Introduction

You're in a wealth advisory meeting. Your adviser mentions private equity as a portfolio option — perhaps a Category II AIF targeting 14% IRR. The concept sounds compelling, but the mechanics aren't always clear. How does it fit with the rest of your portfolio? Is this replacing your wealth management strategy, or adding to it?

This confusion is common among founders, CXOs, and family office managers in India. Private equity and wealth management are not competing ideas — PE is one tool within a broader wealth management framework. This guide breaks down both — so you can evaluate PE on its own terms and decide whether it belongs in your portfolio.

Key Takeaways:

- PE means investing in unlisted companies with capital typically locked for 10+ years

- Wealth management is a holistic advisory service covering your entire financial life

- PE is one asset class within wealth management — not a replacement for it

- Fit depends on your liquidity needs, risk tolerance, and time horizon

- In India, PE is accessed via SEBI-regulated AIFs with a ₹1 crore minimum ticket

What Is Private Equity?

Private equity is capital invested into companies not listed on public stock exchanges. These can be startups, growth-stage businesses, or mature companies undergoing restructuring. Unlike buying shares of a listed company, PE investors take active ownership stakes and directly influence company direction, strategy, and operations.

The Fund Structure

PE capital is raised through a fund managed by a General Partner (GP). Individual and institutional investors participate as Limited Partners (LPs), committing capital for a defined period.

Key structural characteristics:

- Capital is typically locked for 10+ years — longer than most investors expect

- The J-curve effect means early returns are often negative, as fees are paid before portfolio valuations rise; meaningful assessment of a PE manager may require 5–6 years, with portfolio-level conclusions requiring at least 8 years

- The investment period (when capital is deployed) typically runs through the first half of the fund's life; returns are realised in the latter half

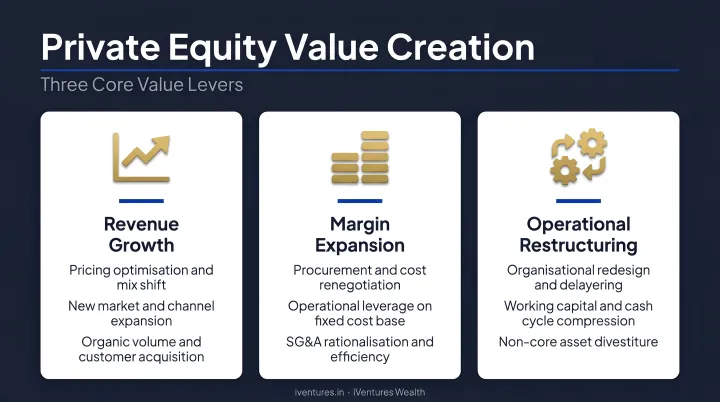

How PE Creates Value

Value creation in PE is hands-on and operational, not passive. According to McKinsey, well-executed value-creation programmes can deliver 25–45% margin growth through three core levers:

- Revenue growth: expanding markets, customer segments, or pricing power

- Margin expansion: operational efficiencies, procurement, and cost restructuring

- Operational restructuring: leadership changes, business model improvements, or carve-outs

Exits — the point at which investors realise returns — happen via IPO, merger/acquisition, or recapitalization, typically in the fund's latter years.

Who Invests and What It Costs

Traditionally, PE was the domain of pension funds, endowments, and sovereign wealth funds. Increasingly, UHNIs and family offices participate too. In India, HNI access to PE flows through SEBI-regulated Alternative Investment Funds (AIFs), with a statutory minimum investment of ₹1 crore per the SEBI AIF Regulations.

The standard fee model is "2 and 20":

- 2% annual management fee on committed capital

- 20% carried interest on profits above a hurdle rate (typically 8%)

Preqin's fund terms research found 44% of direct PE funds charge a 2% management fee, 82% use 20% carried interest, and 52% apply an 8% hurdle rate. For investors evaluating PE funds, the key question is whether net-of-fee returns meaningfully outpace what liquid alternatives — public equities or debt — would have delivered over the same period.

What Does Wealth Management Actually Cover?

Wealth management is an ongoing advisory relationship — not a one-time transaction. The CFA Institute defines private wealth management as combining financial planning and investment management for high-net-worth individuals. In practice, that spans portfolio construction, tax planning, estate planning, and multigenerational wealth transfer.

The Scope of Services

A comprehensive wealth management engagement covers:

- Portfolio construction across equities, fixed income, real estate, and alternative investments including PE and AIFs

- Tax optimisation — structuring portfolios to manage LTCG, STCG, and DTAA implications

- Estate and succession planning — wills, trusts, and intergenerational transfer structures

- Family governance — particularly relevant for business families managing promoter stakes and multiple entities

- Consolidated reporting — a single view across all holdings, including illiquid AIF positions

The primary objective: maximise after-tax, risk-adjusted returns while aligning the portfolio with your goals, liquidity requirements, and time horizon.

Who It Serves — and How Complexity Scales

Wealth management serves a spectrum from mass affluent to UHNI. For affluent Indian families — founders, CXOs, NRIs managing assets across geographies — the service typically spans multiple entities and generations.

The scale of this segment is significant. The Kotak Private Top of the Pyramid Report (2024) reports India had 2,83,000 UHNIs in 2023 with combined wealth of ₹232 trillion — projected to reach 4,30,000 UHNIs and ₹359 trillion by 2028.

Within that cohort, the alternatives shift is already underway. UHNIs allocate an average of 18% to alternate assets, with 47% of UHNIs preferring PE, VC, or co-investing within that bucket — and 53% planning to increase their alternatives exposure further.

That context matters for how PE fits in: it is one allocation within a structured wealth plan, sized against liquidity needs, tax position, and time horizon — not a standalone strategy.

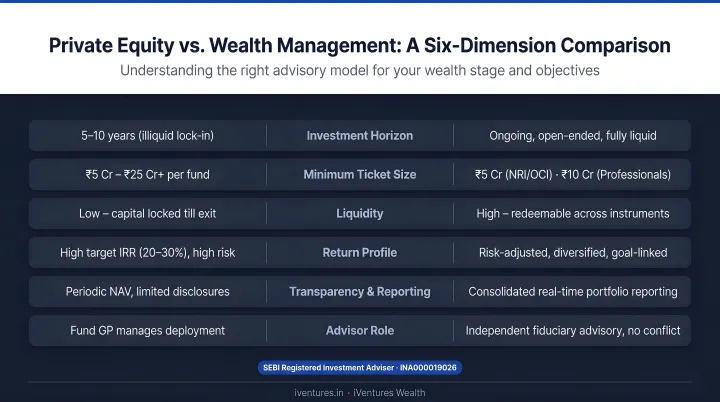

Private Equity vs. Wealth Management: Key Differences

These two concepts operate at different levels. Wealth management is the overall strategy; private equity is one specific instrument within it. The table below maps the key structural differences across six dimensions.

| Dimension | Wealth Management | Private Equity |

|---|---|---|

| Scope | Broad — all asset classes | Narrow — unlisted companies |

| Liquidity | Generally liquid; adjustable | Illiquid; 10+ year lock-up |

| Risk profile | Varies by client (conservative to aggressive) | High risk; illiquidity; potential total loss |

| Involvement | Passive advisory and monitoring | Active; GPs often control portfolio companies |

| Fee model | Advisory fee on assets under advice (SEBI cap: 2.5% AUA) | "2 and 20" — management fee plus carried interest |

| Return target | Risk-adjusted across diversified portfolio | Higher absolute return to compensate for illiquidity |

On Returns: What the Data Shows

Global PE benchmarks provide useful context. The Cambridge Associates US Private Equity Index delivered 15.05% net IRR over 10 years as of June 2024, versus 9.37% for the public-market equivalent (MSCI ACWI). For comparison, India's Sensex has delivered a CAGR of approximately 14.34% over 25 years — making the return premium from PE less automatic than often assumed.

PE's edge is not purely about illiquidity. Preqin describes a complexity premium: specialist skill in managing access, risk, and operational transformation generates returns that go beyond simply being paid for locking up capital.

In practice, this means fund manager quality determines outcomes more than any other variable. Manager selection is the primary driver of PE performance — not asset class exposure alone.

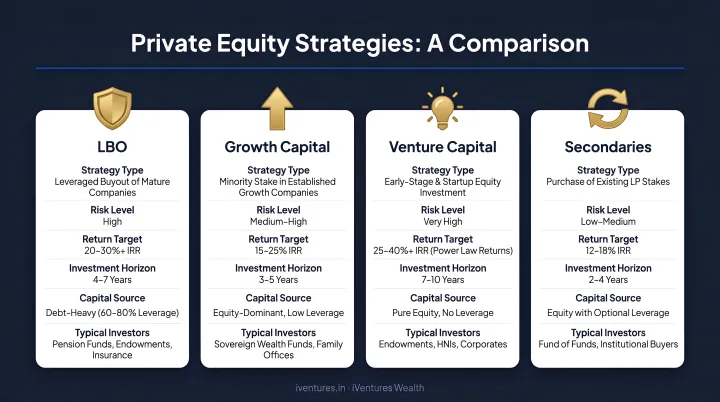

Common Private Equity Strategies You Should Know

Three strategies are most relevant for HNI investors evaluating PE exposure:

1. Leveraged Buyouts (LBO) Acquisition of mature, cash-generating businesses using a combination of equity and debt. The GP improves operations and exits at a profit. ILPA defines an LBO as an acquisition using significant borrowed capital — the debt amplifies returns but also amplifies risk.

2. Growth Capital Minority equity investment in established companies expanding into new markets or products. Unlike LBOs, there is no change of control. More common in India's PE market, where many high-growth companies seek capital without ceding majority ownership.

3. Venture Capital Early-stage equity in startups with high growth potential and correspondingly higher failure rates. Capital loss ratios have improved — Cambridge Associates data shows a drop from 51.5% for 1991–2001 vintages to 20% for 2002–2015 vintages. Even so, VC remains the highest-risk PE sub-strategy.

Secondary Investments: A More Accessible Entry Point

For first-time PE investors, secondary investments — buying existing LP interests from other investors in a PE fund — offer a meaningful advantage. Because you're buying into a seasoned portfolio that is typically 50–80% funded, the J-curve effect is reduced. Cambridge Associates reports secondaries may distribute cash as early as day one, with maximum out-of-pocket exposure of roughly 50–75% of total commitments.

On the performance side, Preqin data shows secondary funds with 2013–2022 vintages delivered 16% net IRR, rising to 19% for 2020–2022 vintages.

The Indian AIF Context

Whether investing through primary PE funds or secondary positions, Indian HNIs access these strategies through SEBI-regulated AIFs. The relevant categories are:

- Category I AIFs — venture capital funds, angel funds, infrastructure funds, SME funds

- Category II AIFs — private equity funds, real estate funds, debt funds, distressed asset funds

The minimum investment threshold is ₹1 crore per SEBI AIF Regulations. SEBI data shows cumulative net AIF commitments of ₹15,74,050 crore as of December 2025, with investments made totalling ₹6,45,026 crore. The broader India PE/VC market saw investments of approximately $43 billion in 2024, up ~9% year-on-year according to the Bain India PE Report 2025.

Is Private Equity Right for You?

PE is not suitable for every investor — even wealthy ones. The right profile looks like this:

- Surplus investable wealth beyond your core liquidity needs

- Multi-year investment horizon — you cannot access this capital for 10+ years

- Comfort with illiquidity — no exits mid-fund without significant discount

- Desire for diversification beyond public markets

If you meet these criteria, the next step is rigorous due diligence before any commitment.

Questions to Ask Before Committing

Before allocating to any PE fund:

- What percentage of my total portfolio can I afford to lock up for a decade?

- Do I understand this specific fund's strategy, the GP's track record, and the exit thesis?

- How does this fit with my overall tax position and financial goals?

- Am I adequately diversified across PE vintages to manage timing risk?

Risks to Understand Plainly

- Illiquidity — capital tied up for 10+ years, often with no secondary market

- Manager risk — PE returns are highly dispersed; manager selection drives outcome

- Capital loss — Cambridge data shows impairment ratios of 40.9% for VC and 27.7% for buyouts across 2002–2015 vintages

- Fee drag — "2 and 20" fees erode net returns substantially if gross performance is modest

PE works best as a strategic allocation within a diversified core portfolio — not as a replacement for one. In the Indian context, SEBI-regulated Category II and III AIFs are typically the regulated route for HNIs accessing private equity, and understanding fund structure, manager quality, and vintage diversification matters as much here as in any global market.

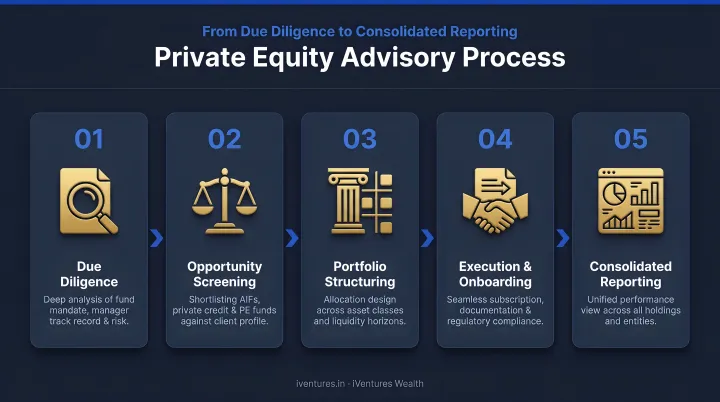

How a Wealth Manager Helps You Access and Evaluate Private Equity

Most HNI investors should not be evaluating PE funds independently. The analytical demands are substantial: manager track record, fund vintage, fee structure, exit history, sector concentration, drawdown schedule, and tax implications all require expert assessment.

What Good Wealth Manager Involvement Looks Like

A qualified, fiduciary wealth manager acts as a filter, not a sales channel. In practice, this means:

- Reviews GP track records, fund vintages, fee structures, and capital-call schedules before any recommendation

- Sizes your PE allocation against your liquidity profile and overall portfolio — so illiquid commitments don't crowd out near-term needs

- Coordinates with your chartered accountants on capital gains treatment, FEMA compliance, and DTAA considerations

- Consolidates PE and AIF positions alongside liquid holdings in a single portfolio view

- Tracks quarterly performance reports, capital-call schedules, and cash flows post-commitment

At iVentures Wealth, AIF advisory runs under a fee-only RIA model — the firm accepts no placement commissions, so recommendations reflect suitability rather than distribution revenue. The CFA-led research team handles fund-house due diligence, GP track-record review, and performance benchmarking as part of the standard advisory engagement.

Clients track AIF positions alongside mutual funds, equities, bonds, and other holdings through the Wealth Monitor App in a single consolidated dashboard.

Fiduciary Adviser vs. Distributor: A Critical Distinction

The distinction is straightforward — and consequential for PE specifically:

- A distributor earns placement commissions from recommending specific funds — creating a structural conflict between their incentive and your interest

- A fiduciary adviser (a SEBI-registered Investment Adviser) must act in your best interest, disclose all fees, and cannot accept compensation from product manufacturers

Under SEBI Investment Advisers Regulations 2013, a registered investment adviser cannot receive remuneration from any party other than the client for advice. This regulatory framework is the structural reason a SEBI RIA provides genuinely unconflicted PE guidance — while a distributor, however well-intentioned, cannot.

For UHNI clients making meaningful PE allocations, this determines one thing: whether the fund recommended is the best fit for your portfolio, or the one carrying the highest placement fee.

Frequently Asked Questions

What is private equity wealth management?

"Private equity wealth management" refers to the integration of PE investments into a broader wealth strategy — where a wealth manager evaluates, selects, and monitors PE or AIF allocations alongside other asset classes to meet your long-term financial goals. It is PE considered in context, not in isolation.

How does private equity differ from traditional wealth management?

Wealth management is a broad, ongoing advisory service covering diversified investments across liquid and semi-liquid asset classes. Private equity is one specific, illiquid asset class focused on private companies — PE is a tool used within wealth management, not a substitute for it.

Who can invest in private equity in India?

Individual investors typically access PE through SEBI-regulated AIFs, which require a minimum investment of ₹1 crore (₹25 lakh for employees or directors of an AIF or its manager). These instruments suit UHNIs and HNIs with significant investable surplus, a long investment horizon, and comfort with illiquidity.

What are the main risks of private equity investments?

The four primary risks are illiquidity (capital locked for 10+ years), manager risk (returns vary widely by GP quality), concentration risk (less diversification than public markets), and potential capital loss in early-stage or distressed strategies. High fees further erode net returns when gross performance is ordinary.

How long is the typical investment horizon for private equity?

Most PE funds have a lifecycle of 10+ years, with capital deployed in the first half and returns realised in the latter half. Investors should not commit capital they may need before this period ends. Early years often show negative returns due to the J-curve effect.

Do I need a wealth manager to invest in private equity?

Not mandatory, but genuinely valuable. A SEBI-registered investment adviser evaluates fund quality, assesses portfolio fit, manages tax implications, and ensures PE sits within a coherent strategy. Without that filter, investors risk choosing poorly structured funds or over-allocating to illiquid assets beyond their actual liquidity needs.