The stakes are real. India's life expectancy has risen to 72.2 years, and urban Indians who reach 60 can expect to live another 19.6 years on average. That's nearly two decades of expenses without a salary.

There is no single correct corpus figure. The right number depends on your lifestyle, city, retirement age, health situation, dependents, and passive income sources. This article breaks down realistic corpus ranges for Indian retirees, the variables that shape those ranges, proven calculation methods, and the planning mistakes that leave retirees financially exposed.

Key Takeaways

- Your corpus must sustain 20–30 years of expenses; retiring earlier means you need significantly more

- The 25x rule is a useful starting point, but India's higher inflation may require a 28–33x multiplier

- Healthcare, lifestyle inflation, and longevity are the three most underestimated variables

- Passive income from EPF, NPS, rental yield, and dividends reduces how much corpus you actually need to draw down

- Build your retirement number around your actual expenses, income sources, and expected lifespan — not a generic formula

How Much Corpus Do You Need? Realistic Ranges for Indian Retirees

A retirement corpus is the total savings required to fund all post-retirement expenses without depleting capital before the end of life. Undershoot it and you outlive your savings. Overshoot it and you sacrifice present quality of life unnecessarily.

The right starting point is your current monthly expenditure. From there, you inflate that figure to your retirement date, multiply by your expected retirement horizon, and add buffers for healthcare and contingencies.

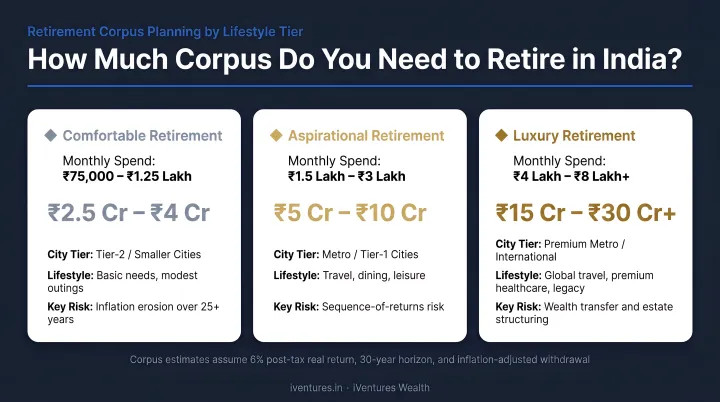

Corpus Ranges by Retirement Lifestyle

The table below uses illustrative monthly expense inputs and applies the 25x annual expense rule, assuming retirement at 60 with a 25-year horizon and India's long-term inflation. These are starting-point calculations, not guarantees.

| Lifestyle Tier | Monthly Expense (Today) | Indicative Corpus Required |

|---|---|---|

| Basic/Frugal (Tier 2/3 city, minimal expenses) | ₹50,000 | ₹1.5 crore |

| Comfortable/Moderate (metro or semi-metro) | ₹1,00,000 | ₹3 crore |

| Affluent/UHNI (urban, travel, comprehensive healthcare, legacy) | ₹3,00,000+ | ₹9 crore+ |

What each tier typically covers:

- Basic tier: Groceries, utilities, modest healthcare, no help at home. Suits individuals or couples in smaller cities with pension income supplementing the corpus.

- Moderate tier: Full household expenses, routine medical care, occasional domestic travel, some leisure. Typical for metro couples without pension income.

- Affluent tier: Comprehensive health coverage, international travel, family support, legacy corpus. For urban HNIs and UHNIs with broader financial obligations.

These ranges assume retirement at 60. Those retiring at 45 or 50 need a significantly larger corpus to cover the extended horizon — sometimes 30–35 years or more.

Couples typically need 1.5–1.8x a single person's corpus, not double — shared household costs reduce the per-head requirement considerably.

Key Factors That Determine Your Retirement Corpus

Your retirement corpus depends on a mix of personal, financial, and environmental variables — and four of them move the number more than anything else.

Retirement Age and Post-Retirement Duration

Retirement age is the single most consequential variable in corpus planning. Consider the difference:

- A person retiring at 45 may need to fund 40+ years without active income

- A person retiring at 60 typically plans for 20–25 years

- A person retiring at 65 may only need 15–20 years of corpus coverage

The impact compounds twice: earlier retirees have fewer working years to accumulate savings, and far longer drawdown periods to manage. This is why FIRE planning requires not just discipline in saving, but a fundamentally larger corpus target than conventional retirement.

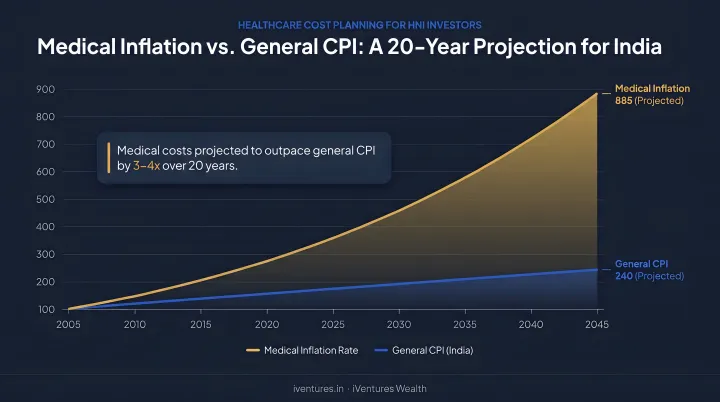

Inflation — Especially Healthcare Inflation

India's long-term consumer price inflation has averaged ~6.5% annually between 2004 and 2024, according to World Bank CPI data. The compounding effect is severe:

- ₹1 lakh in monthly expenses today becomes approximately ₹2.58 lakh per month in 15 years

- At 20 years, the same expense climbs to ₹3.55 lakh per month

Healthcare inflates significantly faster. Milliman's research on India's medical trend reported medical cost inflation at 12% in 2024, projected to hit 13% in 2025 — more than triple the general CPI rate. That same ₹1 lakh in monthly medical costs becomes over ₹9.65 lakh per month in 20 years if medical inflation holds at 12%.

Most retirement plans model a single blended inflation rate. That assumption quietly erodes purchasing power — which is why healthcare costs deserve a separate, higher inflation assumption in any serious corpus calculation.

Lifestyle Expectations, Location, and Legacy Goals

Post-retirement lifestyle choices create dramatically different corpus requirements:

- Downsizing to a Tier 2 city can reduce monthly expenses by 30–40% compared to metro living

- International travel of even two trips per year adds ₹8–15 lakh annually at current costs

- Supporting adult children financially is common in India but rarely quantified in corpus estimates

- Legacy goals — leaving wealth for heirs or a charitable corpus — are priorities for many affluent retirees but often handled informally rather than as a formal corpus tranche

Post-Retirement Income Sources and the Income Gap

Reliable passive income directly reduces the amount your corpus must cover each year.

Annual corpus draw = Projected annual expenses − Projected passive income

Sources that reduce this gap include:

- EPF (earning 8.25% for FY 2024-25)

- PPF (earning 7.1% for April–June 2026)

- NPS annuity (40% of corpus mandatorily annuitised at exit)

- Rental income from investment properties

- Dividend income, REIT distributions, bond interest

- Corporate pension if applicable

Once you know the annual gap, you apply the 25x multiplier (or a more conservative 28–33x for India) to arrive at the corpus that must actively fund your retirement.

What Does Your Retirement Corpus Need to Cover?

A retirement corpus has to do more than fund monthly expenses. It needs to absorb both predictable recurring costs and sudden, large one-time events — across what could be 25 to 35 years of post-retirement life.

Recurring Expenses (Inflation-Adjusted Over the Horizon)

- Daily living: Groceries, utilities, household help, transport

- Healthcare: Insurance premiums (IRDAI-capped at 10% annual hike for senior citizens), treatments, specialist visits, elder care facilities

- Housing: Maintenance, property taxes, possible rent if relocating

- Leisure and travel: Domestic or international trips, entertainment, hobbies

- Family support: Regular gifting, children's annual needs, festival expenses

One-Time Costs (Often Underestimated)

These can cause sharp, unexpected drawdowns if not budgeted separately:

- Major medical procedures (cardiac, orthopaedic, oncology)

- Home renovation or relocation costs

- Children's or grandchildren's weddings

- Assisting adult children during financial difficulty

- Legal costs for succession and estate matters

Earmark a 15–20% contingency buffer within your total corpus for these events — kept separate from your regular drawdown pool. A practical approach is to park this in liquid funds or short-duration debt instruments, so the money is accessible without disrupting your long-term allocation when an unplanned need arises.

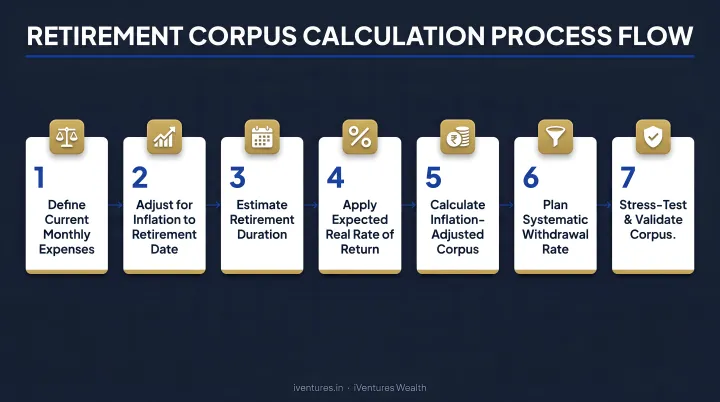

How to Estimate Your Retirement Corpus

Several widely-used methods help estimate your target corpus. Each works best when adapted to your income structure, lifestyle, and retirement timeline.

The 25x Annual Expense Rule and the 4% Framework

The 25x rule works as follows: calculate your expected annual retirement expenses and multiply by 25. The result is a corpus that can theoretically sustain a 4% annual withdrawal rate over approximately 30 years.

The 4% rule originates from William Bengen's 1994 research using US historical market data. It has a critical limitation in the Indian context: it was calibrated to US inflation, not India's. Given India's higher long-term CPI (~6.5%) and medical inflation (~12%), a more conservative 3–3.5% withdrawal rate is warranted for Indian retirees — which implies a 28–33x multiplier for the same lifestyle sustainability.

The Inflation-Adjusted Projection Method

This step-by-step approach produces a more accurate estimate:

- Calculate current monthly expenses — include EMIs, utilities, discretionary spending, and lifestyle costs

- Remove expenses that end at retirement (commuting costs, work clothing, children's school or college fees)

- Add retirement-specific expenses (healthcare buffer, leisure, travel, domestic help)

- Inflate the resulting figure to your retirement date using ~6.5% annual inflation

- Multiply by 12 to get your annual retirement need

- Multiply by expected retirement years (minimum 25, ideally 30)

- Add a 15–20% contingency buffer for unplanned costs

Here's how that plays out in practice — current monthly expenses of ₹80,000, retiring in 15 years, with a 25-year post-retirement horizon:

- Inflated monthly expense at 6.5% over 15 years: ~₹2.06 lakh/month

- Annual need: ~₹24.7 lakh

- 25-year total: ~₹6.2 crore

- Add 20% buffer: ~₹7.4 crore required corpus

Calculating the Gap and Monthly Savings Required

Once you have a target corpus:

- Project the future value of existing retirement savings (EPF, PPF, mutual funds, NPS) at retirement using a realistic return assumption

- Subtract this from the required corpus — the difference is your savings gap

- Reverse-engineer the monthly SIP or investment needed to close that gap over your remaining working years

This gap analysis is where most DIY retirement plans fall short. The numbers look clean on a spreadsheet, but real-world variables — portfolio mix, tax drag, withdrawal sequencing — can shift the outcome significantly.

iVentures Wealth's advisors build retirement corpus plans that account for current portfolio composition, tax efficiency, risk tolerance, and legacy goals. For clients targeting early retirement, the firm also applies glide-path planning in the five years before the retirement date to reduce exposure to sequence-of-returns risk.

Common Mistakes That Leave Retirees Short

Planning for a Shorter Life Than You May Live

India's SRS data shows that life expectancy at age 60 is 18.1 years nationally and 19.6 years for urban Indians. Many people plan for 15–20 years of retirement, underestimating the actual horizon. The financial consequence of outliving your corpus is severe: 40% of Indians surveyed by PGIM India in 2025 feared they would outlive their savings.

The solution: plan for a minimum 30-year post-retirement horizon regardless of current health.

Ignoring Healthcare Cost Inflation

A longer retirement also means more years of medical exposure — and healthcare costs compound faster than most budgets account for. Most retirees budget healthcare at current rates. Given 12% annual medical inflation, a health budget that looks adequate today will likely fall short a decade later. Two adjustments help:

- Secure comprehensive senior health coverage before retirement, not after a diagnosis

- Build a dedicated healthcare buffer within the corpus, separate from general living expenses

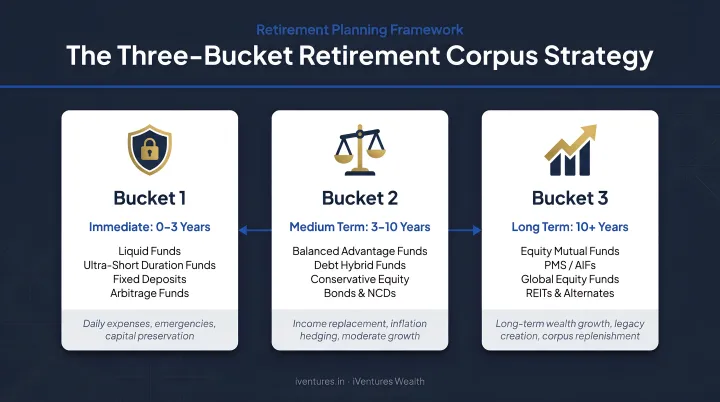

Locking the Entire Corpus in Low-Yield or Illiquid Instruments

Fixed deposits, physical gold, and residential real estate provide security but often lag inflation over long periods. Structure the corpus across three buckets:

- Safety bucket (5–7 years of expenses): High-quality fixed income for near-term needs

- Stability bucket (8–15 year horizon): Balanced, asset-allocated portfolio

- Growth bucket: Equity, AIF, or other growth assets for long-term appreciation

Each bucket serves a different time horizon — so a market downturn never forces you to sell growth assets to cover monthly expenses.

Conclusion

No single number defines the right retirement corpus. The figure that works for a frugal retiree in Indore is very different from what a metro-based couple with legacy goals requires. What matters is having a structured, inflation-adjusted estimate — built on your actual expenses, passive income, and retirement timeline — that you revisit annually as life changes.

The goal is a corpus that doesn't just survive the first decade of retirement but sustains quality of life through all of it. That means addressing several moving parts before you stop drawing a salary:

- Starting accumulation early enough for compounding to do real work

- Allocating across asset classes to balance growth and stability

- Building in a healthcare buffer that accounts for medical inflation

- Planning for 25–30 years of longevity, not just 10–15

- Leaving room for the unexpected — family needs, market downturns, lifestyle shifts

Getting these variables right is harder to do alone. A fiduciary advisor can stress-test your corpus assumptions, model different scenarios, and flag gaps before they become problems — so your retirement plan holds up not just on paper, but across decades.

Frequently Asked Questions

How much corpus is required for retirement?

The required corpus depends on your expected annual expenses and retirement horizon. Multiply your annual retirement expenses by 25 as a baseline — this is the 25x rule. Given India's inflation rate, many planners recommend a 28–33x multiplier for greater sustainability over a 25–30 year retirement.

What is the 4% rule and does it apply to Indian retirees?

The 4% rule suggests withdrawing 4% of your corpus annually to make it last roughly 30 years. It was based on US market and inflation data, so Indian retirees — facing higher CPI and healthcare inflation — should consider a more conservative 3–3.5% withdrawal rate, implying a larger corpus for the same lifestyle.

How does inflation affect my retirement corpus?

At India's historical average inflation of ~6.5%, monthly expenses roughly double in 15 years and triple in 25 years. Healthcare inflates at approximately 12% annually — far faster than general costs — so a corpus that looks adequate today can run dry well before your retirement does.

At what age should I start building my retirement corpus?

Starting in your 20s gives compounding the most runway and dramatically reduces your monthly savings burden. Starting a decade later requires investing 2–3x more per month to reach the same corpus target by retirement.

Is ₹1 crore enough for retirement in India?

For most metro retirees, ₹1 crore is unlikely to sustain a 25–30 year retirement. Scenario modelling shows that even at ₹50,000/month in expenses with 6% annual inflation, ₹1 crore lasts less than 17 years — and that's before accounting for medical emergencies or healthcare cost escalation.

Should I count my home as part of my retirement corpus?

A self-occupied property does not generate income and should not be counted as part of your liquid retirement corpus. Only accessible, income-generating assets count: mutual funds, bonds, EPF, NPS, REITs, and rental properties that actually fund your withdrawals.