Introduction

Most Indian expats earn in dollars, pounds, or dirhams while holding assets in rupees — two currencies, two regulatory systems, one financial life. Your country of residence has its own tax rules. India has its own. And then there's FEMA, NRE/NRO account structures, and DTAA claims that most generic financial advisors have never dealt with.

Getting any one of these wrong has consequences.

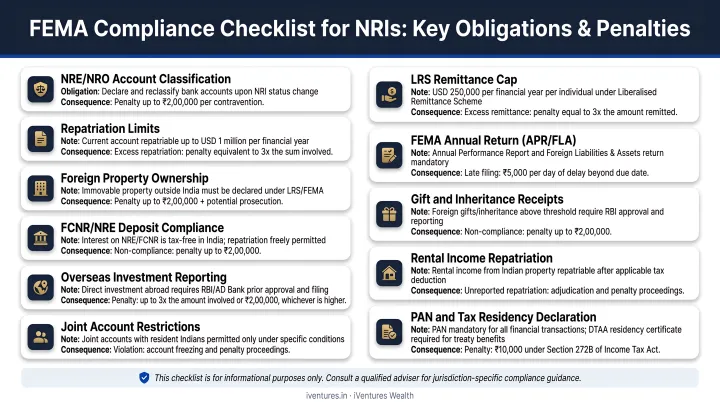

The stakes are real. FEMA violations carry penalties up to three times the amount involved, with continuing contraventions adding ₹5,000 per day. US-based NRIs with Indian accounts exceeding USD 10,000 face mandatory FBAR filing. And without proper DTAA documentation, you may end up paying tax twice on the same income.

This guide covers the full cross-border planning picture: residency status, banking structure, tax optimisation, retirement coordination, and estate planning across jurisdictions — with specific guidance for Indian expats at each step.

Key Takeaways

- Your residency status under the Income Tax Act and FEMA are determined by different tests — confusing them is a costly mistake

- NRE accounts are tax-free and fully repatriable; NRO accounts are taxable with a USD 1 million per financial year repatriation cap

- DTAA relief requires Form 10F and a Tax Residency Certificate — without them, you pay full Indian TDS

- Indian mutual funds held by US-based NRIs trigger PFIC classification, requiring complex Form 8621 filings each tax year

- A SEBI-registered, fee-only advisor with cross-border expertise is essential for compliant, optimised NRI wealth management

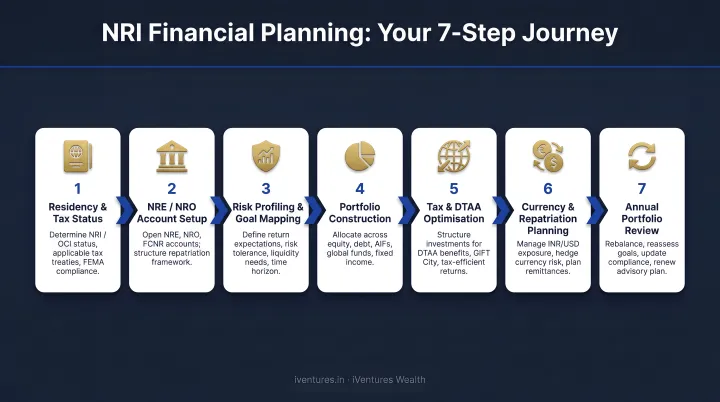

The 7 Steps of Financial Planning for Indian Expats

Step 1: Determine Your Residency Status

This is the foundation. Under Section 6 of the Income Tax Act, you are a tax resident if you spend 182 or more days in India during the previous year, or 60+ days in the year plus 365+ days in the preceding four years. Indian citizens leaving for employment abroad get the 60-day limb replaced by 182 days — a critical distinction.

FEMA applies a different test. It defines a "person resident outside India" based on the preceding financial year's 182-day count, plus purpose and intention of stay.

Crucially, you can be a tax NRI and still carry FEMA obligations if your intention to remain abroad isn't clearly established.

One special category worth knowing: RNOR (Resident but Not Ordinarily Resident) status, available to Indians who were non-resident in 9 of the preceding 10 years, or spent 729 days or fewer in India over the prior 7 years. During RNOR status, foreign-source income remains non-taxable in India — a useful window for portfolio restructuring on return.

Step 2: Map Goals Across Both Countries

Most NRIs under-plan in one direction. Some optimise heavily for the host country while Indian assets sit unmanaged. Others focus entirely on India and neglect retirement savings where they actually live.

A coherent plan sets goals in both contexts:

- Host country: Retirement accounts, property, local emergency fund, children's education

- India: Family property, NPS or EPF balances, equity portfolio, eventual return planning

Misaligned timelines, different currencies, and conflicting tax treatments between these two tracks is where most planning mistakes originate. Step 3 addresses the banking structure that holds it all together.

Step 3: Organise Your Banking Structure

Three account types, three distinct purposes:

- NRE accounts — foreign income converted to rupees; fully repatriable, tax-free in India

- NRO accounts — Indian-source income (rent, dividends, pensions); taxable, repatriable up to USD 1 million per financial year

- FCNR(B) accounts — foreign currency deposits; eliminates exchange rate risk for savings you'll eventually convert

Choosing the wrong structure creates avoidable tax exposure and repatriation complications.

Steps 4–7: Build, Coordinate, Protect, Review

The final four steps translate structure into execution:

- Step 4 — Tax-Efficient Investments: Every decision must account for Indian capital gains treatment, host-country taxation, and applicable DTAA relief across both jurisdictions

- Step 5 — Cross-Border Retirement: EPF, NPS, and host-country pension schemes need active coordination; bilateral treaty treatment on withdrawals varies significantly by jurisdiction

- Step 6 — Estate Planning: Indian succession law and your host country's inheritance rules frequently conflict; separate wills for each jurisdiction are often necessary

- Step 7 — Annual Review: Residency changes, regulatory updates, currency shifts, and life events (marriage, children, return to India) all require the plan to be revisited and adjusted

Tax Planning for NRIs: Residency Rules, DTAA, and FEMA Compliance

What India Taxes — and What It Doesn't

As an NRI, India taxes only income that originates in India:

- Interest on NRO accounts

- Rental income from Indian property

- Capital gains on Indian assets

- Dividends from Indian companies

NRE account interest is fully exempt from Indian income tax. This asymmetry (NRO taxable, NRE exempt) makes account structuring a tax decision, not just a banking one.

How DTAA Works in Practice

India has DTAA agreements with over 94 countries, covering salary, dividends, capital gains, interest, and pensions. The treaty prevents double taxation by allowing you to offset taxes paid in your country of residence against your Indian tax liability — or by exempting certain income from Indian tax altogether.

To claim relief, you need:

- Tax Residency Certificate (TRC) — issued by your host country's tax authority

- Form 10F — filed under Section 90(5)/90A(5) of the Income Tax Act

- Other declarations as required by the specific treaty

Without these documents, Indian banks and fund houses withhold TDS at standard rates regardless of your treaty entitlement. Claiming a refund later is possible but time-consuming.

Jurisdiction-Specific Disclosure Requirements

- US-based NRIs: FBAR applies when aggregate foreign accounts exceed USD 10,000 at any point during the year; Form 8938 thresholds start at USD 50,000 (last day) or USD 75,000 (any point) for unmarried US residents, with higher thresholds for those living abroad

- UK-based NRIs: HMRC taxes UK residents on worldwide income; the Worldwide Disclosure Facility applies where a UK tax liability relates to an offshore asset or account

- UAE and Singapore: Both have active DTAA treaties with India — verify article-level coverage against current IRAS and Income Tax Department schedules, as treaty protocols are periodically updated

FEMA Compliance: Not Optional

FEMA governs all cross-border money movements. Key obligations include:

- Converting resident savings accounts to NRO accounts upon becoming non-resident

- Staying within the USD 1 million/year NRO repatriation cap

- Filing Form 15CA (remittance declaration) and Form 15CB (accountant certificate, required when aggregate taxable remittance exceeds ₹5 lakh)

- Avoiding prohibited investments under FEMA schedules

Penalties for violations reach up to 3 times the amount involved if quantifiable, or ₹2 lakh if not, plus ₹5,000 per day for continuing contraventions. Enforcement is active, and penalties compound quickly — corrective action taken early costs far less than remediation after a notice is issued.

NRI Bank Accounts and Cross-Border Currency Management

Account Comparison

| Feature | NRE | NRO | FCNR(B) |

|---|---|---|---|

| Currency held | INR (from foreign income) | INR (Indian income) | Foreign currency |

| Repatriability | Fully repatriable | Up to USD 1 million/FY | Fully repatriable |

| Indian tax on interest | Exempt | Taxable | Exempt |

| Best for | Foreign earnings parked in India | Indian rent, dividends, pensions | Savings without FX conversion risk |

Managing Currency Risk

Every transfer between your host currency and the rupee is an FX transaction — and cumulative losses can erode returns significantly over time. Practical strategies:

- Stagger transfers rather than converting lump sums during unfavourable rate windows

- Match asset currency to future spending currency — if you plan to retire in India, rupee-denominated assets make sense; if children are studying abroad, building dollar-linked assets reduces FX exposure

- GIFT City structures allow NRIs to invest in Indian markets while benchmarking in USD, reducing the need for frequent currency conversion

iVentures Wealth's currency management advisory helps clients evaluate whether unhedged, partially hedged, or fully hedged strategies align with their portfolio size and financial objectives.

Account Conversion Timing

When you become non-resident, your existing resident savings account must be redesignated as an NRO account. Some Indian banks request this proactively; others wait for the customer to initiate it. Either way, continuing to operate a resident account after establishing non-residency creates FEMA exposure.

Host-country banks are also applying enhanced due diligence to customers with Indian financial ties, driven by global compliance frameworks. Keeping your NRI account structure clean and properly classified reduces friction on both ends.

Investment and Retirement Planning Across Borders

What NRIs Can — and Cannot — Invest In

NRIs have access to most Indian investment products, with some notable exceptions:

Permitted:

- Indian equities via the PIS (Portfolio Investment Scheme) route through an RBI-designated bank branch

- Most Indian mutual funds (NRIs from most countries)

- NPS (National Pension System) — eligible for NRIs aged 18 to 60 per NPS Trust FAQ; confirm current PFRDA limits before investing

- Real estate (residential and commercial; agricultural land is prohibited)

- AIFs, PMS, bonds, and government securities

Not permitted:

- PPF contributions after becoming NRI — effective 25 July 2003, NRIs are not eligible to open PPF accounts

- Agricultural land, plantation property, farmhouses

- Certain commodity and currency derivatives

The PFIC Problem for US-Based NRIs

This is one of the most overlooked tax traps in NRI planning. Under US tax law, Indian mutual funds qualify as Passive Foreign Investment Companies (PFICs), and US persons holding them must file Form 8621. The tax treatment under Section 1291 excess-distribution rules is punitive — interest charges apply on deferred gains, and the compliance burden is real and ongoing.

For US-based NRIs, direct Indian equities via PIS or US-listed ETFs with India exposure are generally more tax-efficient alternatives. iVentures Wealth addresses PFIC exposure as part of its cross-border tax coordination for US-resident clients, including GIFT City structures as an alternative access point.

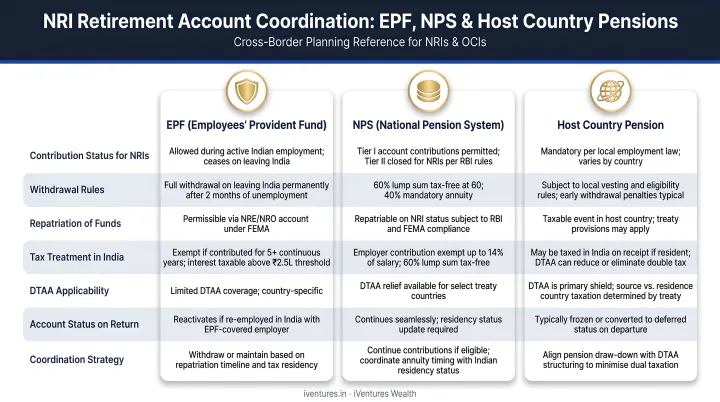

Retirement Account Coordination

Three accounts to coordinate:

- EPF: Funds can remain until withdrawal. EPFO confirms TDS does not apply if total service exceeds 5 years. Withdrawals before five years of service trigger TDS.

- NPS: Partial repatriation is allowed for NRIs; NPS allows repatriation of pension and annuity payments subject to FEMA guidelines

- Host-country pension schemes: Check the bilateral tax treaty before contributing or withdrawing — treaty provisions on pension income vary widely by country

Estate Planning and Asset Protection for NRIs

Why a Single Will Is Often Insufficient

Indian succession law — the Hindu Succession Act, 1956 and the Indian Succession Act, 1925 — governs assets located in India. Your host country's law governs overseas assets. These two systems can conflict on inheritance shares, asset distribution timelines, and who qualifies as a legal heir.

The practical recommendation: draft separate wills for each jurisdiction, with each will explicitly limited to assets in that jurisdiction to avoid overlap or contradiction.

NRI-Specific Estate Risks

Several risks are specific to NRI situations:

- US estate tax: Non-US-citizen surviving spouses do not receive the unlimited marital deduction. IRS Form 706 instructions require a Qualified Domestic Trust (QDOT) for qualifying property to pass to a non-citizen spouse — a detail that catches many NRI families off guard

- UK inheritance tax: GOV.UK confirms that when someone living outside the UK dies, UK IHT applies only to UK assets, but UK-resident NRIs with Indian assets need full residence and domicile analysis before assuming this applies to them

- Nominee designations: Nominees on NRE/NRO accounts and demat accounts facilitate administrative settlement but are not automatic legal owners — succession is determined by the will and applicable succession law

- Nominee-estate alignment: Mismatches between nominees and named heirs are a common source of family disputes — reviewing both together avoids conflicts at the time of settlement

Structuring Tools Worth Evaluating

Trusts, joint holdings, and HUF (Hindu Undivided Family) structures each have a role — but each requires careful evaluation in an NRI context. HUF status, for example, has implications when members permanently return to India or when beneficiaries are non-resident.

iVentures Wealth advises NRI clients on structuring decisions in this space — coordinating with legal counsel across jurisdictions including the US, UK, UAE, and Singapore to align Indian succession requirements with foreign probate processes before structures are finalised.

How to Choose the Right Expat Financial Advisor for NRIs

Credentials That Actually Matter

Not every advisor who claims NRI expertise has it. Look for:

- SEBI registration — mandatory under SEBI Investment Advisers Regulations, 2013 for anyone providing investment advice in India; no NRI-specific exemption exists

- Cross-border tax literacy — DTAA, FEMA, FBAR/FATCA, PFIC implications for US clients

- CFA or CFP credentials — indicative of rigorous financial training beyond product sales

- Jurisdiction experience — active clients in your country of residence, not just theoretical familiarity

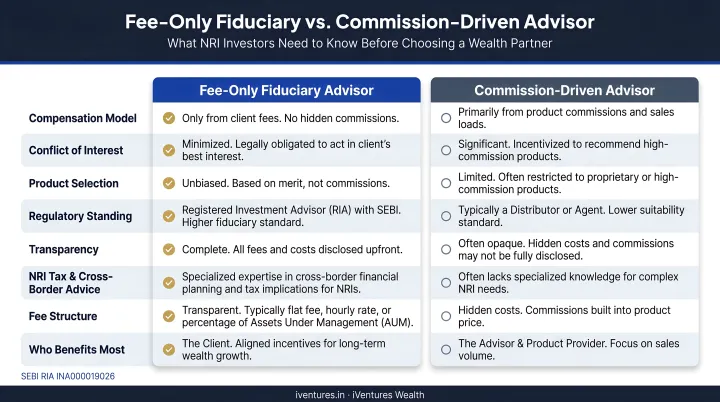

Fee-Only vs. Commission-Driven: The Difference That Matters Most

The structure of your advisor's compensation shapes every recommendation they make:

- Commission-driven: Earns more when selling higher-fee products — incentives and your interests can diverge

- Fee-only fiduciary: Charges a transparent advisory fee and is legally obligated to act in your interest

In cross-border wealth management — where products range from GIFT City funds to PMS to international ETFs — that distinction directly determines the quality of advice you receive.

iVentures Wealth: NRI Advisory Built for Complexity

iVentures Wealth is a SEBI-registered investment adviser (INA000019026) operating since 2005 with 20+ years of experience serving NRIs and OCIs across the US, UK, UAE, Singapore, Canada, and Australia. The firm's CFA-led research team provides cross-border tax coordination, DTAA optimisation, FEMA compliance advisory, and consolidated portfolio reporting across Indian and international accounts.

Key terms for NRI/OCI clients:

- Minimum investable assets: ₹5 crore

- Fee structure: Transparent, AUM-based — no trail commissions, no product placements

- Advisory model: Open-architecture, product-neutral — recommendations are driven by portfolio fit, not distributor margins

For NRIs managing significant cross-border wealth, a conflict-free fee structure means every allocation decision reflects your goals, not your advisor's revenue.

Frequently Asked Questions

What are the 7 steps of financial planning for NRIs?

The seven steps are:

- Assess your residency status under the Income Tax Act and FEMA

- Define cross-border financial goals

- Structure your NRE/NRO/FCNR accounts correctly

- Build a tax-efficient investment plan using DTAA where applicable

- Coordinate retirement accounts across jurisdictions

- Draft an estate plan valid in both countries

- Commit to an annual review as your circumstances change

Is a 1% advisory fee worth it for NRI wealth management?

For NRIs juggling cross-border tax, FEMA compliance, and multi-jurisdictional investments, a fee-based fiduciary advisor typically generates savings — through tax efficiency, avoided penalties, and better net returns — that exceed the cost. What matters more than the percentage is whether the advisor is genuinely qualified to handle cross-border complexity.

What is the difference between NRE and NRO accounts?

NRE accounts hold foreign income converted to rupees — fully repatriable and exempt from Indian income tax. NRO accounts hold Indian-source income like rent or dividends — taxable in India with repatriation capped at USD 1 million per financial year with proper documentation.

Can NRIs invest in mutual funds in India?

Yes — most NRIs can invest in Indian mutual funds via the PIS route. US- and Canada-based NRIs face restrictions from several fund houses due to FATCA compliance requirements, so verify directly with individual AMCs before investing.

How does DTAA help NRIs avoid double taxation?

DTAA lets you offset taxes paid in your country of residence against your Indian tax liability on the same income. To claim relief, you need a Tax Residency Certificate from your host country and Form 10F filed with the Income Tax Department — without these, Indian payers deduct TDS at standard rates regardless of your treaty entitlement.

Do NRIs need to file income tax returns in India?

Yes, if India-sourced income — rent, capital gains on Indian assets, NRO interest — exceeds the basic exemption limit. Non-filing can result in penalties and loss of treaty benefits, and it creates complications if you later need to repatriate funds or sell Indian property.