Introduction

India currently has no inheritance or estate tax. The Estate Duty Act was repealed in 1985, and the Finance Bill 2024 contained no provision to revive it. Yet wealthy families who treat this as the end of the conversation are making a costly assumption.

Capital gains on inherited assets, stamp duty on property transfers, succession disputes, and probate delays create real financial drag — even without a formal inheritance tax.

For NRI and OCI families with assets in the US or UK, the exposure is more direct. The US applies estate tax to non-resident aliens holding US-sited assets above $60,000, and the UK levies 40% inheritance tax on UK-sited assets regardless of the owner's domicile.

This article covers what inheritance tax planning actually means, why it matters for Indian families today, the core strategies available, the cross-border risks NRIs face, and the mistakes most likely to cost your heirs.

Key Takeaways:

- India has no inheritance tax, but capital gains, stamp duty, and legal costs still erode inherited wealth

- NRIs with US or UK assets face direct estate/inheritance tax exposure above very low thresholds

- Trusts, gifting programs, HUF structures, and life insurance are the primary planning tools

- A nominee on a financial account is not a legal heir — misaligned designations routinely trigger disputes

- Structures set up shortly before death can be challenged; early planning is the only reliable approach

What Is Inheritance Tax Planning?

Inheritance tax planning is the deliberate process of structuring assets, ownership, and transfers so that heirs receive as much of the estate as possible — with minimal erosion from taxes, legal fees, or disputes.

This is distinct from routine tax saving. It operates across a much longer horizon — planning for what happens to wealth once the wealth creator is no longer there to manage it.

Two Concepts Worth Distinguishing

- Estate tax is levied on the total estate before assets are distributed to heirs

- Inheritance tax is paid by the beneficiary on what they receive

India abolished estate duty in 1985 and has neither today. The US, UK, and several other countries still impose one or both. For Indian families with connections abroad, this distinction matters enormously.

Why Planning Still Matters Without an Inheritance Tax

Even with no formal inheritance tax, Indian families face real succession costs:

- Capital gains tax on inherited equities, mutual funds, or real estate when eventually sold — the heir's cost basis is set at the original owner's purchase price under Section 49 of the Income Tax Act

- Stamp duty on property transfers, which varies significantly by state

- Income tax on interest or rent earned by the estate during the settlement period

- Probate and legal fees, often extending years in contested estates

The capital gains exposure can be substantial. An heir who inherits shares bought decades ago at ₹10 and sells at ₹500 faces tax on virtually the entire gain. At post-Budget 2024 rates, that means 12.5% LTCG on listed equity above ₹1.25 lakh, or 20% STCG if sold within the holding period.

The Indian Tax and Legal Landscape: Why Planning Still Matters

The Hindu Succession Act and Intestate Risk

For most Indian Hindu families, the Hindu Succession Act, 1956 governs how assets are distributed when someone dies without a valid will. The Act also covers Buddhists, Jains, and Sikhs.

Intestate succession can produce outcomes that directly conflict with the wealth creator's intentions — particularly in blended families, where business continuity is critical, or where one child has contributed significantly more than others. The Act distributes assets equally among eligible heirs, regardless of individual contribution, relationship dynamics, or the practical realities of holding a business together.

This matters most when estates include illiquid assets, operating businesses, or complex family structures where equal division would destroy value rather than preserve it.

HUF Planning

For families looking to address some of these risks proactively, the Hindu Undivided Family offers one structural option. The HUF is a legal entity unique to Indian tax law that allows income-splitting across family members and can hold ancestral property and business interests in a tax-efficient manner.

Key points to understand:

- HUF status must be established proactively; it doesn't arise from asset ownership alone

- Section 64(2) of the Income Tax Act clubs income back to a member who converts separate property into HUF property without adequate consideration

- HUFs are not suitable for all family structures, and the clubbing provisions mean they don't automatically reduce tax

Private Family Trusts

A private family trust under the Indian Trusts Act, 1882 holds assets outside the personal estate of the settlor. Assets in a trust don't go through probate, pass to beneficiaries on the terms the settlor sets, and remain private.

Trusts are particularly useful for:

- Protecting assets intended for minors until they reach a specified age

- Ring-fencing wealth from potential creditors

- Maintaining business continuity across generations

- Managing distributions for beneficiaries who may not handle a lump sum responsibly

A tax point that trips up poorly structured trusts: if beneficiary shares are indeterminate or unspecified, Section 164 of the Income Tax Act taxes trust income at the maximum marginal rate. The drafting must define each beneficiary's share precisely to avoid this outcome.

Life Insurance as a Succession Tool

Under Section 10(10D) of the Income Tax Act, proceeds paid to nominees under qualifying life insurance policies are generally tax-free. For policies issued after 1 April 2023, the exemption applies in full on death payouts — though annual premium limits apply for maturity proceeds.

This makes life insurance a practical tool for:

- Providing liquidity to cover estate settlement costs

- Equalising inheritance among heirs when illiquid assets like real estate can't easily be split

- Delivering a defined sum to a specific beneficiary outside the estate

Core Strategies to Reduce Inheritance Tax Exposure

Structured Gifting During Lifetime

Under Section 56(2)(x) of the Income Tax Act, gifts received from specified relatives are exempt from income tax in the hands of the recipient. Gifts to non-relatives exceeding ₹50,000 in a financial year are taxable as income for the recipient.

Exempt categories cover a broad range of relationships and occasions:

- Spouses, siblings, siblings of parents, lineal ascendants and descendants, and their spouses

- Gifts received on marriage, by inheritance, or under a will

For families with US connections, the 2026 annual gift tax exclusion is $19,000 per recipient per year. A consistent multi-year gifting programme can materially reduce a taxable US estate over time — particularly useful for Indian Americans or NRIs holding US assets who want to transfer wealth to the next generation gradually.

A gift deed with proper valuation, supported by banking records, protects both parties if the transaction is ever questioned.

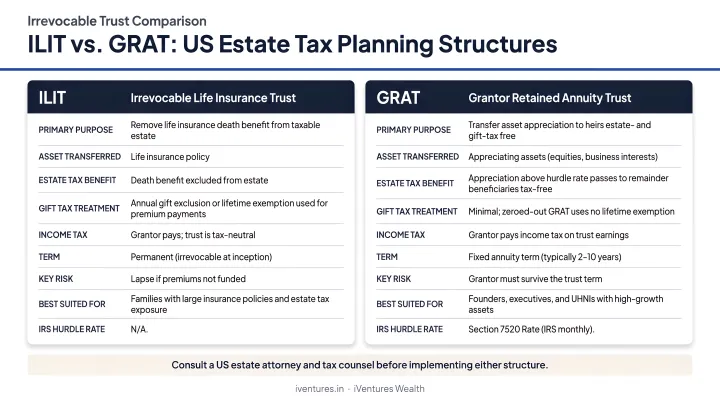

Using Irrevocable Trusts for Asset Protection

An irrevocable trust removes assets from the grantor's personal estate permanently. The grantor gives up control — but the assets are no longer subject to estate or inheritance tax on death, and they're shielded from creditors.

For US-exposed families, two structures apply:

- Irrevocable Life Insurance Trusts (ILITs): The trust owns the policy. When the insured dies, proceeds flow to beneficiaries outside the taxable estate — bypassing the estate tax that would otherwise apply under IRC Section 2042

- Grantor Retained Annuity Trusts (GRATs): The grantor transfers high-growth assets into a trust, retains an annuity stream, and any appreciation above the IRS Section 7520 assumed rate passes to heirs with minimal gift tax cost — most effective in low interest rate environments, with assets expected to appreciate significantly

Charitable Giving as a Planning Tool

Donations to registered charitable trusts and institutions qualify for deductions under Section 80G — at 100% or 50% depending on the institution, with some categories subject to a 10% of adjusted gross total income ceiling.

For families with philanthropic intent, setting up a private charitable foundation achieves two goals simultaneously: directing assets toward causes the family values, and potentially reducing the taxable estate.

For US-sited assets, IRC Section 2055 permits an estate tax deduction for qualifying charitable bequests — making philanthropy doubly effective as a planning tool for cross-border estates.

Family Limited Partnerships and Business Structures

LLPs and family limited partnership-type structures allow a wealth creator to transfer economic interests in a business or investment portfolio to heirs — often at a valuation discount for lack of control — while retaining management authority as general partner.

This reduces the taxable value of transferred assets while keeping the founder in operational control during the transition period — and it creates a governance structure that outlasts the founder.

iVentures Wealth coordinates these structures across legal, tax, and wealth planning — working alongside specialist counsel to ensure business succession aligns with the family's broader estate and tax strategy.

Special Considerations for NRIs and Cross-Border Families

NRI and cross-border families face a category of inheritance risk that purely domestic planning cannot address: simultaneous tax exposure across multiple jurisdictions, with no treaty protection in many cases.

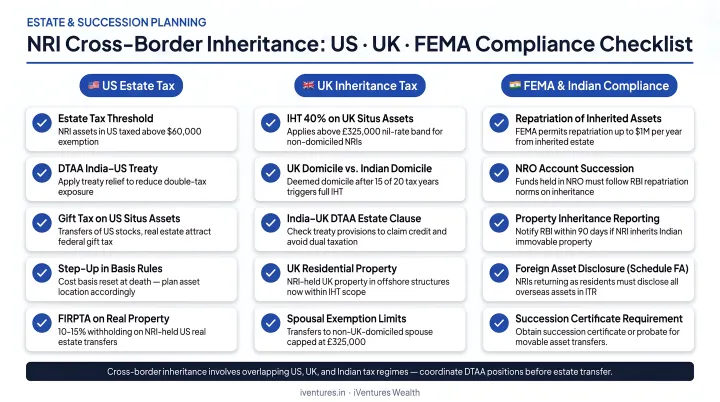

US Estate Tax for Non-Resident Aliens

Indian residents face no estate tax today, but non-resident aliens holding US-sited assets must file Form 706-NA when those assets exceed $60,000 — a threshold that can be crossed with a single US brokerage account or a share of a US property.

The top rate is 40%. Compare this with the $15 million basic exclusion available to US citizens and residents in 2026. For an NRI with $500,000 in US stocks, the exposure is immediate and significant.

US-situs assets include:

- Stock in US domestic corporations

- US real estate and tangible property physically in the US

- Certain US debt obligations

Some exclusions apply — bank deposits not connected to a US trade or business, and certain portfolio debt — but direct US equity holdings are fully exposed.

UK Inheritance Tax

The UK imposes 40% inheritance tax on UK-sited assets above the nil-rate band (currently £325,000, with a residence nil-rate band of £175,000) regardless of the owner's domicile. Families with UK property, UK bank accounts, or children settled in the UK need to map this exposure carefully.

GOV.UK distinguishes rules before and after 6 April 2025, with residence-based treatment coming into effect. The government has also announced freezing nil-rate bands from April 2028 and extending IHT to unused pension funds.

Treaty Gaps and Double Taxation Risk

India does not have a current estate or inheritance tax treaty with the US. The India-UK arrangement dates from before 1975 during the Estate Duty era and has different parameters from a modern treaty. Where no treaty applies, the same assets can face tax in two jurisdictions simultaneously.

Key planning considerations for cross-border families:

- India-US gap: No active estate tax treaty; US situs assets taxed from the first dollar above $60,000

- India-UK gap: The pre-1975 arrangement does not function as a modern IHT treaty

- FEMA remittance limit: Under RBI's FEMA 21 framework, NRIs can remit up to USD 1 million per financial year from inherited assets

- Documentation prerequisite: Tax compliance records must be in order before any cross-border remittance proceeds

Managing these gaps requires coordination across Indian succession law, foreign jurisdiction tax rules, FEMA compliance, and nominee designations across multiple countries — not sequentially, but simultaneously. For NRI and OCI families navigating this complexity, iVentures Wealth structures cross-border succession engagements that address each layer in a single, coordinated process.

Common Mistakes That Can Cost Your Heirs

Dying Intestate or With an Outdated Will

According to data cited by Moneycontrol from 1 Finance Magazine, 84.8% of Indian respondents lacked a will, and 30.5% of households faced inheritance disputes. These numbers reveal a systemic planning failure across even affluent families.

Without a current, legally valid will, assets distribute according to succession laws that may not reflect the owner's intentions. Business interests, jointly held property, and overseas assets each require specific treatment — a generic will often fails to address them.

Confusing Nominees with Legal Heirs

In India, a nominee on a bank account, mutual fund, or insurance policy is not automatically the beneficial owner. The Supreme Court confirmed this in Sarbati Devi v Usha Devi for insurance nominees and in Shakti Yezdani v Jayanand Jayant Salgaonkar for securities nominees: a nominee receives assets as a trustee, not as an heir.

When a will names a different beneficiary for the same asset, the nominee's trustee status creates a direct conflict — and disputes follow. Nominee designations must be reviewed regularly and aligned with the overall estate plan, not treated as a substitute for it.

A common scenario: a parent names a child as nominee on a mutual fund account, but leaves the same asset to a different beneficiary in a will drafted years later. The outcome is a legal dispute that can freeze assets for years.

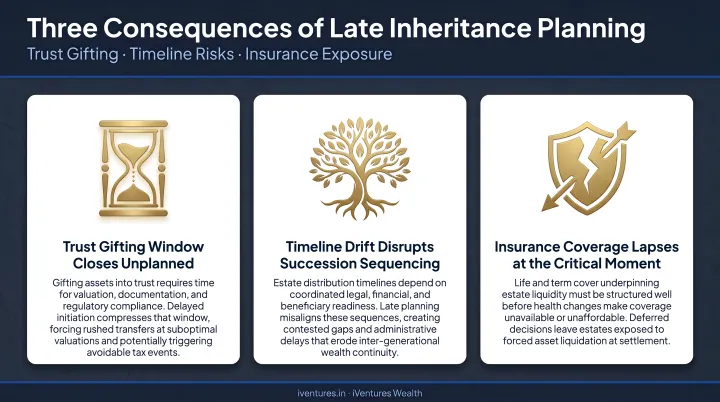

Leaving Planning Too Late

Trust formation, systematic gifting programmes, and insurance-based structures need time to deliver their full tax-efficiency benefits. Starting late undermines each one in a distinct way:

- A trust established weeks before death may be legally challenged

- A gifting programme started too late produces minimal estate reduction

- Structures set up under urgency accumulate documentation gaps — the same gaps that invite the disputes they were meant to prevent

When to Start and Who to Work With

Succession and inheritance planning should begin when significant wealth exists — not when retirement approaches. The most effective structures take years to produce their full effect, and waiting limits the available options.

What to look for in an advisor:

- Fiduciary orientation — advice structured around your interests, not product commissions

- Integrated expertise across investment management, tax planning, and legal structuring

- For families with overseas assets: genuine cross-border capability, not just familiarity with the topic

- Proven ability to coordinate with external legal counsel, CAs, and foreign-jurisdiction advisors

iVentures Wealth (SEBI RIA: INA000019026) has worked with UHNIs and family offices for over 20 years, delivering succession and estate planning as part of its integrated wealth management mandate — not as an add-on.

The firm coordinates with specialist legal counsel, including Supreme Court-level practitioners, and with tax advisors across the UAE, Singapore, UK, US, and other jurisdictions for cross-border engagements.

Frequently Asked Questions

What is inheritance tax planning?

Inheritance tax planning means structuring your assets and transfers so more of your estate reaches intended beneficiaries — with less lost to tax, probate delays, or disputes. It covers gifting strategies, legal structures, and cross-border compliance, ideally put in place well before they're needed.

What is the best way to avoid inheritance tax?

The most effective approaches combine structured lifetime gifting, irrevocable trusts to hold assets outside the personal estate, life insurance for tax-free liquidity, and charitable giving. These work best when implemented early and coordinated across all asset classes with a qualified advisor.

Who is best to advise on inheritance tax?

A SEBI-registered fiduciary advisor with expertise in estate planning, tax law, and — for NRI families — cross-border regulations. Inheritance planning spans legal structures, investments, and multi-jurisdiction compliance at once; a generalist or product-seller rarely covers all three.

Does India currently have an inheritance or estate tax?

No. India abolished estate duty in 1985 and has no inheritance tax today. Families still face succession-related costs including capital gains on inherited assets, stamp duty on property transfers, and probate fees. NRIs with overseas assets may face inheritance or estate taxes in those jurisdictions.

How does inheritance tax affect NRIs with assets in the US or UK?

Non-resident aliens holding US assets face estate tax above a $60,000 threshold at up to 40%. UK-sited assets are subject to 40% inheritance tax above the nil-rate band regardless of domicile. Both exposures require proactive cross-border structuring well before an estate event occurs.