The earlier rules caused real damage. HDFC Bank recorded a specific provision of ₹1,034.49 crore against AIF investments in FY2023-24 alone, against nil the previous year. The problem wasn't the intent — preventing loan evergreening was legitimate — it was the bluntness of the tool.

The 2025 Directions take a different approach: calibrated concentration limits, targeted provisioning triggers, and governance requirements that create guardrails without shutting the door entirely. For HNI and UHNI investors who co-invest alongside banks and NBFCs in AIF schemes, this shift has concrete portfolio implications.

Key Takeaways

- No single RE can hold more than 10% of any AIF scheme's corpus; all REs combined are capped at 20%

- The blanket ban on REs investing in AIFs with debtor-company exposure is replaced by a 5% provisioning threshold

- Equity instruments — CCPSs and CCDs included, not just equity shares — do not trigger provisioning requirements

- All REs must maintain a board-approved investment policy governing AIF investments

- Existing fully-drawn commitments remain under the old rules; the new Directions apply to fresh commitments made after January 1, 2026

What Are AIFs and Why Does RBI Regulate Them?

An Alternative Investment Fund (AIF) is a privately pooled investment vehicle registered under SEBI. It collects capital from sophisticated investors — typically with a minimum ticket of ₹1 crore — to deploy into assets like private equity, venture capital, real estate, or private credit.

SEBI's AIF Regulations classify AIFs into three categories:

| Category | What It Includes | Primary Relevance |

|---|---|---|

| Category I | Venture capital, SME, infrastructure, angel, social venture funds | Early-stage exposure; longer lock-ins |

| Category II | Private equity, debt funds, real estate, distressed assets | Core allocation for HNI/UHNI portfolios; 74% of total commitments |

| Category III | Hedge funds, long-short equity, complex trading strategies | Absolute return strategies |

As of December 31, 2025, total AIF commitments stood at ₹15,74,050 crore, with Category II alone accounting for ₹11,64,118 crore — the segment most directly affected by RBI's rules.

That scale is precisely what draws RBI into the picture. SEBI regulates the AIF products themselves; RBI regulates the banks and NBFCs that invest in them. When bank and NBFC capital flows into AIFs without guardrails, it can create channels for concealing loan stress — which is exactly what the 2023 circular was designed to prevent.

The Problem: Loan Evergreening Through AIFs

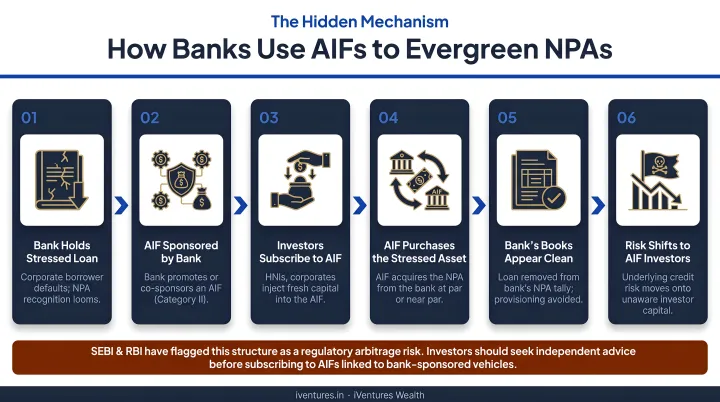

Evergreening, in plain terms, is when a lender uses fresh money to help a struggling borrower repay an existing loan — making the loan appear healthy rather than non-performing. The AIF structure made this possible in a less visible way.

How the Mechanism Worked

The typical structure looked like this:

- RE (bank or NBFC) lends ₹100 crore to Company X

- Company X's repayment capacity deteriorates — the loan looks stressed

- RE invests in an AIF scheme

- The AIF invests in or lends to Company X

- Company X uses AIF proceeds to repay the RE's original loan

- RE's loan books look clean; the NPA classification is avoided

The AIF acted as a pass-through, converting a direct stressed-loan relationship into an indirect one that was harder to detect.

Why the 2023 Ban Created Problems

RBI's December 19, 2023 circular responded forcefully: REs were prohibited from investing in any AIF with downstream exposure to their debtor companies, and had 30 days to exit or face 100% provisioning on the entire investment.

The problem was collateral damage. Many REs held legitimate, uncorrelated AIF positions with no link to any stressed borrower. But the circular applied uniformly, creating three immediate consequences:

- No realistic exit route, given how thin the secondary market for AIF units is

- 100% provisioning requirements that hit bank P&Ls hard in Q3 FY2024

- Legitimate AIF strategies disrupted alongside the genuinely problematic ones

The March 2024 clarification softened some of this — limiting provisioning to the proportionate debtor-linked share and excluding equity shares from triggers. But the underlying framework remained a blunt instrument.

The 2025 Directions address this directly, replacing the across-the-board restriction with look-through norms, proportionate provisioning triggers, and category-specific carve-outs.

Key Provisions of the RBI (Investment in AIF) Directions, 2025

Investment Concentration Caps

Two new caps apply to all RE investments in AIFs — not just those with debtor-company exposure:

- Single-RE cap: No RE may contribute more than 10% of any AIF scheme's corpus

- Aggregate-RE cap: All REs combined cannot exceed 20% of any single AIF scheme's corpus

An RE with a concentrated AIF stake — even one with zero debtor overlap — must still comply.

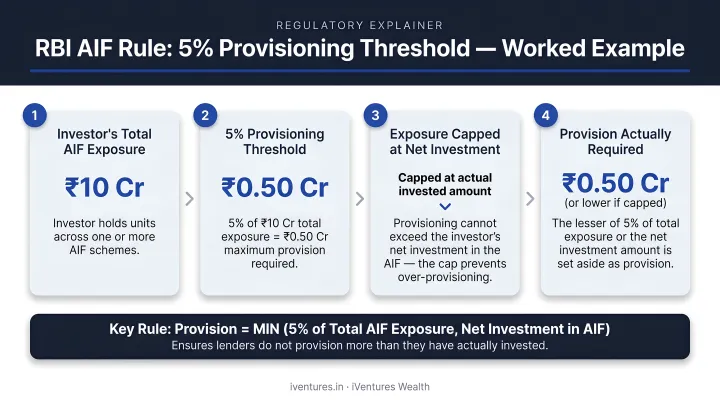

The 5% Provisioning Trigger

This is the framework's most precise mechanism. The threshold is binary:

- Below 5% RE stake: No provisioning required, even if the AIF holds downstream non-equity exposure to the RE's debtor company

- Above 5% RE stake: 100% provision required — but only on the RE's proportionate share of the AIF's investment in the debtor company, capped at the RE's direct loan exposure

A simplified example:

- RE has a ₹10 crore direct loan to Company X

- AIF invests ₹200 crore in Company X (non-equity instruments)

- AIF's total corpus is ₹800 crore

- RE holds 7.5% of the AIF corpus = ₹60 crore investment

- RE's proportionate share of AIF's Company X exposure = 7.5% × ₹200 crore = ₹15 crore

- Provision required = ₹15 crore, but capped at ₹10 crore (the direct loan exposure)

Provisioning on the proportionate share — not the full AIF investment — significantly reduces the compliance burden for REs with small stakes in large funds.

What Counts as "Equity Instruments"

The 2025 Directions expand the definition of equity instruments excluded from provisioning triggers. Under the March 2024 clarification, only equity shares were excluded. The new framework now covers:

- Equity shares

- Compulsorily Convertible Preference Shares (CCPS)

- Compulsorily Convertible Debentures (CCD)

This matters because many private credit and structured deals use CCPS and CCDs rather than plain equity. Excluding these from provisioning obligations significantly reduces friction for legitimate hybrid-instrument investments.

Subordinated Units and Capital Deduction

If an RE invests in subordinated units of an AIF — common in priority distribution model structures where senior investors get paid first — the entire subordinated investment must be deducted from the RE's capital funds. The deduction is split proportionately between Tier 1 and Tier 2 capital, reflecting the junior, first-loss nature of these positions.

Mandatory Board-Approved Investment Policy

All REs must now maintain a board-approved investment policy specifically governing AIF investments. The policy must cover:

- Investment limits per scheme and in aggregate

- Debtor-exposure monitoring procedures

- Provisioning methodology

- Escalation procedures for threshold breaches

This governance requirement is new — the earlier circulars addressed provisioning mechanics but didn't mandate a formal policy framework.

From Blanket Ban to Calibrated Limits: What Changed?

The philosophical shift matters as much as the technical details.

The December 2023 circular treated all RE-AIF-debtor triangles as suspect. The 2025 Directions treat them as manageable — provided concentration limits and provisioning discipline are maintained. REs can now invest in AIFs that have downstream exposure to their debtor companies, which was outright prohibited before.

Transition Provisions for Existing Investments

The Directions create three distinct buckets:

| Investment Status | Governing Framework |

|---|---|

| Fully drawn commitments as of July 29, 2025 | Old circulars (Dec 2023 + March 2024) continue to apply |

| Commitments made pre-effective-date but not fully drawn | One-time choice: old circulars or new Directions |

| New commitments post-January 1, 2026 | New Directions apply exclusively |

One practical implication: the new 10%/20% caps apply universally, regardless of debtor overlap. Some REs with large concentrated AIF positions — even in schemes with no debtor-company exposure — may need to restructure holdings to comply by January 1, 2026.

SEBI's Parallel Requirements

The SEBI Circular of October 8, 2024 on specific due diligence for AIF investors and investments runs alongside the RBI framework. SEBI's circular requires AIFs, managers, and investment committees to conduct enhanced due diligence where an RE investor holds 25% or more, is linked to the sponsor/manager, or has control-type rights.

Both frameworks must be complied with simultaneously. For AIFs that rely on RE capital, this means a genuine dual-compliance obligation across two separate regulatory regimes.

What These New Directions Mean for HNI and UHNI AIF Investors

Most HNI and UHNI investors aren't REs — the rules don't apply to them directly. But the indirect effects are real.

Fundraising Dynamics Are Shifting

AIFs — particularly Category II debt-oriented and private credit funds — that historically used bank or NBFC capital as anchor commitments now face structural constraints. The 10%/20% caps limit how much RE capital can sit in any single scheme. For fund managers who relied on one or two large NBFC cornerstone investors, this changes the fundraising math entirely.

Many managers will actively court family offices, UHNIs, HNIs, and corporate treasuries to fill the gap. For sophisticated non-RE investors, this creates genuine opportunities to access funds that were previously over-subscribed on the RE side — often with better negotiating position on terms.

Enhanced Governance Benefits Everyone

The compliance obligations REs now face will raise the baseline of transparency across AIF reporting — benefiting all investors in the scheme, not just regulated ones. Specifically, fund managers will need to maintain cleaner records across:

- Board-approved investment policies and downstream allocation rationale

- Debtor-exposure monitoring against updated concentration limits

- Instrument classifications and provisioning calculations at a granular level

- Investor concentration disclosures across LP categories

For HNI and UHNI investors, this means better visibility into how fund capital is deployed — and clearer signals when a fund's LP base is shifting in ways that could affect corpus targets or deployment timelines.

Evaluating AIF Structures in the New Environment

With REs potentially restructuring positions to meet concentration caps, and the distinction between old-framework and new-framework investments creating temporary complexity, evaluating AIF structures requires more than return analysis. Understanding the fund's LP composition, the instrument types used for downstream investments, and whether any RE investors are above the 5% provisioning threshold all become relevant inputs.

iVentures Wealth works with HNI and UHNI clients to assess AIF structures in this evolving regulatory environment — evaluating fund composition, manager quality, and how developments like these Directions affect existing and prospective allocations. As a fee-only SEBI-registered RIA, the firm takes no AIF placement commissions, so recommendations reflect only the client's interest.

Frequently Asked Questions

What is the full form of AIF in RBI?

AIF stands for Alternative Investment Fund — these are privately pooled investment vehicles registered under SEBI, not RBI. RBI's involvement relates specifically to how banks and NBFCs (which it supervises) invest in these funds, not to regulating the AIF products themselves.

What is Cat 1, Cat 2, and Cat 3 AIF?

Category I covers venture capital, SME, and infrastructure funds. Category II — the most common for HNI portfolios — includes private equity, debt, real estate, and distressed-asset funds. Category III covers hedge funds and complex trading strategies, each governed by distinct SEBI rules on leverage and eligibility.

What are the AIF Regulations for 2026?

The key change effective January 1, 2026 is the RBI (Investment in AIF) Directions, 2025, replacing the earlier 2023–2024 circulars for RE investors. SEBI's October 2024 due diligence circular also remains applicable, creating a dual compliance framework for AIFs with RE investors.

What is the effective date of the new RBI AIF Directions, 2025?

The Directions come into force on January 1, 2026, though REs may adopt them earlier voluntarily. Fully drawn pre-existing commitments remain under old circulars; partially drawn commitments get a one-time transition election.

What is "evergreening" and why did RBI step in?

Evergreening is the practice of routing fresh funds through an AIF to help a stressed borrower repay an existing bank loan, masking NPAs. RBI stepped in to ensure banks and NBFCs cannot use AIF structures to conceal the true credit quality of their loan books.

Can an RE still invest in an AIF that lends to one of its borrowers?

Yes. The 2025 Directions permit this, reversing the 2023 ban. Where the RE's stake exceeds 5% of the AIF's corpus and the downstream exposure is in non-equity instruments, the RE must make 100% provision on its proportionate share, capped at its direct loan exposure to the debtor.