The confusion usually runs in two directions: some investors assume offshore funds are synonymous with tax evasion, while others dive in without understanding the regulatory obligations, structural nuances, and real risks involved. Neither approach serves them well.

This article covers what offshore funds actually are, how they are structured, what advantages they genuinely offer Indian investors, and where the complications lie — including tax obligations that cannot be ignored. The goal is a clear framework so you can evaluate whether offshore fund exposure belongs in your portfolio.

Key Takeaways

- Offshore funds are legal, regulated investment vehicles domiciled outside India — Indian residents can access them via RBI's LRS (up to USD 250,000/year)

- Master-feeder structures dominate global hedge funds, with Cayman Islands hosting 30,000+ funds as of 2024

- INR depreciated roughly 85% against USD over the last 20 years — a concrete case for currency diversification

- Hedge fund fees average 1.35% management + ~19% performance — materially higher than domestic funds

- Undisclosed foreign assets face a 30% flat tax plus penalties under India's Black Money Act, 2015

What Is an Offshore Fund?

An offshore fund is an investment fund incorporated, registered, and domiciled outside the investor's home country. For an Indian investor, any fund based in the Cayman Islands, Luxembourg, Ireland, or Mauritius qualifies as offshore.

The term carries no inherent implication of illegality. These are regulated investment vehicles governed by the laws of their domicile jurisdiction, and all holdings are fully disclosable under Indian law.

Types Indian Investors Typically Encounter

| Fund Type | Typical Structure | Investor Profile |

|---|---|---|

| Offshore Mutual Funds | UCITS (Luxembourg/Ireland), open-ended | HNIs, institutional |

| Hedge Funds | Cayman LP or limited company | UHNIs, institutional |

| Private Equity Funds | Cayman or BVI limited partnership | UHNIs, family offices |

| Fund-of-Funds | Offshore feeder into multiple strategies | UHNIs seeking diversification |

The Legal Reality

Indian residents can invest in offshore funds through the RBI's Liberalised Remittance Scheme (LRS), which permits remittances of up to USD 250,000 per individual per financial year. All holdings must be disclosed in the investor's ITR under Schedule FA. The funds themselves operate transparently under their domicile's regulatory framework — Mauritius under the FSC, Ireland under the Central Bank of Ireland, Cayman Islands under CIMA.

Common Structures of Offshore Funds

Structure choice affects everything from tax treatment to operational complexity. Four architectures account for the vast majority of offshore fund setups.

Offshore Standalone Structure

A single fund vehicle incorporated in an offshore jurisdiction — typically Cayman Islands or BVI — with no domestic counterpart. Used primarily by managers targeting non-US investors or US tax-exempt entities, the appeal is simplicity: lower administrative burden, one entity, straightforward governance. According to CIMA's historical data, approximately 21% of Cayman hedge funds operated as standalone vehicles.

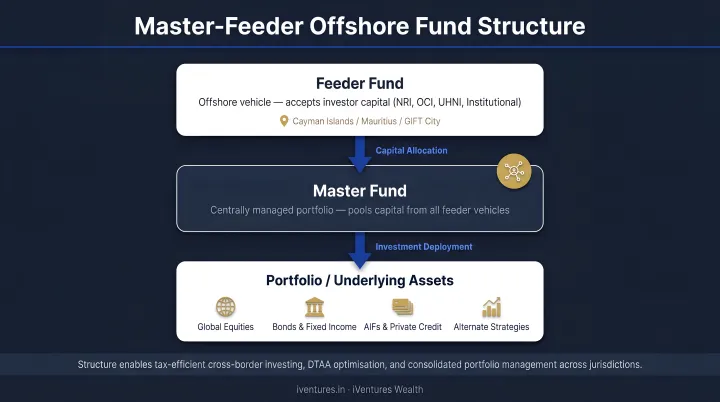

Master-Feeder Structure

The most widely used architecture for global funds. Here's how it works:

- A master fund (offshore, usually Cayman) executes all trading

- A domestic feeder (US LP) routes US taxable investors in

- An offshore feeder (Cayman blocker corporation) routes non-US investors and US tax-exempt entities

The offshore blocker prevents non-US investors from triggering US tax return obligations on US-source income. All investors benefit from a single trading entity, which reduces execution costs and simplifies portfolio management. CIMA data shows 50% of Cayman hedge funds used master-feeder structures — the dominant choice for a reason.

Side-by-Side Structure

Two parallel funds — one offshore, one domestic US — managed identically but legally separate. Less common than master-feeder because executing identical trades across two entities creates operational complexity. Most useful when specific tax elections or income treatments in one fund would negatively affect investors in the other.

Segregated Portfolio Company (SPC)

A single corporate entity with multiple legally ring-fenced sub-portfolios. Each portfolio has its own assets and liabilities — a default or claim in one cannot reach another. Popular for umbrella structures running multiple strategies or share classes under one legal entity, particularly in Mauritius and Cayman. A manager running three distinct credit strategies, for instance, can house all three under one SPC rather than filing three separate incorporations.

Where a fund is domiciled matters as much as how it's structured. The jurisdiction determines regulatory oversight, distribution access, and tax treatment for investors.

Key Offshore Jurisdictions

- Cayman Islands — CIMA reported 13,008 mutual funds and 17,910 private funds as of Q1 2026. The largest global domicile for hedge and private funds.

- Luxembourg — EUR 6,207 billion in net assets for supervised UCIs (ALFI/CSSF data). The European hub for UCITS distribution. BlackRock Global Funds and Franklin Templeton Investment Funds are both Luxembourg SICAVs.

- Ireland — EUR 4,992 billion NAV for Irish-resident investment funds as of Q4 2024. PIMCO's UCITS strategies are managed from Dublin through PIMCO Global Advisors (Ireland) Limited.

- Mauritius — Regulated by the FSC, but its historical tax advantage for India-linked structures has largely eroded since a 2016 treaty protocol gave India capital gains taxation rights on shares acquired from April 2017 onwards.

Key Benefits of Offshore Funds

Global Diversification

India's domestic market, despite its depth, cannot provide exposure to global private equity, international hedge strategies, frontier market debt, or multi-currency portfolios. For UHNIs and family offices with significant India-concentrated wealth, offshore funds reduce correlation risk — when domestic markets underperform, globally diversified positions can partially offset losses.

MSCI research on frontier markets notes that low integration and correlation between markets create genuine diversification benefits, though rising global integration does gradually reduce this effect over time.

Currency Protection

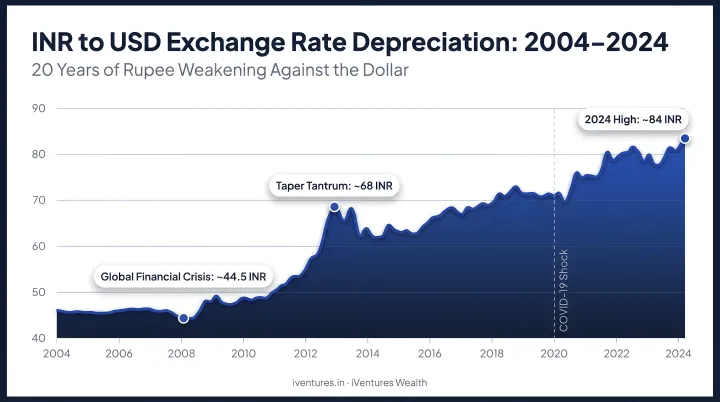

The numbers make a direct case. World Bank data shows India's exchange rate moved from approximately ₹45.3 per USD in 2004 to ₹83.7 per USD in 2024 — roughly 85% more INR required per dollar over two decades. For families with children in foreign universities, global real estate obligations, or planned emigration, holding assets in USD or EUR through offshore funds provides a structural hedge against INR depreciation over long periods.

Historical INR weakness has materially eroded the real value of purely domestic portfolios for families with global commitments — and that track record is reason enough to plan around it.

Access to Institutional-Grade Managers

Offshore funds give Indian UHNIs access to strategies not registered for domestic sale. Several categories are only reachable through offshore structures:

- Institutional strategies from managers like BlackRock, PIMCO, and Franklin Templeton — typically distributed through Luxembourg SICAVs or Irish UCITS vehicles

- Specialist alternative managers running event-driven, macro, or credit strategies

- Multi-asset global mandates unavailable through Indian feeder or mutual fund routes

iVentures Wealth, as a SEBI-registered advisor, provides research-backed guidance to help UHNIs and NRIs identify offshore fund exposure that matches their risk profile, currency requirements, and time horizon — rather than allocating based on distributor incentives.

Fund-Level Tax Efficiency

Jurisdictions like Luxembourg, Ireland, and Cayman typically impose no fund-level capital gains or withholding tax on the fund itself. Returns therefore compound more efficiently within the fund before distribution. That said, Indian investors remain fully liable for Indian tax obligations on gains — the benefit is reduced friction at the fund level, not tax elimination. The distinction matters when comparing gross and net compounding over 10+ year horizons.

Challenges and Risks of Offshore Funds

Regulatory and Compliance Complexity

Indian investors navigating offshore funds must manage multiple regulatory layers simultaneously:

- RBI LRS: Capped at USD 250,000 per individual per financial year

- FEMA: Overseas investment guidelines govern the structure of permissible investments

- SEBI: A November 2024 circular (SEBI/HO/IMD/IMD-I POD1/P/CIR/2024/149) now permits Indian mutual funds to invest in overseas funds subject to at least 80% of the target fund's assets being in securities — relevant for domestic fund-of-funds accessing offshore vehicles

- Tax disclosure: Schedule FA and Schedule FSI filing obligations under the Income Tax Act

Violations carry significant penalties. Penalties range from monetary fines to prosecution under FEMA, and LRS violations can trigger suspension of remittance privileges — consequences that demand proactive compliance management, not reactive remediation.

Currency Risk

Currency diversification cuts both ways. If INR strengthens against the fund's base currency, an Indian investor's returns shrink even when the underlying fund performs well. Currency hedging within offshore funds is available in some structures but adds cost, and not all fund structures offer it. Evaluate currency exposure and hedging availability before committing capital — not after.

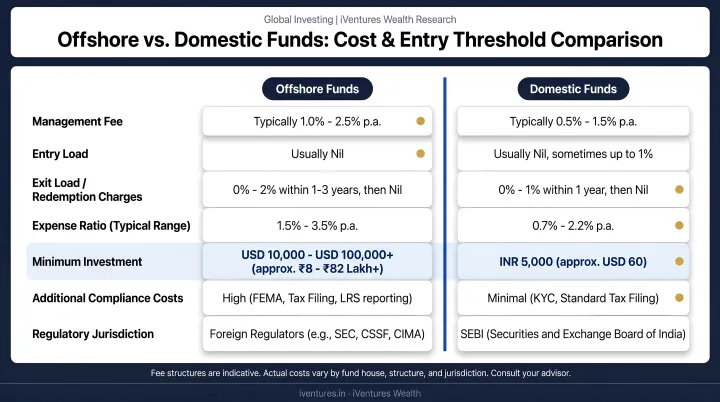

Higher Costs and Minimums

Offshore funds cost meaningfully more than domestic alternatives:

- Hedge fund management fees: Industry average of 1.35% as of June 2024 (HFR data), with performance fees averaging approximately 19% of profits above a hurdle rate

- Traditional model: Still quoted as 2% management / 20% performance for many funds

- Minimum investment thresholds: CIMA's registered fund route requires a minimum of USD 100,000 per investor; institutional share classes at managers like BlackRock can require EUR 1,000,000 or equivalent as minimum initial subscription

For context, these costs are materially higher than domestic Indian mutual fund expense ratios. The allocation only makes sense when the offshore fund delivers net-of-fee alpha, meaningful correlation reduction versus domestic holdings, or access to strategies — such as global macro, distressed credit, or developed-market private equity — that simply aren't available through domestic vehicles.

Jurisdictional and Counterparty Risk

Offshore funds operate under the regulatory environment of their domicile. Several layers of risk require assessment before committing capital:

- Treaty and tax risk: Mauritius-routed investments lost capital gains exemptions post-2016 amendments — a reminder that treaty benefits are not permanent

- Investor protection gaps: Offshore domiciles may offer weaker recourse mechanisms than SEBI's investor grievance framework

- Counterparty exposure: Prime brokers, custodians, and administrators in foreign jurisdictions operate under different regulatory backstops, with limited recourse if a counterparty defaults

Taken together, these factors mean due diligence on an offshore fund extends well beyond performance track record.

Tax Considerations for Indian Investors

Tax is where most offshore fund conversations get complicated — and where errors are most costly.

Mandatory Disclosure Under Indian Law

Indian residents holding offshore fund interests must:

- Report holdings under Schedule FA (Foreign Assets) in their ITR

- Report income under Schedule FSI (Foreign Source Income)

- Treat gains as capital gains (if units are capital assets under Section 2(14)) or income from other sources under Section 56, depending on the nature of the distribution

The Black Money (Undisclosed Foreign Income and Assets) Act, 2015 is unambiguous: undisclosed foreign assets attract a 30% tax charge, plus penalties including three times the tax amount and ₹10 lakh for specified reporting failures. Non-disclosure is not a grey area.

Accumulating vs. Distributing Funds

Indian tax law taxes actual receipts and, in some structures, accruals. Whether a fund distributes income annually or accumulates it within the fund affects when Indian tax liability crystallises. Investors should understand the fund's distribution policy before committing capital, not after.

DTAA Applicability

India has Double Taxation Avoidance Agreements with Luxembourg, Ireland, Mauritius, and Singapore. These treaties can reduce withholding tax rates on dividends and interest at the fund level — the India-Ireland DTAA, for example, applies 10%/15% rates on dividends depending on the shareholding condition, and 10% on interest.

Treaty provisions are not static, however. Mauritius is the clearest recent example of how quickly terms can shift. Treaty benefits also require proper documentation, including tax residency certificates — which must be obtained and maintained before claiming any relief.

Getting this wrong is expensive. Professional advisory here isn't a luxury — it's a prerequisite. iVentures Wealth coordinates with tax advisors across jurisdictions, handling Schedule FA disclosures, capital gains statements, and treaty benefit claims as part of a structured global investing engagement — not as an add-on addressed after the fact.

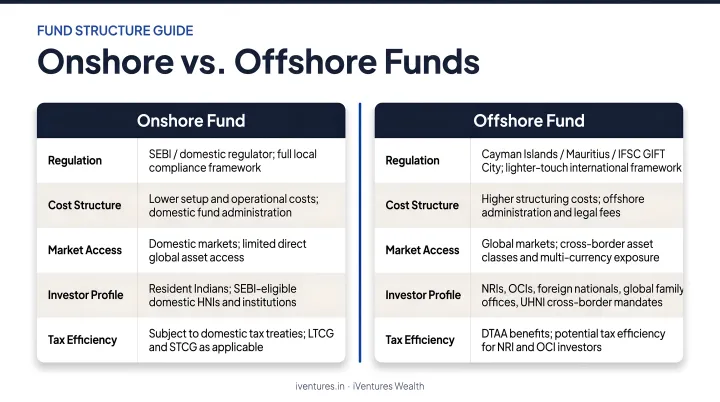

Onshore vs. Offshore Funds: Key Differences

| Factor | Onshore (Indian) Funds | Offshore Funds |

|---|---|---|

| Domicile & Regulation | SEBI-regulated, India | Foreign jurisdiction (Cayman, Luxembourg, etc.) |

| Accessibility | Open to all Indian investors | Requires LRS remittance; higher minimums |

| Tax Treatment | Straightforward domestic capital gains rules | Cross-jurisdictional; Schedule FA disclosure mandatory |

| Typical Investor | Retail, HNI | UHNI, NRI, institutional, family offices |

| Costs | Lower (SEBI-regulated TER caps) | Higher (management + performance fees) |

| Asset Access | Domestic + some international via FoFs | Genuinely global strategies and managers |

The table above clarifies the structural differences — but the more useful question is when offshore exposure actually earns its place in a portfolio. Consider offshore funds when:

- You need genuine geographic and currency diversification beyond what domestic international fund-of-funds provide

- Specific global strategies (hedge, private equity, structured credit) are not accessible domestically

- Your family has significant foreign liabilities, education commitments, or planned emigration

- Your portfolio is large enough that the higher costs and minimums are proportionate to the diversification benefit

For investors with investable assets below ₹5 Cr, domestic international fund-of-funds typically offer better cost efficiency and simpler compliance — offshore structures become genuinely compelling as portfolio size and cross-border complexity grow.

Frequently Asked Questions

What do you mean by offshore fund?

An offshore fund is an investment fund incorporated and domiciled outside the investor's home country, pooling capital to invest across global assets. For an Indian investor, funds based in the Cayman Islands, Luxembourg, Ireland, or Mauritius qualify as offshore — and are subject to both that jurisdiction's laws and Indian disclosure requirements.

What is the difference between onshore and offshore funds?

Onshore funds are domiciled and regulated within the investor's home country — for example, SEBI-regulated Indian mutual funds. Offshore funds are domiciled in foreign jurisdictions and subject to those countries' regulations, typically offering broader asset access, different tax treatment, and higher investment minimums than their domestic counterparts.

Is an ETF an offshore fund?

An ETF can be offshore if domiciled outside the investor's home country. A UCITS ETF accessed via LRS remittance requires Schedule FA disclosure and qualifies as offshore. International ETFs listed directly on Indian exchanges (NSE or BSE) are domestic instruments and do not.

Are offshore funds legal for Indian investors?

Investing in offshore funds is completely legal for Indian residents when done through the RBI's LRS within the permissible annual limit, and when all foreign assets and income are disclosed in the ITR. The structure of the investment and full disclosure are what separate compliant investment from violation.

What is the LRS limit for investing in offshore funds from India?

The current RBI LRS limit is USD 250,000 per individual per financial year. Each family member holds a separate limit. A family of four can collectively remit up to USD 1,000,000 annually, giving family offices meaningful offshore exposure within the LRS framework.

What are the tax implications of offshore funds for Indian residents?

Indian residents must declare offshore fund holdings under Schedule FA in their ITR. Income is taxed under Indian law as capital gains or income from other sources, based on holding period and fund classification. Applicable DTAAs may reduce withholding taxes at the fund level, but Indian tax on ultimate gains remains payable regardless of domicile.