For Indian SMEs, the stakes are equally real. SIDBI's 2025 MSME sector report found that 41% of MSMEs cite lack of finance as a primary growth barrier, with delayed payments hitting 15% of trading-sector businesses hardest.

A structured financial plan doesn't eliminate these risks — but it gives you enough visibility to act before a cash crunch becomes a crisis.

This guide covers what a business financial plan actually is, its core components, a five-step process to build one, and the mistakes that consistently derail even experienced founders.

Key Takeaways

- A business financial plan covers revenue projections, cash flow, expense budgets, and risk contingencies — typically over 1–5 years

- Build your foundation on three core documents: a P&L statement, cash flow statement, and balance sheet

- Always model revenue forecasts across three scenarios — conservative, moderate, and optimistic

- Monthly reviews and quarterly deep-dives keep the plan relevant as conditions change

- Indian businesses must embed GST filing dates, advance tax deadlines, and TDS cycles directly into the plan

What Is a Business Financial Plan and Why Does It Matter?

A business financial plan is a structured document that outlines your company's financial goals, revenue and expense projections, cash flow expectations, and strategies for growth and risk mitigation — typically covering a 1–5 year horizon. Unlike a general business plan, which describes your strategy and market position, a financial plan quantifies those ambitions: how much money comes in, where it goes, and whether the business can sustain itself.

Why It Matters Beyond the Numbers

Business owners who formalize their financial planning gain several concrete advantages:

- Smarter resource allocation: knowing your cost structure prevents over-hiring or over-investing before cash flows support it

- Investor and lender credibility: banks and institutional investors require financial projections before committing funds; RBI guidelines specifically note that MSE working-capital limits up to ₹5 crore are computed based on projected annual turnover

- Early warning signals — a month-by-month cash flow projection reveals shortfalls 60–90 days before they hit your account

- Concrete performance benchmarks: without projected numbers, there's no basis for evaluating whether actual results are good, bad, or simply adequate

India-Specific Compliance Dimension

These strategic benefits don't exist in isolation. For Indian businesses, a financial plan also functions as a compliance tool — and missing key deadlines adds real costs. A well-built plan must account for:

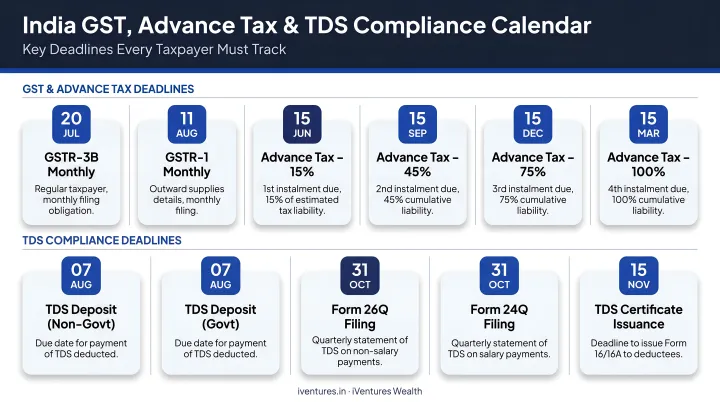

- GST filings: GSTR-1 due by the 11th of the following month for monthly filers; GSTR-3B due by the 20th

- Advance tax: Companies pay in four instalments — 15% by June 15, 45% by September 15, 75% by December 15, and 100% by March 15

- TDS deposits: Generally due by the 7th of the following month (April 30 for March deductions)

Missing these deadlines adds interest costs and compliance risk that a structured plan helps you anticipate and budget for.

Key Components of a Business Financial Plan

Income Statement (P&L)

The Profit & Loss statement shows revenues, cost of goods sold (COGS), operating expenses, and net profit or loss over a defined period — monthly, quarterly, or annually.

This document answers one core question: is the business making money? It directly informs pricing decisions (are margins adequate?), staffing calls (can the revenue base support the headcount?), and cost reduction priorities (which expense lines are disproportionate to output?).

Under Schedule III of India's Companies Act, 2013, the Statement of Profit and Loss must include Revenue from Operations, Other Income, Employee Benefits Expense, and Finance Costs — providing a standardised framework for comparison across periods.

Cash Flow Statement

Cash flow is where many profitable businesses hit an unexpected wall. A pattern well-documented across markets: startups and scale-ups frequently fail not because they're unprofitable, but because they run out of cash even when sales are strong.

The cash flow statement covers three activity types:

- Operating: Day-to-day cash from sales, payroll, rent, vendor payments

- Investing: Capital expenditure, asset purchases or sales

- Financing: Loans, equity infusions, dividend payments

The P&L can show a profit while the cash flow statement reveals you can't meet next month's payroll. Tracking both together gives you the full picture — one shows performance, the other shows survival.

Balance Sheet

The balance sheet is a snapshot of your business at a specific point in time: what you own (assets), what you owe (liabilities), and what remains for owners (equity). It answers a fundamental question — how much is the business actually worth, and how leveraged is it?

For growth-stage businesses, the balance sheet reveals whether expansion is fundable internally or requires external capital. For lenders, it's typically the first document they examine.

Revenue Projections and Expense Budgets

Two common forecasting approaches:

- Bottom-up: Unit sales × price per unit — grounded in actual sales capacity

- Top-down: Estimate your share of the total addressable market — useful for early-stage planning but less precise

Best practice is to build projections under three scenarios — conservative, moderate, and optimistic — and categorise expenses into:

| Category | Examples |

|---|---|

| Fixed costs | Rent, salaries, insurance premiums |

| Variable costs | Raw materials, commissions, packaging |

| One-time costs | Equipment purchases, office fit-outs |

| Often-overlooked | GST liability, professional fees, compliance costs |

Break-Even Analysis

The break-even formula:

Fixed Costs ÷ (Price per Unit – Variable Cost per Unit)

This tells you the minimum revenue needed to cover all costs before generating profit. It's especially useful when:

- Launching a new product line

- Entering a new geography

- Setting sales targets for the team

If your break-even point can't be reached at achievable volumes, revise the financial model before committing capital.

How to Create a Business Financial Plan: A Step-by-Step Guide

The components above describe what the plan contains. The steps below describe how to build it. One caveat worth stating upfront: a rough plan acted upon beats a perfect plan that exists only in a spreadsheet.

Step 1: Define Clear Financial Goals

Goals must follow the SMART framework — Specific, Measurable, Achievable, Relevant, Time-bound — and connect directly to broader business strategy.

Examples relevant to Indian SMEs and founders:

- Increase revenue by 20% within 12 months by expanding into two new cities

- Reduce overhead costs by 15% in Q3 by renegotiating vendor contracts

- Build a 6-month operating cash reserve by December 31

Vague goals like "grow faster" or "cut costs" provide no basis for tracking progress or making decisions.

Step 2: Forecast Revenue and Plan Your Expenses

Use historical financial data, industry benchmarks, and direct market research to estimate revenue. Avoid anchoring on best-case numbers. Founders who build plans around optimistic projections consistently underperform those who plan conservatively — the gap almost always traces back to flawed revenue assumptions, not execution.

Build separate line items for:

- Fixed costs: rent, salaries, SaaS subscriptions

- Variable costs: raw materials, delivery charges, sales commissions

- India-specific costs: GST liability, TDS obligations, CA/legal fees, advance tax instalments

Don't build the plan without accounting for compliance costs — they're not optional, and they're often underestimated.

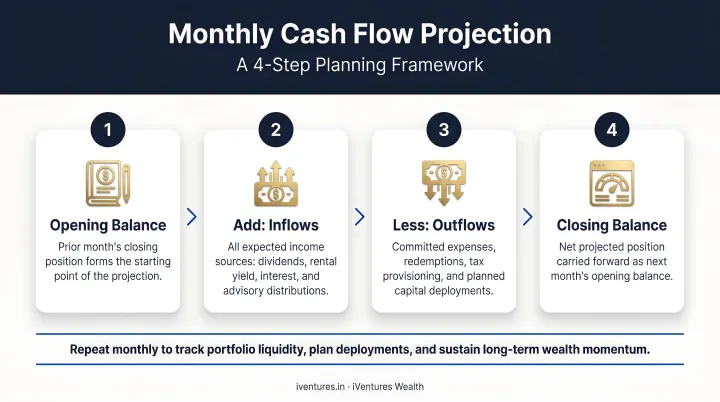

Step 3: Build Month-by-Month Cash Flow Projections

A 12-month cash flow projection requires four inputs per month:

- Opening cash balance — what's in the account at month start

- Expected inflows — sales receipts, loan disbursements, investor capital

- Expected outflows — all fixed and variable costs, tax payments, debt service

- Closing cash balance — opening + inflows – outflows

Flag every month where the closing balance drops below a safe threshold (typically 1–2 months of operating expenses). That's your early warning signal — time to arrange a credit line, accelerate collections, or defer discretionary spend.

Step 4: Identify Risks and Build Contingency Plans

Risk planning covers two categories:

- Internal risks: Key employee departure, operational breakdowns, technology failures

- External risks: Market downturns, regulatory changes, supply chain disruptions, client concentration

Most advisors recommend maintaining at least 3–6 months of operating expenses as a contingency buffer. Beyond the buffer, stress-test your projections against worst-case scenarios — if revenue drops 30%, which costs must be cut first? Having these answers documented in advance means faster, calmer decision-making when pressure actually arrives.

Step 5: Monitor, Review, and Update Regularly

A financial plan isn't a document you file and forget. Suggested review cadence:

- Monthly: Compare actual vs. projected revenue and expenses; identify variances early

- Quarterly: Deep-dive into cash flow, gross margin trends, and expense categories

- Annually: Full revision of the plan incorporating market changes, business growth, and updated compliance obligations

Markets shift. Costs change. Regulatory requirements evolve. A plan that isn't updated regularly provides a false sense of control rather than genuine visibility.

Common Mistakes Business Owners Make in Financial Planning

Overestimating Revenue and Underestimating Costs

Founders consistently overestimate revenue. When best-case projections become the baseline, hiring decisions, lease commitments, and inventory purchases all get sized against numbers the business never actually achieves.

The fix: anchor every projection to historical data. If last year's revenue grew 12%, building a plan around 40% growth requires a specific, documented set of assumptions.

Mixing Personal and Business Finances

Blending personal and business accounts creates three compounding problems:

- Inaccurate financial statements that don't reflect true business performance

- Complicated tax filing, especially for GST and income tax reporting

- Inability to assess actual business profitability separate from the owner's personal draw

Under India's Companies Act, Section 128, every company must maintain books of account that give a true and fair view of its state of affairs. Commingled finances make this structurally impossible. Separate accounts, separate cards and credit lines, from day one.

Treating the Financial Plan as a One-Time Exercise

A plan created once — even a very good one — becomes wrong the moment market conditions shift. Businesses that revisit their financial plan only at year-end are typically reacting to problems that a monthly review would have surfaced months earlier.

The review cadence isn't optional. It's what separates a plan that works from one that sits in a drawer.

When to Work with a Financial Advisor for Your Business

At a certain point, managing business finances internally hits its limits. Clear signals that professional advisory adds value:

- Rapid growth that outpaces internal financial management capacity

- Preparing for a funding round or institutional investment

- Surplus cash sitting idle across multiple accounts with no deployment strategy

- Complex tax structures or entities across multiple jurisdictions

- Major decisions involving business succession or ownership transitions

A qualified financial advisor brings more than compliance support. For business owners who have accumulated surplus capital, the next challenge is deploying it efficiently — across debt funds, fixed income instruments, liquid funds, and other regulated products — without sacrificing the liquidity needed for operations.

The distinction between product-driven sales and fiduciary-grade advisory is material here. A SEBI-registered investment adviser advises on the full universe of regulated products without commission incentives — no bias toward specific instruments, no hidden agenda.

iVentures Wealth (SEBI Registration No. INA000019026) is a Gurugram-based investment advisory firm with 20+ years of experience serving founders, CEOs, CXOs, SMEs, and corporates across India. As a product-neutral treasury advisor, the firm helps businesses consolidate idle balances, deploy surplus capital into appropriate instruments — liquid funds, overnight funds, bonds, ultra-short-term debt funds — and maintain the liquidity needed for day-to-day operations. Their CFA-led research team and fee-only advisory model are well suited for business owners who need credible, conflict-free guidance on capital allocation.

Frequently Asked Questions

What is business financial planning?

Business financial planning is the process of setting financial goals, projecting revenues and expenses, managing cash flow, and creating a roadmap for sustainable business growth. It differs from accounting or bookkeeping — those record what happened; financial planning determines where the business is headed and how to get there.

What are the 5 steps in business financial planning?

The five core steps are:

- Define SMART financial goals

- Forecast revenue and plan expenses

- Build month-by-month cash flow projections

- Identify risks and establish contingency buffers

- Monitor actual vs. projected performance monthly and quarterly

What are the 7 components of a business plan?

A business plan typically includes an executive summary, company description, market analysis, organisational structure, product or service overview, marketing and sales strategy, and financial projections. The financial projections section is what lenders and investors scrutinise most closely — it determines whether your business model is viable on paper before it is tested in the market.

What financial documents are essential for a business financial plan?

The three core financial statements are the income statement (P&L), cash flow statement, and balance sheet. Supporting documents include revenue forecasts, expense budgets categorised by fixed, variable, and one-time costs, and a break-even analysis.

How often should a business financial plan be updated?

Monthly performance check-ins, quarterly reviews of core financials, and a comprehensive annual revision are the recommended minimum. Revisit the plan whenever a major business change occurs: expansion, new product launches, significant market shifts, or key regulatory changes.