This growing wealth pool has attracted a crowded market of advisors — genuine fiduciaries, product distributors, and bank relationship managers who all use the same title. Picking the wrong one means paying hidden commissions, receiving biased recommendations, and watching compounding work against rather than for you.

The right advisor, by contrast, acts as a true financial partner: one who puts your interests first, charges transparently, and builds a plan around your life — not around their product shelf.

This guide tells you exactly how to tell the difference.

Key Takeaways

- Only SEBI Registered Investment Advisers (RIAs) are legally required to act as fiduciaries in India

- Always verify credentials (CFA, CFP) and SEBI registration before engaging any advisor

- Confirm exactly how your advisor is paid — by you, or by product manufacturers

- Walk away if an advisor pressures you into specific products or cannot provide a SEBI registration number

- A good advisor addresses your full financial picture: investments, taxes, estate planning, and long-term goals

What Does a Personal Financial Advisor Do?

A personal financial advisor evaluates your complete financial picture — income, assets, liabilities, goals, risk tolerance, and time horizon — and provides guidance tailored to where you are and where you want to go.

Some advisors focus exclusively on portfolio management. Others offer comprehensive planning across tax strategy, estate planning, retirement income, and succession. That scope difference directly determines the value you receive — and whether the advisor can actually handle your situation's complexity.

Types of Financial Advisors in India

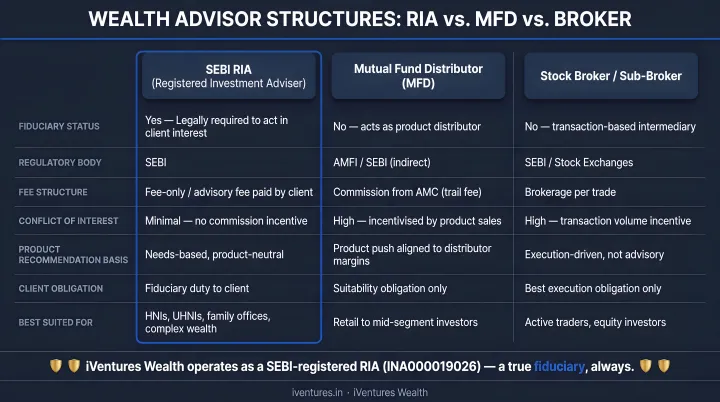

The Indian market has three broad categories, and conflating them is a costly mistake:

| Advisor Type | Regulatory Status | How They're Compensated | Fiduciary? |

|---|---|---|---|

| SEBI Registered Investment Adviser (RIA) | SEBI-registered | Fee paid by client | Yes |

| AMFI Mutual Fund Distributor (MFD) | AMFI ARN holder | Commissions from fund houses | No |

| Bank RM / Insurance Agent | Varies | Product commissions and trails | No |

SEBI RIAs operate under the Investment Advisers Regulations 2013, which legally requires them to act in a fiduciary capacity, disclose all conflicts of interest, and charge clients directly — not earn from product manufacturers. As of June 2026, SEBI lists only 1,044 registered Investment Advisers across India. Set against India's rapidly growing investable wealth, that number signals just how high the regulatory bar actually sits.

Mutual fund distributors hold an AMFI ARN and earn commissions from fund houses — they are not fiduciaries. The same applies to most bank relationship managers and insurance agents, regardless of the word "advisor" in their title.

Beyond these three categories, wealth managers and family office advisors serve HNI and UHNI clients with integrated services spanning investments, tax structuring, succession planning, and estate advisory. The category that fits you follows directly from the complexity of your financial situation and the scale of assets involved.

Key Factors to Consider When Choosing a Personal Financial Advisor in India

Selecting an advisor isn't just about credentials. It's about finding someone whose regulatory standing, expertise, incentive structure, and communication style align with your goals. Here's what to evaluate.

SEBI Registration and Fiduciary Status

This is the single most important check. Only SEBI-registered RIAs are legally required to act as fiduciaries — disclosing all conflicts of interest and placing your interests before their own. Distributors and agents operate under a fundamentally different standard.

You can verify any advisor's SEBI RIA registration on the SEBI Investment Adviser registry. Ask for the registration number directly and check it yourself. iVentures Wealth, for example, holds SEBI RIA registration INA000019026 — publicly verifiable, issued in 2010, and maintained continuously since.

An advisor who cannot or will not provide their SEBI registration number on request is a red flag.

Credentials and Qualifications

Titles are easy to claim — credentials can actually be verified.

- CFA (Chartered Financial Analyst): Requires passing three rigorous exams, meeting work experience requirements, and adhering to the CFA Institute's Code of Ethics. Verify CFA charterholder status through the CFA Society India member directory

- CFP (Certified Financial Planner): Built around financial planning standards, ethical practices, and lifelong learning. Verify CFP credentials through FPSB India's CFP Professionals Directory

Neither credential substitutes for SEBI RIA registration when it comes to providing regulated investment advice in India — but both signal a meaningfully higher standard of analytical and planning competence.

Ask for verifiable credential details, not just titles on a brochure.

Fee Structure and Transparency

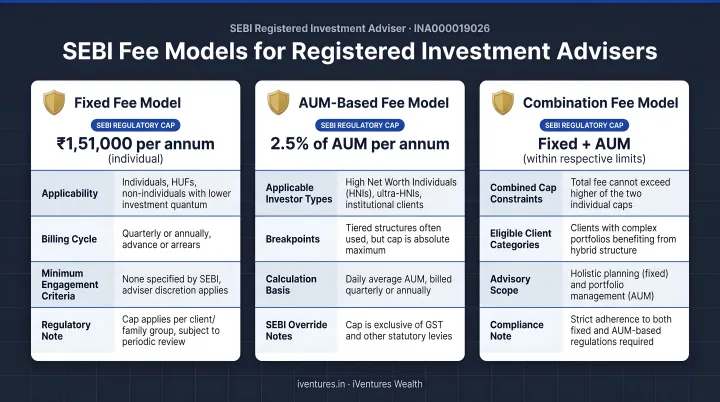

Three main fee models exist in India:

- AUM-based fee: A percentage of assets under advice, charged annually. SEBI caps this at 2.5% of Assets Under Advice per annum per client or family

- Fixed fee: A flat annual advisory fee. SEBI caps this at ₹1,25,000 per annum per client or family

- Commission-based: The advisor earns from product manufacturers, creating an inherent conflict of interest. Recommendations are shaped by what pays the advisor, not what suits you

Transparency is the metric that separates trustworthy advisors from the rest. Before engaging anyone, you should receive a clear written explanation of what you're paying, what you get in return, and how the advisor is compensated. No buried trail commissions. No undisclosed affiliations.

Track Record, Experience, and Service Breadth

Years of experience across different market cycles matters. An advisor who has navigated multiple bull and bear markets, regulatory changes, and economic disruptions will handle volatility more steadily than someone who has only operated in a single market environment.

Ask directly:

- How many client relationships do you currently manage?

- What is your total AUM?

- Have you received any industry recognition or awards?

- How many years have you been advising clients?

Beyond track record, assess the range of services offered. The best advisors cover wealth holistically: investments, tax planning, NRI advisory, estate and succession planning, and family office services.

A founder exiting a business has fundamentally different needs than a CXO managing a compensation portfolio or a family office overseeing generational assets. The right advisor should have demonstrated experience with clients who share your financial profile and complexity.

Relationship Fit and Communication

The advisor-client relationship is long-term and personal. A good advisor asks thoughtful questions about your goals, your values around money, and your risk psychology before making a single recommendation. Risk questionnaires are a starting point, not a substitute for genuine conversation.

Accessibility also matters. Clarify upfront:

- How frequently will portfolio reviews occur?

- Do you have a dedicated point of contact?

- Will the advisor proactively reach out during significant market events, or only during scheduled reviews?

Red Flags to Watch Out For and Questions to Ask

Some warning signs are easy to miss when an advisor presents confidently. Watch for these:

Red flags specific to India:

- Cannot provide a SEBI RIA registration number on request

- Pushes specific mutual fund schemes without clear suitability rationale (often high-commission products)

- Promises fixed or guaranteed returns — a direct regulatory violation

- Discourages questions about fees or compensation structure

- No written disclosure document provided before onboarding

SEBI has issued enforcement orders against unregistered advisory entities — including M/s NIFM Equity and Commodity Research — confirming that "investment advisory" claims without valid registration carry real regulatory risk for clients. Before signing anything, verify your advisor's standing directly on SEBI's enforcement orders database.

Questions to ask every advisor before signing anything:

- Are you a SEBI Registered Investment Adviser? What is your registration number?

- How are you compensated — do you earn any commissions from product manufacturers?

- Can you provide your disclosure document and client agreement before we proceed?

- Who will I work with if my primary contact leaves the firm?

- Has your firm faced any SEBI disciplinary actions or client complaints on record?

How iVentures Wealth Can Help

iVentures Wealth is a SEBI Registered Investment Adviser (registration INA000019026) with over 20 years in wealth advisory and capital markets. The firm manages ₹1,146+ Crores in assets across 150+ client relationships — affluent families, UHNIs, CEOs, CXOs, founders, and NRIs.

Founded in 2005 by Nirmal A Bansal — a UCLA Anderson alumnus and former Merrill Lynch professional — iVentures was built on a straightforward idea: your advisor's interests should align with yours, not with the products they sell. That philosophy shapes everything below.

What sets iVentures apart:

- CFA-led research: Krishna Makhariya, CFA Charterholder and Head of Research, leads independent investment analysis across equities, debt, alternatives, and global markets — every recommendation is grounded in evidence, not product incentives

- Fee-only model: As a SEBI RIA, iVentures cannot accept commissions or trail income from product manufacturers — clients pay one transparent advisory fee and receive unbiased recommendations across mutual funds, equities, bonds, and alternatives

- Comprehensive services: Portfolio management, tax optimisation, NRI and OCI advisory, cross-border DTAA structuring, estate and succession planning, family office services, and corporate treasury advisory

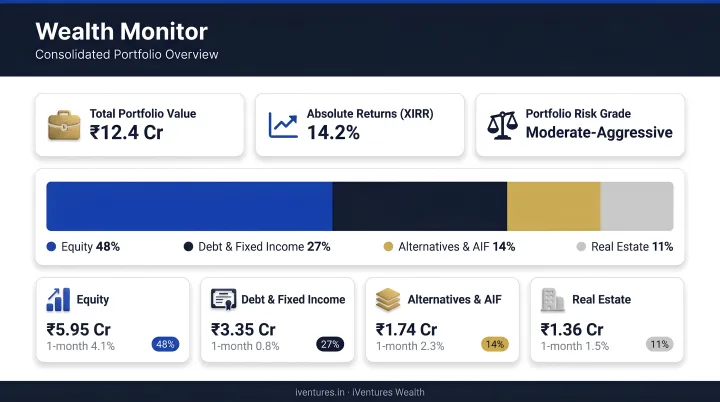

- Real-time portfolio visibility: The Wealth Monitor App (launched 2020, rated 4.7 stars on Apple App Store) consolidates all investments — mutual funds, equities, bonds, PMS, AIFs — into a single dashboard with daily performance tracking

- Recognised expertise: Named Preferred Wealth Partners of 2022 by the Government of Haryana, with industry panel participation alongside SIDBI and IamSMEofIndia leadership

iVentures serves clients across Delhi NCR, Gurugram, Mumbai, and NRI clients globally. Minimum investable assets: ₹5 Crore for NRIs/OCIs, ₹10 Crore for CXOs and professionals, ₹50 Crore for corporates, and ₹100 Crore for family businesses.

To start a discovery conversation, reach out at info@iventures.in or +91 124 463 4433.

Conclusion

The right personal financial advisor in India is non-negotiable on three fronts: SEBI RIA registration that confirms fiduciary accountability, a fee structure with no hidden product commissions, and an advisory relationship built around your specific goals — not a generic portfolio template.

Before you sign anything, act on these steps:

- Verify SEBI RIA registration directly on the SEBI SCORES portal

- Ask explicitly how the advisor earns — fee-only, commission, or both

- Review their regulatory history and any past client complaints

- Revisit the relationship periodically as your income, assets, and life stage shift — because the right advisor at 35 may not be the right advisor at 55

The advisory market in India is noisy, and not every registered firm operates with the same standards. Use the criteria in this guide as your filter — and apply it without compromise.

Frequently Asked Questions

What does a personal financial advisor do?

A personal financial advisor evaluates your complete financial situation and provides tailored guidance on investments, tax planning, retirement, estate planning, and wealth preservation. The scope varies by advisor type — SEBI RIAs typically provide the most comprehensive, conflict-free coverage across all these dimensions.

How much does a personal financial advisor cost in India?

SEBI RIAs can charge either up to 2.5% of Assets Under Advice per annum or a fixed fee of ₹1,25,000 per annum per client/family, subject to SEBI conditions. Commission-based distributors earn from product manufacturers rather than clients directly — but that cost is embedded in the products you hold, without direct disclosure to the client.

Is a personal financial advisor worth the money?

For individuals with significant assets, complex financial situations, or major life transitions, professional advisory typically pays for itself through optimised investment decisions, tax savings, and avoided costly mistakes. In practice, a single well-structured tax decision or avoided mis-allocation can exceed years of advisory fees.

Can a personal financial advisor help with retirement and pension planning?

Yes. A qualified advisor can structure retirement income across NPS (note: NPS intermediation falls under PFRDA regulation) and EPF, while building a portfolio that generates reliable post-retirement cash flow suited to your longevity and income needs.

What is the difference between a SEBI RIA and a mutual fund distributor in India?

A SEBI RIA charges the client a fee and is legally obligated to act as a fiduciary, placing your interests first and disclosing all conflicts. A mutual fund distributor earns commissions from fund houses and is not held to a fiduciary standard.

How do I verify a financial advisor's credentials in India?

Verify SEBI RIA registration on the SEBI Investment Adviser registry. Cross-check CFA credentials via CFA Society India and CFP credentials via FPSB India. Also review SEBI's enforcement orders database for any disciplinary history before signing.