Introduction

Most conversations about GIFT City stop at "the tax benefits are significant." What they rarely address is how those benefits actually get captured — and what it costs when they don't.

India's GIFT City (Gujarat International Finance Tec-City) has grown into a credible financial center with over 1,147 registered entities and USD 111B+ in banking assets as of early 2026.

For NRIs, family offices, and UHNIs, it offers something genuinely different: a distinct regulatory and tax framework that sits outside standard Indian tax treatment, governed by the International Financial Services Centres Authority (IFSCA).

Knowing GIFT City exists is not the same as benefiting from it. Far fewer investors have actually structured their portfolios to capture what's on offer — leaving capital gains tax exposure, transaction levies, and compliance friction on the table year after year.

This article breaks down the specific tax provisions within GIFT City's IFSC framework, which investor types gain the most from each, and what practical structuring actually involves.

Key Takeaways

- Section 47(viiab) exempts qualifying non-resident transfers on IFSC exchanges from capital gains tax.

- IFSC transactions are exempt from STT, CTT, stamp duty, and GST, reducing per-trade costs below domestic equivalents.

- IFSC entities qualify for 100% income tax deduction under Section 80LA for any 10 consecutive years within a 15-year window, extended to March 2030.

- Interest income on qualifying funds lent to IFSC units is fully exempt under Section 10(15)(viii); dividends attract a concessional 10% rate under Section 115A.

- DTAA benefits stack on top of IFSC-specific exemptions, creating dual-layer tax efficiency that domestic channels cannot replicate.

What GIFT City's IFSC Actually Is

GIFT City is India's first International Financial Services Centre, located in Gandhinagar, Gujarat, established under the International Financial Services Centres Authority Act, 2019. IFSCA serves as its unified regulator covering banking, securities, insurance, and fund management.

The key legal distinction lies in FEMA IFSC Regulations, 2015: financial institutions and branches operating within an IFSC are treated as persons resident outside India. That precise FEMA formulation — not a loose offshore label — is what unlocks a distinct set of regulatory and tax provisions unavailable to domestic investors or domestic financial institutions.

Two IFSC-regulated exchanges operate within GIFT City:

- India INX (India International Exchange) — India's first international exchange at GIFT IFSC, offering index derivatives, single-stock derivatives, and debt listings

- NSE IX (NSE International Exchange) — operates from GIFT IFSC with derivatives coverage and access to international market instruments

GIFT City is a jurisdiction and structural choice. Which exchange, entity type, and instrument an investor uses within GIFT IFSC directly determines the applicable tax treatment, repatriation rules, and regulatory norms — making the structural decision itself a core part of tax planning.

Key Tax Benefits of Investing Through GIFT City IFSC

These are codified provisions under Indian income tax law and IFSCA regulations. Their impact on net returns is real — but only when the right investment structures are in place.

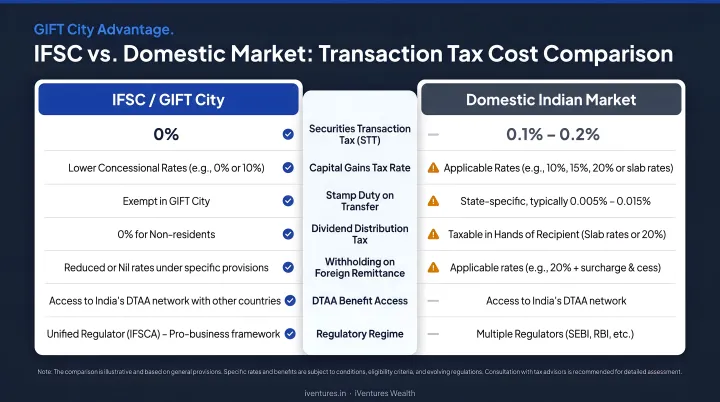

Capital Gains and Transaction Tax Relief

Section 47(viiab) is the operative provision here. It treats qualifying transfers by non-residents of bonds, GDRs, rupee-denominated bonds, derivatives, and notified securities — transacted on a recognised IFSC stock exchange for foreign-currency consideration — as not a transfer for income tax purposes. The result: no Indian capital gains tax on those transactions.

This applies most directly to:

- Large single-ticket investments in listed IFSC-exchange securities

- Actively managed Category III AIF structures where transaction velocity is high

- High-frequency portfolio rebalancing where gains would otherwise trigger repeated tax events

The transaction-tax relief compounds this further. According to IFSCA-hosted EY material on GIFT City IFSC tax benefits, transactions carried out on GIFT IFSC exchanges attract no STT, CTT, stamp duty, or GST.

For context on what domestic markets cost: NSE data shows STT on equity delivery trades at 0.1% on purchase and sale, with options sale STT revised upward to 0.10% from October 2024 per a September 2024 NSE circular. The government collected ₹52,196.86 crore in STT in FY 2024-25, with revised estimates of ₹63,670 crore for FY 2025-26. These are real costs borne by domestic-market participants — costs that IFSC-structured investments can legitimately avoid.

Income Tax Exemptions for Investors and Entities

There are two distinct layers here, and conflating them is a common mistake.

For entities — fund management entities, banks, AIFs, and financial institutions set up within GIFT City — Section 80LA provides a 100% deduction on income for any 10 consecutive assessment years out of 15. Budget 2025 extended the sunset for IFSC unit commencement under this provision to 31 March 2030, making this window time-bound but still open.

As of June 2025, IFSCA statistics show 118 registered Fund Management Entities in GIFT IFSC, with AIF AUM exceeding USD 18 billion — growth that reflects the compounding appeal of tax-efficient fund operations.

For individual investors, two specific income categories attract relief:

| Income Type | Provision | Treatment |

|---|---|---|

| Interest on qualifying funds lent to IFSC units | Section 10(15)(viii) | Fully exempt |

| Dividend from IFSC unit (non-resident) | Section 115A | Concessional 10% rate |

Budget 2025 added further provisions: the Section 10(10D) relief was extended to life insurance policies issued by IFSC insurance intermediary offices, and the Section 47(viiad) deadline for tax-neutral relocation of offshore funds to GIFT City was extended to 31 March 2030, with expanded coverage to retail schemes and ETFs (effective April 2026 for capital gains purposes).

This entity-level efficiency is not abstract. When fund managers operating inside GIFT City retain more post-tax income, that efficiency flows through to fund performance and distributions — which is precisely why the AIF ecosystem has scaled as rapidly as it has.

This structure is most relevant for:

- UHNIs and family offices with substantial recurring income from financial instruments

- NRIs earning interest on IFSC banking unit deposits

- Corporates evaluating treasury management through GIFT City

Cross-Border Advantages: Repatriation, PAN Relief, and DTAA Benefits

The FEMA treatment of IFSC units as persons resident outside India supports a meaningful cross-border advantage. NRIs and OCIs can hold foreign-currency accounts (USD, EUR, GBP) through GIFT IFSC banking units, with the structural flexibility to repatriate capital and returns without the additional compliance steps that apply to standard domestic investment routes.

PAN relief is verified under Rule 114AAB, which exempts qualifying non-residents and foreign companies from Section 139A PAN requirements where specific IFSC fund or exchange conditions — and required investor information requirements — are met.

Return filing relief for certain non-residents investing through IFSC structures has also been identified under CBDT Notification 119/2021, though eligibility is structure-specific and should be confirmed with a qualified adviser before relying on it.

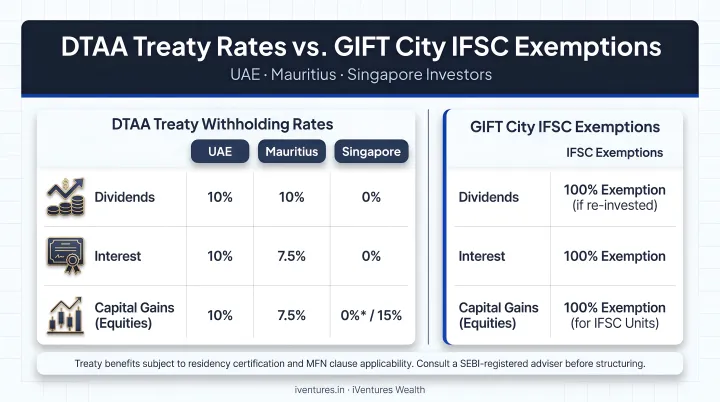

DTAA layering adds another dimension. Where India has a tax treaty with an NRI's country of residence, applicable provisions can further reduce withholding on dividends and interest — creating dual-layer tax efficiency:

| Residence Country | Dividend Treaty Cap | IFSC Comparison |

|---|---|---|

| UAE | 10% | Section 115A IFSC rate also 10%; Section 10(15)(viii) interest exemption may produce a better result |

| Mauritius | 5% (if beneficial owner holds ≥10% of capital); 15% otherwise | Treaty may reduce dividend below 10% for qualifying corporate holders; interest exemption may override treaty entirely |

| Singapore | 10% (if beneficial owner owns ≥25% of shares); 15% otherwise | IFSC 10% aligns with qualifying Singapore cap; interest exemption may supersede treaty relevance |

DTAA benefits and GIFT City-specific exemptions are not mutually exclusive. Which one produces the better outcome depends on investor type, beneficial ownership structure, and documentation. There is no universal rule that applies across all cases. iVentures Wealth advises NRI clients from UAE, Singapore, and other DTAA-treaty countries on exactly this kind of layered structuring, coordinating GIFT City vehicles with treaty benefit claims as part of broader cross-border tax planning.

What Investors Lose by Not Using GIFT City's Tax Framework

Investors who continue routing capital through domestic channels — or through offshore hubs like Singapore — without evaluating the GIFT City alternative absorb STT, GST, and capital gains tax loads on every eligible transaction. These are not marginal costs. With STT collections running at ₹52,000+ crore annually across Indian markets, these levies represent a substantial real cost pool that IFSC-structured investments can legitimately bypass.

Three specific loss patterns are worth naming:

Structural mismatch — Many investors are aware of GIFT City conceptually but hold investments through non-IFSC-compliant vehicles. Standard Indian tax treatment applies regardless of whether better options exist within the same jurisdiction. Awareness without structure delivers no benefit.

Window risk — The Section 80LA tax holiday and the Section 47(viiad) fund relocation deadline both run until March 2030. Entities and investors who delay may find eligibility conditions have changed or the window has narrowed by the time they engage seriously.

The advisory gap — Most investors who miss these benefits do so not from lack of interest, but because they have not worked with advisers who understand both the IFSC regulatory framework and individual portfolio structuring. The result is tax drag that persists for years, driven by incomplete structuring rather than poor investment choices.

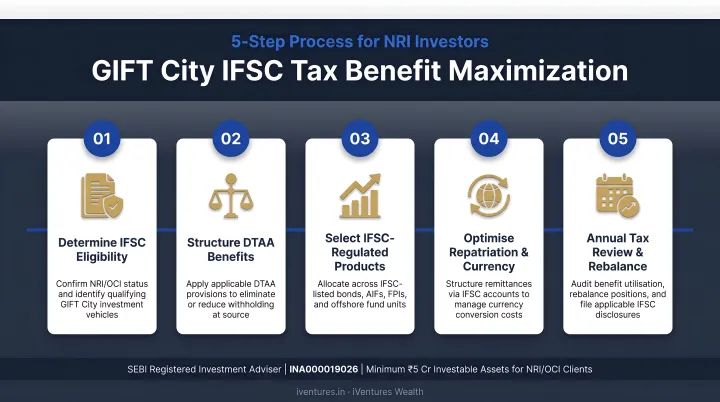

How to Maximise GIFT City Tax Benefits in Practice

Maximising GIFT City tax benefits is a structuring exercise, not a product selection exercise. The specific exemption that applies — and whether it applies at all — depends on decisions made at the vehicle level, the holding structure, and the transaction platform chosen.

Here is the practical sequencing:

Audit eligible income categories — Identify which income streams from existing or planned investments (interest, dividends, capital gains on listed securities) could qualify for IFSC-specific treatment if rerouted through the right structure.

Evaluate entity-level options — If you are a family office, corporate treasury, or UHNI with recurring financial income, assess whether establishing or investing through an IFSC-regulated entity makes Section 80LA relevant to your situation.

Confirm DTAA residency status — For NRIs and OCIs, determine your treaty country, applicable rates on dividend and interest income, and whether the IFSC domestic exemption or the treaty provision produces the better outcome.

Route through IFSCA-regulated intermediaries — All investments must go through IFSCA-regulated and SEBI/RBI-compliant intermediaries. Routing through non-compliant intermediaries eliminates eligibility for the exemptions entirely.

Review annually — GIFT City's regulatory landscape has moved quickly. Budget 2025 alone introduced extensions, new fund categories, and revised insurance provisions. Investors who do not review their GIFT City positioning annually risk missing new exemptions or inadvertently losing eligibility for existing ones.

Each of these steps requires specialist coordination across tax, compliance, and portfolio domains — not sequential checklists handled by different advisers.

iVentures Wealth's NRI and UHNI advisory practice addresses this through a single mandate that integrates GIFT City structuring, DTAA coordination, consolidated USD/INR reporting, and FEMA compliance. As a SEBI-registered investment adviser with deep cross-border structuring experience, the firm ensures these provisions are applied with precision — not just acknowledged on paper.

Frequently Asked Questions

What are the tax rules for GIFT City?

GIFT City IFSC operates under a targeted tax framework covering Section 47(viiab) (non-resident capital gains exemptions), Section 80LA (entity tax holidays), Section 10(15)(viii) (interest income exemptions), and Section 115A (concessional 10% dividend tax). Zero STT, CTT, stamp duty, and GST apply to eligible IFSC exchange transactions.

Who is eligible for GIFT City?

GIFT City IFSC is open to domestic investors, NRIs, OCIs, FPIs, AIFs, banks, insurance companies, and fintech firms. NRIs and global investors benefit especially from repatriation flexibility and potential PAN or return filing relief under qualifying structures.

What are the main benefits of GIFT City?

Key benefits include a globally competitive tax framework, USD-denominated instrument access, a unified IFSCA regulatory environment, exemption from multiple transaction taxes, and full repatriation of capital and returns. Entities also qualify for a 100% income tax holiday under Section 80LA.

Is GIFT City income tax-free for investors?

Not universally. Specific income streams — interest on qualifying funds lent to IFSC units and capital gains on specified listed securities transferred by non-residents — are exempt. Dividends benefit from a concessional 10% rate under Section 115A rather than full exemption. The framework is targeted, not a blanket waiver.

Can NRIs invest in GIFT City without an Indian PAN?

Under certain IFSC investment structures, qualifying non-residents may be exempt from PAN requirements under Rule 114AAB. Eligibility depends on the specific investment vehicle, investor type, and conditions met — this should be confirmed with a qualified adviser before relying on it for any specific transaction.

How does GIFT City compare to domestic Indian markets from a tax perspective?

IFSC-eligible investments avoid STT, stamp duty, GST, and domestic capital gains tax rules that apply on Indian exchanges. For active investors and larger portfolios, this creates a materially lower transaction cost base — particularly in equity derivatives, where domestic STT on options sales now runs at 0.10%.