Introduction

Your ZIP code may be costing you more than your mortgage rate. According to the Tax Foundation's March 2026 report, property taxes accounted for 70% of local tax collections in FY2023 — making this levy the single largest source of local government funding across the United States.

Yet what surprises most buyers and long-term owners is how dramatically rates vary. A home in New Jersey can carry a tax bill four to six times higher than a comparable property in Alabama. The reason: property taxes are set at the local level — by counties, municipalities, school districts, and special taxing authorities — making your ZIP code one of the most powerful determinants of your annual bill.

For homebuyers evaluating a purchase, homeowners managing holding costs, or NRI/OCI investors with US real estate exposure, this guide breaks down the highest property tax states in 2026 — the effective rates, what's driving them, and how they affect your real cost of ownership.

Key Takeaways

- New Jersey and Illinois share the highest effective property tax rate in the US at 1.88%, based on 2024 ACS data

- Effective rate (taxes paid ÷ home value) is the most reliable cross-state metric — raw dollar amounts skew comparisons across markets with different home values

- Northeast and Midwest states dominate the high-tax list, primarily because they fund K-12 education through local property taxes

- States with no income or sales tax, such as New Hampshire and Texas, offset that revenue gap through higher property tax rates

- Homeowners can legally reduce their bill through exemptions, reassessment requests, and formal appeals

How Property Taxes Work in the US

Every property tax bill comes down to two numbers working together.

Assessed value is what your local assessor says your home is worth for tax purposes. This is often a fraction of market value — an assessment ratio. If a home sells for $400,000 and the local ratio is 60%, the assessed value is $240,000.

Millage rate is the tax applied per $1,000 of assessed value. One mill equals $1 per $1,000, so a 20-mill rate equals $20 per $1,000 — an effective 2%. Multiply assessed value by the mill rate and you have your annual bill.

Simple example: A home assessed at $250,000 with a 15-mill rate generates a $3,750 annual tax bill.

Why Rates Vary So Much

Property taxes are not administered by the federal or state government. Counties, municipalities, school districts, and special taxing authorities each set their own rates — which is why two neighboring counties in the same state can have wildly different effective burdens.

The Metric That Matters: Effective Rate

Comparing nominal millage rates across states is misleading because assessment ratios differ. The cleanest cross-state measure is the effective property tax rate: total taxes paid divided by home value. All figures here use 2024 American Community Survey (ACS) data compiled by the Tax Foundation. With that baseline in place, here's how the highest-tax states stack up.

States With the Highest Property Taxes in 2026

States below are ranked by effective property tax rate on owner-occupied homes using 2024 ACS data — actual taxes paid relative to home value, not nominal millage rates.

New Jersey — 1.88% (Tied #1)

New Jersey holds the top spot with an effective rate of 1.88%. On a median home valued at $496,000, the median annual property tax bill runs $9,358.

Seven counties — Bergen, Essex, Hunterdon, Morris, Passaic, Somerset, and Union — each show median annual property tax bills exceeding $10,000.

The driver: New Jersey funds dense, layered local government structures through property taxes. With 565 municipalities and hundreds of independent school districts, every layer of government levies its own millage — and there is no meaningful state-level offset.

| Metric | Figure |

|---|---|

| Effective Tax Rate (2024) | 1.88% |

| Median Home Value | $496,000 |

| Median Property Taxes Paid | $9,358 |

Illinois — 1.88% (Tied #1)

Illinois ties New Jersey at 1.88%, but with a much lower median home value of $280,700, the median annual tax bill comes to $5,399.

Suburban Chicago carries some of the most extreme county-level rates in the country: Lake (2.26%), McHenry (2.49%), Kendall (2.53%), DeKalb (2.33%), and Kane (2.39%) all exceed 2.2%.

Illinois funds a large share of public education through local property taxes across 102 counties, with limited state equalization. High-spending districts set high millage rates with little counterweight from Springfield.

| Metric | Figure |

|---|---|

| Effective Tax Rate (2024) | 1.88% |

| Median Home Value | $280,700 |

| Median Property Taxes Paid | $5,399 |

Connecticut — 1.54% (#3)

Connecticut sits at 1.54%, with a median home value of $396,900 and median annual taxes of $6,573. The Western Connecticut Planning Region — covering high-income suburbs — sees median property taxes approaching $9,295 annually.

Connecticut has one of the highest costs of local government in the country. Municipal service levels, teacher compensation, and infrastructure demands are funded almost entirely through town-level property taxes, with minimal state revenue sharing.

| Metric | Figure |

|---|---|

| Effective Tax Rate (2024) | 1.54% |

| Median Home Value | $396,900 |

| Median Property Taxes Paid | $6,573 |

Vermont — 1.51% (#4)

Vermont's effective rate is 1.51%, against a median home value of $352,800 and median annual taxes of $5,026. Windsor and Washington counties both carry effective rates of 1.64% — above the state average.

Vermont is unusual: it funds public education through a statewide education fund that draws heavily on property taxes. Even residents in lower-income towns face high effective rates relative to their home values because the funding structure is state-mandated rather than locally discretionary.

| Metric | Figure |

|---|---|

| Effective Tax Rate (2024) | 1.51% |

| Median Home Value | $352,800 |

| Median Property Taxes Paid | $5,026 |

New Hampshire — 1.50% (#5)

New Hampshire rounds out the top five at 1.50%, with a median home value of $458,800 and median annual taxes of $6,707. Hillsborough County carries an effective rate of 1.66%; Cheshire County reaches 1.87%.

New Hampshire levies no broad-based state income tax and no sales tax. Property taxes carry almost the entire weight of local government funding — New Hampshire levies no broad-based state income tax and no sales tax. Property taxes carry almost the entire weight of local government funding. This deliberate policy choice shows up directly in the effective rate.

| Metric | Figure |

|---|---|

| Effective Tax Rate (2024) | 1.50% |

| Median Home Value | $458,800 |

| Median Property Taxes Paid | $6,707 |

States Ranked 6 Through 10

The next tier includes states from the Midwest, Plains, and one notable Sun Belt outlier. Texas stands out: despite being a low-income-tax state in the South, its effective property tax rate of 1.40% exceeds most of its regional neighbors precisely because local governments compensate through millage.

| Rank | State | Effective Rate | Median Home Value | Median Annual Taxes |

|---|---|---|---|---|

| 6 | Nebraska | 1.44% | $263,100 | $3,739 |

| 7 | Texas | 1.40% | $313,200 | $4,108 |

| 8 | Ohio | 1.36% | $239,800 | $2,937 |

| 9 | Iowa | 1.33% | $227,300 | $2,937 |

| 10 | Wisconsin | 1.32% | $294,700 | $3,680 |

Source: Tax Foundation, Property Taxes by State and County, 2026 using 2024 ACS data

Why Are Property Taxes So High in These States?

Education Funding Structure

In most high-tax states, K-12 public schools are funded primarily through locally collected property taxes rather than state-distributed revenue. This creates a direct, visible link between school quality and homeowner tax burden. Because school district spending is politically popular and legally protected, reforming the funding mechanism is extremely difficult — even when voters recognize the cost.

Absence of Competing Revenue Sources

States that forgo a state income tax must generate equivalent revenue somewhere else. New Hampshire and Texas are the clearest examples — both rely heavily on property taxes to substitute for income tax revenue. This is the tax substitution effect: reduce one revenue stream and another rises to fill the gap.

Assessment Lag and Rising Bills

US home prices rose 54.4% nominally from January 2020 through July 2024, according to Tax Foundation analysis. Because assessments are updated periodically — often every few years rather than annually — many homeowners are now receiving reassessments that reflect those peak values, even as the broader housing market has cooled. The result: property tax bills continue climbing in 2025-2026 even where home prices have stalled.

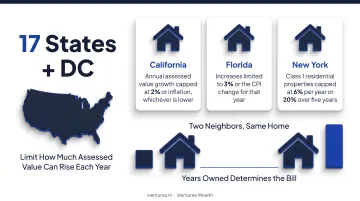

Assessment Caps and Unintended Shifts

Roughly 17 states plus DC have laws limiting how much a property's assessed value can rise annually. State caps vary significantly in how aggressively they protect homeowners:

- California: Annual assessed value growth capped at 2% or inflation, whichever is lower

- Florida: Increases limited to 3% or the CPI change for that year

- New York: Class 1 residential properties capped at 6% per year or 20% over five years

These caps protect long-time owners — but shift burden onto new buyers, who are assessed at current market value upon purchase. Two neighbors in identical homes can face dramatically different tax bills depending solely on how long they've owned.

How to Lower Your Property Tax Bill

Three approaches work. They require some effort but are entirely legal and widely underused.

1. Request a Formal Reassessment or Appeal

If you believe your home has been overvalued, you can contest the assessment through your local assessor's office. The general process:

- Request your current assessment record — verify the property details are accurate (square footage, bedroom count, lot size)

- Gather comparable sales data — find recent sales of similar homes in your neighborhood that sold below your assessed value

- File within the appeal window — most jurisdictions require a challenge within a defined period after the assessment notice is mailed; this window is often narrow, so act promptly

- Attend the hearing or submit documentation — the burden is on you to demonstrate the overvaluation

2. Apply for Available Exemptions

Many states and localities reduce the taxable value of a home for qualifying owners. Common categories include:

- Homestead exemption — for owner-occupants as a primary residence; 48 states and DC offer some form of homestead relief

- Senior exemption — age-based programs (typically 65+) that reduce assessed value or cap tax liability

- Military veteran exemption — often conditioned on disability rating, service period, or deployment status

- Disability exemption — for homeowners meeting defined disability criteria

Eligibility rules and amounts vary widely by state and county. Check your county assessor's website for current programs and application deadlines.

3. Monitor Your Assessment Notice

The annual assessment notice — or the notice following a periodic reassessment — is the trigger for any challenge. Most jurisdictions impose a strict filing deadline from the date of that notice. Missing it forfeits your right to appeal for that cycle.

When your notice arrives:

- Don't discard it — file it immediately and note the appeal deadline

- Check the assessed value against recent comparable sales in your neighborhood

- Act within the filing window if your assessed value exceeds what similar homes have sold for in the area

Conclusion

Property taxes are among the most significant recurring costs of homeownership — and among the least analyzed when buyers run their numbers. For anyone comparing markets across state lines, the effective property tax rate belongs in the financial model alongside mortgage payment, insurance, and maintenance.

For NRI/OCI investors and UHNIs with US real estate holdings, the picture is more complex. Property tax obligations vary not just by state but by county, and they interact directly with rental yields, capital gains treatment, and after-tax return projections.

A property generating a 6% gross yield in a high-tax Illinois suburb may deliver a materially different net return than the same yield in a lower-tax state — a distinction that only shows up when you model the full tax picture.

That's where advisory context makes the difference. iVentures Wealth works with NRI/OCI clients to build a complete picture of US real estate exposure within a broader wealth framework. This includes:

- DTAA structuring to manage cross-border tax obligations

- Cross-border tax coordination across Indian and US jurisdictions

- Multi-jurisdictional portfolio analysis to model net returns accurately

To discuss your US real estate holdings in detail, reach out to the team at wealth@iventures.in.

Frequently Asked Questions

Which states have the highest property taxes in the US?

New Jersey and Illinois share the top position at a 1.88% effective rate, based on 2024 ACS data. They are followed by Connecticut (1.54%), Vermont (1.51%), and New Hampshire (1.50%). These figures reflect actual taxes paid on owner-occupied homes relative to home value.

How much are property taxes on a $1,000,000 house in Texas?

At Texas's 1.40% effective rate, annual property taxes on a $1,000,000 home would run approximately $14,000. Actual amounts vary by county and local jurisdiction. Texas levies no state income tax, which is the primary reason its property tax rates exceed those of most other Sun Belt states.

Which states have the lowest property taxes?

Hawaii (0.29%) and Alabama (0.37%) consistently rank at the bottom for effective property tax rates. One caveat on Hawaii: median home values there are among the highest in the country, so dollar tax bills can still be meaningful in absolute terms.

Can you deduct property taxes on your federal income tax return?

Yes. Under the SALT (State and Local Tax) deduction, homeowners may deduct qualifying state and local taxes — including property taxes — on their federal return. For tax year 2025, the deduction limit has been raised to $40,000 ($20,000 for married filing separately), subject to an income phase-down — especially impactful for residents of high-tax states like New Jersey and Illinois.

What happens if you don't pay property taxes?

Unpaid property taxes trigger penalties and interest, and the taxing authority can place a lien on the property. If the debt goes unresolved beyond the statutory window, the government can foreclose — even with no outstanding mortgage. Timelines vary by state, but the core mechanism is the same nationwide.

Do property taxes go up every year?

Not automatically — but they tend to rise over time as assessed values increase during periodic reassessments and local governments adjust millage rates to cover rising service costs. Homeowners can challenge increases by appealing their assessed value through their local assessor's office within the applicable appeal window.