Introduction

Picture this: an NRI returns to India for a family visit and casually checks their old savings account — only to discover it's been non-compliant for years. Or they've been collecting rental income from a property in Delhi without realising it should be routed through an NRO account, not a regular savings account. These aren't rare oversights. They're among the most common FEMA violations NRIs unknowingly commit.

The Foreign Exchange Management Act, 1999 governs how Indian citizens residing abroad manage their financial ties to India — from bank accounts and investments to property ownership and fund repatriation. Getting these rules wrong can result in penalties, account freezes, or even legal proceedings under FEMA.

This guide covers what you need to know:

- How FEMA defines NRI status and residential classification

- Which bank accounts NRIs are permitted to hold

- What you can and cannot invest in under FEMA

- Repatriation limits and remittance rules

- Compliance requirements that carry the highest risk

Key Takeaways

- FEMA defines NRI status by residence and purpose of stay, not by a fixed day count

- Regular Indian savings accounts must be converted to NRO accounts upon acquiring NRI status

- NRIs can invest in listed equities, mutual funds, and real estate, though PPF and agricultural land remain off-limits

- NRO repatriation is capped at USD 1 million per financial year; NRE and FCNR accounts allow full repatriation

- FEMA penalties can reach three times the sum involved, with additional daily continuing penalties

Who Qualifies as an NRI Under FEMA?

The FEMA Definition

Under FEMA, an NRI is defined under Regulation 2 of FEMA Notification No. 13 (May 3, 2000) as a person resident outside India who is a citizen of India. The controlling test is based on residence and purpose — whether you've left India for employment, business, profession, or circumstances indicating an indefinite stay abroad.

FEMA Section 2(v) does reference 182 days, but the purpose and intention of stay override a mechanical day count. This is where many NRIs get confused.

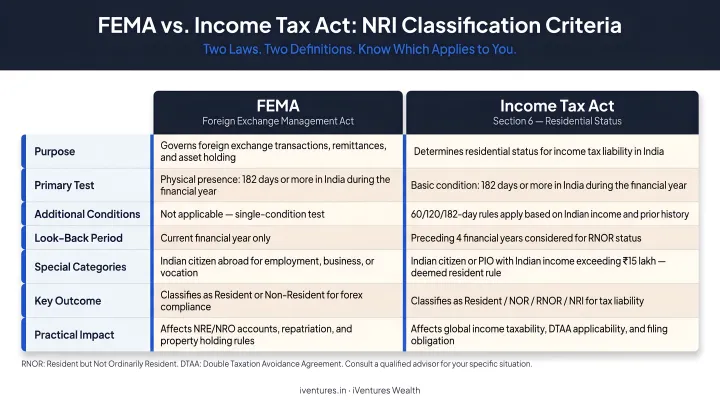

FEMA vs. Income Tax Act: A Critical Distinction

| Criterion | FEMA | Income Tax Act |

|---|---|---|

| Basis | Residence + purpose of stay | Day count (182-day rule) |

| Threshold | No fixed day count | Present in India <182 days in a financial year |

| Key question | Why are you living abroad? | How many days were you in India? |

Example: An Indian professional moves to Dubai for a 3-year employment contract. Under FEMA, she becomes a non-resident from the day she leaves with employment intent — even if she visited India for 100 days that year. Under the Income Tax Act, she would still be a resident for that year if she spent 182+ days in India. Same person, different status under each law.

Treating these two frameworks as interchangeable is where compliance errors typically begin — misclassified bank accounts, incorrect TDS deductions, and avoidable FEMA penalties are all common consequences.

OCI Status Under FEMA

Overseas Citizens of India (OCIs) — foreign citizens of Indian origin — are treated at par with NRIs for most investment and property purposes under FEMA. SEBI's investor materials confirm that OCI investments in securities follow the same rules, and the RBI's immovable property FAQs are framed for "NRI/OCI" jointly under the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019.

That said, certain distinctions do apply — particularly around repatriation documentation and country-specific restrictions that may affect OCIs differently from Indian citizen NRIs.

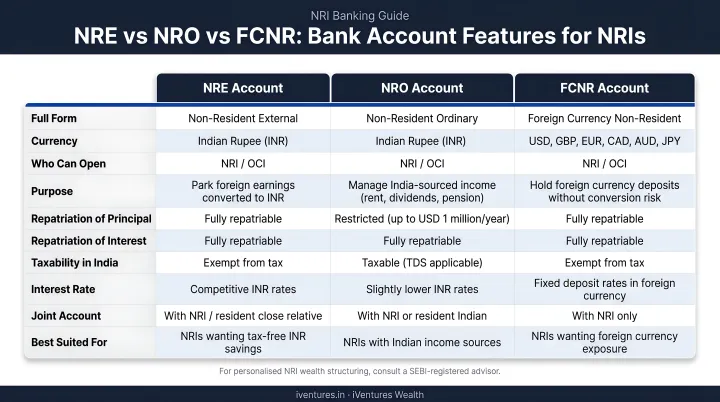

NRI Bank Accounts Under FEMA: NRE, NRO, and FCNR Explained

The Account Conversion Requirement

Under FEMA, NRIs cannot hold a regular resident savings account in India after acquiring NRI status. Any existing savings account must be redesignated as an NRO account or closed. Continuing to hold a regular savings account is one of the most common — and easily avoidable — FEMA violations.

Side-by-Side Comparison

| Feature | NRE Account | NRO Account | FCNR(B) Account |

|---|---|---|---|

| Currency | INR | INR | Foreign currency (USD, GBP, EUR, etc.) |

| Income source | Foreign-earned | India-sourced (rent, dividends, pension) | Foreign-earned |

| Repatriability | Fully repatriable | Capped at USD 1 million/year | Fully repatriable |

| Tax on interest | Tax-free in India | Taxable in India | Tax-free in India |

| Best for | Parking foreign income in India | Managing India-sourced income | Avoiding INR exchange rate risk |

Account Details

NRE (Non-Resident External): The key compliance point: interest is fully exempt under Section 10(4)(ii) of the Income Tax Act, so no Indian tax filing obligation arises on NRE interest income.

NRO (Non-Resident Ordinary): The repatriation ceiling of USD 1 million per financial year requires CA certification (Form 15CA/15CB) and proof of tax compliance before funds can be moved abroad — a step NRIs frequently overlook.

FCNR(B) (Foreign Currency Non-Resident): Held in foreign currency (USD, GBP, EUR, and others), this term deposit protects you from INR depreciation risk — the deposit matures in the same currency you put in, with no exchange rate loss on principal or interest.

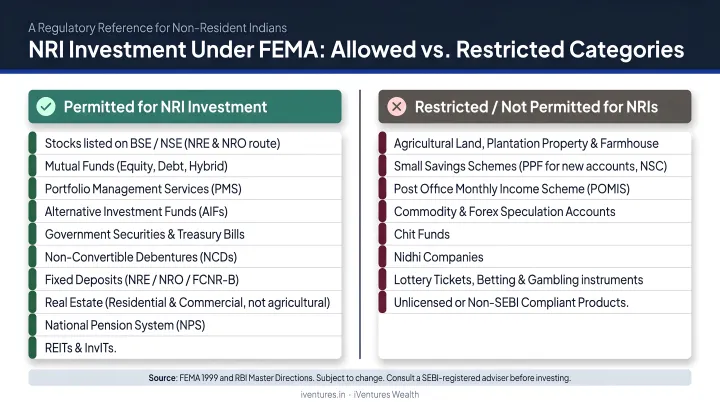

FEMA Rules for NRI Investments in India

What NRIs Can Invest In

NRIs have access to a broad range of regulated investment options:

- Listed equities via the Portfolio Investment Scheme (PIS) route through an RBI-approved Authorised Dealer bank

- Mutual funds through NRE or NRO accounts (direct plans are permitted)

- Government securities and bonds, including select NCDs and listed bonds

- Residential and commercial real estate

- Indian startups and companies under the Foreign Direct Investment (FDI) framework

Investment Restrictions

Several instruments are off-limits after acquiring NRI status:

- PPF accounts cannot be opened by NRIs — only resident citizens qualify. If you held a PPF account before becoming an NRI, it may continue until maturity under Government Savings Promotion General Rules, 2018, but no extension is permitted thereafter

- Small savings schemes are similarly restricted to resident citizens

- Intraday trading and short selling are not permitted — all equity transactions must be delivery-based

- Individual NRI holding cannot exceed 5% of paid-up capital of any single listed Indian company; the aggregate NRI/OCI ceiling is 10%

The PIS Route for Equities

To invest in listed Indian equities, NRIs must open a designated PIS bank account linked to their NRE or NRO account, along with a demat account. All purchases and sales are reported to the RBI through the Authorised Dealer bank. This ensures regulatory oversight and accurate tracking of NRI investment limits across companies.

FDI: Repatriation vs. Non-Repatriation Basis

NRIs can invest in Indian companies and startups through two routes:

- Repatriation basis — Investment made from NRE/FCNR funds. Both capital and returns can be freely repatriated abroad

- Non-repatriation basis — Investment made from NRO funds. Capital and gains remain in India and cannot be freely remitted abroad without meeting the USD 1 million annual cap

DTAA and Tax Planning

India has entered into Double Taxation Avoidance Agreements with numerous countries — the Income Tax Department lists 191 DTAA notification items. For NRIs, these treaties can reduce or eliminate double taxation on Indian investment income, including dividends, interest, and capital gains.

DTAA planning is complex and jurisdiction-specific. For NRIs managing India investments from the US, UK, UAE, Singapore, or Canada, working with an adviser experienced in cross-border structuring matters. iVentures Wealth (SEBI RIA: INA000019026) works with NRI and OCI clients on DTAA-aligned portfolio structuring, Form 15CA/15CB compliance, and TDS planning across jurisdictions — for those with investable assets above ₹5 Crores.

Property Ownership and Repatriation Under FEMA

What NRIs Can Buy

NRIs can purchase residential and commercial property in India — either directly or through inheritance. There is no cap on the number of such properties they can hold.

Prohibited Property Categories

A widely misunderstood rule: NRIs cannot purchase agricultural land, plantation property, or farmhouses in India. However, they can inherit or receive these as gifts from relatives — the restriction applies only to purchase transactions. Many NRIs assume inherited agricultural land is also restricted; it is not.

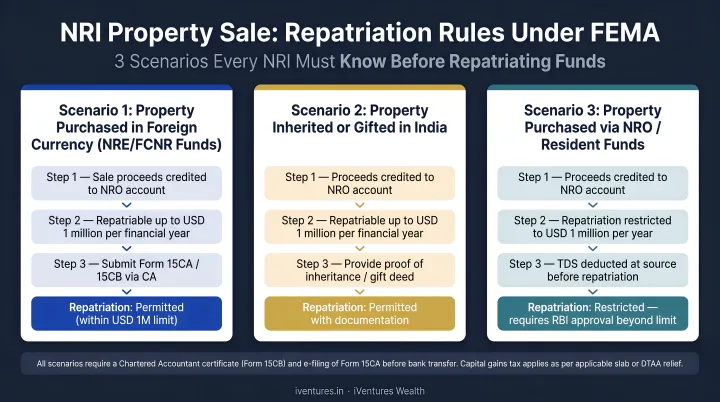

Repatriation of Property Sale Proceeds

The repatriation framework depends on how the property was originally purchased:

- Properties bought using NRE/FCNR funds: Sale proceeds can be repatriated abroad for up to two residential properties, provided the repatriation does not exceed the original foreign exchange amount paid

- Properties bought using NRO or INR funds: Proceeds are credited to the NRO account and can be repatriated within the USD 1 million annual cap

- Inherited property: NRIs can repatriate up to USD 1 million per financial year from the sale of inherited immovable property, subject to documentation

Inherited Property: Documentation and Restrictions

For repatriation of inherited property sale proceeds, the following documentation is typically required:

- Proof of inheritance (will, succession certificate, or similar)

- Certificate from a Chartered Accountant

- Undertaking to the Authorised Dealer bank

Beyond documentation, there is a nationality-based restriction that applies across all property categories: citizens of Pakistan, Bangladesh, Sri Lanka, Afghanistan, China, Iran, Nepal, or Bhutan cannot repatriate property sale proceeds without specific RBI approval. This applies regardless of NRI status under FEMA.

Key Compliance Requirements and Common FEMA Mistakes

Essential Compliance Checklist

- ✅ Maintain current KYC documentation with your Authorised Dealer bank

- ✅ Use correct purpose codes for all foreign exchange transactions

- ✅ File Form 15CA and 15CB for applicable remittances (Form 15CB is required when remittance or aggregate remittance exceeds ₹5 lakh in a financial year and is chargeable to tax)

- ✅ Route all forex dealings exclusively through RBI-authorised channels

- ✅ Review investment holdings against FEMA restrictions periodically

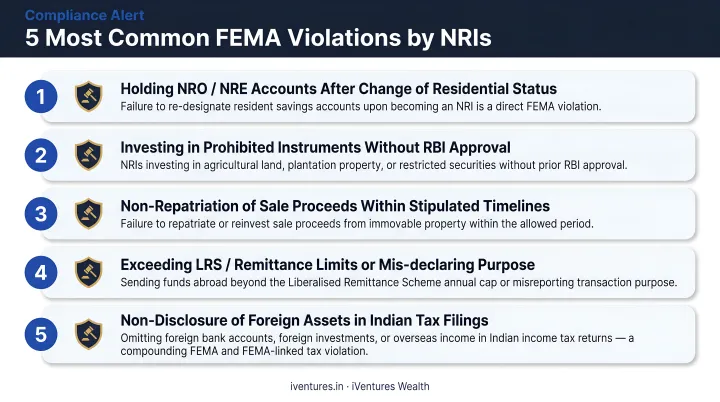

Common FEMA Violations by NRIs

These are the violations that come up most often — and most are avoidable with proper guidance:

- Holding a regular savings account after acquiring NRI status (must be converted to NRO)

- Continuing or extending PPF contributions after becoming an NRI

- Failing to set up an NRO account for India-sourced income like rent or dividends

- Not converting back to RFC (Resident Foreign Currency) accounts upon permanent return to India — RFC is the correct vehicle for returning NRIs to hold eligible foreign-currency assets

- Not declaring Indian assets under applicable reporting obligations in the country of residence

FEMA Penalties

Under Section 13 of FEMA, penalties can reach:

- Up to three times the sum involved where the amount is quantifiable

- Up to ₹2 lakh where the sum cannot be quantified

- ₹5,000 per day as a continuing penalty for each day the violation persists

A periodic compliance review is the most practical safeguard — especially when your residency status changes, you sell Indian property, or you start receiving India-sourced income. iVentures Wealth's NRI advisory team works with clients to identify and resolve compliance gaps early, coordinating with Authorised Dealer banks and tax advisors across jurisdictions.

Frequently Asked Questions

Which NRI account allows full repatriation?

Both NRE and FCNR(B) accounts allow full, unrestricted repatriation of principal and interest with no annual cap. NRO accounts are subject to a USD 1 million per financial year limit, with documentary evidence and tax compliance required before remittance is permitted.

What is the difference between NRI and PIO as per FEMA?

Under FEMA, an NRI is an Indian citizen residing outside India. A PIO (Person of Indian Origin) was a foreign citizen of Indian descent, though the category has largely been superseded by OCI (Overseas Citizen of India) status, which now provides similar rights for most investment and property transactions.

What is the new rule for NRI in India?

FEMA and RBI regulations applicable to NRIs are updated periodically through RBI circulars and master directions. Recent updates include changes to FCNR(B) interest rate frameworks and amendments to the Foreign Exchange Management (Non-Debt Instruments) Rules. Check the RBI's official FAQs and Master Directions or consult a qualified adviser for the most current guidance.

What is the FEMA definition of NRI?

FEMA defines an NRI as a person resident outside India who is a citizen of India, based on permanent residence or purpose of stay (employment, business, or profession abroad). This differs from the Income Tax Act, which uses a day-count threshold of fewer than 182 days in a financial year.

Can NRIs invest in mutual funds and stocks in India under FEMA?

Yes. NRIs can invest in listed equities via the PIS route and in mutual funds through designated NRE or NRO accounts. Some mutual fund houses do not accept investments from US- and Canada-based NRIs due to FATCA compliance obligations, so check individual fund house requirements before investing.

What are the penalties for FEMA violations by NRIs?

FEMA violations attract penalties of up to three times the amount involved, or ₹2 lakh where the sum is not quantifiable, plus a daily penalty of ₹5,000. Proactively rectifying common violations — such as holding a resident savings account — is far less costly than enforcement.