The right retirement tax planning advisor prevents this. The wrong one — or none at all — means you're reactive, not strategic. There's a meaningful difference between filing taxes correctly and structuring your retirement to legally minimise them.

This guide gives you a clear framework for evaluating and selecting a retirement tax planning advisor in India: what credentials to check, what questions to ask, and the red flags that should end a conversation early.

Key Takeaways

- A retirement tax planning advisor builds a year-round strategy — not just a March return

- In India, verify SEBI RIA registration first — it's the only licence for fee-based investment advice

- The right advisor operates as a fiduciary — no product commissions, no conflicts

- Start the engagement 5–7 years before retirement, not at the withdrawal stage

- Evaluate credentials, India-specific expertise, fee transparency, and holistic planning scope

What Is a Retirement Tax Planning Advisor?

A retirement tax planning advisor is a financial professional who provides ongoing, year-round advice on structuring retirement income, investments, and withdrawals to minimise lifetime tax liability. The scope extends well beyond annual return filing — it covers how income is sequenced, how gains are timed, and how withdrawals interact with your tax slab across retirement years.

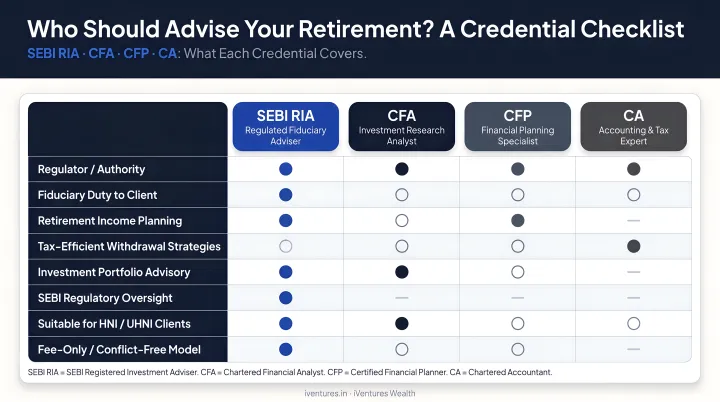

Types of Professionals Who Can Fill This Role

India has several professional categories relevant here:

- SEBI-registered Investment Advisers (RIAs) — the only professionals legally permitted to charge a fee for personalised investment advice under SEBI IA Regulations 2013

- Chartered Accountants (CAs) — deep India-specific tax law expertise, but cannot formally advise on investment products unless also RIA-registered

- Certified Financial Planners (CFPs) — trained in comprehensive financial planning including retirement income structuring

- CFA charterholders — rigorous investment and analytical training, often leading research and portfolio construction

The best advisors combine these roles or operate within a team that does. Only SEBI RIAs can legally provide fee-based investment advice — a CA can help with tax, but coordinating investment structure with tax outcomes requires an RIA. Treating these as separate functions creates gaps that tend to be expensive.

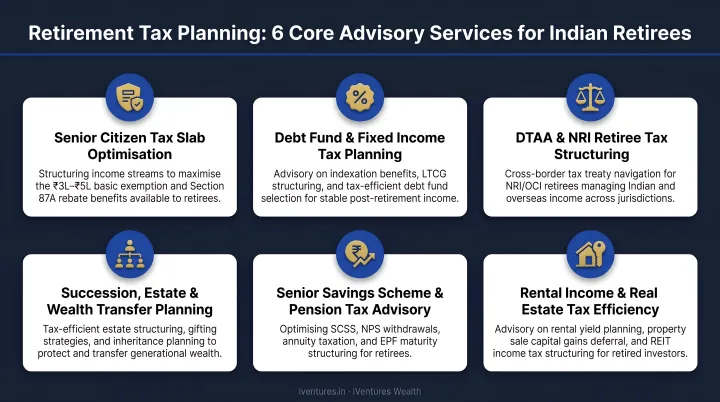

Core Services a Retirement Tax Planning Advisor Provides

- Tax-efficient withdrawal sequencing from EPF, NPS, and equity portfolios

- Shifting accumulated wealth toward tax-free instruments (ELSS, PPF, tax-free bonds) before retirement

- Senior citizen-specific exemption planning — Section 80TTB, old-regime slab optimisation, Section 87A rebate eligibility

- Capital gains management, including equity LTCG harvesting below the ₹1,25,000 annual threshold

- NPS allocation and annuity structuring decisions

- Estate and succession planning coordination for HNIs and family offices

The best advisors begin planning in Q1 and Q2, not February. Strategies unavailable at year-end — like changing NPS fund allocation, restructuring SWPs, or harvesting LTCG — require early action.

Why Retirement Tax Planning in India Is More Complex Than You Think

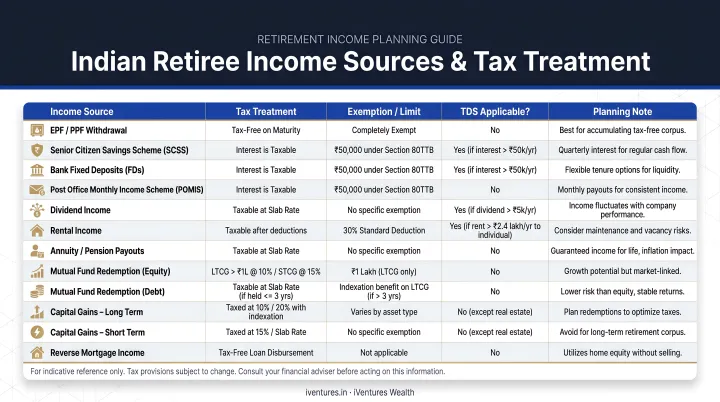

Retirees in India don't face one income stream — they face several, each taxed differently, each capable of pushing total income into a higher slab.

Consider a typical HNI retiree's income profile:

| Income Source | Tax Treatment |

|---|---|

| NPS annuity payouts | Fully taxable as income in year of receipt |

| EPF corpus (5+ years continuous service) | Exempt from income tax |

| EPF withdrawal (under 5 years) | Taxable; 10% TDS under Section 192A on ₹50,000+ |

| Listed equity LTCG above ₹1,25,000 | 12.5% from 23 July 2024 onwards |

| Dividend income | Taxable at applicable slab rate |

| Rental income | Added to total income, taxed at slab rate |

Without sequencing these carefully, a retiree with ₹80 lakh in dividend and rental income, plus NPS annuity, can breach senior citizen exemption thresholds and face a materially higher tax bill. Without sequencing these carefully, a retiree with ₹80 lakh in dividend and rental income plus NPS annuity can breach senior citizen exemption thresholds — and NPS is where the gap between accumulation advice and income-structuring advice becomes most costly.

NPS: The Annuity Tax Cliff

This is where many retirees are caught off guard. The 60% lump sum withdrawal on NPS exit is tax-free under Section 10(12A). But the 40% minimum annuity corpus generates fully taxable income every year thereafter. An advisor who only helps you accumulate in NPS — without planning the annuity-selection and income-timing strategy — leaves you exposed to a recurring tax drag that compounds across your entire retirement horizon.

The NRI and OCI Layer

Retirees with NRI or OCI status face additional complexity: DTAA documentation requirements (Tax Residency Certificate, Form 10F), TDS on India-sourced income under Section 195, and remittance planning under FEMA. Under the India-UAE DTAA, private pension income is generally taxable only in the country of residence — but claiming this relief requires proper documentation before withholding occurs. An advisor without cross-border tax experience will typically miss this window, leaving clients to claim refunds after the fact — if at all.

According to the PGIM India Retirement Readiness Survey 2025, only 37% of Indians had a retirement plan in 2025, down from 67% in 2023. That decline points to a specific failure: most financial advisors focus on corpus accumulation, not on how that corpus gets drawn down and taxed — and the difference directly affects how much income a retiree actually keeps.

Key Factors to Consider When Choosing a Retirement Tax Planning Advisor

Your net worth, income sources, family structure, retirement timeline, and NRI exposure all shape what you need from an advisor. No two profiles are identical — and neither is the right fit. These six factors help you evaluate candidates with precision.

Credentials and Regulatory Compliance

Start here. Before assessing anything else, verify that the advisor holds SEBI RIA registration — check the SEBI registered adviser list directly. This is the only licence permitting fee-based personalised investment advice in India.

Beyond registration, look for:

- CFA charterholder — signals rigorous investment training and analytical depth

- CFP designation — comprehensive financial planning including retirement income

- CA on the team — India-specific tax law expertise for EPF, NPS, and capital gains structuring

An advisor or firm combining these credentials offers the most complete coverage. No single designation substitutes for SEBI RIA registration when investment advice is involved.

Specialisation in Retirement-Specific Tax Planning

General financial advisors and retirement tax specialists are not the same. Ask candidates directly:

- Have you structured NPS annuity options for clients approaching exit age?

- How do you approach EPF withdrawal timing for clients with varied service histories?

- What's your approach to tax-free instrument positioning in the 5 years before retirement?

- Can you walk me through a real (anonymised) case where you reduced a client's projected lifetime tax outgo?

Vague answers — or answers that default to product recommendations — are a red flag. Advisors with genuine expertise can explain their process with specifics.

Fiduciary Standard vs. Commission-Based Advice

SEBI RIAs are legally prohibited from receiving commissions from product manufacturers. In retirement planning, this distinction is critical — the temptation to recommend high-commission annuity products or ULIPs over more tax-efficient alternatives is built into how commission-based advisors are paid.

Ask any candidate two direct questions:

- "Are you a SEBI-registered Investment Adviser?"

- "How are you compensated — and do you receive any third-party commissions, referral fees, or product incentives?"

A fiduciary RIA answers the second question with a clear no. A mutual fund distributor or insurance agent can offer retirement guidance, but they're legally permitted to earn commissions — and their recommendations follow the money accordingly.

These compensation structures have downstream consequences that compound over decades of retirement. Retirement tax planning doesn't exist in isolation, either.

Holistic and Long-Term Approach

An advisor managing only your NPS allocation while ignoring your rental income and equity portfolio will miss cross-stream interactions that create the biggest tax exposures.

Evaluate whether the candidate asks about:

- Family structure and succession goals

- All income sources, not just investable portfolio size

- Insurance adequacy and healthcare buffer planning

- Estate and inheritance considerations for HNI families

Planning cadence matters too. A good advisor is discussing next financial year's strategy by July. If they only reach out in February, their focus is filing — not planning.

Track Record and Client References

Look specifically for advisors who have managed retirement transitions for clients with profiles similar to yours — HNIs, NRIs, business founders unwinding equity positions, or public sector employees with pension income.

- Ask for the proportion of their client base that is in or approaching retirement

- Request anonymised case examples with measurable outcomes

- Verify their SEBI registration number independently

- Check for third-party accreditations — Dun & Bradstreet registration is one objective marker

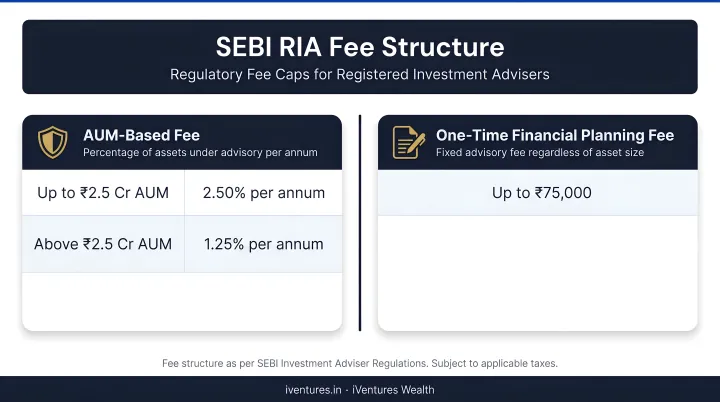

Fee Transparency and Structure

Common fee structures for SEBI RIAs in India:

- AUM-based fees run up to 2.5% of assets under advice per annum under the SEBI framework

- Fixed annual fees are capped at ₹1,51,000 per annum for new clients per the SEBI Master Circular dated January 8, 2025

- One-time planning fees apply to standalone retirement plans, often with an optional annual review retainer

Fee opacity is a major red flag. Any credible advisor provides a written fee agreement before onboarding that clearly states compensation structure and confirms no third-party product incentives. If this isn't offered upfront, don't proceed.

How iVentures Wealth Can Help

iVentures Wealth is a SEBI-registered Investment Adviser (RIA No. INA000019026) based in Gurugram, operating since 2005 with ₹1,146+ Cr in assets under advice across 150+ affluent families, HNIs, UHNIs, CXOs, and NRIs. The firm operates on a fee-only, fiduciary-first model — no commissions, no product conflicts.

For retirement-phase clients, the firm builds systematic withdrawal frameworks, structures income portfolios alongside pension income, and implements tax-efficient SWPs for post-career cash flow. The NRI and OCI advisory practice covers DTAA structuring, TDS planning on India-sourced income, and FEMA compliance.

Cross-jurisdiction tax coordination extends across the US, UK, UAE, Singapore, Canada, and Australia — with each engagement structured to the client's specific residency and income profile.

Advisory Team

Krishna Makhariya (CFA charterholder, Head of Research) leads investment research and portfolio construction. CA Shailender Bajaj provides chartered accountancy and compliance advisory support. Together, the team covers the investment, tax, and regulatory dimensions that retirement planning requires.

Key differentiators for retirement tax planning clients:

- SEBI RIA with true fiduciary mandate — zero commissions from any product manufacturer

- CFA-led research integrated into portfolio construction, not bolted on as a feature

- NRI and OCI tax advisory spanning DTAA, TDS, FEMA, FATCA/CRS, and GIFT City structuring

- Quarterly portfolio reviews with continuous monitoring between sessions

- Wealth Monitor App for consolidated multi-account views and tax statements

- Tax optimisation embedded in portfolio construction — not addressed separately at year-end

- Written fee agreement provided before any advisory engagement begins

Minimum investable assets: ₹5 Cr for NRIs/OCIs, ₹10 Cr for CXOs and professionals, ₹50 Cr for corporates, ₹100 Cr for family businesses and family offices.

Conclusion

The right retirement tax planning advisor brings SEBI registration, fiduciary accountability, proven India-specific expertise, and a fee structure with no conflicts of interest. These criteria matter far more than brand recognition or firm size.

Start this partnership 5–7 years before your target retirement date. NPS allocation decisions, EPF withdrawal timing, tax-free instrument positioning, and capital gains sequencing are all moves that must happen before retirement, not after. Once withdrawals begin, many of these options close permanently.

Tax laws change, income sources shift, and personal circumstances evolve. Build in annual reviews with your advisor — not as a formality, but as the mechanism that catches what static plans miss and keeps your lifetime tax liability on the right trajectory.

Frequently Asked Questions

What is the cost of a tax advisor in India?

SEBI RIAs may charge either an AUM-based fee (up to 2.5% of assets under advice per SEBI regulations) or a fixed annual fee capped at ₹1,51,000 per annum for new clients as per the SEBI Master Circular dated January 8, 2025. Lower cost doesn't mean better value — an advisor who lacks retirement-specific expertise can cost far more through missed planning opportunities.

Who is the best person to talk to about retirement planning?

The ideal profile is a SEBI-registered Investment Adviser with retirement income structuring expertise, ideally supported by a CA or tax specialist on the team. A single firm offering integrated investment and tax advice avoids the coordination gaps that separate professionals create.

Is it worth getting a financial advisor for retirement?

For HNI and UHNI investors with multiple income streams — NPS, EPF, equity portfolios, rental income — yes. Proactive strategies like LTCG harvesting, withdrawal sequencing, and pre-retirement instrument positioning can materially reduce lifetime tax liability. The first year of engagement alone typically recovers the advisory fee.

What credentials should a retirement tax planning advisor in India have?

SEBI RIA registration is non-negotiable — verify it independently on the SEBI website. Beyond that, look for a CFA charterholder (investment depth), CFP designation (retirement planning competency), and a CA on the team for tax expertise. Each credential addresses a different gap; none replaces the others.

When should I start working with a retirement tax planning advisor?

Start 5–7 years before your target retirement date. EPFO allows withdrawal of up to 90% of PF balance one year before retirement (for members aged 54+), but whether that withdrawal is taxable depends on decisions made well before that window opens.

What is the difference between tax planning and tax filing for retirement?

Tax filing is a compliance activity — you report what happened and pay what's due. Tax planning is a proactive, year-round strategy to legally reduce what will be due in the future, through investment structure, withdrawal sequencing, and income timing decisions. For retirees, planning delivers far more value than accurate filing ever can.