Key Takeaways

- Tax-loss harvesting lets you offset realised capital gains by selling loss-making investments before March 31.

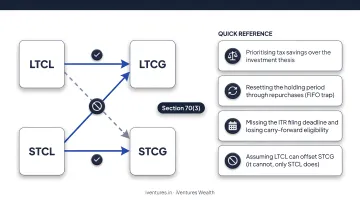

- STCL offsets both STCG and LTCG; LTCL can only offset LTCG — making short-term losses the more flexible tool.

- Losses carry forward for up to 8 assessment years, but only if your ITR is filed by the Section 139(1) due date.

- India has no formal wash-sale rule, but sham sell-and-rebuy transactions attract GAAR and income tax scrutiny.

- Post-Budget 2024, STCG on equity is taxed at 20% and LTCG at 12.5%, raising the stakes for disciplined loss harvesting.

Market downturns are rarely welcome. But for investors with realised capital gains, a falling portfolio carries a silver lining: the opportunity to cut your tax bill through tax-loss harvesting — legally, deliberately, and before March 31.

This strategy is particularly relevant for Indian equity investors, mutual fund holders, founders liquidating equity, and CXOs sitting on ESOP gains. The rules governing it are specific, the deadlines are hard, and the savings can be material. This article explains how it works, what Indian tax law permits, and where investors most commonly go wrong.

What Is Tax-Loss Harvesting?

Tax-loss harvesting is the practice of selling investments that are currently at a loss to offset taxable capital gains earned elsewhere in the same financial year. The goal is to reduce your net taxable capital gains — and therefore your tax liability — using mechanisms explicitly permitted under the Income-tax Act, 1961.

It is not tax evasion — the strategy is entirely legal, structured around statutory set-off provisions under Sections 70 and 74. Nor is it panic selling. The sale is deliberate and calculated, followed by reinvestment in similar securities to preserve portfolio positioning.

The strategy works because Indian tax law allows capital losses to be set off against capital gains in the same year, or carried forward against future gains. In practice, this means:

- Short-term capital losses can offset both short-term and long-term capital gains

- Long-term capital losses can only be set off against long-term capital gains

- Unabsorbed losses can be carried forward for up to eight assessment years

Done right, it reduces what you owe today without changing where your money is invested tomorrow.

How Tax-Loss Harvesting Works in India

The End-to-End Process

The mechanics follow a straightforward sequence:

- Identify unrealised losses in your taxable portfolio — stocks, mutual funds, ETFs, PMS holdings

- Sell those positions before March 31 to convert unrealised losses into realised losses

- Apply those losses against realised gains from the same financial year

- Reinvest proceeds into similar (but not identical) securities to maintain your portfolio allocation

Current Tax Rates (Post-Budget 2024)

As amended by the Finance (No. 2) Act, 2024, the applicable rates for transfers on or after July 23, 2024 are:

| Gain Type | Rate | Threshold |

|---|---|---|

| STCG on listed equity/equity funds (Section 111A) | 20% | No exemption |

| LTCG on listed equity/equity funds (Section 112A) | 12.5% | First ₹1.25 lakh exempt annually |

These rates make harvesting especially valuable for investors with significant STCG — every rupee of STCL you book saves ₹0.20 in tax.

A Worked Example

Say you've booked ₹80,000 in STCG from selling one stock. You also hold another stock sitting at a ₹50,000 unrealised STCL.

| Scenario | Taxable Gain | Tax at 20% |

|---|---|---|

| Without harvesting | ₹80,000 | ₹16,000 |

| With harvesting | ₹30,000 | ₹6,000 |

Tax saved: ₹10,000 — by executing a sale before March 31.

Here's how to execute that in practice.

Step 1: Review Your Portfolio for Gains and Losses

Before year-end, audit your portfolio for two things: all gains already realised in the financial year, and all positions currently sitting at an unrealised loss. Both direct equities and mutual fund units qualify — so the exercise covers your entire investable portfolio, not just listed shares.

Step 2: Sell Loss-Making Assets Before March 31

The sale must be executed — not just planned — before the financial year closes. For exchange-traded securities, CBDT Circular No. 704 confirms the broker's contract-note date determines the transfer date. Once March 31 passes, those unrealised losses cannot be applied against that year's gains.

Step 3: Reinvest in Similar Securities

The goal is to register the loss for tax purposes while staying invested — not to exit the market. Use the proceeds to buy a comparable security: a different stock in the same sector, or a similar fund from a different AMC.

Avoid repurchasing the exact same security immediately after booking the loss. This can invite tax authority scrutiny on whether the transaction was a genuine transfer or a colourable arrangement to manufacture a paper loss.

Indian Capital Gains Tax Rules Every Investor Must Know

The Offsetting Hierarchy

This is the rule most commonly misunderstood:

| Loss Type | Can Offset STCG? | Can Offset LTCG? |

|---|---|---|

| Short-Term Capital Loss (STCL) | ✅ Yes | ✅ Yes |

| Long-Term Capital Loss (LTCL) | ❌ No | ✅ Yes |

Under Section 70 of the Income-tax Act, STCL can be set off against gains from any capital asset — short-term or long-term. LTCL is restricted to LTCG only. This asymmetry matters in practice when planning which losses to harvest.

Carry-Forward: Up to 8 Years — With a Catch

Losses that cannot be fully utilised in the current year can be carried forward under Section 74 for up to 8 assessment years. Carried-forward STCL can still offset both STCG and LTCG in future years; carried-forward LTCL remains restricted to LTCG.

The catch: this carry-forward benefit comes with one hard condition.

- File on time: Your ITR must be filed within the due date under Sections 80 and 139(3), read with Section 139(1)

- No late-filing relief: Miss the deadline and the right to carry forward those losses is permanently forfeited — there is no remedy after the fact

Capital Losses Cannot Offset Other Income

The carry-forward rules clarify what happens across years — but there is an equally important constraint within the same year. Under Section 71(3), capital losses — whether short-term or long-term — cannot be set off against income from any other head. Salary, business income, interest income, and rental income are all beyond reach. Only capital gains can absorb capital losses.

India's Position on Wash-Sale Style Repurchases

Unlike the US, India has no automatic wash-sale rule that disallows a loss because the same security is repurchased within a fixed window. The Income-tax Act contains targeted provisions under Section 94 for dividend stripping and bonus stripping, but no general fixed-period loss disallowance.

That said, this is not a blank clearance. The Mumbai ITAT disallowed a loss in Trends Pharma v. ITO where shares were bought and sold between related entities at artificial prices — the transaction was found to be a sham. GAAR provisions under Section 96 can also apply if an arrangement lacks commercial substance and has tax avoidance as its primary purpose.

Practical guidance: avoid immediately repurchasing the same security after booking a loss. Either wait a reasonable period or switch to a comparable but different security. The former avoids scrutiny; the latter is often the cleaner approach.

Benefits and Who It Helps Most

Financial Benefits

- Cuts current-year liability directly — at 20% on STCG and 12.5% on LTCG, every rupee of net gain eliminated has a measurable tax value

- Carries forward unused losses for up to 8 years, converting a bad position into a future planning asset

- Creates a natural trigger for annual portfolio review — identifying fundamentally weak holdings and prompting redeployment into stronger opportunities

Who Benefits Most

Tax-loss harvesting delivers the most value for:

- Active equity investors and traders with significant STCG exposure (taxed at 20%)

- Founders and promoters partially liquidating equity stakes

- CEOs and CXOs realising ESOP gains — for listed shares, the holding period starts at allotment, so 12+ months from that date determines long-term status

- UHNIs managing multi-asset portfolios with gains across multiple instruments in a single year

- NRI/OCI investors with Indian capital gains exposure, where DTAA implications, TDS obligations, and FEMA-compliant structuring add a further dimension to the planning

For investors with complex gain profiles across asset classes, a SEBI-registered investment adviser ensures the strategy is executed correctly and fits within a broader tax-efficient plan.

iVentures Wealth works with CXOs, founders, UHNIs, and NRI clients to do exactly this — coordinating with their chartered accountants so that year-end positions are structured to reflect the full picture, not just individual transactions.

When It May Not Be Appropriate

- Investors with no or minimal realised gains in the current year and limited future gain expectations

- Those in lower tax brackets where the marginal savings don't justify transaction costs

- Investors holding fundamentally strong securities at a temporary loss, where exiting costs more in forgone upside than the tax saving is worth

Common Mistakes to Avoid

Mistake 1: Letting Tax Drive Investment Decisions

Selling a security purely to book a tax loss — when it has strong long-term prospects — can cost far more in forgone gains than it saves in tax. The decision to harvest a loss should be consistent with your underlying investment view. Tax saving complements sound investing; it doesn't replace it.

Mistake 2: Ignoring the Holding Period Reset

When you sell a position and repurchase a similar security, the new lot's holding period begins on the repurchase date. What might have matured into a long-term gain (taxed at 12.5%) can be accidentally reset to short-term (taxed at 20%).

For demat holdings, FIFO applies — so partial sales may leave older lots intact, but any repurchased units start fresh. Factor this into the overall tax arithmetic before executing.

Mistake 3: Missing the ITR Filing Deadline

Failing to file your ITR by the Section 139(1) due date eliminates the ability to carry forward losses. This is not recoverable. The administrative error costs you the full value of the carry-forward — potentially across 8 future assessment years. Miss the deadline and the carry-forward benefit is gone permanently — there is no rectification route under current provisions.

Mistake 4: Assuming LTCL Can Offset STCG

Many investors overestimate the utility of their long-term losses, expecting them to offset short-term gains — they cannot. Under Section 70(3), LTCL is strictly limited to LTCG. Only STCL crosses both categories. Misclassifying your losses leads to an incorrect tax position that the tax department may flag during assessment.

Quick reference — the four mistakes that erode harvesting value:

- Prioritising tax savings over the investment thesis

- Resetting the holding period through repurchases (FIFO trap)

- Missing the ITR filing deadline and losing carry-forward eligibility

- Assuming LTCL can offset STCG (it cannot — only STCL does)

Frequently Asked Questions

What is tax-loss harvesting?

Tax-loss harvesting is selling investments at a loss to offset capital gains and reduce net tax payable in a financial year. It is a legal optimisation strategy explicitly permitted under the Income-tax Act, 1961 — not a tax avoidance scheme.

Is tax-loss harvesting worth it?

Most worthwhile for investors with significant realised capital gains, particularly STCG taxed at 20%, and available unrealised losses to offset them. Less beneficial for those with minimal gains, low tax exposure, or loss-making assets that have strong recovery potential.

Are stock losses 100% tax deductible?

Not universally. STCL can offset both STCG and LTCG; LTCL can only offset LTCG — neither applies against salary or other income. Unutilised losses carry forward for up to 8 assessment years, provided the ITR was filed on time.

What is the 30-day wash-sale rule for tax-loss harvesting?

The wash-sale rule is a US regulation that disallows a tax loss if the identical security is repurchased within 30 days. India has no equivalent statutory rule, but immediately repurchasing the same security after booking a loss may attract income tax scrutiny under substance-over-form principles.

Can short-term capital losses offset long-term capital gains in India?

Yes. Under Section 70(2), STCL can be set off against both STCG and LTCG. This makes STCL more flexible than LTCL, which is restricted solely to offsetting LTCG.

What is the deadline for tax-loss harvesting in India?

March 31 of the financial year — all sale transactions must be completed with the contract note issued before this date. Losses missed in one year cannot be backdated; they carry forward only if reported in the next ITR under applicable rules.