This scenario plays out more often than most Indian women would admit. Retirement planning for women isn't just under-discussed — it's structurally harder. Longer lifespans, career breaks, the gender pay gap, and deeply ingrained financial dependence combine to create a retirement gap that quietly widens every year. The good news: awareness is the starting point, and starting at any life stage makes a real difference.

Key Takeaways

- Women in India live longer than men on average, so retirement savings must stretch further — start investing early and stay consistent

- Career breaks and the gender pay gap quietly erode EPF/NPS balances, compounding the savings shortfall over decades

- NPS, PPF, EPF, and ELSS are powerful instruments — own these decisions rather than leaving them to default or a spouse

- Women in their 40s and 50s can still meaningfully catch up with the right strategy

- Working with a SEBI-registered, fiduciary advisor measurably improves retirement outcomes

Why Retirement Planning Is Different for Women in India

Retirement planning follows the same rules for everyone — but the outcomes diverge sharply along gender lines.

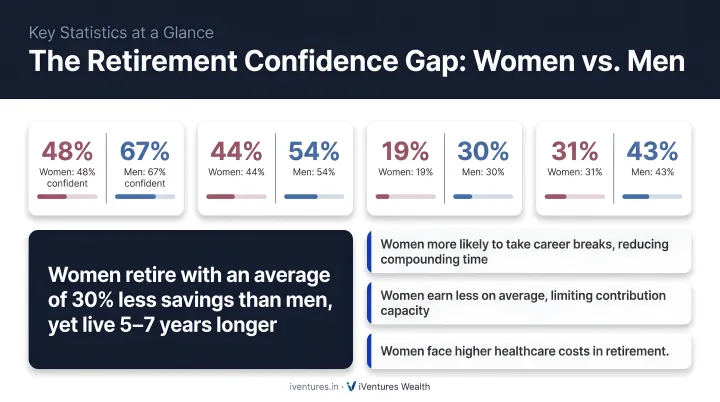

According to the Axis Max Life India Retirement Index 5.0, women score just 49 out of 100 on retirement preparedness, and only 39% are confident their savings will last more than a decade. That's not a reflection of capability — it's the result of structural and social conditions that work against women's long-term financial security.

The Longevity Problem

World Bank data shows Indian women have a life expectancy of 73.6 years versus 70.8 years for men. That 2.8-year gap at birth often translates to 5–8 more years of retirement to fund in practice, once age at retirement and widowhood patterns are factored in. A retirement corpus that seems adequate for a man may simply run short for a woman.

The Dependence Pattern

Many Indian women — including working professionals — defer financial decisions entirely to spouses or fathers. This leaves them dangerously unprepared for life events like widowhood, divorce, or a spouse's incapacitation. Building financial independence is, at its most practical level, a contingency plan for life's uncertainties.

The Confidence Gap

BlackRock's 2024 research puts the gap in stark numbers:

- Only 59% of women feel on track to retire with their desired lifestyle, versus 75% of men

- 65% of women worry about outliving their savings

The gap reflects a deficit of financial education, not ability. A structured plan — started early and owned personally — is what closes it.

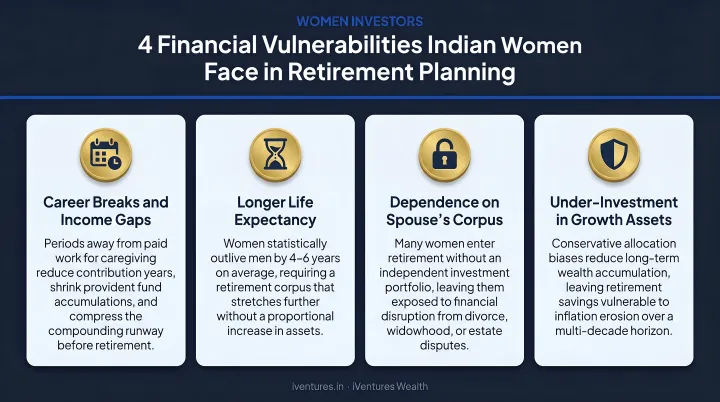

Key Retirement Challenges Women Face in India

Shorter Earning Windows Due to Career Breaks

India's caregiving burden falls disproportionately on women. MoSPI's 2024 Time Use Survey found 41% of Indian women aged 15–59 participate in caregiving, spending nearly double the time men do on unpaid care work. When caregiving intensifies, women leave the workforce — or shift to part-time work — creating gaps in EPF and NPS contributions precisely during their 30s, when compounding is most powerful.

A 3–5 year career break at age 32 doesn't just mean fewer contributions. It means the compound growth on those missing contributions is gone permanently. Over a 25-year horizon, that compounding loss can easily outweigh the missed contributions themselves.

The Gender Pay Gap and Its Retirement Impact

PLFS 2023-24 data shows urban salaried women earn ₹19,879/month on average versus ₹26,105 for men — a gap of 23.9%. In rural areas, the gap widens to 31.9%. Lower income means lower EPF contributions, lower NPS accumulations, and less surplus available for additional investing. Compounded over a 25-year career, this gap in contributions translates into a substantially smaller retirement corpus.

Higher Healthcare Costs in Retirement

NSS 75th round analysis estimates average annual out-of-pocket health spending for Indians aged 60+ at approximately ₹23,459 — and 81% of older adults lack any health insurance. Women who live longer face more years of these expenses. Building a dedicated healthcare reserve — separate from the core retirement corpus — is one of the most overlooked steps in women's retirement planning.

Financial Vulnerability After Widowhood or Divorce

LASI data shows 36% of Indians aged 60+ are widowed, and widows experience measurably lower household consumption than married women.

The practical consequences arrive fast and all at once:

- Managing finances independently for the first time

- Navigating EPF/NPS pension transfers in a spouse's name

- Handling succession, nominee claims, and estate documentation

- Maintaining household consumption without a second income

Joint planning helps, but it's not a substitute for independent financial literacy and individually held assets.

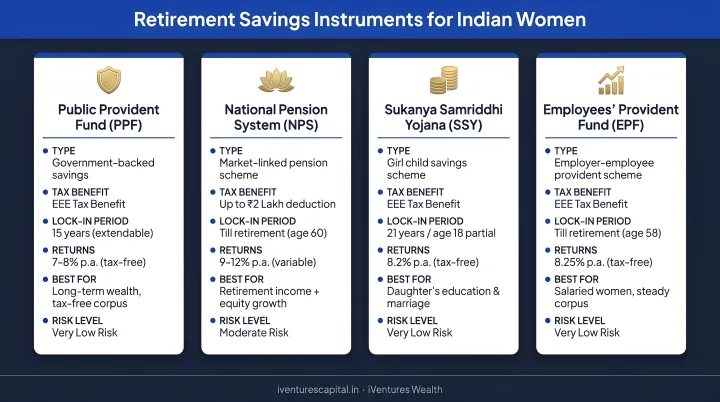

Retirement Savings Instruments Every Woman Should Know

Choosing the right savings instruments — not just saving more — is what separates a comfortable retirement from a stressful one. Here's a practical breakdown of the instruments most relevant to Indian women at different career and life stages.

National Pension System (NPS)

NPS is one of the most effective long-term retirement tools available to Indian women. Key facts:

- Open to any Indian citizen aged 18–70, including homemakers (under the All Citizen Model)

- Additional tax deduction of up to ₹50,000 under Section 80CCD(1B), over and above the ₹1.5 lakh Section 80C limit

- Equity and debt allocation across Active or Auto Choice options, at low fund management costs, with an annuity-based income structure at exit

- Under PFRDA's December 2025 exit amendment, non-government subscribers exiting normally can take up to 80% as lump sum if the corpus exceeds ₹8 lakh

NPS works especially well for women who want a structured, tax-advantaged retirement vehicle that runs independently of an employer.

Public Provident Fund (PPF)

PPF is ideal for conservative investors and those mid-career who want guaranteed, government-backed accumulation:

- Current interest rate: 7.1% per annum

- EEE tax status — contributions deductible under 80C, interest and maturity proceeds tax-free

- Minimum annual deposit ₹500; maximum ₹1.5 lakh

- 15-year lock-in, extendable in 5-year blocks

The 15-year lock-in enforces savings discipline — particularly useful during career transitions when the temptation to dip into savings is highest.

EPF and Voluntary Provident Fund (VPF)

For salaried women, EPF is the foundation of retirement savings:

- Standard employee contribution: 12% of wages, currently earning 8.25% interest for FY 2024–25

- VPF allows voluntary contributions above the mandatory 12%, with the same tax treatment and interest rate

- Critical mistake to avoid: withdrawing EPF during a job change. This is one of the most common and costliest retirement planning errors Indian women make

ELSS Mutual Funds

For women with a longer time horizon and moderate-to-high risk tolerance, ELSS offers equity-linked growth with a tax benefit:

- Qualifies for Section 80C deduction (within the ₹1.5 lakh limit)

- Shortest lock-in among 80C instruments: 3 years per SIP instalment

- At least 80% invested in equity — returns are market-linked, not guaranteed

- SIP-based investing makes it accessible even during lower-income periods

Senior Citizen Savings Scheme (SCSS) and Post-Retirement Options

For women at or approaching retirement:

| Instrument | Key Feature | Current Rate |

|---|---|---|

| SCSS | Available from age 60 (55 for VRS retirees) | 8.2% p.a. |

| RBI Floating Rate Bonds | 7-year tenure, taxable | 8.05% (Jan–Jun 2026) |

| SWP from Mutual Funds | Monthly income from existing corpus | Market-linked |

Fixed deposit laddering and systematic withdrawal plans (SWP) from debt or hybrid funds can provide predictable monthly income without depleting capital rapidly.

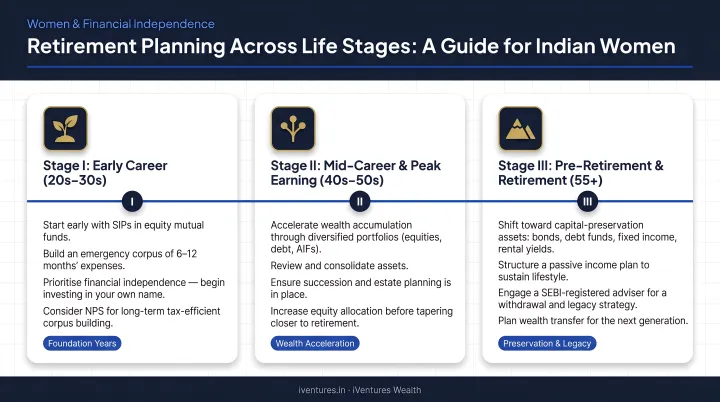

Retirement Planning by Life Stage

In Your 20s and 30s: Build the Foundation

Start immediately. The compounding math is unambiguous:

| Monthly SIP | Return Assumption | Over 20 Years | Over 30 Years |

|---|---|---|---|

| ₹2,000 | 10% p.a. | ₹15.3 lakh | ₹45.6 lakh |

| ₹2,000 | 12% p.a. | ₹20.0 lakh | ₹70.6 lakh |

The 30-year figure is roughly 3–3.5 times the 20-year figure. Ten years of delay doesn't just shrink your corpus — it can cut it by more than half. These numbers are illustrative at ₹2,000/month; the proportional impact of compounding scales identically across any contribution size.

Priorities for this decade:

- Open NPS and begin contributions on your first salary

- Start a PPF account

- Begin ELSS SIPs — consistency matters more than contribution size in the early years

- Don't withdraw EPF when changing jobs

In Your 40s: Accelerate and Catch Up

This is typically the peak earning decade — and the window where catch-up contributions have the most impact.

- Increase SIP amounts substantially — don't let lifestyle inflation consume all salary growth

- Maximise both Section 80C (₹1.5 lakh) and 80CCD(1B) (additional ₹50,000 via NPS)

- If returning after a career break: resume contributions immediately and increase VPF or SIP amounts to compensate for lost years

- Build a dedicated healthcare reserve and review insurance coverage

In Your 50s and Beyond: Shift to Preservation

By this stage, the goal shifts from accumulation to protecting what you've built.

- Gradually reduce equity exposure; move toward a balanced debt-equity allocation

- Use a retirement calculator to project actual income needs — don't rely on rough estimates

- Ensure all nomination details are updated across NPS, EPF, mutual funds, and bank accounts

- Arrange personal health insurance top-up plans before retiring, since employer group cover ends at retirement

Protecting Your Retirement: Insurance and Emergency Planning

Even a well-built corpus can be wiped out by a single unplanned health crisis. Two protection layers that most retirement plans overlook until it's too late:

Health Insurance: Don't rely solely on your employer's group policy — it ends the day you retire. Arrange a personal health insurance plan (with a top-up or super top-up if needed) while you're still employed and healthy — ideally in consultation with a licensed insurance advisor. Waiting until after retirement means higher premiums and stricter underwriting.

Emergency Fund: Maintain 6–12 months of living expenses in a liquid instrument — a high-yield savings account or liquid mutual fund. This is especially critical for single women, divorced women, or anyone approaching retirement without a partner's income.

Nomination Hygiene Checklist:

- Updated nominees on all NPS, EPF, mutual fund, and bank FD accounts

- Awareness of all family assets — not just your own accounts

- A will or succession document that reflects current intent

- At least one family member who knows where all accounts are held

Estate planning and nomination alignment are core to how iVentures Wealth structures retirement advisory through its Investments for HER programme — not added on after the portfolio is built, but woven into the plan from day one.

When and How to Work with a Financial Advisor

Bryn Mawr Trust's 2024 study of 826 affluent women aged 40+ found 87% felt financially well prepared for retirement when they had hands-on planning and advisor support. Only 57% preferred a professional advisor as their primary learning source — meaning a significant share of women are still navigating retirement planning without qualified guidance.

For Indian women, the advisor quality question matters as much as the decision to seek one. Look for:

- SEBI registration — verifiable on the SEBI public registry

- Fiduciary obligation — the advisor is legally required to act in your interest, not earn commissions from product manufacturers

- Fee transparency — you should know exactly what you pay and why

- Life-stage relevance — cookie-cutter advice doesn't account for career breaks, longevity planning, or single-woman household dynamics

iVentures Wealth, a SEBI-registered investment advisory firm (INA000019026) with 20+ years of experience, offers personalized retirement planning for women through its dedicated Investments for HER programme. The programme covers:

- Retirement and longevity planning

- Emergency fund structuring

- Catch-up strategies after career breaks

- Estate planning and wealth transfer

- Financial literacy workshops

Each plan is built around the individual woman's life stage, risk profile, and long-term goals. As a fee-only RIA, iVentures earns no commissions — removing the product-conflict that can arise when advisors are compensated by fund manufacturers rather than clients.

Frequently Asked Questions

What is the best age for a woman to retire?

Most Indian women target 55–60, but the more useful question is whether your corpus can sustain 25–30 years of post-retirement living. That number — not the retirement age — should drive your planning.

What are the 3 R's of retirement?

Resources (building sufficient savings and investments), Risk management (insurance, diversification, and contingency planning), and Retirement income (creating sustainable income streams post-work). For women, all three need to be calibrated for a longer horizon and higher healthcare costs.

How much should a woman save for retirement in India?

Target saving 15–20% of monthly income, with a retirement corpus of roughly 25–30 times your annual expenses. A SEBI-registered advisor can personalise this based on your current age, income, and expected lifestyle.

What retirement accounts are best for women in India?

A combination works best:

- NPS — market-linked growth with annuity income at retirement

- PPF — safe, tax-free long-term accumulation

- EPF/VPF — ideal for salaried women building a guaranteed corpus

- ELSS SIPs — equity exposure with 80C tax benefits

The right mix depends on your age, income, and risk tolerance.

How can women catch up on retirement savings after a career break?

Return to contributions as soon as you re-enter the workforce. Increase SIP amounts and VPF contributions to make up for missed years. Ten years of disciplined saving can still build a meaningful corpus — starting later is far better than not starting at all.

Should women invest differently than men for retirement?

The core principles are the same. Women do need to account for a longer retirement horizon, higher healthcare costs, and the likelihood of managing finances independently at some point. These factors argue for more equity exposure early on and make financial literacy especially important.