Portfolio Management Services come up consistently in HNI conversations for a reason. The advantages aren't theoretical — they show up in quarterly tax statements, in how a business owner's sector exposures are managed, and in whether a portfolio's returns actually reflect the manager's conviction or just shadow the Nifty 50.

This article unpacks the specific, practical reasons experienced HNIs in India consistently allocate to PMS — not just what PMS is, but why it keeps earning a place in sophisticated wealth strategies.

Key Takeaways

- PMS gives HNIs individually managed portfolios with direct security ownership — not pooled units

- Key advantages include customised portfolio construction, superior tax control, and access to concentrated high-conviction strategies

- SEBI mandates a ₹50 lakh minimum, placing PMS squarely in HNI territory

- PMS works best with a 5+ year horizon and comfort with equity volatility

- Provider selection matters: a poor fit creates tax drag and portfolio misalignment that compounds quietly over time

What Is PMS? A Quick Framing for HNI Investors

Portfolio Management Services is a professionally managed investment account where an SEBI-registered portfolio manager builds and manages a direct-equity portfolio held in the investor's own demat account. No pooling, no shared units — each client's portfolio is legally and structurally separate.

SEBI's PMS regulations set clear structural guardrails for investors:

- Minimum investment: ₹50 lakh (in cash or securities)

- Mandatory disclosure document before any agreement is signed

- Client-level segregated reporting — your holdings, your statement

As of June 2026, there are 520 SEBI-registered portfolio managers offering strategies across market caps, themes, and risk profiles.

Where does PMS sit in the investment hierarchy? Above mutual funds in terms of customisation, minimum ticket size, and direct control over holdings — and typically used alongside mutual funds as a satellite allocation aimed at generating alpha rather than broad-market exposure.

For HNI investors, the real value is precision: a portfolio built around your tax situation, goals, and risk profile — not a generic allocation that happens to fit your bracket. That distinction shapes every other reason HNIs choose PMS over alternatives.

Key Reasons HNIs Choose PMS Investments in India

The advantages below aren't abstract claims. They're the practical, outcome-linked reasons experienced HNIs cite when explaining why PMS earns a place in their portfolio alongside — or in preference to — mutual funds and self-managed equity.

Reason 1: Portfolio Customisation That Reflects Individual Goals, Not a Fund Mandate

Unlike a mutual fund that runs a single portfolio across thousands of investors, PMS constructs a unique portfolio for each client. Sector biases, cash allocation timing, stock exclusions, and risk limits are all negotiable — calibrated to the specific investor's situation.

In practice, this looks like:

- A business owner with heavy real estate exposure requesting that property-linked stocks be excluded

- A CXO with large ESOP positions structuring PMS to reduce further concentration in the same sector

- A family office aligning the portfolio toward dividend income rather than pure capital growth

HNIs rarely have generic financial situations. Customised portfolios avoid unintended overlap with existing holdings, reduce sector concentration risk, and ensure each rupee does purposeful work aligned to the investor's actual financial picture.

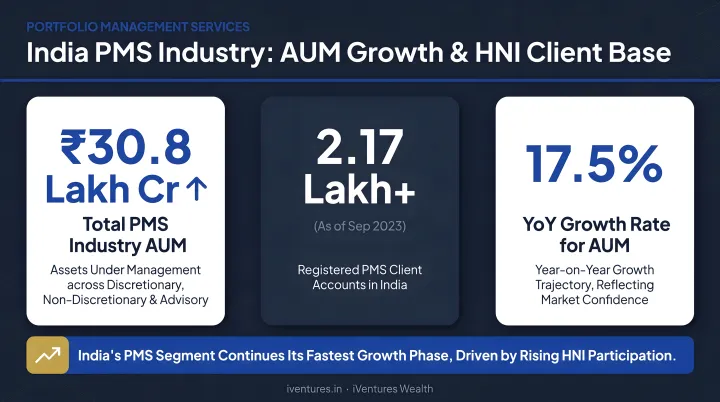

The scale of the industry reflects this demand. APMI's April 2026 data shows PMS industry AUM at ₹42.2 lakh crore, growing 2.1% month-on-month — with over 2.1 lakh clients across registered providers. The EY Indian Family Office Playbook (June 2025) notes that Indian family offices grew from 45 to approximately 300 between 2018 and 2024, with increasing allocations to PMS and AIFs as the need for personalised structures has intensified.

When this matters most: Business owners, family offices, NRIs with cross-border asset exposure, and investors with large ESOP or single-stock positions who need PMS to deliberately balance the rest of their wealth.

That growing demand for personalised structures is also why strategy selection sequence matters. At iVentures Wealth, PMS engagements start with the client's existing wealth picture — concentrated positions, sector biases, and liquidity timelines — before evaluating which strategy fits, rather than recommending a strategy and working backward.

Reason 2: Tax Efficiency Through Direct Ownership of Securities

Because PMS holds securities directly in the investor's demat account, the investor is the legal owner of each stock. This creates a fundamentally different tax situation compared to holding mutual fund units.

The current tax landscape for listed equity:

- LTCG on listed equities: 12.5% (post-Budget 2024)

- LTCG exemption threshold: ₹1.25 lakh per financial year (increased from ₹1 lakh)

- STCG on specified financial assets: 20%

Source: CBDT/PIB FAQ on the new capital gains regime, July 2024

With direct ownership, a PMS manager can:

- Time the realisation of gains and losses strategically across the financial year

- Harvest LTCG within the annual ₹1.25 lakh exemption limit before gains exceed it

- Book tactical losses to offset gains from other positions

- Avoid triggering taxable events unnecessarily

Mutual funds don't allow this. NAV-level capital gains events are outside the investor's control — when the fund manager sells a stock inside the scheme, the tax event happens regardless of the unit-holder's timing preferences. The investor has no mechanism to defer or sequence these events.

One structural difference cuts the other way: as Mint's analysis explains, when a PMS manager trades within a client portfolio, it triggers tax at the investor level — unlike mutual funds, which have scheme-level pass-through treatment. Tax efficiency in PMS isn't built in by default. It has to be actively managed in coordination between the investor, their adviser, and the portfolio manager. Done well, the post-tax compounding advantage over a 10-year horizon can be substantial. Left uncoordinated, it erodes the benefit.

When this matters most: HNIs in the 30% tax bracket, investors transitioning large liquidity events (business sale proceeds, ESOPs, inheritance) into equity, and those with large corpora where unoptimised capital gains treatment creates compounding post-tax drag over a 10-year horizon.

Reason 3: Concentrated, High-Conviction Strategies That Mutual Funds Cannot Offer

PMS portfolios typically hold 15–25 stocks. A 2021 deep scan of 124 PMS strategies by PMS Bazaar found an average of 25 stocks per portfolio, with 89 of those strategies holding 25 or fewer positions.

Mutual funds, by contrast, operate under SEBI diversification norms and liquidity requirements that push most equity schemes toward 50–100+ holdings. The result is that any individual position in a mutual fund rarely moves the needle on overall portfolio returns.

In PMS, the manager's best ideas drive outcomes. A well-researched mid-cap thesis or special situation opportunity isn't diluted to near-irrelevance; it can be held at 5–8% of the portfolio, where conviction translates to return impact.

The historical performance across completed strategies reflects this:

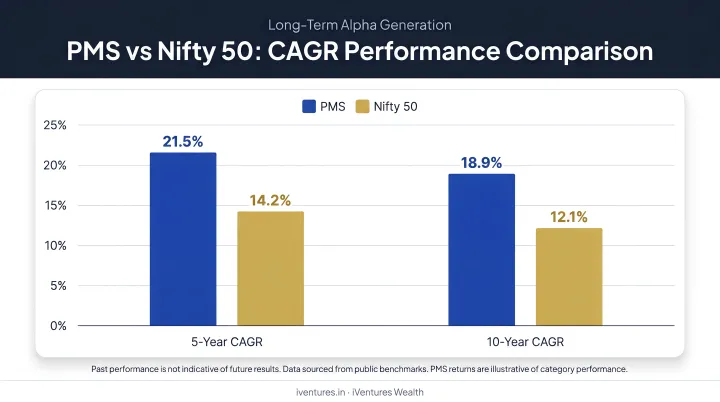

- PMS Bazaar's 10-year review of 53 completed strategies showed average PMS returns of 18.94% CAGR vs. 14.73% for Nifty 50 TRI through February 2024

- The top 10 PMS strategies over 10 years delivered approximately 20% CAGR vs. ~14% for the market through July 2024

- Over 5 years, 59% of PMS approaches outperformed benchmarks vs. 46% of mutual funds; over 10 years, 79% of PMS approaches outperformed vs. 65% of direct mutual funds

One important caveat: concentration isn't a guaranteed alpha generator. Research from Acadian Asset Management (2024) found no systematic evidence that concentrated strategies, as a category, produce higher active returns than higher-breadth strategies. The data supports PMS outperformance for selected cohorts, but manager quality and investment philosophy matter as much as concentration alone.

When this matters most: HNIs with 5+ year investment horizons who are not dependent on these assets for near-term liquidity, and who want differentiated returns rather than market-tracking performance.

What HNIs Risk When They Skip PMS

Not using PMS doesn't mean avoiding risk — it means accepting a different set of trade-offs that often cost more over time.

Common consequences for HNIs without PMS:

- Unintended portfolio duplication: Generic mutual funds don't account for existing holdings, often creating sector overlaps that aren't visible without consolidated reporting

- Tax inefficiency at scale: Multiple fund redemptions across large corpora, with no ability to sequence or time capital gains events, create a post-tax drag that compounds significantly over a 10-year horizon

- Benchmark-hugging performance: Funds built for broad retail audiences rarely take the concentrated bets that generate genuine outperformance for investors with the risk tolerance and time horizon to hold through volatility

- Behavioural drift without oversight: The SEBI Investor Survey 2025 found 59% of investors rely on friends and family for financial decisions, and 62% act on social media influencer tips — PMS structures a professional buffer against exactly this

At large corpus sizes, a single panic exit during a correction or a FOMO-driven entry near a peak doesn't just cost percentage points. On a ₹5 crore portfolio, a 15% behavioural misstep translates to ₹75 lakh in avoidable losses — before accounting for the opportunity cost of re-entry timing.

How to Get the Most Value from PMS as an HNI

PMS delivers its full value when the investor engages with it correctly. Three conditions consistently separate good outcomes from disappointing ones:

1. Hold through a full market cycle High-conviction concentrated strategies need time for thesis validation and compounding to work. PMS managers who ran concentrated strategies through the March 2020 crash and held discipline saw recoveries of up to 56% in the following quarter. Conversely, the June 2022 correction saw only 129 of 279 PMS schemes outperform the Nifty — which was itself down 4.85% — highlighting that short-term noise is real. Evaluate over 7–10 years, not 12 months.

2. Measure risk-adjusted returns, not just absolute performance How a PMS performed during the 2020 and 2022 corrections matters as much as its bull-run numbers. Sharpe ratio, Sortino ratio, maximum drawdown, and benchmark-relative returns across full cycles give a more complete picture than a 3-year CAGR in isolation.

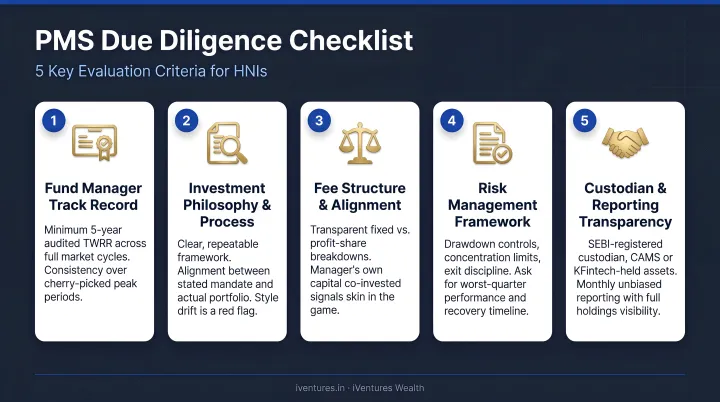

3. Select through rigorous due diligence SEBI requires portfolio managers to provide a disclosure document covering fees, portfolio risks, related-party transactions, and a three-year audited track record before agreement execution. Non-negotiables beyond that include: investment philosophy alignment with the investor's goals, fee structure transparency (management fees, performance fees, hurdle rate, exit loads), and whether the adviser recommending the PMS earns commissions from the recommendation.

iVentures Wealth, a SEBI-registered investment adviser operating since 2005 with a CFA-led research team and a fee-only model, helps HNIs evaluate, access, and monitor PMS strategies as part of an integrated wealth strategy. As a fee-only RIA, iVentures earns no commissions or trail income from product manufacturers, so PMS recommendations are driven by client suitability, not product incentives.

The firm's consolidated Wealth Monitor App lets clients track PMS performance alongside mutual funds, AIFs, bonds, and other holdings in a single dashboard, which is particularly useful when assessing how a PMS allocation is contributing within the broader portfolio.

Conclusion

HNIs choose PMS because, beyond a certain wealth threshold, generic fund mandates stop fitting. Customised portfolios, direct security ownership, and tax-aware management aren't premium features — they're prerequisites for managing wealth at this scale effectively.

A well-structured PMS portfolio managed across a 7–10 year horizon does more than target returns. It systematically reduces tax drag, adapts to shifting financial goals, and reflects the investor's actual wealth picture — not a standardised allocation built for the average investor.

The investors who extract the most value from PMS revisit the strategy as their circumstances shift. When income profiles change, tax situations evolve, or legacy objectives come into focus, the portfolio should respond — reviewed periodically and anchored to the broader wealth plan at every stage.

Frequently Asked Questions

What are the advantages of PMS over mutual funds?

PMS offers direct security ownership (not pooled units), enabling tax-loss harvesting, gain sequencing, and concentrated high-conviction strategies that mutual fund diversification norms prevent. For HNIs, these structural differences translate to better tax outcomes and closer alignment with personal financial goals.

Which is better, PMS or AIF?

PMS and AIF serve different needs — PMS suits HNIs seeking listed equity with direct ownership and tax control; AIF (especially Category II/III) is designed for investors targeting private markets, long-short strategies, or higher-risk alternative structures. AIF requires a minimum of ₹1 crore vs. ₹50 lakh for PMS. Many sophisticated investors hold both as complementary allocations.

Do HNIs invest in mutual funds?

Yes — HNIs typically use mutual funds as the "core" allocation for broad diversification, liquidity, and stability. PMS is added as the "satellite" layer to seek concentrated alpha and personalised tax management that mutual funds structurally cannot provide. The two work together rather than as substitutes.

What is the minimum investment for PMS in India?

SEBI mandates a minimum of ₹50 lakh for PMS investment in India, in cash or securities. Individual PMS providers may set higher minimums — some strategies require ₹1 crore or more.

Is PMS suitable for NRI investors?

NRIs can invest in PMS through NRE/NRO accounts under FEMA regulations and the RBI's Portfolio Investment Scheme framework. It enables professional management of Indian equity exposure with tax planning that can be coordinated alongside DTAA benefits — though onboarding requirements vary by provider.

How should HNIs evaluate a PMS provider before investing?

Key criteria: SEBI registration status, multi-year performance track record across full market cycles (not just recent bull-run returns), investment philosophy alignment with your goals, full fee transparency (management fee, performance fee, hurdle rate, exit loads), and whether your adviser is fee-only or earns commissions on the recommendation. The last point is often overlooked but directly affects the objectivity of the advice.