. Account-specific requirements are covered in the next section.

Identity Proof

Passport is the primary identity document for all NRI applicants. Submit a self-attested notarised copy covering:

- Personal details page

- Photograph and signature page

- Valid visa or entry stamp page

Foreign passport holders must additionally submit an OCI card or PIO card alongside their passport.

NRI Status Proof

Acceptable documents to establish non-resident status:

- Valid visa (work, employment, student, or residence permit)

- OCI card

- PIO card

- For Merchant Navy NRIs: Continuous Discharge Certificate (CDC) along with a valid contract letter

The document must clearly show that the holder resides outside India.

Address Proof

Overseas address (mandatory): Acceptable documents include:

- Utility bills (electricity, gas, water) — must not be more than 2 months old per NSDL's Master Circular

- Overseas bank statement or passbook — must not be more than 3 months old

- Rental or lease agreement

- Foreign driving licence

- Residence permit card

The address must exactly match what is entered on the application form. Minor formatting differences can trigger rejection.

Indian address (optional): If submitted, acceptable documents include a masked Aadhaar copy, Voter ID, or Indian utility bill. Not all brokers require this if a verifiable overseas address is provided.

PAN Card

PAN is mandatory for all NRIs investing in Indian securities markets under Income Tax Rule 114B. Quoting PAN is required for securities transactions, and it serves as the primary identification number across India's securities market per SEBI's KYC framework.

NRIs without a PAN should apply through the NSDL or UTI portal before starting the Demat account process. Processing typically takes 2–3 weeks.

Banking and Financial Documents

- Self-attested cancelled cheque or latest bank statement from the NRE account (for NRE-PIS accounts)

- Same from the NRO account (for NRO Non-PIS accounts)

- Overseas bank statement (last 3–6 months) may be required as income or financial proof

Compliance and Regulatory Forms

All NRI applicants must submit the following regulatory declarations:

| Declaration | Details Required |

|---|---|

| FATCA | Tax Identification Number (TIN) for your country of residence |

| FEMA | Declaration of non-resident status and source of funds |

| P.O. Box Declaration | Required if overseas address is a P.O. Box |

Country-specific TIN references:

- USA: Social Security Number (SSN)

- UK: Unique Taxpayer Reference (UTR)

- Canada: Social Insurance Number (SIN)

- Australia: Tax File Number (TFN)

Additional Requirements

- Recent passport-sized photographs (quantity varies by broker or DP)

- Income proof — Brokers classify NRIs as Clients of Special Category (CSC) under KYC guidance, requiring one of: last 6 months' bank statement, latest salary slip, ITR acknowledgement, net worth certificate, or Demat holdings statement

Document Requirements by Account Type: PIS vs. Non-PIS

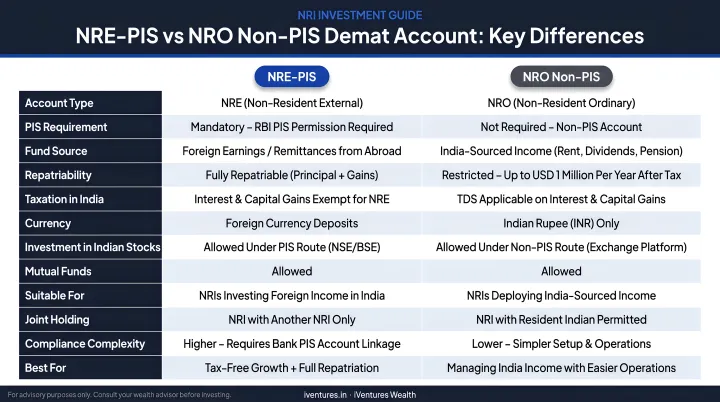

The core difference between these two routes comes down to one document: the RBI PIS permission letter.

PIS accounts are linked to an NRE bank account. All equity trades are reported to the RBI by the designated Authorised Dealer bank. Non-PIS accounts use the NRO account and require no RBI permission letter, though they come with annual repatriation limits.

Documents Exclusive to a PIS Account

The PIS permission letter is the one document that separates the two routes. Without it, a PIS account application cannot proceed. This letter must be:

- Obtained from the designated bank (commonly HDFC, ICICI, Axis, IndusInd, Yes Bank, or IDFC First — based on broker partnerships, not an exhaustive RBI list)

- Self-attested before submission with account opening forms

- Applied for before approaching the broker or DP

Documents for a Non-PIS Account

Non-PIS applicants skip the PIS letter entirely. The account links to an NRO bank account, and the standard document checklist from the previous section applies in full. A few practical points worth noting:

- No RBI permission letter is required at any stage

- The NRO account serves as the primary linked bank account

- An NRE savings account can be added as a secondary account if needed

Key Difference Summary

| Dimension | NRE-PIS | NRO Non-PIS |

|---|---|---|

| Bank account linked | NRE | NRO |

| PIS letter required | Yes | No |

| Repatriation | Fully repatriable | Capped at USD 1 million/year |

| F&O trading eligibility | Not permitted | Permitted |

Document Attestation and KYC Compliance

The attestation requirement depends entirely on a single factor: your KYC status on the Income Tax Department (ITD) portal.

- If KYC shows "Non-Resident": Documents generally do not need to be notarised. Self-attestation is typically sufficient. Check this before gathering documents—it can save considerable time and expense.

- If KYC shows "Resident": All documents except cheques must be notarised or formally attested before submission.

Who Can Attest Your Documents?

Authorised attestors per SEBI guidelines include:

- Indian Embassy or Consulate General in your country of residence

- Notary Public abroad

- Court Magistrate or Judge

- Overseas branches of Indian scheduled commercial banks (authorised officials only)

The attestor must affix a "verified with original" stamp along with their name, designation, and signature. NSDL additionally requires their seal.

These attestation rules apply whether you're applying from abroad or within India. If you're physically present in India at the time of application, the process is slightly different:

- Provide a copy of your latest immigration stamp as proof of NRI status

- Notarisation can be done through Indian authorities rather than overseas attestors

In-Person Verification (IPV) is mandatory for all applicants, regardless of location. It can be completed digitally via video OTP or offline at a branch, per SEBI's KYC guidelines.

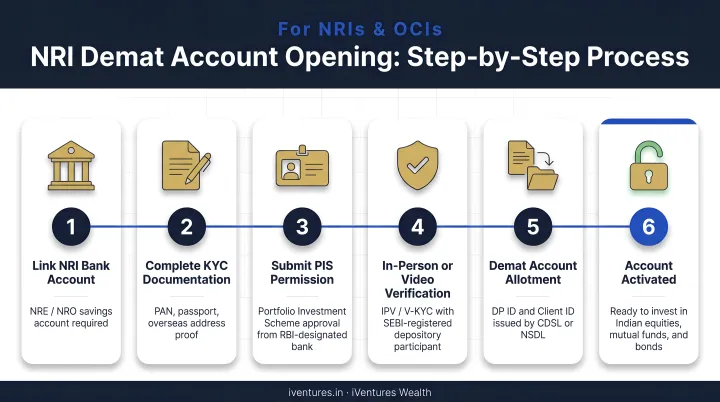

Step-by-Step Process to Open an NRI Demat Account

- Open an NRE or NRO bank account if not already held — this must precede all other steps

- Apply for PIS permission from a designated Authorised Dealer bank (NRE route only)

- Choose a SEBI-registered broker or DP — confirm they support the NRI account type you need

- Submit KYC documents — typically soft copies first via email, followed by attested hard copies by courier where required

- Complete IPV — online via video OTP or offline at a branch

- Receive account credentials and begin investing

The full end-to-end timeline is typically 3–4 weeks, factoring in PIS letter processing, document attestation, and broker review. Some brokers complete account activation in under 72 hours once all documents are in order.

NRIs dealing with FATCA/FEMA compliance or multi-jurisdiction structuring often work with a SEBI-registered adviser — such as iVentures Wealth (INA000019026) — for documentation support and cross-border execution across markets like the US, UK, UAE, and Singapore.

Two additional steps are worth completing at account opening:

- Designate a nominee by submitting their ID details and contact information via the Nomination Form

- Consider a Power of Attorney (POA) or DDPI if a trusted person needs to manage the account — not required if you can authorise trades directly using a CDSL T-PIN

Common Mistakes NRIs Make With Documentation

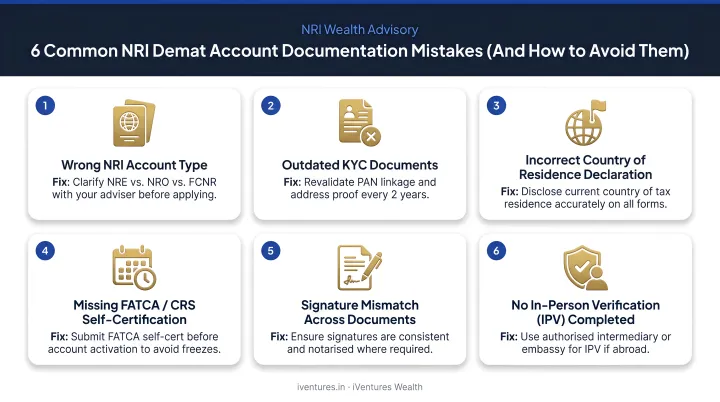

Most account opening delays trace back to a small set of avoidable errors:

- Expired or outdated documents — overseas utility bills older than 2 months or bank statements older than 3 months are typically rejected outright

- Name mismatches across documents — even minor discrepancies (initials vs. full name) require a self-declaration letter to resolve

- Address discrepancy — the address on supporting documents must match the application form exactly

- Incorrect or missing TIN on FATCA forms — a blank or wrong Tax Identification Number is one of the most common causes of FATCA rejection

- Incorrect attestation — notarising documents when attestation is sufficient (or skipping notarisation when it is required) adds weeks to processing; always check your ITD KYC status first

- Residential status not updated on ITD portal — if PAN is linked to a "Resident" status on the Income Tax portal, it may be blocked from trading

Before submitting your application, run through these three checks: document validity dates, name and address consistency across all submissions, and your ITD KYC status. Getting these right at the outset is faster than chasing corrections after the fact.

Frequently Asked Questions

Can NRIs open a Demat account?

Yes. NRIs, OCIs, and PIOs are permitted to open Demat accounts in India under RBI and SEBI guidelines. They can invest in Indian equities, bonds, and mutual funds subject to FEMA regulations and investment limits set by RBI.

Can an NRI use a resident Demat account?

No. Once residential status changes to non-resident, the existing resident Demat account must be converted to an NRI Demat account or closed. Continuing to operate a resident account as an NRI is non-compliant with FEMA rules.

What is the difference between NRE and NRO Demat accounts?

The two accounts differ primarily on repatriation and compliance requirements:

- NRE Demat: Fully repatriable; requires RBI PIS permission

- NRO Demat: Non-repatriable beyond USD 1 million annually; no PIS letter needed; permits F&O trading

NRIs with India-sourced income generally find the NRO account simpler to manage.

Is PAN card mandatory for NRIs to open a Demat account?

Yes. PAN is mandatory for all NRIs investing in Indian securities markets under the Income Tax Act. NRIs without a PAN must apply for one before initiating the Demat account process.

Do documents need to be notarised for NRI Demat account opening?

Only if your KYC status is not already marked "Non-Resident" on the ITD portal. If ITD KYC confirms non-resident status, documents can typically be self-attested.

How long does it take to open an NRI Demat account?

Most NRI Demat accounts take 3–4 weeks to open in total. The timeline covers PIS letter processing (if required), document gathering and attestation, IPV completion, and broker-side account activation.