The distinction matters more than most people realise. Choose the wrong professional and you may receive advice too generic for your financial complexity, or pay for services you don't yet need. According to Knight Frank's 2025 Wealth Report, India had 85,698 individuals with a net worth of USD 10 million or more, ranking fourth globally — and that population is growing fast. As wealth compounds and financial lives grow more complex, the right advisory relationship becomes a genuine competitive advantage.

This article breaks down exactly what separates a financial advisor from a wealth manager — covering services, credentials, fee structures, fiduciary obligations, and the practical question of which one your situation actually calls for.

Key Takeaways

- Financial advisors handle goal-specific planning for a broad client base; wealth managers offer comprehensive, integrated advisory for HNIs and UHNIs

- Scope, clientele, and fee structure differ significantly between the two roles

- SEBI RIA registration imposes a fiduciary duty that not all financial professionals carry

- Credentials are more reliable indicators of trustworthiness than job titles

- Your choice should hinge on financial complexity, not just net worth

Quick Comparison

| Dimension | Financial Advisor | Wealth Manager |

|---|---|---|

| Primary clientele | Broad — early-career to pre-retirees | HNIs and UHNIs with complex needs |

| Scope of services | Goal-specific (retirement, insurance, SIPs) | Integrated — investments, tax, estate, succession |

| Fee structure | Commission, flat fee, or lower AUM % | AUM-based, retainer, or hybrid |

| Typical asset threshold | ₹50 lakh – ₹2 crore investable | ₹2 crore+ investable (varies by firm) |

| Fiduciary standard | Not guaranteed unless SEBI RIA registered | SEBI RIA registration carries full fiduciary duty |

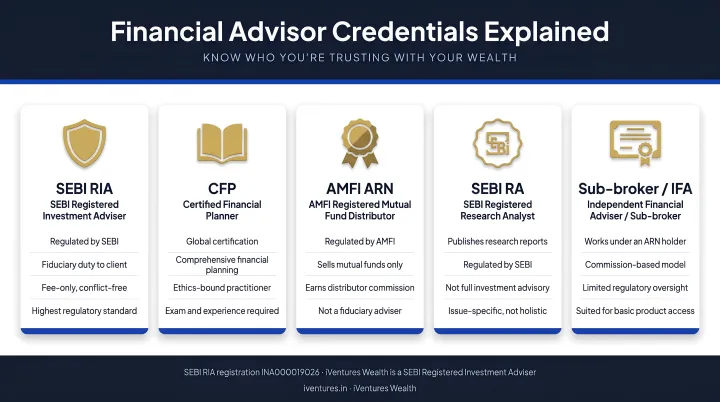

Note on Indian regulatory context: The SEBI-registered Investment Adviser (RIA) framework is the most important regulatory filter when evaluating any financial professional in India. SEBI RIA registration — not job title — determines whether an advisor is legally bound to act in your interest.

What Is a Financial Advisor?

A financial advisor is a professional who helps clients manage their finances — from budgeting and retirement planning to insurance guidance and basic investment management.

In India, the term covers several distinct types of professionals:

- SEBI-registered Investment Advisers (RIAs) — legally bound fiduciaries who earn fees from clients only, not commissions from product manufacturers

- AMFI-registered Mutual Fund Distributors (ARN holders) — earn commissions from fund houses; not fiduciaries

- Independent Financial Advisors (IFAs) — no separate SEBI category; legal status depends on their activity (RIA if charging for advice, MFD if distributing funds)

Core Services

Financial advisors typically cover:

- Building a structured financial plan aligned to life goals

- Recommending investment products — mutual funds, FDs, PPF, NPS

- Retirement and education corpus planning

- Term insurance and health coverage guidance

- Tax-saving investment strategies under Sections 80C, 80D, and related provisions

These services target clients in the wealth accumulation phase: salaried professionals, early-stage entrepreneurs, and others building financial foundations for the first time. Understanding what qualifies someone to offer this guidance matters just as much as what they offer.

Credentials to Look For

| Credential | What it signals |

|---|---|

| SEBI RIA registration | Fiduciary duty; fee-only; cannot earn commissions |

| CFP® certification | Completed structured financial planning curriculum via FPSB India |

| AMFI ARN number | Authorised to distribute mutual funds; not a fiduciary |

| NISM Series certifications | Required for SEBI RIA qualification |

CFP certification and SEBI RIA registration are separate requirements. A CFP® professional is not automatically a registered RIA — the two frameworks have different qualification, experience, and net-worth criteria. SEBI currently lists 1,039 registered Investment Advisers in its intermediary registry — a notably small number for a country of India's size.

Who Should Work with a Financial Advisor?

A financial advisor is the right fit if you are in the wealth-building phase with investable assets below ₹1–2 crore and need structured guidance on specific goals.

Typical scenarios:

- A salaried professional in their 30s building a first SIP portfolio and term insurance plan

- A doctor diversifying beyond fixed deposits into mutual funds and NPS

- An entrepreneur structuring investments tax-efficiently under the new tax regime

What Is a Wealth Manager?

A wealth manager is a specialised financial professional who provides comprehensive, integrated financial services to high-net-worth and ultra-high-net-worth individuals. Wealth management is not just investment management — it is the coordination of a client's entire financial life.

Where a financial advisor might recommend specific products, a wealth manager coordinates the relationships between those products: the tax consequences, the legal structures, the insurance coverage, and the succession plan. Everything moves together, not in isolation.

Services That Go Beyond Standard Advisory

In the Indian context, wealth managers typically offer:

- PMS (Portfolio Management Services) — SEBI minimum investment of ₹50 lakh; client holds assets directly

- AIF access (Categories I, II, III) — minimum ₹1 crore per investor; covers private equity, hedge-fund-like strategies, and venture capital

- Estate planning and succession advisory — wills, private family trusts, lifetime gifting, wealth transfer tax planning

- NRI/OCI investment planning — DTAA structuring, GIFT City solutions, cross-border inheritance coordination

- Business succession advisory — for promoters and founders approaching a liquidity event

- Family office services — governance, family charter drafting, consolidated multi-custodian reporting, next-generation preparation

- Philanthropic structuring — charitable trusts and CSR planning

Wealth managers typically carry advanced credentials — CFA® charterholders, professionals with family office advisory experience — and operate as SEBI-registered RIAs with a legal fiduciary mandate. That level of qualification matters precisely because the clients they serve are operating at a different scale of complexity.

According to EY's Indian Family Office Playbook, Indian family offices grew from 45 in 2018 to around 300 in 2024, reflecting demand from more than 13,000 families with wealth above USD 30 million. This is the segment wealth managers are structured to serve.

Who Should Work with a Wealth Manager?

A wealth manager is the right fit when your financial life has moved beyond individual products into overlapping structures that require active coordination.

Relevant profiles:

- A CXO managing stock options, ESOPs, and personal wealth simultaneously, needing ESOP vesting strategy and post-vesting diversification

- A founder post-exit with ₹100 crore+ across multiple banks, needing a clear deployment framework and estate structure

- An NRI with real estate, demat accounts, NRE/NRO holdings, and retirement assets across India and abroad — facing compliance risk in multiple jurisdictions

- A family managing wealth across nine separate broker and bank relationships with no unified view of performance, risk, or succession plan

Financial Advisor vs Wealth Manager: Key Differences Explained

Clientele and Complexity

Financial advisors serve clients across all wealth levels, often with transactional or product-focused advice. Wealth managers work exclusively with HNIs and UHNIs where financial complexity demands a coordinated, ongoing strategy — not one-time recommendations.

The distinction is not just size. It is the number of moving parts: business interests, foreign assets, multiple income streams, and succession considerations that interact with each other in ways a single product recommendation cannot address.

Scope of Services

A financial advisor typically advises on one or a few financial goals. A wealth manager integrates investments, tax planning, estate structuring, insurance, and business advisory into a single evolving strategy.

iVentures Wealth — a SEBI-registered RIA (INA000019026) operating since 2005 — illustrates what this looks like in practice:

- Coordinates directly with clients' CAs and legal counsel

- Prepares standardised gain and income reports for ITR filing

- Conducts quarterly portfolio reviews alongside ad-hoc rebalancing across market cycles

That kind of embedded coordination is structurally different from an annual product review.

Fee Structure

| Professional | How they are typically paid |

|---|---|

| MFD/ARN holder | Commissions from fund houses; trail income on AUM |

| SEBI RIA (financial advisor) | Client-only fees — flat fee capped at ₹1,25,000/year per client, or AUM mode capped at 2.5% per annum under SEBI IA Guidelines |

| Wealth manager (SEBI RIA) | AUM-based fees on larger portfolios, sometimes combined with retainers or performance components |

The critical point: SEBI Regulation 15A prohibits RIAs from receiving any consideration from anyone other than the client being advised. This is what makes the fee-only model structurally conflict-free — not a marketing claim, a legal requirement.

Commission-earning MFDs, bank wealth managers, and insurance agents have their recommendations shaped by trail revenue. A SEBI RIA cannot.

Fiduciary Standard

Not all financial professionals in India operate as fiduciaries. SEBI RIA registration under Regulation 15(1) imposes a fiduciary duty: the adviser must act solely in the client's interest, disclose all conflicts, and earn remuneration only from the client.

A mutual fund distributor, even a well-intentioned one, has a different regulatory status — they must disclose commissions, but are not prohibited from earning them.

Relationship Model

A financial advisor relationship is often periodic — an annual review, a specific query, a product recommendation triggered by a life event.

A wealth manager operates as an ongoing embedded partner: proactively monitoring risk, rebalancing strategy, coordinating across the client's CA, legal counsel, and family, and managing both scheduled and ad-hoc reviews across market cycles. Over time, this continuity compounds — catching risks early, acting on opportunities others miss, and building a strategy that evolves as the client's life does.

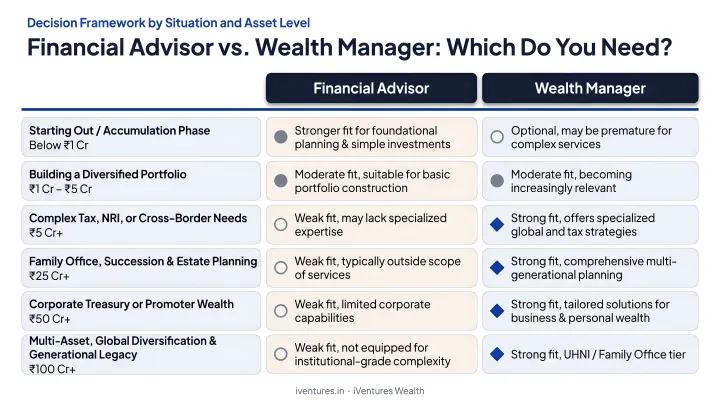

Which One Should You Choose?

Decision Framework

Choose a financial advisor if:

- Your investable assets are below ₹2 crore

- You need guidance on specific goals — first SIP portfolio, term insurance, retirement corpus, child education planning

- Your financial situation does not yet involve multiple income streams, business interests, or cross-border assets

Choose a wealth manager if:

- Your investable assets exceed ₹2 crore (and particularly above ₹5 crore)

- Your financial life involves ESOPs, business exits, foreign assets, or succession considerations

- You need someone to coordinate your entire financial picture — not just recommend products

Situational Recommendations

| Situation | Right choice |

|---|---|

| First SIP portfolio, term insurance, home purchase planning | Financial advisor |

| ESOP vesting strategy and post-exercise diversification | Wealth manager |

| NRI with assets across India and abroad | Wealth manager with cross-border expertise |

| Managing post-liquidity event wealth (business sale or IPO) | Wealth manager |

| Estate structuring, family trust, succession planning | Wealth manager |

| Early-career retirement planning | Financial advisor |

The Transition Point

Many HNIs graduate from financial advisors to wealth managers as their wealth compounds and complexity grows. The right time to make that transition is before a major financial event — a business exit, an inheritance, retirement — not after.

Consider a client in their 40s who started with mutual fund SIPs and term insurance. Their portfolio has grown to ₹5 crore+, a business exit is on the horizon, their children are NRIs, and there is no estate plan in place.

At that point, a SEBI-registered wealth management firm offering fiduciary services, PMS and AIF access, estate coordination, and cross-border planning becomes the right fit — because the complexity of the situation has outgrown what a generalist advisor is structured to handle.

If you are unsure which type of advisor your current financial situation calls for, connect with iVentures Wealth for a complimentary consultation.

Conclusion

A financial advisor is the right starting point for most individuals building wealth. A wealth manager becomes necessary when financial complexity outpaces what general advice can manage. The distinction lies in the depth of service required — not prestige, not branding.

Choosing the right professional has direct financial consequences:

- Fewer tax leakages through proactive structuring

- Better estate coordination across family members and entities

- More informed decisions across asset classes

- A financial strategy that holds up across market cycles and life transitions

The right question isn't "which title sounds more impressive?" It's "how complex is my financial life right now — and where is it headed?" Start there.

Frequently Asked Questions

Do I need a financial advisor or a wealth manager?

The choice depends on your financial complexity. Financial advisors suit those in the wealth-building phase with simpler, goal-specific needs. Wealth managers are better suited for HNIs and UHNIs managing multiple income streams, cross-border assets, business interests, or succession requirements.

What is the minimum net worth needed to work with a wealth manager in India?

Most wealth management firms in India require a minimum of ₹1–2 crore in investable assets, excluding the primary residence. Some firms set higher thresholds — iVentures Wealth, for instance, requires ₹5 crore+ for NRI/OCI clients and ₹10 crore+ for CXOs and professionals — reflecting the complexity of services provided.

How do wealth managers charge fees compared to financial advisors?

SEBI-registered RIAs cannot earn commissions and charge clients directly — as AUM-based fees (capped at 2.5% per annum) or flat fees (capped at ₹1,25,000 per annum per client) — while mutual fund distributors earn commissions from fund houses. Wealth managers operating as SEBI RIAs use AUM-based or hybrid retainer structures, with full fee transparency required upfront.

What credentials should I look for in a wealth manager in India?

Prioritise SEBI RIA registration (the legal fiduciary standard, verifiable on the SEBI public registry), CFA® charterholder status (signals investment research depth), and CFP® certification (indicates comprehensive planning knowledge). Firm-level CDSL or NSE membership covers execution infrastructure. Credentials are more reliable indicators of expertise than job titles.

Can a financial advisor also provide wealth management services?

Some financial advisors with advanced credentials and infrastructure do offer wealth management services. The key is assessing whether they operate as SEBI RIAs (fiduciary, fee-only), have the team depth to manage complex multi-asset portfolios, and can coordinate across tax, legal, and estate requirements — not just recommend products.

What is the difference between a SEBI-registered investment adviser and a regular financial advisor in India?

A SEBI RIA is legally bound to act as a fiduciary under Regulation 15(1) — they cannot earn commissions and must disclose all conflicts of interest. A mutual fund distributor (ARN holder) may earn product-based commissions from fund houses, which can create conflicts between their recommendations and your outcomes. The regulatory status is the most important filter when evaluating any financial professional.