Key Takeaways

- IFSCA is the single unified regulator for GIFT City's IFSC, consolidating powers previously held by RBI, SEBI, IRDAI, and PFRDA

- Section 80LA grants eligible IFSC units a 100% income tax deduction for any 10 consecutive years within the first 15 years of operations

- GIFT City transactions are treated as offshore under FEMA (foreign currency, outside domestic restrictions)

- Fund management, banking, securities listing, payments, and fintech each operate under separate IFSCA regulatory frameworks with distinct compliance requirements

- NRIs, UHNIs, and family offices can access GIFT City through regulated products, with eligibility thresholds that vary by vehicle

What Is GIFT City and India's IFSC?

GIFT City (Gujarat International Finance Tec-City) is India's first operational International Financial Services Centre — a notified Special Economic Zone located on the banks of the Sabarmati, connecting Ahmedabad and Gandhinagar in Gujarat. The IFSC sits within GIFT Multi Services SEZ, with 261 acres demarcated as SEZ and 625 acres as Domestic Tariff Area.

The jurisdiction's defining feature is its FEMA treatment. Under the Foreign Exchange Management (IFSC) Regulations, 2015, any financial institution or branch set up in an IFSC is treated as a person resident outside India. In practical terms, transactions within GIFT City carry the same regulatory character as offshore transactions — with no requirement to physically move capital abroad.

Business within GIFT City is conducted primarily in freely convertible foreign currencies, including USD, EUR, JPY, GBP, and CAD. This currency framework, combined with the non-resident FEMA treatment, creates a genuinely distinct investment environment.

How GIFT City Differs from Mainland India

That distinction becomes most visible when comparing GIFT City directly against the mainland regulatory framework.

| Factor | Mainland India | GIFT City IFSC |

|---|---|---|

| FEMA treatment | Resident | Non-resident (deemed offshore) |

| Operating currency | INR | USD, EUR, GBP, and others |

| Primary regulator | RBI / SEBI / IRDAI | IFSCA (unified) |

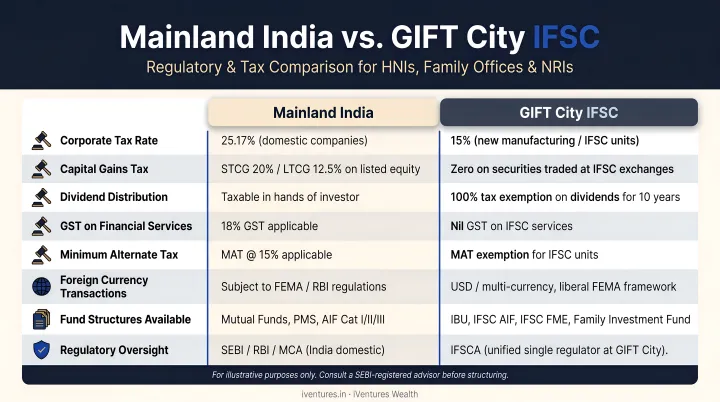

| Tax regime | Standard domestic rates | Section 80LA exemptions apply |

| STT / CTT | Applicable | Exempt on IFSC exchange transactions |

India designed GIFT City to compete directly with Singapore, Dubai, and London — delivering globally benchmarked financial services with Indian regulatory backing. As of March 2024, IBU assets stood at USD 60 billion with cumulative banking transactions exceeding USD 795 billion, underscoring the jurisdiction's rapid growth over a short span.

Who Regulates GIFT City? The Role of IFSCA

IFSCA (International Financial Services Centres Authority) was established by the Government of India on April 27, 2020 under the IFSCA Act, 2019. It is India's first unified financial regulator — consolidating oversight that previously sat across four separate agencies:

- RBI — banking supervision

- SEBI — capital markets

- IRDAI — insurance

- PFRDA — pension funds

What IFSCA Does as a Single-Window Regulator

Rather than navigating four regulators with different filing systems, timelines, and interpretations, entities operating in GIFT City deal with one authority. IFSCA's mandate covers:

- Granting licenses and registrations across all financial service categories

- Issuing sector-specific regulations and directions

- Supervising financial entities on an ongoing basis

- Running a Regulatory Sandbox for testing new financial products (framework issued October 19, 2020, updated via the FinTech Sandbox Framework, 2026)

- Collaborating with international regulators and development bodies

- Providing dispute resolution for IFSC-related matters

IFSCA's internal structure covers five dedicated regulatory verticals: banking supervision, capital markets, insurance and pension, fintech and development, and legal and policy affairs.

Practical Benefits of a Single Regulator for Investors

For UHNIs, NRIs, and family offices, a single regulator translates directly into faster setup timelines, clearer compliance pathways, and greater predictability when structuring investments. Whether you're structuring a cross-border fund or a fintech payment solution, IFSCA is the single point of regulatory authority — no jurisdictional overlap, no conflicting guidance.

Key GIFT City Regulations Investors Should Know

Banking: IFSCA Banking Regulations, 2020

Indian and international banks can establish IFSC Banking Units (IBUs) in GIFT City to offer foreign currency services. As of May 2024, 27 IBUs were licensed and operational.

For corporate treasury clients and HNIs, IBUs provide access to global banking products without routing transactions through correspondent banks abroad:

- USD-denominated deposits and foreign currency lending

- Trade finance instruments

- Treasury solutions across currencies

Crédit Agricole CIB's 2025 announcement of an IFSC Banking Unit branch in GIFT City signals sustained momentum from global banks entering the IFSC.

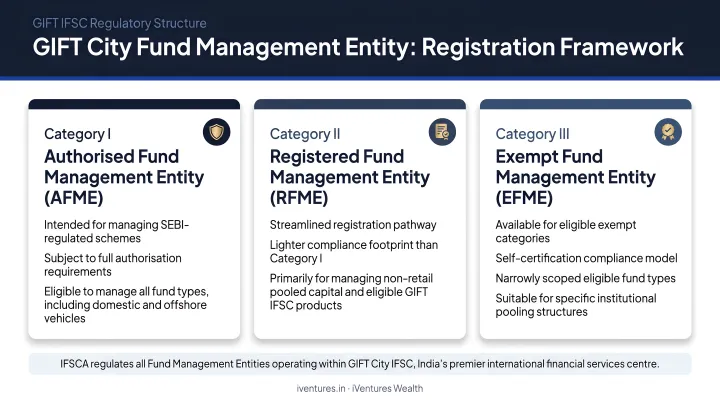

Fund Management: IFSCA Fund Management Regulations, 2022

Any entity managing funds in GIFT City must register as a Fund Management Entity (FME) under one of three categories:

| FME Category | Fund Types | Target Investors |

|---|---|---|

| Authorised FME | Venture capital, family investment funds | Accredited / family investors |

| Registered FME (Non-Retail) | AIFs, restricted schemes | Accredited investors, private placement |

| Registered FME (Retail) | Mutual funds, ETFs | Broader investor base |

Key investor-facing thresholds under these regulations:

- Restricted schemes: Minimum investment of USD 150,000

- Venture capital schemes: Minimum investment of USD 250,000

- Green channel: Accredited investor schemes open for subscription immediately on filing — no prior approval required

- Offshore fund relocation: Existing offshore funds can migrate to GIFT City, with specific relief provisions including waiver of mandatory FME contribution in relocation cases

Securities: IFSCA Listing Regulations, 2024

The current framework (updated from the 2021 regulations) enables direct listing on GIFT City's two exchanges — India INX and NSE IFSC. Following the government's January 24, 2024 notification, Indian public companies can now list equity shares directly on these international exchanges — bypassing the traditional domestic IPO process.

For institutional investors and UHNIs, this means direct access to Indian equity capital markets in foreign currency — through an internationally recognized exchange, without the domestic listing process.

Cross-Border Payments: IFSCA Payment Services Regulations, 2024

IFSCA's payment services framework authorises providers for services including:

- E-money account issuance

- Escrow services

- Cross-border money transfers

- Merchant acquisition

IFSC Payment Service Providers operate outside FEMA's typical domestic constraints, making GIFT City attractive for businesses managing international financial flows. Significant PSP thresholds apply — USD 2M to USD 4M depending on service category — so this is a structured regime, not a blanket open-access framework. The operational flexibility over domestic payment rules is, however, substantial.

TechFin and Ancillary Services: IFSCA Regulations, 2025

The TechFin and Ancillary Services Regulations (dated July 10, 2025) govern technology-enabled financial service providers in GIFT City. Entities must register with IFSCA, appoint a Principal Officer and Compliance Officer, and meet prescribed eligibility criteria.

This framework is directly relevant for:

- Fintech-driven wealth management platforms

- Robo-advisory firms

- Financial crime compliance technology providers

Any fintech entity planning to enter the IFSC should map its activities against this regulation before structuring its presence.

GIFT City Tax Rules: A Clear Breakdown

Income Tax: Section 80LA

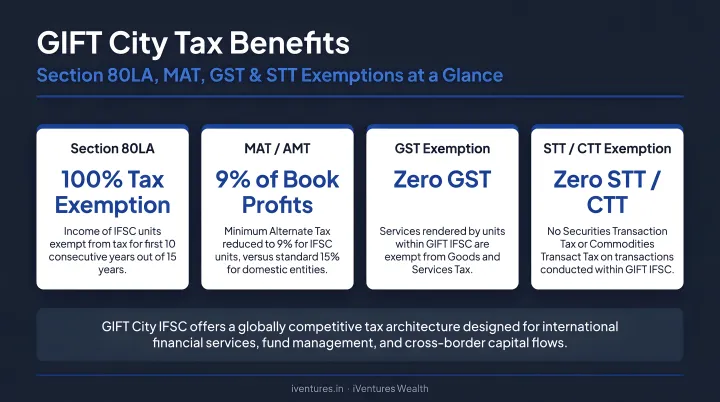

Under Section 80LA of the Income Tax Act, eligible IFSC units receive a 100% deduction on business income for any 10 consecutive assessment years within the first 15 years of operations, beginning from the year the relevant permission, registration, or approval is obtained.

A full 10-year income tax exemption of this kind is rare in Indian tax law — and it applies across banking, fund management, insurance, and other regulated IFSC activities.

Minimum Alternate Tax (MAT)

Companies that have not opted for the new tax regime (Section 115BAA) remain subject to MAT at 9% on book profits, even during the 80LA exemption period. This is lower than the standard MAT rate applicable to domestic companies.

Entities evaluating GIFT City structures should factor this into their tax planning — the 80LA exemption and MAT interact differently depending on the chosen tax regime.

GST, STT, and CTT

- GST: Under Section 16 of the IGST Act, supplies to SEZ units and developers qualify as zero-rated. IFSC entities supplying services to other IFSC/SEZ units or exporting services to offshore clients can claim zero-rated treatment — though export-of-services conditions must be satisfied for each transaction type

- STT and CTT: Trading in IFSC exchanges is exempt from Securities Transaction Tax and Commodity Transaction Tax, making participation significantly cheaper than equivalent domestic market activity

FEMA Treatment and Foreign Currency Operations

IFSC entities transact in freely convertible foreign currencies and are treated as non-residents under FEMA. Capital flows, profit repatriation, and foreign currency transactions face substantially fewer restrictions than in mainland India. For NRI investors and multinational corporates, this removes friction that typically complicates cross-border wealth management.

For NRI and UHNI clients, iVentures Wealth integrates GIFT City structures — including IFSC-domiciled USD-denominated investment vehicles — into its cross-border tax optimisation advisory.

Who Is Eligible to Operate or Invest in GIFT City IFSC?

Entity Types Permitted to Set Up in GIFT City

A broad range of entities can establish operations in GIFT City IFSC:

- Indian companies and LLPs

- Foreign companies and their branches

- Banks (Indian and international, as IBUs)

- Insurance companies and intermediaries

- Fund Management Entities (FMEs)

- Payment service providers

- FinTech and TechFin entities

- Global In-house Centres (under the GIC Regulations, 2025)

- Professional and ancillary service providers

Individuals do not directly establish IFSC units — the regulatory frameworks operate at the entity level. Individual investors, including UHNIs and NRIs, access GIFT City through regulated investment products and banking channels.

Investor Eligibility by Product Type

Eligibility varies depending on the investment vehicle:

- Accredited Investors can access restricted and venture capital schemes with minimum thresholds of USD 150,000 and USD 250,000 respectively. IFSCA's proposed criteria include net worth of USD 200,000 or annual income of USD 50,000 — verify final regulations before relying on these thresholds

- NRIs and OCIs can access GIFT City products including IFSC exchange-listed securities, IBU banking products, and qualifying fund schemes. IFSCA maintains a dedicated NRI/OCI access page detailing available pathways

- Resident individuals (Indian tax residents) can remit up to USD 250,000 per financial year under LRS for permitted purposes, including qualifying GIFT City investment products — note that LRS applies to resident individuals, not NRIs

- Corporates can access GIFT City for treasury operations, IBU banking, and fund investment

Getting Started with GIFT City Advisory

Navigating eligibility, registration, and compliance across GIFT City's multiple frameworks requires tailored structuring guidance. The right entry point — whether an IBU deposit, an AIF investment, a Family Investment Fund, or a direct listing — depends on entity type, residency status, investment objectives, and tax profile.

For NRI families and UHNIs with cross-border portfolios, iVentures Wealth (SEBI RIA INA000019026) integrates GIFT City structuring into its NRI wealth management and family office mandates. Minimum investable asset thresholds apply:

- ₹5 Cr for NRI/OCI clients

- ₹10 Cr for CXOs and professionals

- ₹50 Cr for corporates

- ₹100 Cr for family businesses

GIFT City advisory is delivered as part of a comprehensive wealth management relationship, coordinated with tax advisors and specialist counsel as needed.

Frequently Asked Questions

Who regulates GIFT City?

IFSCA (International Financial Services Centres Authority), established on April 27, 2020 under the IFSCA Act, 2019, is the unified regulator for all financial services within GIFT City's IFSC. It consolidates the powers previously held by RBI, SEBI, IRDAI, and PFRDA under a single-window framework.

What are the tax benefits for GIFT City entities?

Under Section 80LA, eligible IFSC units receive a 100% income tax deduction for any 10 consecutive years within the first 15 years of operations. Companies outside the new tax regime pay MAT at 9%. IFSC exchange transactions are exempt from STT and CTT, and qualifying supplies to SEZ/IFSC units attract zero-rated GST.

Who is eligible to invest in or operate from GIFT City?

Indian and foreign companies, banks, insurers, fund managers, fintech firms, and NRI/OCI investors are all eligible, with eligibility criteria and minimum thresholds varying by product or service type. Individuals access GIFT City through regulated vehicles rather than by setting up units directly.

What financial products are available through GIFT City IFSC?

GIFT City IFSC covers a broad range of foreign-currency-denominated products, including:

- AIFs, venture capital funds, and family investment funds

- Retail mutual funds and ETFs

- IFSC Banking Unit deposits and lending

- Securities listed on India INX and NSE IFSC

- Cross-border payment services and insurance solutions

How does GIFT City differ from investing in domestic India?

GIFT City transactions are treated as offshore under FEMA, conducted in foreign currencies, subject to the Section 80LA tax regime, and regulated by IFSCA rather than domestic regulators. This creates a materially different regulatory and tax environment compared to mainland India investing.

Can NRIs invest through GIFT City IFSC?

Yes. NRIs and OCIs can access GIFT City through IFSC Banking Units, qualifying fund schemes, and IFSC exchange-listed securities. The right structure depends on residency status, investment objectives, and the specific product, so it is worth reviewing these variables carefully before selecting a vehicle.