The challenge is that the framework is genuinely complex. In August 2022, India replaced its nearly two-decade-old outbound investment rules with a modernised regime under FEMA — one that expanded permissions in several areas while tightening compliance requirements in others. Non-compliance carries real consequences: financial penalties, blocked remittances, and regulatory exposure.

This guide breaks down who can invest, how much, in what form, and what reporting obligations follow.

Key Takeaways

- ODI applies to unlisted foreign equity, control-based stakes, or 10%+ holdings in listed entities; everything else falls under OPI

- Total financial commitment under ODI cannot exceed 400% of net worth under the Automatic Route

- Resident individuals are capped at USD 250,000 per financial year under LRS, restricted to operating entities only

- ODI in real estate activity, gambling, and Indian rupee-linked financial products is strictly prohibited

- Reporting delays trigger Late Submission Fees and freeze all further financial commitments until regularised

What Is Overseas Direct Investment (ODI)?

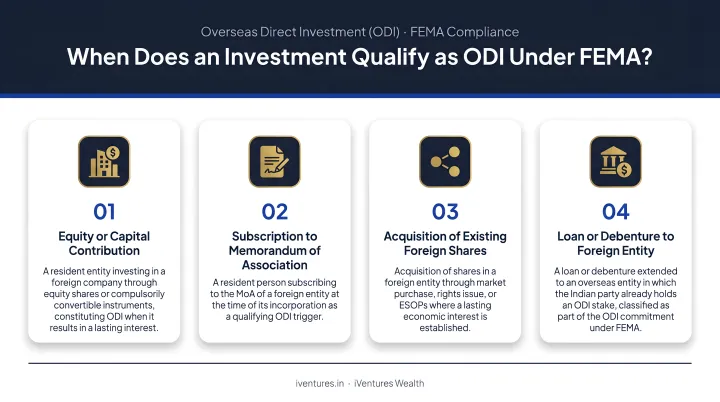

ODI is a financial commitment made by a person resident in India in a foreign entity — through equity capital, debt, or non-fund-based instruments like guarantees.

Under Rule 2(1)(q) of the Foreign Exchange Management (Overseas Investment) Rules, 2022, four specific scenarios qualify as ODI:

- Acquisition of any unlisted equity capital of a foreign entity

- Subscription to the Memorandum of Association of a foreign entity

- Investment of 10% or more in the paid-up equity capital of a listed foreign entity

- Investment with control in a listed foreign entity, even if the stake is below 10%

Once an investment is classified as ODI, it stays ODI. Even if the stake later falls below 10% or control is lost, the "once ODI, always ODI" principle — codified in the Explanation to Rule 2(1)(q) — keeps it in that category.

Common Instruments for ODI

ODI can be made through:

- Subscription to the Memorandum of Association

- Purchase of equity capital (listed or unlisted)

- Rights issues or bonus shares

- Capitalisation of dues

- Swap of securities

- Acquisition through merger, demerger, or amalgamation

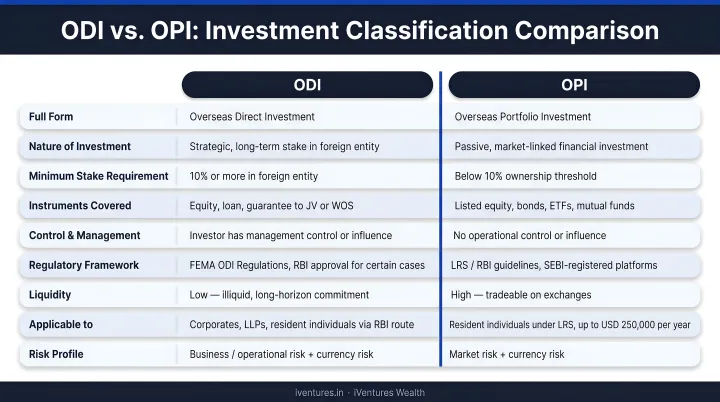

ODI vs. Overseas Portfolio Investment (OPI)

Not every cross-border investment is ODI. OPI, defined under Rule 2(1)(s), covers investment in foreign securities that does not qualify as ODI — typically listed equity below 10% and without control. The boundary between the two turns on two key rules:

- Unlisted equity is always ODI, regardless of percentage held

- Unlisted debt instruments do not qualify as OPI

| Feature | ODI | OPI |

|---|---|---|

| Security type | Unlisted equity or 10%+ listed | Listed equity below 10% |

| Control rights | Permitted | Not permitted |

| Investment limits | 400% of net worth (entities) | LRS limit (individuals) |

| Reporting complexity | Higher | Lower |

India's ODI Regulatory Framework: The 2022 FEMA Structure

The current framework came into force on August 22, 2022, replacing FEMA 120/RB-2004 and the 2015 immovable property regulations. It consists of three instruments issued simultaneously:

| Instrument | Issuer |

|---|---|

| Foreign Exchange Management (Overseas Investment) Rules, 2022 (G.S.R. 646(E)) | Central Government, Ministry of Finance |

| Foreign Exchange Management (Overseas Investment) Regulations, 2022 (FEMA 400/2022-RB) | Reserve Bank of India |

| Foreign Exchange Management (Overseas Investment) Directions, 2022 (AP (DIR Series) Circular No.12) | RBI to Authorised Dealer banks |

What Changed in 2022

Two conceptual shifts define the new regime:

- Broader definitions: The old "Joint Venture / Wholly Owned Subsidiary" framework was replaced with the wider "Foreign Entity" concept. ODI and OPI were formally defined for the first time, eliminating long-standing ambiguity about investment classification.

- Net worth basis restricted to the investing entity: The 400% financial commitment cap now applies exclusively to the investing entity's own net worth, not that of a subsidiary or holding company. This is a material change for corporate groups where the parent carries lower standalone net worth than the consolidated group.

Who Can Make ODI from India?

The 2022 framework applies different rules depending on investor type. One rule applies across the board: the foreign entity must conduct a bona fide business activity that is permissible under the laws of both India and the host country.

Indian Entities: Companies, LLPs, and Partnerships

Indian companies, LLPs, and registered partnership firms have the broadest investment permissions. Two key conditions to note:

- A non-financial-services Indian entity may invest in a foreign financial services entity (excluding banking and insurance) if it has posted net profits in the preceding three financial years

- Entities classified as NPA borrowers, wilful defaulters, or under investigation by agencies like the CBI or Enforcement Directorate must obtain a No Objection Certificate (NOC) before proceeding — with a 60-day deemed no-objection if the authority does not respond

Resident Individuals Under LRS

Resident individuals invest under the Liberalised Remittance Scheme with an annual limit of USD 250,000 per financial year. Key restrictions:

- Can only invest in operating foreign entities not engaged in financial services

- Cannot create step-down subsidiaries where the individual holds control

- Must use own funds for ODI in foreign start-ups (borrowed funds are not permitted)

The Two Routes: Automatic vs. Approval

| Route | When It Applies | Prior Approval |

|---|---|---|

| Automatic | Within the 400% financial commitment limit, permissible sectors | Not required |

| Approval | Above 400% limit, strategic sectors notified by government, or entities under investigation | Explicit RBI or Central Government clearance required |

Financial Commitment Limits, Structural Rules, and Prohibited Sectors

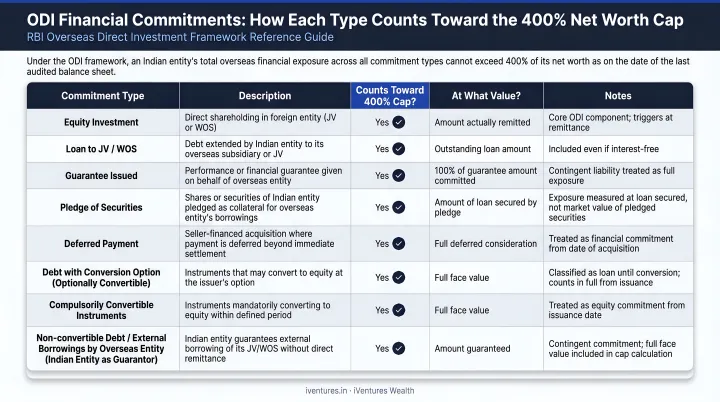

The 400% Net Worth Cap

An Indian entity's Total Financial Commitment (TFC) across all foreign entities combined must not exceed 400% of its net worth as on the date of the last audited balance sheet — which must not be older than 18 months from the transaction date.

Numerical illustration: If an Indian company has a standalone net worth of ₹100 crore, its maximum permissible financial commitment under the Automatic Route is ₹400 crore across all overseas investments combined.

What Counts Toward the 400% Limit

| Commitment Type | How It's Counted |

|---|---|

| Equity investment | 100% of investment value |

| Loans / debt extended | 100% of amount |

| Corporate guarantees | 100% of guarantee value |

| Performance guarantees | 50% of face value |

| Pledges / charges | Lower of pledge value or facility amount |

| Rollover of guarantees (within original amount) | Not counted as fresh commitment |

Two additional rules govern how commitments are measured and priced:

- Deferred consideration, introduced as a liberalisation under the 2022 framework, is permitted under the Automatic Route. The deferred portion is treated as a non-fund-based commitment and counts toward the financial commitment limit.

- All equity issuances and transfers between residents and non-residents must be priced on an arm's length basis using internationally accepted valuation methodologies.

Structural Restrictions: The Two-Layer Rule

Beyond the financial limits, India's ODI framework also restricts how ownership structures can be built. No person resident in India can make financial commitments in a foreign entity if the resulting structure creates more than two layers of subsidiaries — a rule designed to curb complex ownership chains and round-tripping arrangements.

Exempted under the Companies (Restriction on Number of Layers) Rules, 2017:

- Banking companies

- Systemically important NBFCs registered with RBI

- Insurance companies

- Government companies

Prohibited Sectors

Three categories are absolutely prohibited for ODI, regardless of investment size:

- Real estate activity — defined as buying/selling real estate or trading in Transfer of Development Rights (TDRs). Note: development of townships, construction of residential or commercial premises, or roads for sale or lease is not prohibited

- Gambling or betting in any form

- Financial products linked to the Indian Rupee without specific RBI approval

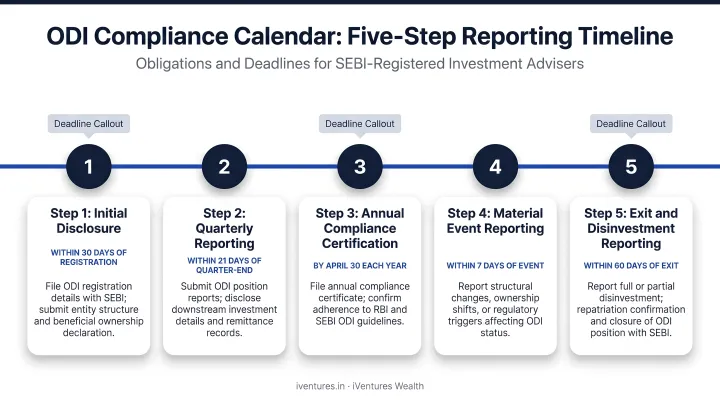

ODI Reporting Requirements and Compliance

All ODI reporting flows through the designated Authorised Dealer (AD) bank. Three reporting milestones govern the compliance calendar:

| Filing | Trigger | Deadline |

|---|---|---|

| Form FC | Before or at the time of outward remittance | Prior to first remittance |

| Annual Performance Report (APR) | Each year for each foreign entity | December 31 |

| Annual Return on Foreign Liabilities and Assets (FLA) | Each year for entities with ODI | July 15 |

Before the first remittance, a Unique Identification Number (UIN) must be obtained from RBI for the foreign entity. All subsequent transactions for that UIN must route through the designated AD bank. Share certificates must be submitted to the AD bank within six months of effecting the remittance.

Late Submission Fees and the Compliance Block

RBI's Late Submission Fee framework applies when reporting deadlines are missed:

- Periodic filings (APR, FLA): Flat fee of ₹7,500 per return

- Transactional filings (Form FC): ₹7,500 + (0.025% × transaction amount × years of delay)

- LSF window: Available for up to three years from the original due date — after which the option lapses entirely

The fee, however, is rarely the bigger problem. Any lapse — fund-based or non-fund-based — blocks all further financial commitments in the foreign entity until regularised. For investors with active overseas operations or pending transactions, that freeze can be far more costly than the penalty itself.

The Multi-Layer Compliance Calendar

Managing ODI compliance means coordinating multiple moving parts — often across foreign entities with different financial year-ends:

- UIN generation and Form FC submission before the first remittance

- APR filing by December 31 each year per entity

- FLA reporting by July 15 annually

- Share certificate submission within six months of remittance

- Ongoing AD bank coordination for every subsequent transaction

iVentures Wealth works with UHNIs, family offices, corporate promoters, and NRI/OCI clients on cross-border investment structuring and compliance coordination. As a SEBI-registered investment adviser (INA000019026), the firm helps investors track reporting timelines across entities, coordinate documentation with AD banks, and avoid the penalty exposure that compounds when multiple deadlines are missed at once.

Frequently Asked Questions

What are overseas direct investment regulations?

ODI regulations in India are governed by the FEMA (Overseas Investment) Rules, Regulations, and Directions issued on August 22, 2022, by the Central Government and RBI. They set out who can invest, in what instruments, up to what limits, and with what ongoing reporting obligations.

What are the limits on overseas direct investment?

An Indian entity's total financial commitment cannot exceed 400% of its net worth (last audited balance sheet, not older than 18 months) under the Automatic Route. Resident individuals investing under LRS are separately capped at USD 250,000 per financial year.

What is the difference between ODI and OPI?

ODI covers investments where the investor acquires control, holds 10%+ in a listed foreign entity, or makes any investment in unlisted equity. OPI covers listed equity below 10% without control. The key dividing line is control and the nature of the foreign entity.

What is an overseas direct investment?

ODI is a financial commitment by a person resident in India in a foreign entity — primarily through equity — where the investor acquires control, subscribes to the MoA, holds 10%+ in a listed entity, or makes any investment in unlisted equity regardless of percentage held.

Who is eligible to make overseas direct investment from India?

Three main categories are eligible:

- Indian companies, LLPs, and partnership firms — broadest permissions under the Automatic Route

- Resident individuals under LRS — capped at USD 250,000 per year, operating entities only

- Registered trusts or societies — limited to the educational or hospital sectors, with prior RBI approval

What happens if you miss the ODI reporting deadline?

A Late Submission Fee applies, and the investor is blocked from making any further financial commitments — fund-based or non-fund-based — until the lapse is regularised. The LSF option expires if unused within three years of the original due date.